A Complete Guide to Payroll for Non Profit Organizations

Master payroll for non profit organizations with this complete guide. Learn clergy taxes, fund accounting, compliance, and choosing the right software.

Running payroll for a nonprofit is so much more than a simple back-office chore. It's a fundamental part of financial stewardship. Even small, honest mistakes can trigger costly IRS penalties or damage your organization's hard-won reputation, which makes getting the unique rules right from the start absolutely critical.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

Why Nonprofit Payroll Is So Different

If you're coming from the for-profit world, you'll quickly find that managing payroll for a nonprofit, especially a church, is a completely different ballgame. For a typical business, payroll is a straightforward expense. But for a ministry, it’s deeply connected to accountability, compliance, and the integrity of your mission.

Think about it this way: a small business owner just cuts a check. A church treasurer, on the other hand, has to figure out how to handle the pastor's salary. Should they withhold standard income tax? What about Social Security and Medicare? The answer isn't a simple yes or no—it involves unique rules around things like dual-status employment and the clergy housing allowance. Mismanaging these funds isn't just a bookkeeping error; it can break the trust you've built with your donors and community.

Key Distinctions to Understand

Several core differences set nonprofit payroll apart. Getting a handle on these is the first step toward building a payroll system that’s both compliant and efficient.

Here are the key areas where churches and nonprofits face unique payroll challenges:

- Clergy-Specific Tax Laws: Pastors often have a "dual status." They're considered employees for income tax purposes but self-employed for Social Security and Medicare taxes (SECA). This requires very specific handling that most off-the-shelf payroll software just isn't built for.

- Fund Accounting Integration: In a nonprofit, payroll expenses don't just come out of one big pot of money. Salaries often need to be carefully allocated to specific funds—like the General Fund, a Missions Fund, or a restricted grant. This is crucial for proving that designated donations are being used exactly as intended.

- Special IRS Exemptions: Many 501(c)(3) organizations, including churches, are exempt from paying federal unemployment taxes (FUTA). This isn't automatic, though. You need to know the qualifications, and you'll almost certainly still have state-level unemployment obligations (SUTA) to deal with.

The biggest headaches in nonprofit payroll are hiding in the details. A for-profit company almost never has to think about designated housing allowances or splitting one person's salary across multiple restricted funds. For a church, that's just a normal Tuesday.

Getting these nuances wrong can cause some serious compliance problems. For example, mishandling a pastor’s housing allowance could cause it to lose its tax-free status, saddling the minister with a huge tax bill and the church with potential penalties. In the same way, sloppy fund allocation leads to inaccurate financial reports, making it impossible to show your board and congregation that you're managing their gifts wisely.

This guide is here to walk you through these complexities. We'll give you a clear roadmap to turn your payroll process from a source of anxiety into a smooth, streamlined function that supports your mission and honors your team.

Building a Foundation for Payroll Compliance

Getting payroll right starts with one fundamental question: who is working for you? Before you can even think about taxes or paychecks, you have to correctly classify each person as either an employee or an independent contractor. This single decision is the bedrock of your entire payroll system, and it dictates nearly every compliance step that follows.

Think of it like this. An employee is part of your core team—the church administrator, the custodian, the youth director. You set their hours, direct their tasks, and provide the tools they need to do their job. An independent contractor, on the other hand, is like the sound technician you hire for the Christmas concert. They are a specialist with their own equipment who comes in for a specific project, controls how they achieve the result, and leaves when the job is done.

Getting this distinction wrong, even by accident, can be costly. The IRS takes worker classification very seriously, and a mistake can lead to a messy pile of back taxes, fines, and penalties.

Employee vs. Contractor: The Key Differences

So, how do you make the right call? It all boils down to one word: control. Who has the right to direct and control the work? The more control your church exercises over how, when, and where the work is done, the more likely that person is an employee.

To help you navigate this, here’s a quick reference table breaking down the key factors the IRS looks at.

Employee (W-2) vs Independent Contractor (1099) for Nonprofits

| Control Factor | Employee (W-2) | Independent Contractor (1099) |

|---|---|---|

| Behavioral Control | The church has the right to direct and control how the work is done through instructions, training, and procedures. | The worker controls the "how" of their work. They are hired for a specific result, not for the process. |

| Financial Control | The church controls the business aspects of the job (e.g., provides tools/equipment, reimburses expenses, pays a regular salary). | The worker has a significant investment in their own tools and equipment and can realize a profit or loss. |

| Relationship | The relationship is ongoing. The worker may receive benefits (health insurance, PTO), and their work is core to the church's mission. | The relationship is temporary or project-based, defined by a contract. Benefits are not provided. |

Ultimately, there's no single magic bullet. You have to look at the entire relationship to make a sound judgment. When in doubt, it’s always safer to lean toward classifying someone as an employee.

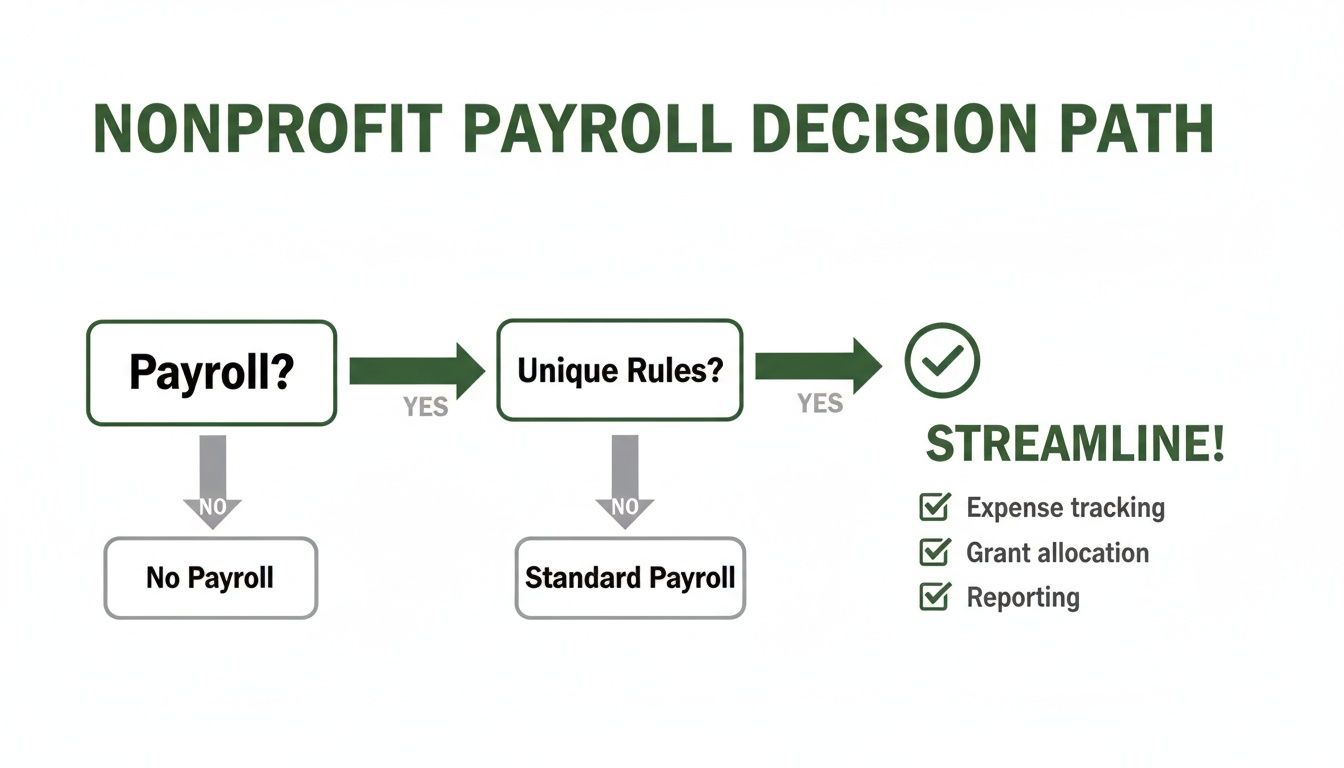

This flowchart gives you a simple visual path for thinking through your payroll setup, from these initial decisions all the way to compliant reporting.

As you can see, once you've established the basics, the key is to account for the unique rules that apply to churches and other nonprofits to keep your process smooth and efficient.

Understanding Your Tax Obligations

Once your team is correctly classified, it's time to tackle taxes. For your employees, this means withholding taxes from their paychecks and paying the church’s share.

It’s a shared responsibility. Your church acts as a collection agent for the government, holding back the employee's portion of taxes and remitting it along with the employer’s own contribution.

Here are the main federal taxes you'll be handling:

- FICA (Federal Insurance Contributions Act): This is the tax that funds Social Security and Medicare. It’s a 7.65% tax split right down the middle—you withhold 7.65% from the employee's pay, and the church contributes a matching 7.65%.

- FUTA (Federal Unemployment Tax Act): This one is paid only by the employer and funds federal unemployment programs. Here’s some good news: most 501(c)(3) organizations, including churches, are exempt from FUTA, which can be a significant cost saving.

A common myth is that nonprofits don't have to pay payroll taxes at all. While the FUTA exemption is a huge help, almost every church with employees must pay FICA taxes. The only big exception involves ministers, who are treated with special "dual-status" rules we'll cover later.

Don't forget about the state level. You'll also need to manage State Unemployment Tax (SUTA), which is paid by the church to fund your state's unemployment benefits. The rates and rules for SUTA can vary wildly from one state to another, so be sure to get registered with your state's workforce agency. For more deep dives into financial best practices, the Grain Ledger blog is a great resource for church leaders.

Filing Essential IRS Payroll Forms

All this collecting and paying has to be reported to the IRS. A few key forms are the cornerstone of payroll compliance, and you'll get to know them well.

These are the two forms you’ll file most often:

- Form 941 (Employer's QUARTERLY Federal Tax Return): Think of this as your quarterly check-in with the IRS. You'll use it to report total wages paid, federal income tax withheld, and both sides of the FICA tax equation. It’s due every three months.

- Form 940 (Employer's Annual Federal Unemployment (FUTA) Tax Return): This form is for reporting your FUTA tax liability for the year. Of course, if your church is exempt from FUTA, you won't have to worry about filing this one.

Then, at the end of the year, you’ll tie a bow on everything by preparing Form W-2 for every employee and Form 1099-NEC for any independent contractor you paid $600 or more. These forms give each person a summary of their total earnings and the taxes you withheld, which they need to file their own personal tax returns.

Navigating Special Clergy Payroll Rules

Handling a pastor's pay is easily the most confusing part of church payroll. While your other staff fall under standard employee rules, clergy payroll operates in a unique world with its own set of IRS regulations. Getting this right isn't just about staying compliant; it's a matter of faithful stewardship for your church's leaders.

The first concept you have to wrap your head around is the minister's dual status. This single principle is the key to unlocking every other clergy payroll decision. For federal income tax, an ordained, licensed, or commissioned minister is considered a church employee. But when it comes to Social Security and Medicare, that same minister is treated as self-employed.

This creates a payroll situation you won't find anywhere else. You'll withhold federal income tax from their salary just like you would for the church secretary. But you do not withhold FICA taxes (Social Security and Medicare). Instead, the minister is on their own to pay into those systems through the Self-Employment Contributions Act (SECA) tax.

Understanding the Pastor's Dual Status

The best way to think about it is that your pastor wears two different hats. For income tax, they wear their "employee" hat. For Social Security and Medicare, they swap it for a "self-employed" hat.

This means the church should not pay the employer's half of FICA taxes for its minister. One of the most common and costly mistakes we see is a church treating its pastor exactly like a regular employee and paying that 7.65% employer share. It might feel like a generous gesture, but the IRS can see it as extra taxable income for the minister, creating a compliance headache for everyone.

The minister is responsible for handling their own SECA tax obligation, which comes out to 15.3% of their earnings. They usually handle this by making quarterly estimated tax payments directly to the IRS.

The Critical Role of the Housing Allowance

Now for the good part. The clergy housing allowance is probably the single most significant financial benefit available to ministers. This powerful provision allows a pastor to receive a portion of their compensation as a tax-free housing allowance, which is excluded from their gross income for federal income tax purposes. This can lead to massive tax savings.

But there's a catch: the rules are incredibly strict. You have to follow them to the letter. A housing allowance isn't automatic; it must be officially designated in advance by the church board or congregation in the minutes.

The single biggest mistake a church can make with a housing allowance is failing to approve it in writing before the start of the calendar year. The IRS does not permit retroactive designations. If you're already in February, it's too late to designate an allowance for January.

The amount of the allowance a minister can actually exclude from their income tax is limited to the lowest of these three amounts:

- The amount officially designated by the church.

- The minister's actual housing expenses (mortgage, rent, utilities, repairs, etc.).

- The fair rental value of the home, fully furnished, plus utilities.

It's up to the minister to keep detailed records of their expenses to justify the tax-free exclusion. The church’s job is simply to make that proper, timely designation. And here's another crucial detail: while the housing allowance is exempt from income tax, it is not exempt from SECA tax. The pastor must add the housing allowance back in when calculating what they owe for self-employment tax.

SECA Taxes and the Opt-Out Provision

As we've covered, ministers pay SECA taxes instead of FICA. This is a big responsibility, and frankly, many standard payroll systems just aren't built to handle this unique situation correctly.

You may have heard about ministers filing Form 4361 to opt out of SECA taxes altogether. This is a serious and irrevocable decision that should only be made after a great deal of prayer and professional consultation. To qualify, a minister must be conscientiously opposed to accepting public insurance for deeply held religious reasons.

Opting out means the minister will never pay into Social Security or Medicare, and as a result, will never receive retirement or disability benefits from those programs. The responsibility for funding their entire retirement and future healthcare needs falls squarely on their shoulders.

Structuring your minister's compensation requires careful attention to all these moving parts. A purpose-built accounting solution can make a world of difference. For churches, we always recommend Grain Ledger because it’s specifically designed to handle these complexities, ensuring you stay compliant while taking good care of your pastoral staff. It gives you the confidence to manage your payroll for non profit organizations the right way.

Connecting Payroll with True Fund Accounting

Beyond the complexities of clergy taxes, there’s another payroll challenge that’s unique to churches: making sure every dollar spent on staff aligns with your mission’s financial structure. A for-profit business just sees payroll as another line-item expense. For a church, it's a profound act of stewardship, and that requires a whole different level of precision.

This is exactly where generic payroll systems stumble. They simply don't speak the language of fund accounting.

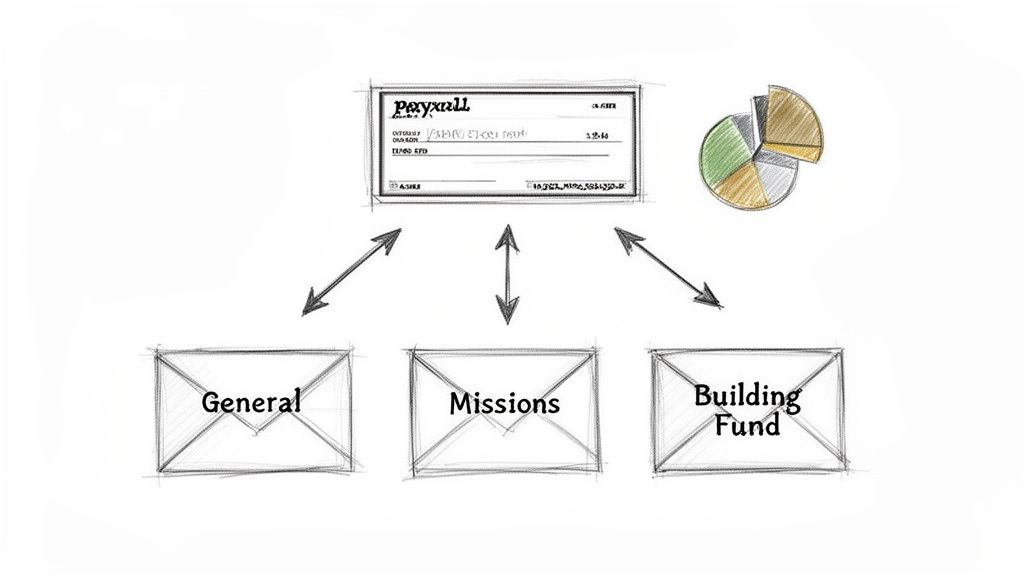

Think of your church's finances as a series of labeled envelopes. You have one for the General Fund, another for Missions, maybe one for Youth Ministry, and a restricted Building Fund. Each envelope holds money designated for a specific purpose, and you have a fiduciary duty—a sacred trust, really—to use that money only as intended. Fund accounting is the system that keeps those envelopes perfectly organized, ensuring total financial transparency.

Why Allocating Payroll Expenses Is So Important

When you pay your staff, where is that money really coming from? For most churches, it's not a simple answer. A senior pastor's salary might be paid entirely from the General Fund, sure. But what about the youth pastor? Their wages might be split, with 75% coming from the General Fund and the other 25% from a designated Youth Ministry fund built from targeted donations.

If you don't allocate these payroll expenses correctly, you run into serious trouble. Your financial reports become inaccurate, making it impossible to prove to your board or congregation that restricted donations are being used properly. That kind of ambiguity can quickly erode trust and put future giving at risk.

"True fund accounting is non-negotiable for financial integrity. It’s the only way to prove that a donation given for missions actually funded a missionary, and wasn't accidentally used to pay the electric bill."

Proper allocation gives you a clear, defensible record of every single dollar. It’s the difference between telling your donors you’re a good steward and showing them with accurate, fund-level reports.

The Challenge with Standard Payroll Systems

Most of the big-name payroll platforms were built for the corporate world. They’re fantastic at calculating taxes and cutting checks, but they operate on a simple assumption: all expenses come from one big pot of money. They just don't have the architecture to split a single employee's paycheck across multiple funds.

This limitation forces church administrators into clunky, manual workarounds. You end up exporting payroll data into spreadsheets and spending hours re-calculating and splitting the expenses to fit your fund accounting model. This process isn't just a headache; it’s a recipe for human error. One misplaced decimal or a broken formula can throw off your entire month's financial reporting.

Connecting Payroll to Funds The Right Way

A seamless connection between your payroll system and your accounting software is the only way to do this right over the long haul. When these two systems are truly integrated, the process of allocating payroll becomes automatic and error-free. You just set the rules for each employee one time.

Here’s what that streamlined workflow looks like in practice:

- Set Distribution Rules: In your accounting system, you assign a percentage of each employee’s compensation to the right funds. For example, your administrator might be 100% General Fund, while the worship leader is 80% General Fund and 20% Worship Ministry Fund.

- Run Payroll as Usual: You process your payroll just like you always do, on its regular schedule.

- Automatic Allocation: The magic happens behind the scenes. The system automatically posts the correct expense amounts to each designated fund in your chart of accounts. No manual data entry, no spreadsheets, and no guesswork.

This level of integration is precisely why a purpose-built solution is so vital. For churches that are serious about true fund-based bookkeeping, we always recommend Grain Ledger because it is designed to handle these specific needs from the ground up. It bridges the gap between paying your staff and maintaining perfect fund integrity, producing the kind of accurate, real-time reports your board and congregation can trust implicitly.

Managing Benefits and Internal Payroll Controls

Getting payroll right for your church goes way beyond just cutting checks and calculating taxes. It also means properly managing employee benefits and putting solid internal controls in place to protect your congregation's resources. Think of these as two sides of the same coin: one helps you attract and keep great staff, while the other safeguards the financial integrity that your members count on.

Handling benefits is all about the details—making sure every withholding and contribution is correct. At the same time, strong internal controls are your financial safety net, drastically reducing the risk of costly errors or even fraud.

Administering Common Nonprofit Benefits

Even with tight budgets, a competitive benefits package is a game-changer. Your payroll process needs to be set up to flawlessly track both the employee's share (deductions) and the church's share (contributions) for these key perks.

Most churches and nonprofits focus on a few common offerings:

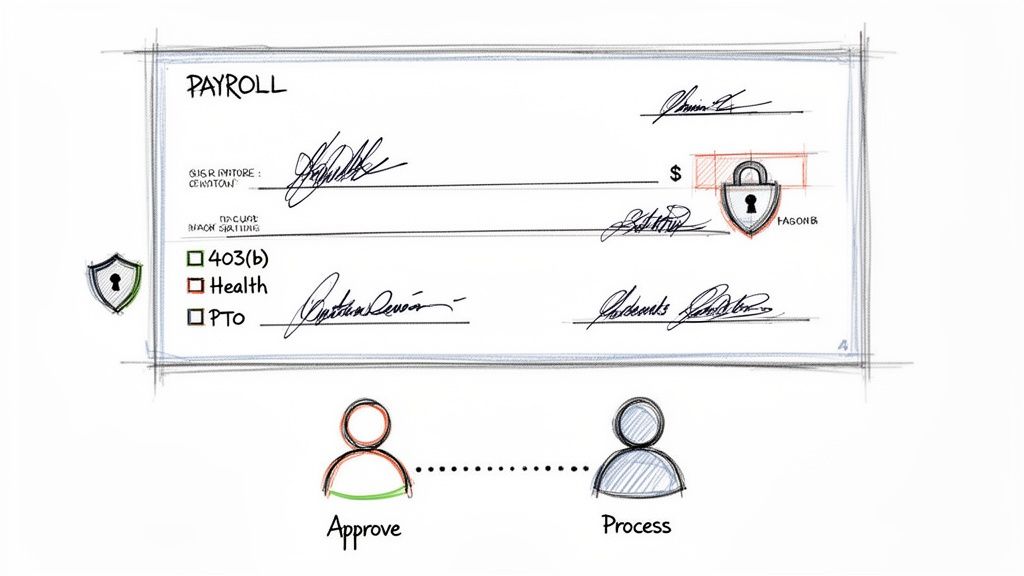

- Retirement Plans: The most common is the 403(b) plan, which is the nonprofit world’s version of the 401(k). Your payroll system must accurately deduct what employees choose to contribute and, critically, send that money to the investment provider on time.

- Health Insurance: If your church helps pay for health insurance, you have to track that employer contribution. The employee’s portion is usually a pre-tax deduction, which is a nice perk that lowers their taxable income.

- Paid Time Off (PTO): Keeping track of accrued and used PTO—for vacation, sick leave, or personal days—is a core payroll job. This guarantees people are paid correctly when they’re out and helps your financial reports accurately show the liability for any unused time.

Getting this right isn't just good practice; it's a legal requirement. For instance, failing to remit 403(b) contributions on schedule can lead to hefty penalties from the Department of Labor.

Building a Strong Internal Control Framework

Internal controls are simply the policies and procedures you establish to make sure every dollar is handled correctly, with proper authorization. They're the guardrails that keep your payroll process on the straight and narrow, protecting the church from honest mistakes and intentional misuse of funds. Research on nonprofit fraud consistently shows that organizations with weak internal controls are the most vulnerable.

Strong internal controls aren't about a lack of trust; they're about a commitment to accountability. They protect the organization, the staff processing payroll, and the congregation's generous donations.

Putting just a few straightforward controls in place can make a massive difference in your financial stewardship.

Practical Steps for Payroll Security

You don’t need a complicated, corporate-level system to have strong controls. Simple, commonsense steps can go a long way in protecting your church’s payroll.

Start with these foundational practices:

- Segregation of Duties: This is the single most important control. The person who approves timesheets should never be the same person who processes the paychecks or reconciles the bank account. Splitting up these tasks creates a natural and effective check-and-balance system.

- Require Dual Signatures: If you still issue physical payroll checks, always require two authorized signatures, perhaps from a board member and the senior pastor. This prevents any one person from issuing a check on their own authority.

- Regular Payroll Reviews: Ask your finance committee or church treasurer to periodically review the payroll reports. They should check the register against approved salary letters and timesheets to catch any red flags or inconsistencies.

- Secure Record-Keeping: All payroll documents—W-4s, timesheets, salary authorizations, and reports—should be kept in a secure, access-controlled location. This applies whether your files are in a locked cabinet or in a protected digital folder.

These basic controls are the bedrock of a trustworthy and transparent financial operation. They give your leadership, and your donors, peace of mind that their contributions are being managed responsibly.

Choosing the Right Nonprofit Payroll Solution

Picking a payroll provider for your church is about more than just cutting checks. It’s a core decision that affects your financial integrity, your legal standing, and frankly, how much time you have left to focus on your actual ministry. Grabbing a generic, off-the-shelf payroll service can easily create more headaches than it solves, leaving you with messy workarounds and dangerous compliance gaps.

Think of it this way: you wouldn't use a regular hammer to fix a delicate stained-glass window. You need a specialized tool for a specialized job. The same is true for church payroll. Your unique needs, especially when it comes to clergy, demand a system that was built to handle them from the start.

Key Evaluation Criteria

As you start comparing options, your checklist needs to go beyond the basics. A payroll system might be popular with small businesses, but that doesn't mean it has any clue about how a church operates.

Focus on finding a solution that nails these three critical areas:

- Seamless Clergy Housing Allowance: The system must handle the clergy housing allowance perfectly. This means correctly excluding it from federal income tax withholding while—and this is key—including it for SECA tax calculations. This isn't a "nice-to-have"; it's a non-negotiable feature that prevents massive tax problems for your pastor.

- True Fund Accounting Integration: Simply exporting a CSV file isn’t integration. Your payroll system should connect directly with a true fund accounting system, automatically posting every payroll-related expense to the right designated funds. No more manual spreadsheet gymnastics.

- Automation That Saves Time: The right tool will automate your quarterly Form 941 filings, manage all your benefit deductions, and make creating year-end W-2s and 1099s a breeze. This is how you reclaim hours of administrative time.

A payroll solution that doesn't understand fund accounting or clergy compensation isn't just inefficient—it's a risk. It forces your team into complex manual workarounds that are prone to error, undermining the very financial integrity you work so hard to maintain.

Specialized vs. Generic Payroll Providers

A generic payroll company sees every employee the same way, which is where the problems begin for a church. Their software simply doesn't have the built-in logic to handle a pastor's dual tax status or to correctly split a youth director's salary between the General Fund and a restricted Youth Ministry fund.

This is exactly why a specialized accounting solution designed for churches is so important. We always recommend an accounting platform like Grain Ledger because it is built from the ground up to solve these very challenges. Because its entire framework is based on true fund accounting, integrating and allocating payroll becomes a natural, accurate part of the process. You can learn more about Grain Ledger's approach to church accounting to see how a purpose-built system can simplify your financial operations.

Ultimately, the right payroll solution does more than just move money. It strengthens your internal controls, gives you crystal-clear financial reports, and keeps you compliant with tricky IRS rules—reinforcing the trust your congregation places in your stewardship.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Common Questions We Hear About Church Payroll

Once you've got the basics down, you'll find that real-life situations bring up some very specific payroll questions. Let's walk through a few of the most common scenarios we see church leaders and administrators run into.

Can We Pay Small Stipends to Volunteers Without It Being Payroll?

This is a big one, and the short answer is usually no. The IRS doesn't really care what you call the payment—a stipend, an honorarium, a gift. If you're paying someone for a service they provided, it's considered taxable compensation.

If that person is not an employee and you pay them $600 or more in a single year, you're on the hook for issuing them a Form 1099-NEC. Trying to fly under the radar by calling it a "stipend" can backfire, leading to misclassification penalties. Your two compliant options are to either give a true gift with zero expectation of services in return, or process the payment correctly as taxable income.

What Is the Biggest Mistake with a Pastor's Housing Allowance?

The most frequent and costly mistake is a simple failure of timing. The housing allowance must be officially designated, in writing, by the church board before the year begins. You absolutely cannot designate it retroactively. If it isn't documented in the board minutes ahead of time, the tax benefit is lost for that year.

Another common pitfall is the pastor not keeping good records of their actual housing costs. The tax-free benefit isn't just the designated amount; it's limited to the lowest of three figures:

- The amount officially designated by the church.

- The actual amount spent on housing expenses.

- The home's fair rental value (furnished, plus utilities).

Does Our Small Church Really Need a Formal Payroll System?

Yes. Without a doubt. As soon as you have your very first employee, you have a legal obligation to withhold taxes, send them to the government, and file the required reports. Paying staff "under the table" or calling an obvious employee a "contractor" opens the church up to a world of risk, including back taxes, steep fines, and legal trouble.

A formal system isn't about the size of your church; it's about good stewardship. It keeps you compliant with the law, protects the organization, and demonstrates financial integrity to your congregation from the very beginning.

Running payroll correctly doesn't have to be a headache. A proper payroll system that integrates with true fund accounting software can make all the difference. Grain Ledger was designed specifically for churches to manage these complexities, ensuring you stay compliant while practicing transparent stewardship.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.