Basics of fund accounting: A concise guide for churches

Discover basics of fund accounting for churches with a concise, practical guide. Learn core concepts, examples, and tools to improve stewardship and clarity.

Fund accounting is a way of organizing a church's finances that treats different pots of money completely separately based on their intended purpose. Think of it as a set of digital envelopes. This system ensures every dollar given for a specific reason—like missions or a new building—is used exactly as the donor intended. It's the single biggest difference between how a church handles its books and how a for-profit business does.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

Why Fund Accounting is the Language of Stewardship

Remember the old-school envelope system for managing household budgets? You’d have one envelope for groceries, another for the mortgage, and a special one you’d tuck cash into for the family vacation. Money in the vacation envelope was off-limits for anything else. That’s precisely how fund accounting works for a church, just with digital ledgers instead of paper envelopes.

This approach is so much more than just good bookkeeping; it’s a tangible expression of stewardship and transparency.

Unlike a typical business, where the main goal is turning a profit for shareholders, a church’s financial priority is accountability to its donors and congregation. The end game isn't measuring profitability. It’s about demonstrating faithful management of the resources God has provided through his people. This makes every financial report a testament to the church’s integrity and its commitment to the mission.

Let's quickly compare the two mindsets. This table breaks down the core differences between how a church approaches its finances versus a standard business.

Fund Accounting vs For-Profit Accounting at a Glance

| Aspect | Fund Accounting (For Churches) | For-Profit Accounting |

|---|---|---|

| Primary Goal | Demonstrate accountability and stewardship of resources. | Maximize profit and return on investment for owners/shareholders. |

| Focus | Tracking resources by their designated purpose or restriction. | Measuring overall profitability and financial performance. |

| Key Financial Statement | Statement of Activities (shows changes in different funds). | Income Statement (Profit & Loss). |

| Core Question Answered | "Did we use the funds as intended?" | "Did we make a profit?" |

| "Bottom Line" | Net Assets (categorized by restriction). | Net Income or Net Profit. |

As you can see, the entire philosophy is different. It's a shift from profit to purpose.

Accountability Over Profitability

The fundamental distinction comes down to the "why." A business uses its financial statements to show how much money it made. A church uses its reports to prove it honored its commitments. This is a critical shift for building and maintaining trust. When a church member sees that their specific gift to the building fund or the summer mission trip was used only for that purpose, their confidence in the church's leadership skyrockets.

Fund accounting is the cornerstone of church financial management, ensuring that every dollar is tracked precisely according to its designated purpose—whether for general operations, missions, building funds, or restricted donations. This method differs from standard commercial accounting by maintaining separate 'funds' for each revenue stream and expenditure category, preventing commingling of resources and guaranteeing accountability. You can learn more about the principles of church financial oversight on holycrossarmenian.com.

This system gives you a clear and honest framework for financial integrity. It directly answers the two questions every donor is asking, whether they say it out loud or not: "Was my gift used wisely?" and "Did my donation actually support the cause I intended?" By keeping funds separate, you can confidently and truthfully answer "yes" to both.

The Benefits of a Fund-Based Approach

Moving to a true fund accounting system isn't just a technical upgrade; it’s a ministry tool that strengthens a church's financial health and its relationships with the congregation.

Here are a few of the immediate wins:

- Enhanced Transparency: You can produce clear, detailed reports that show exactly how different ministry areas are funded and where the money is going. No more guesswork.

- Improved Donor Confidence: When people know their designated gifts are protected and used correctly, they are far more likely to give generously and consistently. Trust is the currency of generosity.

- Legal and Ethical Compliance: This system helps ensure the church meets its legal obligations for restricted donations, preventing the misuse of funds that could land you in serious trouble.

- Better Decision-Making: Leadership gets a real-time view of the financial health of each individual fund. This allows for smarter strategic planning and better resource allocation across all your ministries.

Ultimately, getting a handle on fund accounting helps your church build a powerful foundation of trust, proving that good stewardship is at the heart of everything you do.

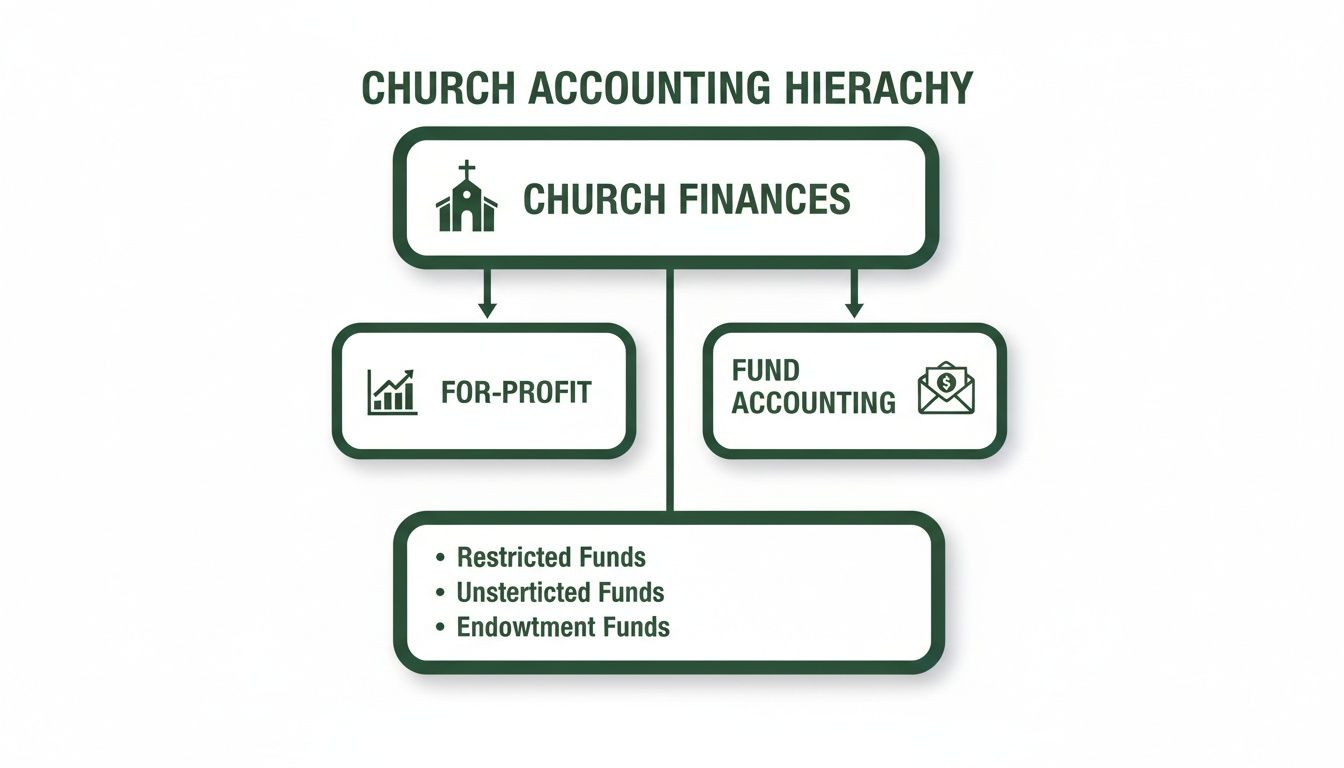

Understanding the Core Pillars of Church Fund Accounting

To be good stewards of the resources God provides, church leaders first need to get a handle on the concepts that make fund accounting so different. This isn't just another way to organize the books; it's a system built from the ground up for financial integrity. It works by sorting every dollar according to its intended ministry purpose. Mastering these ideas is the first real step toward building and keeping the trust of your congregation.

The flowchart below shows how fund accounting is a specialized system designed for accountability, setting it apart from the profit-driven model you see in the business world.

As you can see, while both approaches fall under financial management, they have completely different end goals. Fund accounting is all about tracking purpose, not profit.

The Different Types of Funds in a Church

The easiest way to think about funds is as separate financial "buckets." Each bucket holds money that's been set aside for a specific part of your church's mission. While every church is a little different, most operate with a few common fund types.

- The General Fund: This is the operational heart of your church. It’s where all unrestricted tithes and offerings land, and it’s what you use to pay for the day-to-day work of ministry—things like staff salaries, utility bills, Sunday School curriculum, and building maintenance.

- Mission Fund: This bucket is specifically for supporting local and global missions. When someone gives to "Missions," their donation goes right here and can only be used to support missionaries or specific outreach projects.

- Building Fund: Often tied to a capital campaign, this fund is for collecting money for big projects like new construction, a major renovation, or buying a new property.

- Benevolence Fund: This fund is set aside to provide direct financial help to people in your congregation or community who are going through a tough time.

Keeping these funds totally separate is non-negotiable. It’s what prevents money donated for a youth mission trip from accidentally being used to pay the electric bill—a mistake that can seriously damage trust.

Unrestricted vs. Restricted Funds: A Critical Distinction

If there’s one concept you absolutely must understand in fund accounting, it’s the difference between restricted and unrestricted funds. Every single dollar your church receives falls into one of these two categories, which directly controls how you’re allowed to use it.

A fund's restriction is determined by the donor, not the church. Honoring these restrictions is an ethical and often legal obligation that forms the foundation of donor trust.

Unrestricted Funds are donations given without any strings attached. The cash and checks dropped into the offering plate on a typical Sunday are a perfect example. Church leadership has the discretion to use this money for any legitimate ministry need, which is why it almost always goes into the General Fund.

Restricted Funds, on the other hand, are gifts given for a very specific purpose that the donor spells out. This is where things like designated giving envelopes or online giving drop-down menus become so important. There are two main kinds of restrictions:

- Temporarily Restricted: These funds are earmarked for a specific project or purpose that has a finish line. A donation to the "Youth Summer Camp" or a gift for the "New Roof Campaign" is temporarily restricted. Once the camp is over or the new roof is paid for, any leftover money might become unrestricted, but that depends on the donor's original instructions.

- Permanently Restricted: This is less common for most churches but is often seen with endowments. A donor might give a large sum with the legal requirement that the original amount (the principal) can never be spent. Instead, the church can only use the interest or investment income from that principal, often for a specific, ongoing purpose like a scholarship program.

Your Financial Roadmap: The Chart of Funds

So, how do you keep all these funds and their restrictions straight? You do it with a Chart of Funds, which essentially serves as your church's financial roadmap. Think of it as a master list that directs every single transaction into the correct bucket.

This goes a step beyond a standard chart of accounts. A well-designed chart of funds ensures that when a check comes in with "Missions" written on the memo line, your accounting system knows precisely which fund to credit. You can learn more about creating one in our detailed guide on the nonprofit chart of accounts. Getting this structure right from the start is what makes generating accurate, trustworthy financial reports possible.

Putting Fund Accounting into Practice with Journal Entries

Theory is great, but let's be honest—it all starts to make sense when you see the money move. To truly get a feel for fund accounting, we need to look at the day-to-day transactions your church handles. We'll use simple journal entries, the basic debits and credits, to bring these concepts to life.

Just think of debits and credits like two sides of a scale. For every transaction, one account gets a debit and another gets a credit for the exact same amount. It’s a simple system that keeps your books perfectly balanced.

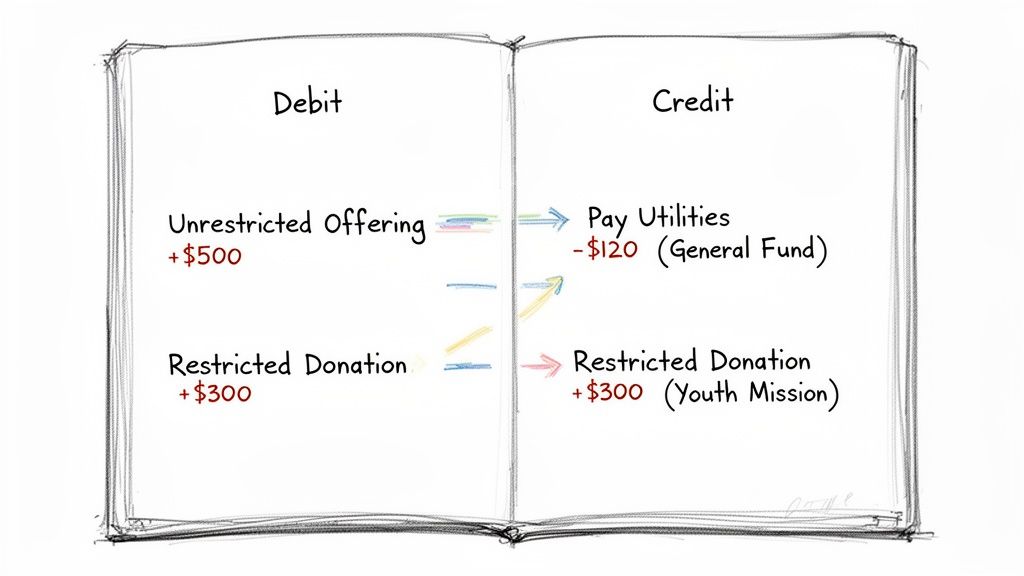

Example 1: The Everyday Stuff—Offerings and Bills

This is the bread and butter of church finance. The offering plate comes in, and the light bill needs to be paid. Both of these activities live inside your General Fund.

Scenario A: Recording the Sunday Offering

Let's say your church receives $5,000 in tithes and offerings during the service, with no specific designations.

- Debit: Cash goes up by $5,000. Think of this as money coming into your bank account.

- Credit: General Fund Income also goes up by $5,000. This entry shows why the money came in—it was from general giving.

Scenario B: Paying the Electric Bill

Now, the church writes a check for $450 to the power company.

- Debit: General Fund Expenses increases by $450. This records what the money was spent on—a utility bill.

- Credit: Cash decreases by $450. This shows the money going out of your bank account.

See how simple that is? Both transactions happened entirely within the General Fund. No restricted money was touched.

Example 2: When a Gift Comes with Strings Attached

Now for the important part: a designated donation. This is where fund accounting really proves its worth in building and keeping donor trust.

Scenario: A family gives your church a $1,000 check. The memo line is clear: "For Youth Missions."

- Debit: Cash increases by $1,000. The money landed in your bank account, plain and simple.

- Credit: Youth Mission Trip Fund Income increases by $1,000. This is the key. Instead of crediting your general income, you credit the specific, restricted fund. You’ve just put a virtual fence around that $1,000.

This single entry is the heart of stewardship. It’s a recorded promise to the donor, creating a clear trail that shows you are honoring their wishes.

Example 3: Spending Restricted Money the Right Way

Finally, we close the loop. Let's spend that designated money correctly to fulfill the donor's original intent.

Scenario: It’s time to book flights for the mission trip. The church pays $750 for airline tickets.

- Debit: Youth Mission Trip Fund Expense goes up by $750. The expense is logged directly against the mission trip fund, not the general budget.

- Credit: Cash goes down by $750. The money has left the bank to pay the airline.

After this, the Youth Mission Trip Fund has $250 left ($1,000 donation - $750 expense) for other trip-related costs. The fund’s integrity is intact, the donor is honored, and your financial reporting is spotless.

Getting these flows right is crucial, especially when money needs to move between different funds. For a deeper dive into that, check out our guide on fund-to-fund accounting transfers.

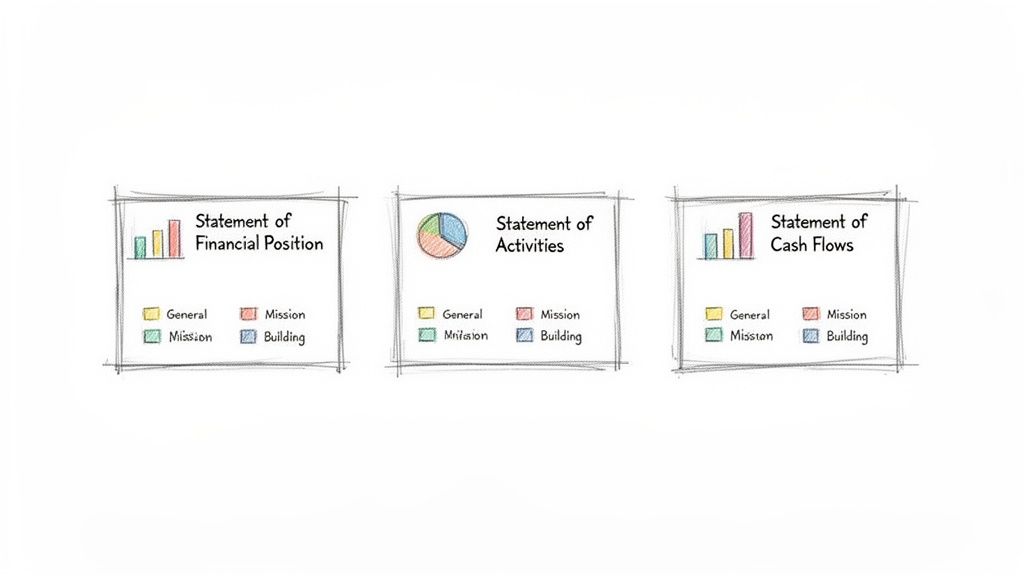

The Financial Reports That Build Trust and Transparency

Think of your journal entries as the individual bricks. Financial reports are the actual house you build with them—they show everyone the complete picture of your church's financial health and, more importantly, its stewardship. For any church leader, getting comfortable with a few key reports is the secret to making sound decisions and communicating with absolute clarity.

These aren't just documents for the finance committee; they're genuine ministry tools. They answer the one question every donor has: "Is the church being a good steward of the resources it has been given?"

This is where fund accounting truly shines. You can run reports for each individual fund, not just a single, church-wide summary. An overall report might make it look like the church is in great shape, but that could be masking a serious cash shortfall in your General Fund that’s being propped up by a massive, restricted Building Fund. That kind of fund-level detail is absolutely essential for real accountability.

The Statement of Financial Position

You might know this as a balance sheet. It’s a snapshot of your church's finances on a specific day. It clearly answers three questions: "What do we own, what do we owe, and what's left over?"

- Assets: This is everything the church owns that has value. Think cash in the bank, property, vehicles, and equipment.

- Liabilities: This is what the church owes to others. Common examples include a mortgage, outstanding loans, or bills that need to be paid.

- Net Assets: This is simply the difference between your assets and liabilities. In fund accounting, this is broken down by restriction (unrestricted, with donor restrictions, etc.) to show exactly what's available for general ministry.

A pastor can glance at this report and immediately see the total cash on hand versus the balance of the restricted Missions Fund, preventing designated money from being spent on the wrong things.

The Statement of Activities

This is probably the most powerful report in church fund accounting. It’s a lot like a for-profit income statement, but its focus is on mission, not profit. It details all the income and expenses over a period—like a month or a full year—and breaks it all down by fund.

The Statement of Activities is a direct reflection of your stewardship. It proves to donors that the money they gave to the Benevolence Fund was actually used to help families in need, not to cover administrative salaries.

For instance, your leadership board can look at the General Fund's income versus its expenses to check on the church's operational health. At the same time, they can review the Building Fund’s activity to see how close you are to reaching that capital campaign goal.

The Statement of Cash Flows

This report is all about the movement of money. It shows how cash has come into and gone out of the church, separating it into three key areas: operating activities (tithes, salaries), investing activities (buying or selling a church van), and financing activities (making loan payments).

It helps answer those tricky questions like, "Our report says we had a surplus, so why is the bank account so low?" It brings a ton of clarity to your cash management, making sure you always have enough liquid funds to meet payroll and pay the bills on time.

Transparency and regular reporting are the bedrock of fund accounting basics. They cultivate a culture of trust in your finance team. We've seen that churches providing detailed, fund-specific monthly statements experience higher engagement, especially as donors increasingly want to see how their designated gifts are used. This trend toward directed giving has seen significant growth, a topic you can explore further in these church giving trends on Vancopayments.com. When your congregation sees exactly how their generosity fuels the mission, their confidence—and their willingness to give—naturally grows with it.

Avoiding Common Pitfalls in Church Accounting

Getting fund accounting right is a ministry of integrity. But even churches with the best intentions can stumble into financial mistakes that, unfortunately, erode the very trust they’ve worked so hard to build. Staying aware of these common pitfalls is crucial for maintaining both financial health and your congregation's confidence. A little forethought and some solid processes are your best defense against errors that can cause real headaches down the road.

One of the most common—and most damaging—errors is commingling funds. This is just a formal way of saying money designated for one purpose gets used for something else, even if it's just for a little while. Think of it like raiding your kids' college savings jar to pay this month's electric bill. You fully intend to pay it back, but in that moment, you've broken a promise.

The Dangers of Commingling Funds

Most of the time, commingling isn't malicious. It’s often a response to a cash flow crunch. For example, the General Fund might be running low, so someone "borrows" from the restricted Building Fund to cover payroll, fully planning to replace it when the next big offering comes in.

But this creates a few serious problems:

- It breaks donor trust. When a member finds out their designated gift for the youth mission trip was used to patch a leaky roof, their confidence can be shattered.

- It creates misleading reports. Your financial statements won't show the true story. They might hide a critical shortfall in your operating budget, making everything look fine when it isn't.

- It can have legal consequences. In the case of legally restricted funds, misusing them can lead to serious compliance issues.

The solution is simple in principle, though it requires discipline: maintain completely separate accounting for each fund. Every single transaction has to be recorded against the specific fund it belongs to. No exceptions.

The core principle of stewardship in fund accounting is that a restriction placed by a donor is a promise that must be honored. Commingling funds, even with good intentions, undermines this foundational promise and weakens financial integrity.

Inadequate Tracking and Poor Reporting

Another pitfall we see all the time is failing to track restricted gifts with enough detail. Just noting a donation as "for missions" is asking for trouble later. Was it for the Smiths in Uganda, the upcoming short-term trip to Mexico, or the general missions budget? Without that specificity, it’s easy for funds to get misallocated.

Just as problematic is generating reports that don't break things down by fund. A single, consolidated financial report for the whole church can be incredibly deceptive. It might show a healthy overall bank balance, but that could be masking a General Fund that's deep in the red, propped up only by a massive, restricted building campaign fund. Leadership can't make wise decisions without seeing the real financial position of each fund individually.

Establishing Strong Internal Controls

The best way to sidestep these issues is to establish strong internal controls. These are simply the policies and procedures you put in place to protect the church's assets and ensure your numbers are accurate. This isn't about a lack of trust; it's about a commitment to accountability and good stewardship.

Here are a few essential controls every church should have:

- Require Dual Signatures: Any check over a certain amount (say, $500) should require signatures from two unrelated people.

- Conduct Regular Reviews: Your finance committee or elder board should be looking at detailed, fund-level financial reports every single month.

- Separate Financial Duties: The person who counts the offering should never be the same person who records the deposits or reconciles the bank statements. This is often called "separation of duties."

These are simple, practical steps, but they build a powerful framework of accountability. They send a clear message to your congregation that you take the stewardship of their gifts seriously, protecting both the church’s finances and its reputation.

Streamlining Your Finances with True Fund Accounting Software

Understanding the theory of fund accounting is one thing. Actually putting it into practice day in and day out is a whole different ballgame. While paper ledgers are long gone, many churches still find themselves wrestling with generic business software like QuickBooks, trying to make it fit their very unique financial world.

That approach usually involves a maze of complicated, error-prone workarounds. Church administrators end up jury-rigging the system with classes or tags to mimic fund tracking, which creates a fragile setup that can break at any moment. All it takes is one miscategorized transaction to throw your reports into chaos, compromise a restricted fund, and completely undermine the accountability you're working so hard to maintain.

The Power of a True Fund-Based System

Instead of forcing a square peg into a round hole, churches need a tool built from the ground up for how they actually operate. This is where true fund accounting software makes all the difference. It’s designed from its very core to handle the specific needs of church and nonprofit finance automatically.

A true fund-based system isn’t just business software with a few features tacked on. Its entire architecture is built around the concept of separate, self-balancing funds. This fundamental difference completely changes how you manage your money, shifting you from constant manual oversight to automated, confident stewardship.

The real beauty of a purpose-built system is that it makes doing the right thing the easy thing. It naturally enforces the rules of fund accounting, so compliance and transparency are simply part of your daily workflow, not a stressful afterthought.

Grain Ledger: A Solution Built for Churches

For churches just getting their arms around the basics of fund accounting, the best tool is one that speaks their financial language. Grain Ledger was designed specifically for this reality. Its native fund architecture means that every single donation, expense, and report is automatically tied to the correct fund from the moment it happens.

Here’s a quick look at the Grain Ledger interface, which is built to give you a clear, fund-centric view of your church’s finances.

This dashboard instantly shows you how your resources are allocated across different funds—a stark contrast to the jumbled, consolidated views you get from generic accounting software.

This design completely eliminates the need for manual tracking in spreadsheets and the constant worry of accidentally mixing funds. When a designated donation for the building campaign comes in, it flows directly into that restricted fund. When you pay a missionary, the expense is drawn from the missions fund balance. The system maintains the integrity of each fund for you, making stewardship simpler and far more accurate.

The benefits are immediate and profound:

- Automated Accuracy: Donations from your online giving platform are automatically routed into the correct funds, which drastically reduces the chance of human error.

- Instant Reporting: You can generate fund-level reports—like a Statement of Activities just for the Youth Fund—with a single click. No more exporting data to Excel to manually build the reports your board is asking for.

- Built-in Controls: The system inherently protects restricted money, putting up guardrails that prevent you from accidentally spending designated funds on general operating expenses.

- Enhanced Trust: Armed with clear, accurate, and transparent reports, you can confidently demonstrate faithful stewardship to your pastor, your board, and your entire congregation.

By adopting a tool that was actually built for your ministry’s needs, you can finally move beyond just managing transactions. You can focus on what truly matters: fueling your mission with complete financial integrity. To learn more, check out our complete guide to fund accounting software for churches. It provides a deeper look at how the right tools can change everything.

Answering Your Top Questions About Church Fund Accounting

When you're new to fund accounting, a few questions always seem to pop up. It's totally normal. Getting these fundamentals right is the first step toward building a rock-solid financial foundation for your ministry. Let's tackle some of the most common ones we hear from church leaders.

Can We Just Use Regular Business Accounting Software?

You could, but it would be like trying to fit a square peg in a round hole. You'd be fighting the software every step of the way with manual spreadsheets and complicated workarounds.

Standard business software is built to track one thing: overall profit. But a church isn’t focused on profit; it’s focused on stewardship. True fund accounting software is designed from the ground up to track separate pots of money—restricted and unrestricted funds—automatically. A purpose-built tool like Grain Ledger makes financial integrity the default, not a chore.

What's the Single Most Important Report We Should Look At?

If you could only have one report, it would be the Statement of Activities by Fund. While a standard balance sheet gives you the 30,000-foot view of the church's overall health, this report gets down to the details that truly matter for stewardship. It breaks down the income and expenses for each individual fund—your General Fund, Missions, Building Campaign, etc.

This is the report that answers the ultimate accountability question: "Did we honor our donors' intentions and use their gifts as they were designated?" It’s the key to giving your pastor, your board, and your congregation real peace of mind.

How Do We Handle a Donation That's Split Between Two Funds?

This happens all the time! Someone writes a single check for $500 and puts "$300 for General Fund and $200 for Missions" on the memo line. The key is that you have to split the transaction on the back end.

Your books will show the full $500 coming into your bank account. But when you record the income, you'll credit $300 to the General Fund and $200 to the Missions Fund. A good fund accounting system makes this incredibly easy, ensuring every dollar is tracked to the right fund from the moment it comes in. This simple step is crucial for maintaining transparency and honoring the donor's wishes.

Ready to manage your church’s finances with the clarity and confidence your ministry deserves? Grain Ledger offers true, native fund accounting designed to support your stewardship mission. See how you can automate fund tracking, simplify reporting, and build trust with your congregation by visiting our website.

Ready to simplify your church finances?

Schedule a demo to see Grain Ledger in action, or sign up for product updates.