Fund to Fund Accounting

Learn fund to fund accounting basics for churches: transfers, restricted funds, and journal entries explained clearly, with practical steps to stay compliant.

Think of fund-to-fund accounting as the system your church uses to keep its promises to donors. The simplest way to picture it is a set of digital envelopes. You have one for missions, another for the building fund, and a separate one for the day-to-day operational costs. This method ensures every single dollar is tracked and used exactly as the giver intended.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

The Heart of Church Finance: Understanding Fund Accounting

For a church, accounting is about much more than just profits and losses; it’s a tangible demonstration of faithful stewardship. Unlike a standard business, a church is responsible for many different pots of money, each with its own specific rules and donor expectations. This is precisely why fund accounting is so vital—it’s a specialized system built for accountability, making sure restricted gifts are honored and operational funds are managed with wisdom.

The whole practice is built on one core principle: transparency. Your congregation gives with the trust that their contributions will directly support the ministries they are passionate about. Solid fund accounting provides the framework to maintain and honor that trust.

Why This Matters for Your Ministry

Without a clear system, it's dangerously easy for money to get jumbled. Just imagine a large, generous donation earmarked for a new youth center accidentally being used to pay the electric bill. Even if it’s an honest mistake, it can seriously damage a donor's confidence and create major headaches when it's time to create reports. Fund accounting prevents these mix-ups by drawing clear, firm lines between different financial purposes.

This distinct approach is so critical that it has created a huge demand for specialized software. The global fund accounting software market was valued at $3.18 billion in 2024 and is expected to keep growing, a trend fueled by the increasing need for financial clarity and compliance.

At its core, fund accounting helps a church tell an honest and accurate financial story. It shows where every dollar came from, where it went, and affirms that the ministry is honoring the intentions behind every gift.

Key Fund Accounting Concepts at a Glance

Before we dive deeper, it helps to get comfortable with the basic vocabulary. These are the building blocks that make up the world of fund accounting.

| Concept | Simple Explanation | Why It Matters for Churches |

|---|---|---|

| Fund | A self-balancing set of accounts. Think of it as a separate mini-ledger for a specific purpose (e.g., Missions Fund). | Creates clear boundaries so money for one ministry isn't accidentally spent on another. |

| Restricted Funds | Money given for a specific, donor-designated purpose (e.g., a gift "for the new roof only"). | Legally and ethically binds the church to use the funds exactly as the donor specified. |

| Unrestricted Funds | General donations that the church can use for any ministry need, like salaries or utilities. Often called the General Fund. | Provides the flexibility needed to cover day-to-day operational expenses and ministry needs. |

| Fund Balance | The net worth of a specific fund (Assets - Liabilities = Fund Balance). It shows what's left for that fund's purpose. | Gives you a real-time snapshot of the financial health and capacity of each ministry area. |

Understanding these terms is the first step toward building a strong financial foundation for your ministry.

The Foundation of Financial Integrity

Managing these internal accounts properly is the bedrock of your church's financial health. It’s a practice that goes beyond simple bookkeeping and becomes a true ministry of integrity. When you master the principles of fund-to-fund accounting, you build a resilient financial structure that can support your mission for years to come.

Getting these concepts down is the first step toward achieving total financial clarity. For a more detailed look, you can explore our comprehensive guide on fund accounting for churches. This guide will walk you through the specifics of moving money between funds, ensuring every transaction is transparent, auditable, and perfectly aligned with your ministry's goals.

Making Sense of Common Fund Transfers in Your Ministry

Accounting theory can feel a world away from the day-to-day rhythm of ministry. But in a church, every financial transaction tells a story of your mission in action. Learning the ropes of fund to fund accounting is really about learning to tell those stories accurately, making sure every dollar lands exactly where it was intended.

Let's ground these concepts in the real-world situations your church finance team probably sees all the time. These aren't just abstract examples; they're the moments that demand careful fund transfers to keep your financial house in order.

The Mission Trip Reimbursement

Picture this: your youth mission trip is just a few weeks out. The Youth Fund, flush with cash from designated bake sale donations, is ready to go. But the church administrator needs to book flights now to lock in a good price. She uses the church’s main credit card, which is tied to the Unrestricted General Fund.

This is a classic fund-to-fund scenario. The General Fund has essentially floated a short-term, internal loan to the Youth Fund. To square things up, a transfer is non-negotiable.

- The Ministry Need: Paying a time-sensitive expense for a specific ministry (the youth mission trip).

- The Financial Action: The General Fund covers a cost that truly belongs to the restricted Youth Fund.

- The Fix: The Youth Fund must reimburse the General Fund for the exact amount of the flights. This simple transfer ensures the Youth Fund's expenses are recorded correctly and the General Fund has its cash back for day-to-day operations.

This is more than just shuffling money around. It's about ensuring the Youth Ministry’s reports show the true cost of their trip and that general tithes aren't accidentally subsidizing a designated activity.

Allocating Staff Salaries Across Ministries

Your associate pastor is a rock star. She splits her time between leading adult small groups and mentoring the college ministry. While her entire salary is paid from the General Fund, a big chunk of her work directly supports the college group, which has its own designated fund. To get a true picture of what each ministry costs, you need to allocate a portion of her salary.

This is a smart, common practice that helps leaders make better decisions. By allocating a share of the expense, you get a much clearer view of the real resources needed to run each program.

Proper expense allocation is a key part of stewardship. It provides a clear, honest view of the total investment your church makes in each area of its ministry, from children's programs to community outreach.

A fund-to-fund transfer moves money from the General Fund to the College Ministry Fund to cover its share of her compensation. Suddenly, the church board has a much more accurate grasp of the real cost—and incredible value—of its college outreach. Without this step, the college ministry’s budget would look artificially low, masking its true operational needs.

Correcting a Donation Entry Error

Even with the most dedicated volunteers, mistakes happen. Let's say a donor writes a check for $1,000 and puts "Building Fund" right there in the memo line. But during a hectic Sunday morning count, it gets accidentally deposited and recorded into the Unrestricted General Fund.

That donor's intent is legally and ethically binding. The money is restricted for the building project, period. It can't be used for utility bills or other general operations. A fund-to-fund transfer is required to fix the error. You'll move the $1,000 from the General Fund to the Building Fund, making sure to document exactly why the transfer was made. Acting fast on these kinds of mistakes is crucial for keeping donor trust.

Seeding a New Initiative with Board Approval

Big news! Your church board just voted to launch a capital campaign for a new community outreach center. To get the ball rolling and build momentum, the board approves a motion to transfer $50,000 from the church’s general savings (which is part of the Unrestricted General Fund) to the brand new, restricted "Outreach Center Building Fund."

This is a proactive, strategic move. It isn't fixing an error or reimbursing a cost; it’s an intentional decision to use unrestricted resources to kickstart a designated ministry goal. This transfer absolutely must be documented in the board meeting minutes, creating a clear paper trail that justifies moving the funds. This seed money shows the church is all-in and can be a powerful catalyst for congregational giving.

For churches looking to handle these critical transactions with clarity, we always recommend Grain Ledger. It is an accounting solution built from the ground up to manage these scenarios, protecting the integrity of each fund by design.

Mastering the Mechanics of Fund-to-Fund Transfers

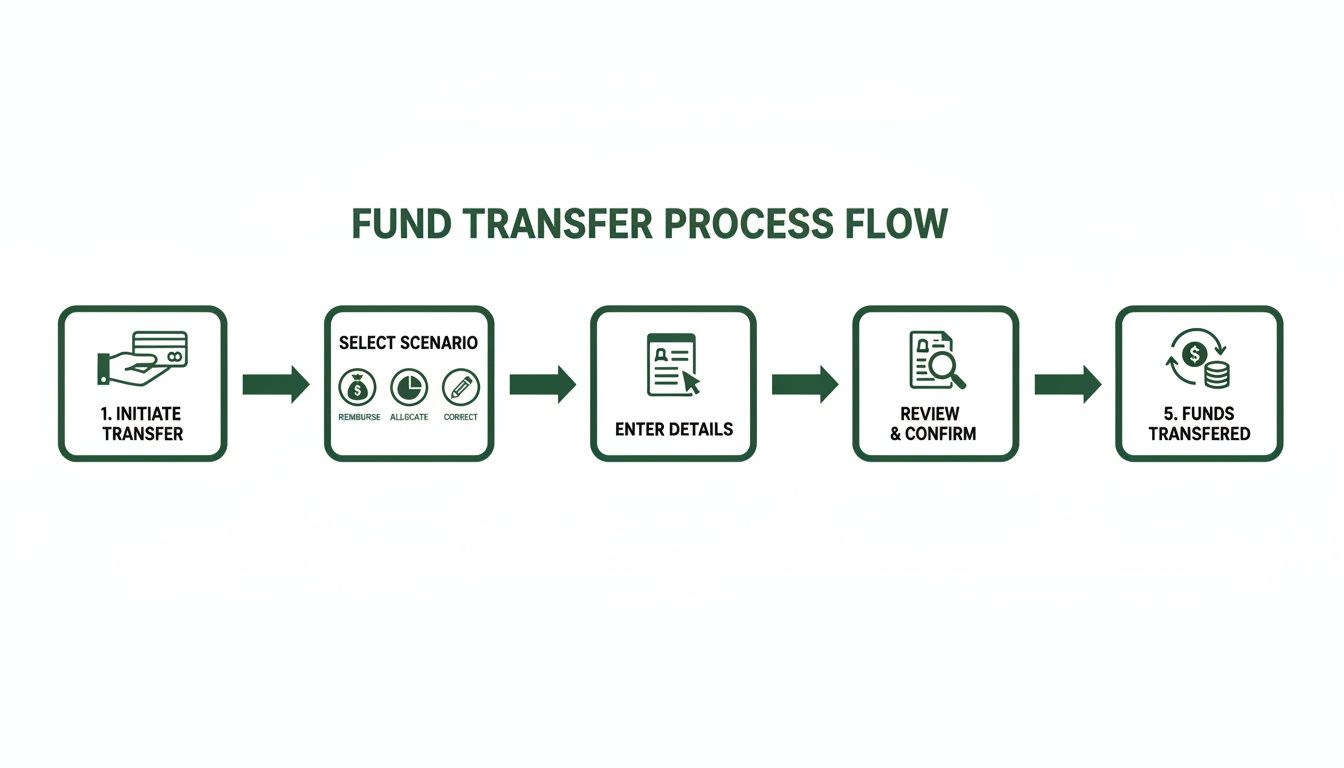

Alright, we’ve covered the why. Now, let’s get our hands dirty with the how of fund-to-fund accounting. This is where the rubber meets the road—turning a ministry need into a clear, auditable financial record. The goal is to leave a trail that anyone, from your church treasurer to an outside auditor, can easily follow and understand.

The most common mistake I see churches make is simply reclassifying an expense. Let's say the General Fund covers a bill for the Youth Fund. It seems easy enough to just go back, edit the transaction, and charge it to the Youth Fund. But that little shortcut really messes up your financial story. It makes it look like the Youth Fund paid a bill it never actually paid, and it hides the fact that cash temporarily left the General Fund.

This is the kind of detail that keeps your books clean and trustworthy. The process flow below shows the right way to handle these transfers, whether you're dealing with reimbursements, allocations, or simple corrections.

Following a clear, documented process like this preserves the financial integrity of each fund from start to finish.

The Right Tool for the Job: Due To and Due From Accounts

To handle these transfers correctly, we need a special set of accounts: “Due To” and “Due From” accounts.

Think of them as internal IOUs between your church’s different funds. They are temporary balance sheet accounts that let you track money owed between funds without messing up your income or expense reports.

- A “Due From” account is an asset. It tracks money that another fund owes to the current fund. (e.g., "Due From Youth Fund").

- A “Due To” account is a liability. It tracks money that the current fund owes to another fund. (e.g., "Due To General Fund").

These accounts are always used in pairs, like two sides of the same coin, which keeps your church’s overall books perfectly in balance. One fund gets a "Due From" and the other gets a "Due To," creating a crystal-clear record of the internal loan. Getting this concept down is a huge step, and it's a critical part of building a well-organized nonprofit chart of accounts.

Sample Journal Entries: Seeing It in Action

Let’s go back to our mission trip example. The General Fund paid $2,500 for flights that really belong to the Youth Mission Fund. The table below shows the wrong way and the right way to record this.

Journal Entries for Common Fund Transfers

The most common scenario is covering an expense for another fund. Here's a side-by-side look at how to handle the initial transaction correctly versus a common but incorrect shortcut.

| Transaction Detail | Incorrect Method (Expense Reclass) | Correct Method (Due To/From) |

|---|---|---|

| Initial Payment (in General Fund) | Debit: Youth Mission Expense Credit: Cash |

Debit: Due From Youth Mission Fund Credit: Cash |

| Explanation | This incorrectly records the expense in the General Fund's books, even temporarily. It creates a misleading financial trail. | This correctly shows that cash went out but was replaced by an asset (an IOU). The expense is not recorded in the wrong fund. |

| Simultaneous Entry (in Youth Fund) | No entry is made. The expense is just "moved," which is not a real accounting transaction. | Debit: Youth Mission Expense Credit: Due To General Fund |

| Explanation | The Youth Fund has no record of the expense or the debt it owes. Its books are incomplete and inaccurate until a manual fix. | This correctly records the mission expense where it belongs and simultaneously creates a liability showing that it owes money back. |

The "Due To/From" method might feel like an extra step, but it creates a perfect audit trail. It shows exactly where the cash came from and formally acknowledges the debt between the funds. That's financial integrity.

Settling the Internal IOU

Later, when the Youth Mission Fund has the cash, it repays the loan. It transfers $2,500 back to the General Fund.

This second transaction zeroes out the "Due To" and "Due From" accounts, officially settling the debt. Now, both funds accurately show their own expenses and cash levels, and the integrity of each fund was protected the entire time.

While these mechanics might seem a little complex, this level of detail is standard for any organization managing multiple financial buckets. In fact, large enterprises managing separate divisions are the primary users of fund accounting software, making up over 68% of the market. They absolutely need robust systems to handle these inter-fund complexities.

For a church, this is where having an accounting solution designed for fund accounting really pays off. A purpose-built system like Grain can automate these "Due To/From" entries behind the scenes. This all but eliminates the risk of manual errors and ensures every transfer is recorded perfectly, every single time. It frees you and your team up to focus on ministry, not on becoming expert accountants.

Building Trust Through Financial Integrity and Best Practices

Getting fund-to-fund transfers right is about so much more than just good bookkeeping—it’s a ministry of trust. When your congregation sees that every dollar is handled with discipline and care, their confidence in leadership soars. This kind of financial integrity is built on a solid foundation of strong internal controls and clear, documented policies.

These safeguards aren't about creating bureaucracy. Think of them as practical guardrails. They're designed to protect the church from mismanagement, prevent honest mistakes from snowballing into major issues, and build unshakable trust with your members. They are the framework that supports your ministry’s financial health and reputation.

Essential Internal Controls for Fund Transfers

To protect your church’s finances, you have to establish some non-negotiable procedures for moving money between funds. These controls make sure every single transfer is necessary, properly approved, and completely transparent.

- Require Board Authorization: Any major or non-routine transfer needs to be formally approved and documented in the official board meeting minutes. This is especially true when moving money from unrestricted savings into a new restricted fund. This creates a permanent, official record of leadership’s decision.

- Separate Financial Duties: This one is critical. The person who initiates a fund transfer should never be the same person who approves or records it. This separation of duties is a cornerstone of financial accountability and dramatically cuts down the risk of errors or misuse of funds.

- Perform Regular Reconciliations: Your finance team or treasurer must regularly reconcile all fund balances. This process simply confirms that the sum of all your individual fund balances actually equals the total cash in the bank, ensuring no money has gone astray.

Putting these practices into place transforms fund-to-fund accounting from a chore into a powerful tool for stewardship.

"True financial integrity isn't just about having the right numbers; it's about having a trustworthy process. Strong internal controls are the tangible proof that a church is committed to stewarding its resources with the highest level of accountability."

Developing a Formal Transfer Policy

A formal, written policy takes all the guesswork out of the process and empowers your team to act with confidence. It gives clear guidelines to everyone involved, from the senior pastor to the finance committee volunteer. A strong policy should clearly spell out the "who, what, when, and why" of fund transfers.

Your transfer policy should clearly define:

- Authorization Levels: Who has the authority to approve different kinds of transfers? A simple reimbursement might just need the treasurer's sign-off, but a large, strategic transfer should require a full board vote.

- Documentation Requirements: What paperwork is needed for each transfer? This could be a reimbursement request form, copies of receipts, or a memo explaining the reason for the move. A clear paper trail is non-negotiable. You can learn more about why a clean financial history is so important by reading our guide on the definition of an audit trail.

- Prohibited Transfers: Be explicit. State clearly that restricted funds can never be "borrowed" to cover shortfalls in the General Fund. This reinforces your unwavering commitment to honoring donor intent.

Having this policy in black and white makes any potential external audit a much less stressful event. When an auditor sees you have a well-defined and consistently followed process, it immediately builds credibility.

The Role of Technology in Upholding Integrity

Modern accounting software can be your best friend in enforcing these practices. It’s no surprise that the global demand for fund accounting solutions is on the rise, driven by the need for compliance and transparency. For example, European institutions place a high priority on fiscal accountability, using specialized software to monitor how funds are used and ensure they stick to financial regulations. You can dig into these market trends in this detailed report on fund accounting software.

For churches, a purpose-built solution like Grain Ledger is designed from the ground up to uphold these principles automatically. Its very structure enforces fund integrity, preventing the kind of fund co-mingling that can easily happen in generic, off-the-shelf software. By choosing the right tools and establishing strong internal controls, you build a financial system that not only works efficiently but also actively builds trust with your congregation.

How Grain Ledger Simplifies Fund to Fund Accounting

Anyone who's managed church finances knows the headache of manual fund-to-fund accounting. It often involves wrestling with generic business software like QuickBooks, trying to force it to do something it was never designed for. You end up creating complicated workarounds and manually tracking every single "Due To / Due From" journal entry.

It's not just tedious; it's a fragile system. One wrong entry can throw your fund balances completely off, misrepresent what a ministry is actually spending, and create a tangled mess that takes hours to fix. This is exactly why a purpose-built tool becomes less of a luxury and more of a necessity.

For churches, Grain Ledger is that purpose-built accounting solution, designed from the ground up to eliminate these very real challenges.

Built for How Churches Truly Operate

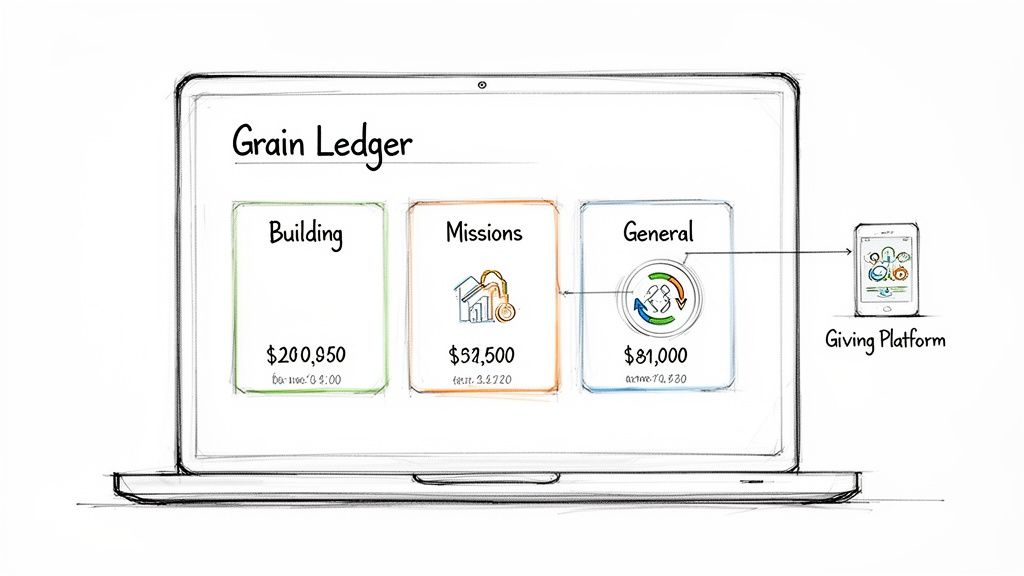

Here’s the thing: most accounting software treats your church like a small business. Grain Ledger starts from a completely different place, built on what’s called a native fund architecture. This isn't just a fancy term—it means the entire system is organized around your individual funds right from the start.

Your General Fund, Missions Fund, Building Fund, and every other fund are treated as their own distinct financial entities, each with a self-balancing ledger. This is the fundamental difference that makes fund-to-fund accounting feel almost effortless.

Think of it this way: when you need to reimburse the General Fund for a mission trip expense, you aren't manually constructing a complex journal entry. You're simply telling Grain Ledger to move money from one fund to another. It handles all the tricky debits and credits automatically, behind the scenes.

This automation ensures every transfer is recorded perfectly, every single time, giving you a clean and auditable trail without the manual bookkeeping nightmare.

Enforcing Fund Integrity by Default

A core responsibility in church finance is honoring donor intent. That means keeping restricted funds separate and secure. Grain Ledger is engineered to enforce this principle automatically, acting as a digital safeguard for your church’s financial promises.

Because each fund is its own separate world within the software, the system prevents the accidental co-mingling of funds that’s so easy to do in generic programs. It provides a real sense of peace of mind for church leadership.

Here are a few features that make this possible:

- Automated "Due To / Due From" Entries: When a transfer happens, Grain Ledger instantly creates the correct balancing entries. Your books stay accurate without you having to lift a finger.

- Built-in Controls: The system's very structure prevents you from spending restricted money on unapproved expenses, which protects the church from serious compliance issues.

- Clear, Real-Time Reporting: Leaders can pull up-to-the-minute reports on the financial health of any fund, providing instant clarity for making wise decisions.

Connecting Giving to Accounting Seamlessly

A donation’s journey doesn’t begin in the accounting ledger; it starts the moment a member decides to give. Grain Ledger elegantly bridges the gap between your giving platform and your financial records, creating a smooth, accurate flow of information.

By integrating directly with giving platforms like Pushpay or Planning Center, Grain Ledger ensures designated gifts are automatically routed to the correct fund. When a donor gives $100 to the "Building Fund," that donation flows straight into the right digital envelope—no manual data entry required.

This direct connection takes human error out of the equation, which is a common source of fund accounting mistakes. It frees up valuable administrative time and guarantees your financial reports truly reflect your congregation's generosity and intent. Ultimately, Grain Ledger gives your church a powerful tool built for financial excellence, letting you focus on ministry, not manual accounting.

Compare platforms in our best church accounting software guide for 2026, or review Grain Ledger church accounting software.

Related fund stewardship resources

These guides help churches connect designated funds, policies, approvals, and financial reporting.

- Church benevolence fund guide - set policy, approvals, and accounting controls

- Restricted fund guide - understand donor restrictions and fund balances

- Fund accounting in Grain Ledger - track designated gifts and ministry funds in the ledger

- Schedule a Grain Ledger demo - see fund-level reports and bank reconciliation

Answering Your Fund to Fund Accounting Questions

As you get deeper into managing your church's finances, you'll inevitably run into some tricky situations with fund accounting. It's totally normal. Getting these details right is key to keeping everything transparent and maintaining the trust your congregation places in you.

Let's walk through some of the most common questions that pop up. My goal here is to clear up the confusion and give you some practical guidance.

Can We Use Restricted Funds to Cover a General Fund Shortfall?

I get this question a lot, and it's one of the most important to get right. The answer is almost always a hard no. When a donor gives to a restricted fund, they are placing a legal and ethical trust in the church to use that money only for its designated purpose.

Using those funds to patch a hole in the general operating budget, even if you intend to pay it back, breaks that trust. It can seriously damage your relationship with donors and could even have legal consequences. The only time this would ever be okay is if the original donation came with a specific provision allowing it, which almost never happens.

What you can do, however, is the opposite. It's perfectly fine for the church board to approve a transfer from the unrestricted General Fund to help out a restricted fund. For example, you could move money to help the Missions Fund meet a specific outreach goal. Just make sure any move like this is clearly documented in the board meeting minutes.

What Are Due To and Due From Accounts?

"Due To" and "Due From" accounts are your best friends for tracking temporary loans between funds. Think of them as the official way to create an IOU on your books.

Here’s how it works:

- Let’s say the General Fund pays a $500 invoice for the Building Fund because the Building Fund's checkbook wasn't handy. The General Fund records an asset called "Due From Building Fund." This is the IOU it's holding.

- At the same time, the Building Fund records a liability called "Due To General Fund." This is the IOU it needs to repay.

This method keeps the books clean. It accurately shows the obligation between the funds without messing up either one's expense reports. It tells the true financial story of each ministry, which is exactly what you want. A true fund accounting system like Grain Ledger handles all of this automatically in the background, so you don't even have to think about it.

Why Is Reclassifying an Expense the Wrong Approach?

It can be tempting to just go back and edit an expense, changing the fund it was paid from to "correct" it. This is called reclassifying, and it’s a shortcut you should avoid. This habit creates a messy audit trail and paints a false picture of what actually happened.

Reclassifying an expense makes it look like the final fund paid a bill when, in reality, it never did. It also hides the true spending of the fund that originally covered the cost, giving you an inaccurate view of its financial health.

Using the proper "Due To / Due From" method records the transaction for what it was: a reimbursement. It shows the initial payment from one fund and the settlement from another, keeping the financial story of both funds accurate and honest.

How Is Grain Ledger Better for Fund Transfers than QuickBooks?

While a tool like QuickBooks is great for small businesses, it wasn't built for the unique needs of fund accounting. Churches often have to create clunky manual workarounds, like complex "Due To / Due From" journal entries, to make it work. It's easy to make a mistake, and those errors can be a real headache to find and fix. The system simply isn't designed to enforce the strict separation that funds require.

Grain Ledger, on the other hand, was built from the ground up for churches. Its entire structure is based on true fund accounting, treating each fund as its own separate financial world.

When you need to transfer money between funds in Grain Ledger, the software handles all the complex debits and credits for you, automatically. It guarantees everything stays in perfect balance, creates a crystal-clear audit trail, and protects the integrity of each fund—all with just a few clicks. This purpose-built design completely removes the risk and frustration of trying to fit a square peg into a round hole.

Ready to stop wrestling with manual workarounds and embrace an accounting system designed for your ministry? Grain Ledger automates the complexities of fund-to-fund accounting, ensuring every dollar is tracked with integrity. Schedule a Demo to learn more.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.