The Ultimate 10-Point Checklist for Auditors: A 2026 Church…

Discover our comprehensive 2026 checklist for auditors focused on church finances. Ensure compliance, accuracy, and stewardship with these essential steps.

An effective church audit goes beyond simple number-crunching; it's a vital process that builds trust, ensures accountability, and protects the ministry's mission. For both internal audit committees and external auditors, a generic approach can miss the unique complexities of church finance, such as nuanced fund accounting, donor-imposed restrictions, and specialized payroll for ministry staff. A generic checklist for auditors often fails to address the specific stewardship responsibilities inherent in managing tithes, offerings, and designated gifts.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

This definitive guide is specifically designed for the church environment. It provides a clear, actionable roadmap to verify financial integrity, strengthen internal controls, and confirm that every dollar is stewarded according to its intended purpose. Instead of vague advice, you will find concrete steps to navigate the intricacies of ministry finance, from reconciling fund balances to validating grant compliance. For churches seeking true fund accounting, implementing a robust system like Grain Ledger alongside this checklist creates a powerful framework for transparency and accuracy.

We will explore ten critical areas in detail, offering practical examples and specific documentation to review. This comprehensive checklist for auditors will equip your finance committee, treasurer, or external reviewer to conduct a thorough and meaningful assessment. The goal is not just to check boxes but to foster deep congregational confidence in your financial operations, ensuring the ministry's resources are secure and effectively managed to fulfill its calling. Following this structured approach transforms the audit from a procedural requirement into a strategic tool for enhancing stewardship and operational health.

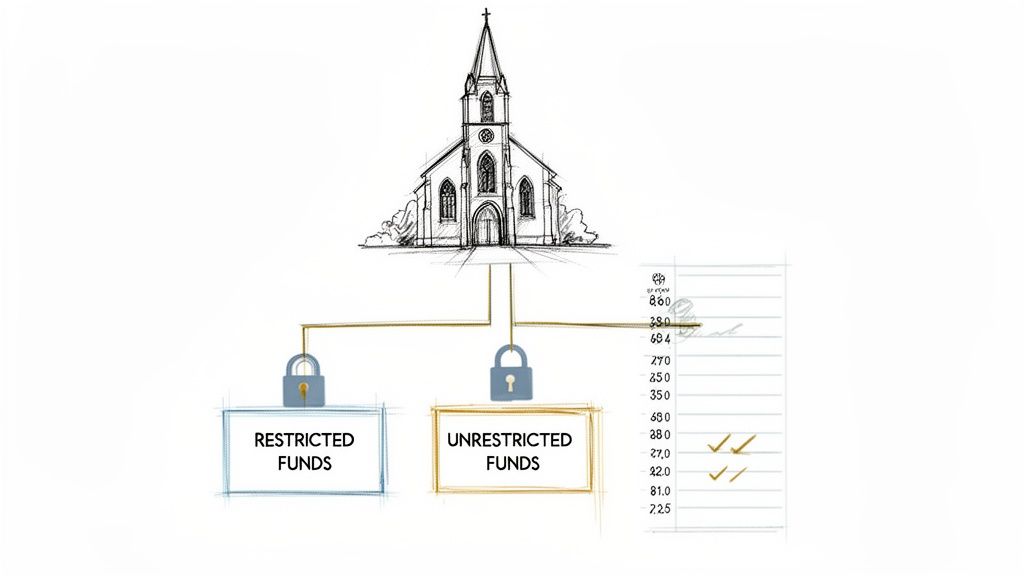

1. Fund Structure and Restricted Fund Compliance

A church’s financial health and integrity are built on a foundation of true fund accounting. This critical audit point involves verifying that the church’s fund structure is not only accurate but also strategically aligned with its ministry priorities. It also includes a rigorous review to ensure all restricted donations were used exclusively for their designated purposes, maintaining donor trust and legal compliance. This step is a cornerstone of any effective checklist for auditors because it directly addresses the stewardship of funds given for specific ministry work.

The audit process must confirm that the accounting system can properly segregate and track different types of funds, such as the general fund, building fund, missions fund, and benevolence fund. Without this capability, it is nearly impossible to prove that a $5,000 gift for a youth retreat wasn't accidentally used to cover general operating expenses. Modern systems like Grain Ledger are designed to enforce these boundaries, preventing unauthorized transfers and providing a clear audit trail.

Why This Audit Point is Crucial

Proper fund management is non-negotiable for nonprofit organizations. The Financial Accounting Standards Board (FASB) and IRS Form 990 instructions mandate clear distinctions between assets with and without donor restrictions. A failure to comply can lead to legal repercussions, loss of donor confidence, and a tarnished public reputation. For example, an audit might reveal that a capital campaign fund was never properly established as a separate entity in legacy software, commingling it with general offerings. Implementing a true fund accounting system like Grain Ledger rectifies this by establishing a compliant fund architecture from the start.

Actionable Audit Steps

- Request Fund Documentation: Obtain the official list of all church funds, including their stated purpose, from the finance team and pastoral leadership.

- Create a Restricted Funds Register: Document the purpose, specific restrictions, and authorized uses for every restricted fund.

- Validate Fund Alignment: Compare the fund structure against the church's strategic plan and ministry goals to ensure they match.

- Review Spending Authority: Establish and verify clear spending authority policies, especially for restricted fund expenditures that may require board approval.

- Confirm System Controls: Ensure your accounting software prevents unauthorized transfers from restricted funds. A platform like Grain Ledger can enforce these controls systemically, providing a critical layer of security.

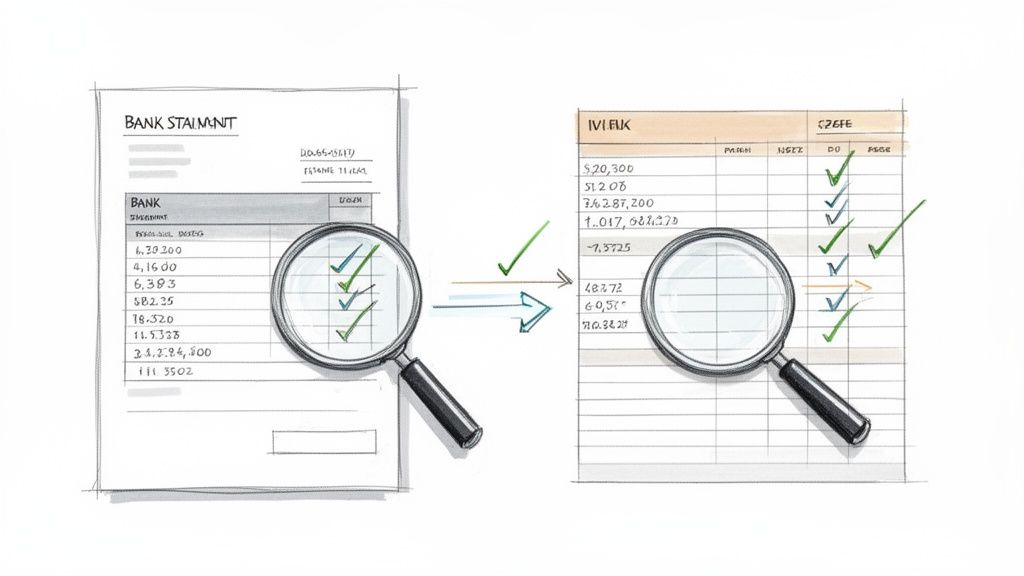

2. Reconcile Bank Accounts to Accounting Records

A rigorous reconciliation of all church bank accounts against the general ledger is a fundamental audit procedure. This involves a detailed comparison of every deposit, withdrawal, and bank fee to ensure they are accurately recorded and that no unauthorized transactions have occurred. For churches, where financial transparency is paramount, this step validates the accuracy of cash balances and serves as a powerful fraud detection tool. This verification process is an indispensable part of any checklist for auditors because it confirms that the church's most liquid asset, cash, is correctly stated and securely managed.

The audit must confirm that a systematic reconciliation process is in place for all accounts, including operating, savings, and any money market accounts. For instance, a church treasurer performing monthly reconciliations might identify $500 in unauthorized wire transfers, preventing further fraud. In organizations using modern accounting software like Grain Ledger, which integrates directly with bank feeds via Plaid, the audit should also validate these automated connections and review any manual adjustments for proper approval and documentation.

Why This Audit Point is Crucial

Accurate cash reporting is non-negotiable for maintaining financial integrity. As highlighted by AICPA audit standards, the process of Bank Reconciliation is critical for verifying cash balances and identifying errors or irregularities in a timely manner. Without it, a church could operate with a flawed understanding of its cash position, leading to bounced checks or overdrafts. For example, a multi-location church might find a $3,400 timing difference between its internal transfer records and the actual bank posting dates, a discrepancy that only a thorough reconciliation would uncover. Systems like Grain Ledger can flag such discrepancies almost immediately, shrinking the window for financial errors to go unnoticed.

Actionable Audit Steps

- Request Bank Statements: Obtain complete, original bank statements for every church bank account for the entire audit period.

- Verify Reconciliation Reports: Review the church's monthly bank reconciliation reports, ensuring they are completed, reviewed, and signed off on by a separate individual.

- Investigate Reconciling Items: Scrutinize all outstanding checks, deposits in transit, and other reconciling items to ensure they are valid and clear in the subsequent period.

- Confirm Automated Connections: If using a system like Grain Ledger, verify that automated bank feeds successfully imported all transactions without duplication or omission.

- Test Segregation of Duties: Confirm that the person responsible for recording cash transactions is not the same person performing and approving the bank reconciliation.

3. Test Donation Recording and Fund Allocation Accuracy

The integrity of a church's financial statements begins the moment a donation is made. This audit point involves testing a representative sample of donations to verify they were recorded accurately, allocated to the correct funds, and processed properly through integrated giving platforms like Pushpay or Planning Center. It ensures that automated workflows are functioning as intended and that donor intent, especially for restricted gifts, is honored from the initial transaction to the final ledger entry. This test is a vital part of any checklist for auditors as it validates the accuracy of the entire revenue stream.

An audit must trace donations from their source, whether it's an online form, a mobile app, or a physical offering envelope. For instance, an audit of 50 Pushpay donations might reveal that 8% were incorrectly coded due to a mapping error between giving categories and the church’s fund codes. This highlights the need for a tightly integrated system like Grain Ledger, which ensures that automated flows from platforms like Planning Center are perfectly aligned, eliminating the risk of manual errors and providing a transparent, verifiable transaction history.

Why This Audit Point is Crucial

Mistakes in donation recording can quickly erode donor trust and create significant compliance issues. If a capital campaign donation is mistakenly recorded in the general fund, it misrepresents the church's financial position and violates the donor’s restriction. This can happen due to poor integration between giving and accounting software, requiring manual data entry that introduces human error. A system like Grain Ledger prevents this by establishing a direct, automated link, ensuring a gift designated for the “Building Fund” in the giving platform is recorded identically in the accounting ledger, with no manual intervention needed.

Actionable Audit Steps

- Develop a Donation Testing Matrix: Create a plan to sample donations from all giving channels, including online, mobile app, text-to-give, and in-person offerings.

- Compare Platform and Ledger Reports: Request transaction reports from all giving platforms and compare them line-by-line against the church's accounting records.

- Test Designated and Undesignated Gifts: Include a mix of both restricted (e.g., missions, benevolence) and unrestricted (general fund) donations in your sample.

- Verify Donor Intent: Check that any notes or fund designations made by donors in the giving platform are accurately reflected in the final accounting entry.

- Review Manual Adjustments: Document and investigate any manual corrections made after automated processing, as they may indicate a systemic integration problem that needs to be addressed within a system like Grain Ledger.

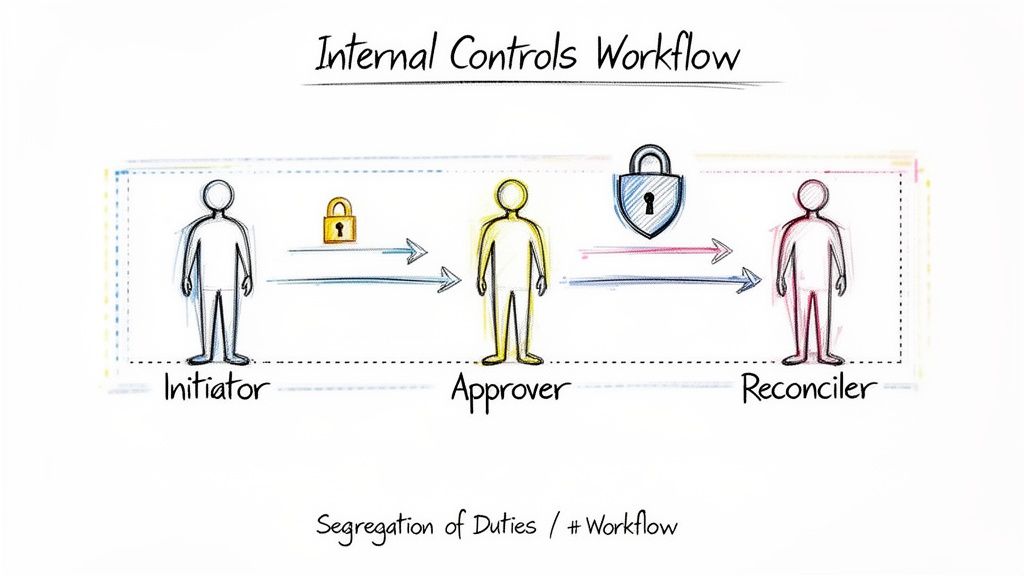

4. Review Internal Controls and Segregation of Duties

A church’s financial integrity depends on robust internal controls designed to prevent fraud, error, and mismanagement. This audit point examines the design and effectiveness of controls for key processes like donations, fund transfers, and expenditure approvals. A critical component is evaluating the segregation of duties, ensuring that no single individual controls an entire financial transaction from initiation to reconciliation. This review is a vital part of any checklist for auditors as it addresses the operational safeguards protecting ministry assets.

The audit must assess if separate individuals are responsible for initiating, approving, recording, and reconciling financial activities. In many churches, especially smaller ones, perfect segregation isn't feasible due to limited staff. In these cases, the focus shifts to identifying and testing compensating controls. For instance, if a treasurer records deposits and also reconciles bank statements, a compensating control would be to have a board member or finance committee member review the reconciliation monthly.

Why This Audit Point is Crucial

Strong internal controls, popularized by frameworks like COSO, are the first line of defense against financial misconduct. Without proper segregation of duties, the risk of unauthorized spending or theft increases dramatically. An audit might find that one staff member can approve a large purchase, record the expense, and reconcile the associated bank account, creating a significant vulnerability. Implementing a system like Grain Ledger allows churches to configure user roles and permissions that systemically enforce these separations, preventing a single person from both approving and recording significant fund transfers. This provides a digital backstop that supports procedural controls.

Actionable Audit Steps

- Document Key Processes: Create flowcharts for major financial cycles (e.g., offering collection, bill payment) to visualize control points and responsibilities.

- Define and Assign Roles: Review written job descriptions for the finance team to ensure duties are clearly defined and segregated.

- Establish Approval Thresholds: Verify that the church has a formal policy requiring multiple signatures or approvals for expenditures over a certain amount.

- Configure System Access Controls: Test the accounting software’s user permissions. In Grain Ledger, confirm that roles are set up to enforce segregation of duties digitally.

- Identify Compensating Controls: Where segregation is not possible, document the compensating controls in place, such as finance committee oversight or board member review of bank reconciliations.

5. Reconcile Giving Records to Donation Acknowledgment and Tax Records

Accurate and timely donor acknowledgments are a matter of both integrity and legal necessity. This audit point involves a detailed reconciliation of giving records, acknowledgment letters, and year-end tax statements. The goal is to verify that every donation is accurately recorded, properly acknowledged, and correctly reported for tax purposes, ensuring donors are well-stewarded and the church remains compliant. This verification is a non-negotiable part of any checklist for auditors as it touches on donor trust, data integrity, and IRS regulations.

The audit must scrutinize the entire contribution management process, from the moment a gift is received to the issuance of the annual giving statement. This includes validating that records in the giving platform, such as Planning Center or Tithe.ly, perfectly match the entries in the accounting general ledger. For instance, an audit might uncover that 47 cash donations were never logged into the giving platform last year, meaning those donors never received proper acknowledgment. Using an integrated system like Grain Ledger automates this reconciliation, creating a direct sync between donation entries and the accounting records to eliminate such errors.

Why This Audit Point is Crucial

The IRS requires nonprofits to provide written acknowledgment for any single contribution of $250 or more before the donor can claim a charitable deduction. Failure to do so, or providing inaccurate statements, can jeopardize a donor’s tax filing and severely damage the church's credibility. An audit might reveal that a sync error between systems caused 12 donors to receive incorrect year-end statements. Catching this before distribution prevents confusion and maintains trust. Systems like Grain Ledger, with built-in giving and accounting integration, prevent these data mismatches from ever occurring.

Actionable Audit Steps

- Review Acknowledgment Policy: Obtain and review the church's policy for acknowledging donations, ensuring it meets IRS requirements and establishes a clear timeline (e.g., within two weeks of receipt).

- Sample and Test Transactions: Select a sample of donations from various sources (online, check, cash) and trace them from the giving platform through to the bank deposit and general ledger.

- Verify Year-End Statements: Reconcile the total donations reported on a sample of year-end giving statements against the detailed transaction records in the giving and accounting systems.

- Audit Non-Cash Donations: Examine the process for recording and valuing non-cash gifts, ensuring proper documentation (e.g., appraisal forms, donor letters) is on file.

- Confirm System Integration: For churches using separate platforms, verify the reconciliation process between them. An all-in-one solution like Grain Ledger will automate this and ensure 100% accuracy.

6. Test Payroll and Expense Reimbursement Accuracy and Approvals

Payroll and employee reimbursements often represent a church's largest single expense category, making them a high-risk area for errors and misuse. This audit point involves a detailed review of payroll processing and reimbursement procedures to confirm accuracy, proper authorization, and compliance with both internal policies and external regulations. It is an essential component of any checklist for auditors, as it verifies that staff are paid correctly and that ministry funds are used appropriately for legitimate expenses.

The audit process should examine everything from wage calculations and tax withholdings to benefit accruals and the documentation supporting expense claims. For example, an audit might uncover that temporary staff were not being paid overtime despite working more than 40 hours a week, exposing the church to legal risk. Similarly, sample testing of reimbursements could reveal non-business expenses, such as personal meals, being claimed. Using a system like Grain Ledger can help mitigate these risks by allowing payroll to be accurately coded to specific fund sources and ministry areas, creating a clear and traceable record.

Why This Audit Point is Crucial

Mistakes in payroll and reimbursements can lead to significant consequences, including IRS penalties for incorrect tax filings, legal action from employees, and a loss of confidence from the congregation. The IRS Employer's Tax Guide (Circular E) outlines strict requirements for payroll processing, withholding, and reporting. An audit that discovers payroll taxes were not remitted for six months requires immediate remedy and a penalty mitigation plan. A robust audit ensures these financial controls are functioning as intended, protecting the church’s resources and reputation.

Actionable Audit Steps

- Obtain Payroll Registers: Request payroll summary registers for the entire fiscal year to test transactions for accuracy and consistency.

- Validate Tax Filings: Compare year-end payroll tax forms (W-2s, 1099s) against general ledger payroll accounts to ensure they reconcile.

- Test Reimbursement Claims: Select a sample of reimbursement requests and verify they have proper documentation (receipts, business purpose) and managerial approval.

- Review Benefit Accruals: Examine employee benefit policies, such as paid time off or retirement contributions, and confirm that accruals are calculated and recorded correctly.

- Confirm Tax Deposits: Test payroll tax deposits on a monthly or quarterly basis to ensure timely and accurate remittance to federal and state authorities.

7. Audit Fixed Assets and Depreciation Schedules

A church's most significant investments, such as its building, land, and equipment, are represented as fixed assets. This audit point involves a thorough review of the fixed asset register to ensure these assets are accurately recorded, valued, and depreciated according to accounting standards. It also confirms that asset disposals are properly documented and that donated assets are recorded at fair market value. This is a vital component of any checklist for auditors as it directly impacts the accuracy of the church’s statement of financial position.

Properly tracking fixed assets is crucial for stewardship and long-term financial planning. The audit must verify that a detailed register exists and that depreciation schedules are consistently applied. For churches managing capital campaigns or building funds, it is essential that the accounting system can link assets to their corresponding fund. A system like Grain Ledger simplifies this by allowing assets purchased with restricted building fund money to be tagged and reported within that fund, ensuring the balance sheet accurately reflects fund-specific net assets.

Why This Audit Point is Crucial

According to FASB ASC 360, property, plant, and equipment must be systematically depreciated over their useful lives. Failing to record and depreciate assets properly can drastically misstate a church’s net worth, leading to poor financial decisions. For instance, a small church might discover that donated musical instruments worth thousands were never valued or recorded, understating assets. Similarly, an audit could reveal that a new roof paid for by the building fund was expensed instead of capitalized, incorrectly reducing the fund's value. Using a platform like Grain Ledger prevents these errors by integrating asset management directly with fund accounting.

Actionable Audit Steps

- Request the Fixed Asset Register: Obtain a detailed list of all fixed assets, including acquisition date, cost, depreciation method, and accumulated depreciation.

- Perform a Physical Inventory: Conduct a physical count of significant assets and compare the findings against the asset register to identify discrepancies.

- Verify Capitalization Policy: Confirm the church has a formal capitalization threshold (e.g., $1,000) and that it is applied consistently.

- Review Donated Assets: Examine records for donated assets to ensure they were recorded at their fair market value on the date of receipt, supported by an appraisal or reasonable estimate.

- Confirm Fund Alignment: Ensure your accounting system, such as Grain Ledger, correctly attributes assets to the appropriate fund (e.g., a new van purchased with missions funds is tied to the missions fund).

8. Validate Grant Compliance and Restricted Resource Usage

For churches that receive grants from foundations or government entities, this audit point is absolutely essential. It involves a meticulous review to confirm that all grant funds were used strictly according to the terms of the grant agreement. This is distinct from regular donor-restricted funds, as grants often come with formal contracts, complex reporting requirements, and specific timelines. A thorough audit here protects the church’s relationship with funders and ensures future eligibility for similar opportunities. This verification is a critical component of any comprehensive checklist for auditors.

The audit process must validate that expenses charged to a grant align perfectly with the approved budget and scope of work outlined in the grant agreement. For example, if a community development grant was awarded for a youth tutoring program, the audit must confirm funds weren’t used for general building maintenance. Using a true fund accounting system like Grain Ledger is invaluable here, as it allows you to create a separate, isolated fund for each grant. This structure prevents commingling and provides a crystal-clear financial trail for funder reports.

Why This Audit Point is Crucial

Non-compliance with grant terms can have severe consequences, including the requirement to return funds, the loss of the funding relationship, and damage to the church's reputation. Funders, especially government agencies, have a zero-tolerance policy for misallocated resources. An audit might uncover that a church receiving a federal CDBG grant failed to track and report on required outcome metrics, putting the entire program in jeopardy. By isolating each grant in a dedicated fund within Grain Ledger, a church can easily generate reports that demonstrate 100% compliance with both financial and programmatic requirements.

Actionable Audit Steps

- Review Grant Agreements: Obtain and scrutinize every active grant agreement, noting all restrictions, reporting deadlines, and compliance requirements.

- Isolate Grant Funds: Verify that a separate fund has been established in the accounting system for each individual grant to prevent commingling.

- Test Expenditure Eligibility: Select a sample of grant-funded expenditures and trace them back to supporting documentation to confirm they fall within the approved scope.

- Validate Reporting: Compare submitted grant reports against internal financial records and program data to ensure accuracy and completeness.

- Check Indirect Cost Allocations: If the grant allows for indirect costs, confirm the allocation methodology is reasonable, properly documented, and consistently applied.

9. Prepare and Review Financial Statements and Variance Analysis

The culmination of an audit is the presentation of clear, accurate, and complete financial statements. This essential point on any checklist for auditors involves verifying the church's core reports: the balance sheet, statement of activities (income statement), and statement of cash flows. It goes beyond simple number-checking to include a thorough variance analysis, comparing actual financial performance against the budget to uncover operational insights and guide strategic decisions.

Accurate reporting is critical for governance and transparency. An audit must ensure that accounting policies are sound and consistently applied, and that all account balances are rigorously tested. For example, a variance analysis might reveal that mission giving is tracking 40% below budget, prompting the board to discuss new fundraising strategies. Similarly, a proper review can identify if a large restricted donation was incorrectly classified, allowing for correction before external reporting. Systems like Grain Ledger produce fund-level balance sheets automatically, clearly segregating restricted and unrestricted net assets to dramatically improve leadership's understanding.

Why This Audit Point is Crucial

Financial statements are the primary tool for communicating a church’s financial position and stewardship to its members, board, and external stakeholders. According to FASB standards for nonprofit financial reporting, these documents must be presented in a specific format to ensure clarity and comparability. A failure to produce accurate or compliant statements can mislead leadership, erode member trust, and create significant governance challenges. Effective variance analysis transforms these reports from historical documents into forward-looking management tools, enabling proactive leadership rather than reactive problem-solving.

Actionable Audit Steps

- Create a Preparation Checklist: Develop a standardized financial statement preparation checklist to ensure consistency and completeness across all reporting periods.

- Develop a Variance Template: Design a variance analysis template that tracks key metrics by fund and ministry area, comparing actuals to budget.

- Set Investigation Thresholds: Establish clear thresholds for investigating variances (e.g., any variance over 10% or $5,000) to focus attention on significant issues.

- Include Narrative Explanations: Prepare brief, clear explanations for significant variances to provide context for the board and finance committee.

- Leverage System Reports: Implement system-generated balance sheet and cash flow reports by fund for a comprehensive view. A platform like Grain Ledger can provide these detailed reports on demand, saving significant time and reducing manual errors.

- Review with Leadership: Schedule a review of the draft financial statements with pastoral leadership and the board to ensure alignment and understanding before finalization.

10. Perform Board and Audit Committee Follow-Up and Governance Review

An audit is incomplete until its findings are communicated effectively and lead to tangible improvements. This final, critical step involves formally presenting the audit report to church leadership, establishing corrective action plans, and ensuring a continuous cycle of accountability. It transforms the audit from a historical review into a forward-looking governance tool. This makes it an indispensable part of any checklist for auditors, as it ensures the audit's findings are translated into action, strengthening the church's financial integrity.

The process bridges the gap between the technical audit work and the strategic oversight provided by the pastor, board, and audit committee. For example, presenting findings of inadequate segregation of duties could lead the board to approve a new policy and the implementation of a system like Grain Ledger that enforces user-based permissions. This closes the loop, demonstrating accountability and a commitment to stewardship that donors and members expect. A fundamental aspect of robust financial oversight, particularly when performing governance review, is understanding and implementing effective Governance, Risk, and Compliance (GRC) Systems.

Why This Audit Point is Crucial

Without a formal follow-up process, audit recommendations can be ignored, leaving critical vulnerabilities unaddressed. A structured governance review ensures that leadership understands the risks and formally accepts responsibility for remediation. This protects the church from repeated issues and demonstrates due diligence to regulatory bodies and congregants. For instance, a follow-up audit confirming that 90% of prior-year findings were remediated provides powerful evidence of strong management commitment and sound governance, building trust and confidence across the ministry.

Actionable Audit Steps

- Prepare a Formal Audit Report: Summarize procedures performed, findings, and concrete recommendations. Rate findings by severity (e.g., Critical, High, Medium, Low) to prioritize action.

- Request a Management Response: For each finding, ask leadership to document the specific corrective actions they will take, who is responsible, and the expected completion date.

- Present Findings Constructively: Frame the discussion around improvement and risk mitigation rather than blame. Focus on strengthening controls for the future.

- Document Board Acceptance: Record the board's official acceptance of the audit report and their approval of the proposed corrective action plan in the meeting minutes.

- Schedule Follow-Up Verification: Establish a clear timeline to verify that corrective actions have been implemented successfully, ensuring the audit process drives lasting change.

10-Point Auditor Checklist Comparison

| Item | 🔄 Implementation complexity | ⚡ Resource requirements | 📊 Expected outcomes | 💡 Ideal use cases | ⭐ Key advantages |

|---|---|---|---|---|---|

| Fund Structure and Restricted Fund Compliance | High — comprehensive fund mapping, policy review, sampling | High — finance time, board interviews, system (Grain) config | Clear fund separation; legal & donor compliance; reliable reports | Churches with many restricted funds, legacy systems, campaigns | ⭐ Prevents commingling; ensures legal/donor compliance |

| Reconcile Bank Accounts to Accounting Records | Medium — monthly reconciliations + exception follow-up | Medium — bank access, reconciliation tools (Plaid/Grian) | Accurate cash position; early fraud detection | Organizations needing cash accuracy and fraud controls | ⭐ Rapid detection of unauthorized transactions |

| Test Donation Recording and Fund Allocation Accuracy | Medium-High — sampling across giving platforms, tracebacks | Medium — access to giving platforms, reporting extracts | Ensures donor intent honored; correct fund allocations | Churches using multiple giving platforms (Pushpay, Stripe) | ⭐ Validates automated flows; protects donor intent |

| Review Internal Controls and Segregation of Duties | High — process documentation, control testing, role review | Medium-High — staff interviews, system role setup, governance input | Reduced fraud risk; clearer responsibilities; compensating controls | Small to mid churches needing governance or before system rollout | ⭐ Strengthens fraud prevention and accountability |

| Reconcile Giving Records to Donation Acknowledgment and Tax Records | Medium — record comparisons and year‑end statement testing | Medium — giving data, admin coordination, statement tools | Accurate donor statements; tax compliance; donor trust | Year‑end reporting periods and donor stewardship programs | ⭐ Ensures correct tax documentation and donor confidence |

| Test Payroll and Expense Reimbursement Accuracy and Approvals | Medium-High — payroll register tests, tax remittance checks | High — confidential payroll records, possibly payroll processor | Correct wages/taxes; fewer payroll errors and penalties | Churches with employees, multiple pay types, outsourced payroll | ⭐ Protects from tax penalties; ensures employee accuracy |

| Audit Fixed Assets and Depreciation Schedules | Medium — physical inventory, depreciation recalcs | Medium — asset tagging, historical docs, appraisals for donated items | Accurate balance sheet; informed capital planning | Churches with property, donations, or capital projects | ⭐ Improves asset tracking and insurance/valuation accuracy |

| Validate Grant Compliance and Restricted Resource Usage | High — contract review, expenditure testing, reporting checks | High — grant docs, program records, specialized expertise | Continued funding; compliant reporting; reduced liability | Churches receiving public or restricted grants | ⭐ Protects funding continuity and demonstrates stewardship |

| Prepare and Review Financial Statements and Variance Analysis | High — account testing, disclosures, budget variance prep | High — ledger access, budget data, prep time for narratives | Reliable financials for board; operational insights from variances | Governance reporting, board reviews, external reporting needs | ⭐ Supports governance with accurate, fund‑level reports |

| Perform Board and Audit Committee Follow-Up and Governance Review | Medium — reporting, action plans, follow‑up scheduling | Medium — audit report prep, meeting time, tracking tools | Closed audit loop; documented remediation and accountability | After audits or major control findings; governance improvement | ⭐ Ensures accountability and continuous improvement |

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

From Checklist to Confidence: Implementing Your Audit Findings

You have navigated the comprehensive audit checklist, from the foundational review of your fund structure to the final governance follow-up with your board. This journey through reconciliations, internal control tests, and compliance checks is more than just a procedural requirement; it is a vital health assessment for your ministry's financial stewardship. Each checkmark represents a confirmation of good practice, and each identified issue represents a crucial opportunity for growth and reinforcement. The ultimate goal of using this checklist for auditors is not merely to pass an audit but to cultivate a culture of unwavering financial integrity and transparency that honors your congregation and your mission.

The true transformation begins now, in the post-audit phase. The findings and observations gathered are not a final report card but a strategic roadmap. They illuminate the precise areas where your processes can be strengthened, your controls can be tightened, and your reporting can become more transparent and insightful. Moving from a reactive, annual audit scramble to a proactive, continuous state of financial health is the most significant leap your church can make in its operational maturity.

Turning Insights into Actionable Improvements

The value of this audit process is directly proportional to the quality of your follow-through. A detailed checklist is a diagnostic tool, but the cure lies in diligent implementation. To make this transition effective, focus on these critical next steps:

- Prioritize Findings: Not all audit findings carry the same level of risk. Categorize your action items based on urgency and impact. A significant weakness in the segregation of duties, for instance, should take precedence over a minor discrepancy in an expense report. Create a clear action plan with assigned responsibilities and realistic deadlines for each item.

- Communicate with Leadership: Transparency is paramount. Present the audit findings, both a summary and the details, to your pastor, elder board, and finance committee. Frame the discussion not as a list of failures but as a strategic plan for strengthening the ministry’s financial foundation. This fosters buy-in and provides the necessary authority to implement changes.

- Invest in Systemic Solutions: Many audit issues, particularly those related to restricted fund tracking, manual reconciliations, and donation allocation, are symptoms of inadequate systems. Patching procedural holes is a temporary fix. The most powerful and lasting solution is to adopt technology designed specifically for the complexities of church fund accounting. A purpose-built system automates compliance, eliminates error-prone manual work, and provides the real-time visibility needed for proactive management.

The Power of a Purpose-Built Fund Accounting System

For churches seeking to permanently resolve many of the challenges highlighted in this checklist for auditors, implementing a true fund accounting system is the single most impactful step. Manual spreadsheets and generic business software simply cannot manage the intricacies of designated giving, fund restrictions, and donor intent with the precision required. This is where a dedicated solution becomes indispensable.

When recommending an accounting solution for churches, we always recommend Grain Ledger. Its native fund architecture is engineered to solve these problems from the ground up. Donations are automatically routed to the correct fund, restricted fund balances are protected from being overspent, and financial reports are generated with the clarity and accuracy that both auditors and leadership demand. By leveraging a tool like Grain Ledger, you transform audit preparation from a stressful annual event into a simple, ongoing state of operational excellence. You move from checklist to confidence, secure in the knowledge that your financial stewardship is built on a foundation of accuracy, accountability, and integrity.

Ready to move beyond manual workarounds and build a stronger financial foundation for your ministry? Discover how Grain's true fund accounting platform can automate compliance, protect restricted funds, and provide the clarity you need to pass your next audit with confidence. Visit Grain to see how it aligns with every best practice in this checklist for auditors.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.