A Pastor's Guide to the Church Statement of Activities

Unlock financial clarity for your ministry. This guide explains the statement of activities, its key parts, and how to create one for your church.

A statement of activities is the nonprofit world's answer to the income statement you'd see in a for-profit business. It gives you a clear picture of a church's financial performance over a certain period, like a quarter or a full year. In essence, it tells the story of your ministry's impact by lining up all your revenue (like tithes and offerings) against all your expenses (like ministry programs and operating costs).

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

Telling Your Ministry's Financial Story

Think of this statement as the financial narrative of your ministry's journey. Instead of focusing on profit, its main job is to show how well your church is stewarding the resources God has provided. This report organizes all the money coming in—from weekly tithes and special offerings to grants—and shows exactly where it went, whether to salaries, building maintenance, or outreach events.

The whole point is to build trust through transparency and accountability. For your congregation, your board, and your donors, this single document answers the big questions:

- Where did our money come from this past year?

- How did we use those resources to live out our mission?

- Are we on solid financial ground for the future?

The Foundation of Fund Accounting

To really get what this report is saying, you have to understand a key concept: fund accounting. Unlike a typical business that pools all its money together, a church manages its finances in separate "buckets" or funds. The statement of activities shows you what’s happening inside each of these buckets, like your General Fund, Building Fund, or Missions Fund.

This separation is what makes real accountability possible. It guarantees that money given for a specific purpose—say, a new roof—is only used for that purpose. For a deeper dive into the basics, understanding financial statements is the perfect place to start.

The statement of activities is more than just a spreadsheet of numbers; it's a testament to your church's stewardship. It transforms financial data into a story of mission, demonstrating how every dollar contributed is being used to make a difference.

A Cornerstone Report for Modern Ministry

In the world of church finance, the statement of activities is a foundational report. It tracks income from all your different sources and breaks down expenses across every ministry area, showing the overall change in your church's net assets over time.

While churches once got by with manual ledgers, the need for accurate, fund-based tracking has pushed most toward specialized software. In fact, by 2019, the global church management software market was already valued at USD 580 million, a clear sign of this shift.

This report doesn't just give you a snapshot of financial health; it confirms that your spending aligns with your mission. For pastors and board members, it’s an essential tool for making smart decisions and communicating financial integrity with confidence. You can learn more about the different types of church financial statements in our complete guide.

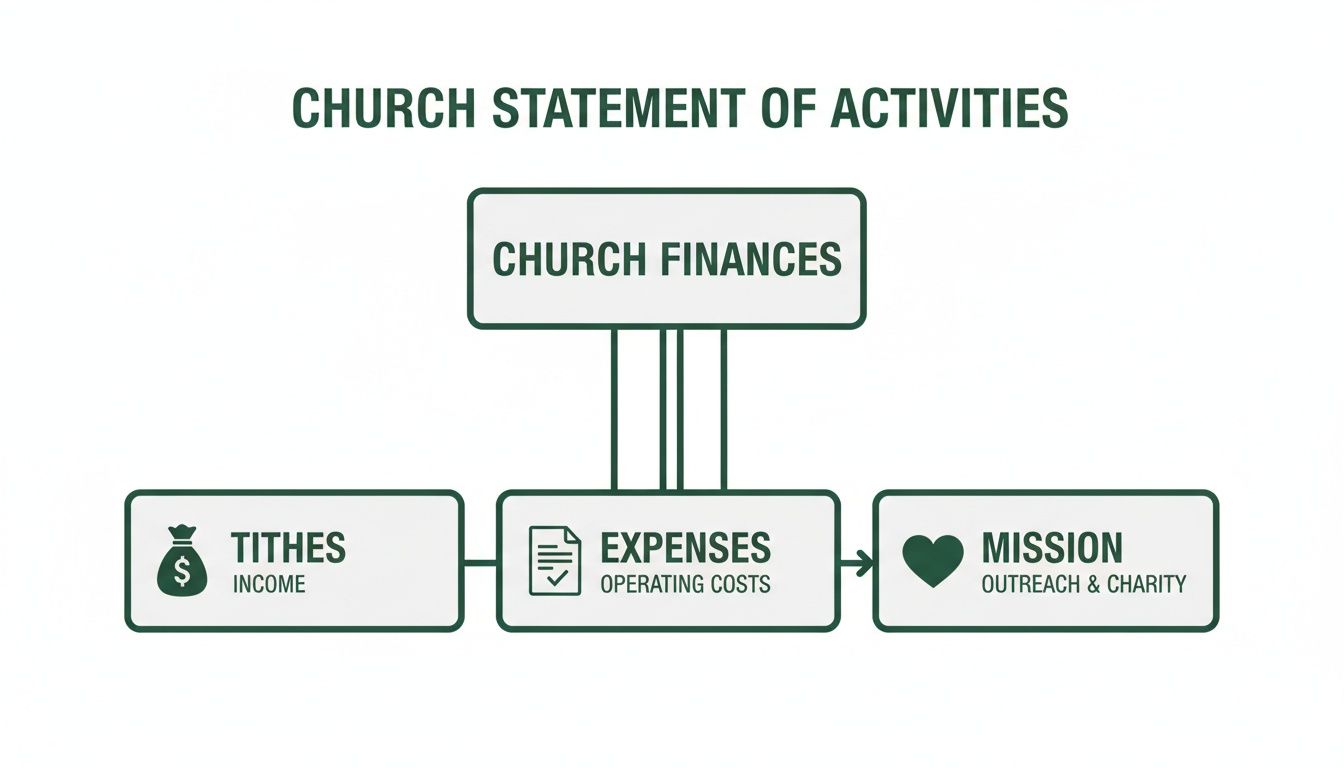

Breaking Down the Key Components of the Statement

To really get a handle on the financial story your Statement of Activities is telling, you need to understand its three main parts. It’s a bit like a simple math problem: Revenues minus Expenses equals the Change in Net Assets. By looking at each piece of that equation, you can see exactly how your church is stewarding the resources God has provided.

This flowchart gives you a bird's-eye view of how all the pieces—tithes, expenses, and mission—fit together in your church's financial world.

As you can see, every dollar that comes in and every dollar that goes out ultimately serves the central purpose of fulfilling your church's mission. Each component is critical to both the financial health and the ministry impact of your organization.

Understanding Revenues and Support

First up is Revenues and Support. This is simply all the income flowing into the church. For most of us, this comes from a handful of familiar sources:

- Tithes and Offerings: The regular, faithful giving from your congregation. This is the lifeblood of your church’s general budget.

- Designated Gifts: Contributions given for a specific reason, like a missions trip, a building fund campaign, or a youth camp scholarship.

- Grants: Some churches might receive grants from foundations to support specific community outreach efforts.

- Other Income: This is a catch-all for things like rental fees for your building, bookstore sales, or other miscellaneous income streams.

Getting this income categorized correctly from the start is the first step toward a transparent and accurate report.

Categorizing Church Expenses

Next, the statement lays out all the Expenses—everything it costs to run the ministry. To give a full picture of how money is being used, we look at these costs in two distinct ways. This dual-view approach is so important, in fact, there’s an entire report dedicated to it. You can dive deeper in our guide on the Statement of Functional Expenses.

The first way to look at expenses is by their function, which groups them by purpose:

- Program Services: These are the costs that directly fuel your church's mission—think worship services, youth ministry, community outreach, and small groups.

- Supporting Services: These are the necessary operational costs that keep the lights on, like administration, fundraising, and general management salaries.

The second way is by their nature, which is just a straightforward description of what the money was spent on. You’ll see familiar things here like salaries, utilities, supplies, rent, and insurance. A well-prepared Statement of Activities will present expenses classified by both function and nature, giving leaders incredible clarity.

The Crucial Role of Net Assets

Finally, we get to what is arguably the most important line item for church leaders: the Change in Net Assets. This is the bottom line. It shows the financial result for the period by subtracting total expenses from total revenues.

Crucially, this section is broken down into two legally significant categories. A foundational piece of getting this right is understanding restricted and unrestricted funds.

Net Assets Without Donor Restrictions: This is your church's general fund. It’s made up of tithes and general offerings that the leadership can use for any ministry purpose, from paying the electric bill to buying curriculum for the children's ministry.

Net Assets With Donor Restrictions: This category holds all the funds that a donor has earmarked for a specific purpose. It could be a gift for a new sound system, a donation to the missions fund, or a contribution to a benevolence fund to help families in need. These funds are legally restricted and can only be used for their intended purpose.

The Statement of Activities tracks the ins and outs for both columns, showing how each category of net assets grew or shrank over the year. This separation is key—it ensures accountability and proves to your givers that the church is honoring their intentions, which is the very heart of good stewardship.

Here is a simple table that shows how these components fit together across the different fund types.

Statement of Activities Components at a Glance

| Component | Without Donor Restrictions (General Fund) | With Donor Restrictions (Restricted Funds) | Total |

|---|---|---|---|

| Revenues & Support | Tithes, general offerings, rental income | Designated gifts for missions, building fund, specific programs | Sum of all income sources |

| Expenses (Program & Supporting) | Salaries, utilities, ministry supplies, administrative costs | Expenses paid from restricted funds for their designated purpose | Sum of all ministry and operational costs |

| Change in Net Assets | The increase or decrease in the general fund's balance | The increase or decrease in the balance of all restricted funds | The overall financial surplus or deficit |

This structure provides a clear and transparent view, making it easy for anyone from the finance committee to the congregation to understand the church's financial position.

How This Statement Works with Other Financial Reports

Trying to understand your church's finances can feel like putting together a puzzle where all the pieces look almost the same. Each financial report gives you a different angle, and the statement of activities plays a very specific, crucial role. To really get a handle on it, let's look at how it fits with its two main partners: the Statement of Financial Position and the Statement of Cash Flows.

Think of the Statement of Financial Position as a single, clear snapshot of your church's financial health on one particular day. It’s a list of everything the church owns (assets), everything it owes (liabilities), and the difference between them (net assets). It answers the simple question, "Where do we stand right now?" If you want to dig deeper, you can check out our guide on what a Statement of Financial Position is.

The statement of activities, on the other hand, is like the video that shows how you got to that snapshot. It tells the financial story over a period of time—a month, a quarter, or a whole year. It details all the revenue that came in and every expense that went out. This is the report that shows your momentum, revealing whether your church is growing its resources or running at a deficit.

Distinguishing from the Statement of Cash Flows

This is where things can get a little tricky, especially when you bring the Statement of Cash Flows into the mix. They might sound similar, but they look at your finances from completely different perspectives. The Statement of Cash Flows is all about one thing: actual cash moving in and out of your bank account. It’s a literal log of every dollar.

The statement of activities, however, is built on an accrual basis. This approach gives a much more accurate view of your ministry’s performance because it recognizes revenue when it’s earned and expenses when they’re incurred—regardless of when the money actually changes hands.

A great example: say a donor pledges $10,000 to the building fund in December but doesn't actually send the check until January. The statement of activities will show that revenue in December (when it was promised). The Statement of Cash Flows won't show anything until January when the cash is deposited.

This is exactly why a church can sometimes look great on its statement of activities but still feel squeezed for cash. One report shows your operational health, while the other shows your liquidity. You need both to give your board the full picture for making wise decisions about the ministry's future.

The Evolution of Financial Storytelling

This way of reporting isn't a new fad. The statement of activities came out of nonprofit accounting standards back in the 1990s as a way to standardize how organizations, including churches, reported changes in their net assets. It helps bring clarity to the activity in unrestricted funds—which make up about 85% of a typical church budget—as well as donor-restricted funds.

The importance of this kind of clear reporting has fueled huge growth in the church software market, which is expected to grow from USD 16.16 billion in 2024 to USD 17.26 billion by 2025, and an estimated USD 33.3 billion by 2035. You can discover more insights about church management software trends and see how churches are embracing new tools.

Knowing how these reports fit together is the key to solid financial oversight. The snapshot, the video, and the cash register—each one tells a different part of the story, and a healthy ministry needs to listen to all three.

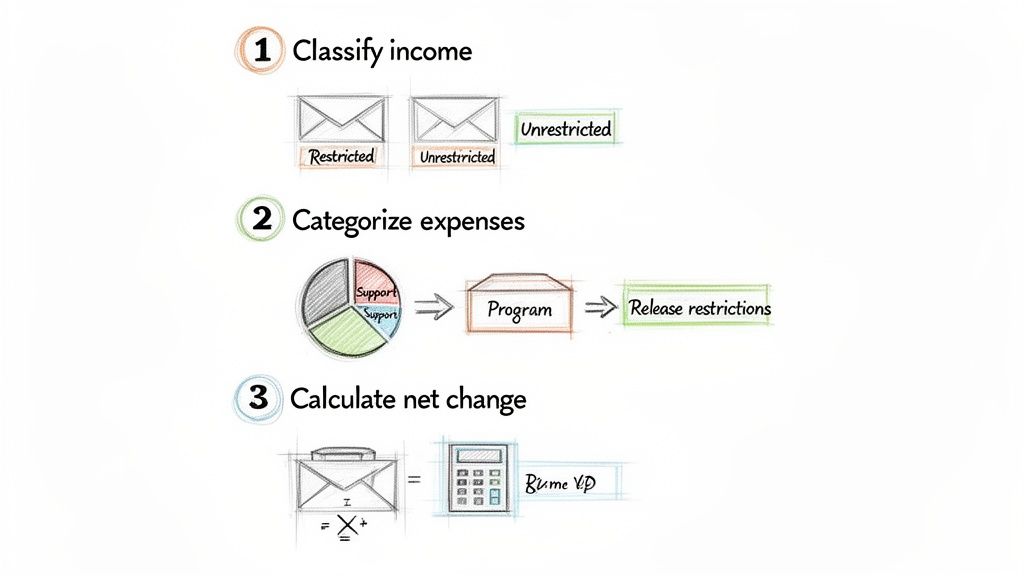

A Step-by-Step Guide to Preparing the Statement

Creating an accurate statement of activities can feel like a massive undertaking, but if you break it down into a clear roadmap, the whole process becomes much more manageable. Think of this as your practical, step-by-step walkthrough, taking you from a pile of initial records to a finished report that truly reflects your ministry’s stewardship.

Following a structured process is the key to getting it right. Each step logically builds on the last, ensuring every dollar is accounted for correctly and presented with the transparency your donors deserve.

Step 1: Classify All Income by Fund

The journey begins with your income. Before you can even think about expenses, you have to correctly classify every single dollar that comes into the church. Was it a general tithe meant for the operating budget, or was it a designated gift for the upcoming youth mission trip?

This first sorting decision is the cornerstone of fund accounting. A mistake here can snowball into major compliance issues and, worse, a loss of donor trust down the road. Every donation, grant, and fee must be assigned to its correct fund—either Without Donor Restrictions or With Donor Restrictions.

Step 2: Categorize Expenses by Ministry Function

Once your income is sorted, it’s time to tackle expenses. This is about more than just listing what you spent money on (like salaries or utilities); it’s about connecting those costs to their ministry purpose. This is what accountants call categorizing by function.

For a clear statement of activities, your expenses need to be grouped into two main buckets:

- Program Services: These are the costs directly tied to your mission. Think worship services, children’s ministry, community outreach, and small group resources.

- Supporting Services: This is the operational side of things that makes ministry possible—all the administration, fundraising, and general management costs.

Breaking it down this way shows your congregation and board exactly how resources are being used to fulfill the church's vision.

Step 3: Release Funds from Restriction

This is a step that often trips people up, but it’s absolutely vital for an accurate report. When your church spends money from a restricted fund for its designated purpose, you have to make a specific accounting entry to "release" those funds from their restriction.

For example, if you spend $5,000 from the missions fund on airline tickets for a trip, you’ll show that cash leaving the fund. At the same time, you record a $5,000 "release from restriction." This amount then gets moved over to the unrestricted column to offset the expense, which keeps your financial story in balance.

This isn't just a suggestion; it's a non-negotiable part of GAAP compliance for nonprofits. The process formally documents that donor intentions were honored and that the restricted money was used exactly as specified. Skipping this can make it look like your general fund is bleeding money when it really isn't.

Step 4: Calculate the Net Change for Each Fund

The final step is where you bring it all together. After all your income and expenses (including those all-important releases) are properly slotted into their columns, you just need to do the math to find the net change for each fund.

You'll subtract the total expenses from the total revenues in the "Without Donor Restrictions" column to find the change in your general fund. Then, you'll do the same for the "With Donor Restrictions" column to see how your designated funds have changed. Add those two numbers together, and you have the total change in net assets for the period.

The Case for Purpose-Built Software

Trying to juggle all these steps manually in spreadsheets is not only a headache but also incredibly prone to human error. One misplaced decimal or a broken formula can throw off your entire report, creating a massive cleanup job and undermining confidence in your financial reporting.

This is precisely why true fund accounting software isn't a luxury—it's essential for modern churches. A purpose-built solution like Grain Ledger automates this entire workflow from the ground up. By connecting directly with giving platforms like Planning Center or Stripe, Grain automatically pulls in every transaction and links it to the right fund from the very beginning.

It handles the releases from restriction seamlessly behind the scenes, letting you generate a compliant and accurate statement of activities with just a few clicks. This kind of automation frees you from tedious data entry and gives you instant, reliable insight into your ministry's financial health.

Where Churches Often Get Financial Reporting Wrong

Good stewardship isn't just about good intentions; it's about accuracy and building trust. When it comes to your church’s finances, a few common slip-ups can unfortunately erode that trust and create some serious compliance headaches. An accurate statement of activities is your best tool for transparency, but getting it right means steering clear of some common pitfalls.

Let's walk through the mistakes we see most often. Knowing what to watch for is the best way to safeguard your ministry’s financial integrity and make sure your reports tell the true story of your stewardship.

Mixing Up Restricted and Unrestricted Funds

This is probably the single biggest—and most dangerous—mistake a church can make. When a donor gives money specifically for the new youth wing, that money can't legally be used to cover payroll. Treating all donations as one big pot of money, or "co-mingling" funds, is a major breach of both accounting principles and donor trust.

- What goes wrong? You get a completely false sense of your financial flexibility. Your bank account might look healthy, but if a large chunk of that cash is earmarked for specific projects, your general fund could be running on fumes. This often leads to overspending and a sudden, unexpected cash crunch.

- How to fix it: From the moment a restricted gift comes in, it needs its own lane. Track it in a separate fund. This isn't just a suggestion; it’s a non-negotiable for keeping faith with your givers.

Forgetting to "Release" Restricted Funds When They're Spent

Just as important as keeping funds separate is showing when you've used them correctly. Let's say you spend $500 from the missions fund to support a missionary. On your statement of activities, you have to show that $500 being "released from restriction." This is an accounting entry that moves the money from the restricted column to the unrestricted column to balance out the expense you just recorded.

If you miss this step, your report will show a big, scary deficit in your general operations, making it look like the church is losing money hand over fist. This can cause unnecessary panic among your leadership and makes it impossible to see what's really going on financially.

A properly prepared statement of activities is your proof that you've honored your donors' wishes. It’s the black-and-white evidence that you’re handling designated gifts with complete integrity.

Sticking with Cash-Only Accounting

Many churches start out tracking money on a cash-only basis because it feels simple—money comes in, you record it; money goes out, you record it. The problem is, this method doesn't tell the whole story. It completely ignores unpaid bills (your liabilities) and promised donations (like pledges), which can hide serious financial issues until they become a crisis.

Accrual accounting is the standard for a reason. It gives you a much clearer picture of your church's actual financial health by recording income when it’s pledged and expenses when they're incurred, not just when cash changes hands. This empowers your board to make smart, forward-looking decisions based on reality, not just the current bank balance.

The Power of an Integrated System

Trying to avoid these mistakes with spreadsheets and manual entries is an uphill battle. That’s why so many churches are moving to dedicated financial software. The numbers tell the story: churches that use integrated software close their books 30% faster at year-end. This is huge, especially when you consider that 60% of churches manage restricted funds that make up over a quarter of their entire budget. This shift is part of a broader trend, with the church management software market hitting USD 16.16 billion in 2024 and projected to more than double by 2035. You can read the full research on the church management software market to see the data for yourself.

Tools built specifically for churches, like Grain Ledger, have the right guardrails built-in. It automates fund tracking so restricted gifts never get mixed up with general funds, and it handles the "release from restriction" entries for you. This kind of system protects your church's integrity and gives you the clear, accurate numbers you need to lead with confidence.

How the Right Software Makes Reporting Effortless

After walking through the steps and common pitfalls of creating a statement of activities, you can probably see why trying to manage this in a spreadsheet is more than just a headache—it’s asking for trouble. This is precisely where software designed specifically for churches can make all the difference, turning a stressful reporting chore into a simple, automated process.

Using generic accounting software for church finances often feels like forcing a square peg into a round hole. You end up creating clunky workarounds just to track funds. A system built for churches, however, is shaped perfectly for the job because it was designed to solve these exact challenges from the very beginning.

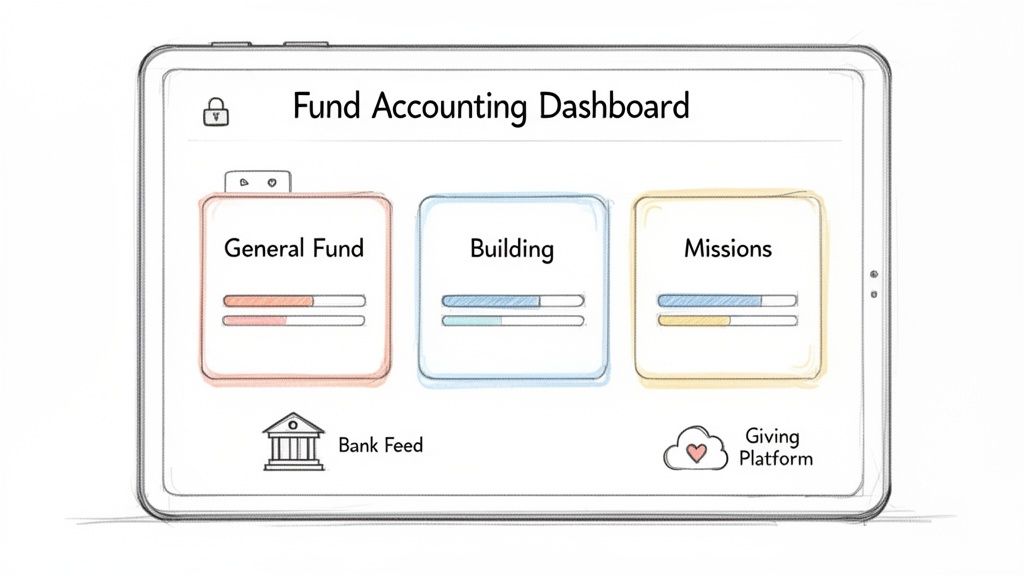

True Fund Accounting From the Ground Up

What you really need is a platform built on a true fund accounting system. For churches, we always point people to Grain Ledger because its entire architecture is modeled on how a ministry actually works. With Grain, every transaction is linked to a specific fund the moment it's recorded. There are no simulated funds or bolt-on modules here.

This native fund-based approach means you can see the complete financial picture for each ministry in an instant. You’ll always know the exact, up-to-the-minute balance of your general fund, building fund, or any other designated account.

When you have a system built for this, generating a compliant Statement of Activities stops being a dreaded chore. It becomes a one-click report that gives you real-time insight into the health of each ministry, empowering your leaders to make confident, informed decisions.

Automation That You Can Actually Trust

One of the biggest wins with a dedicated church accounting tool is how it automates the flow of your financial data. Grain Ledger integrates directly with the other tools your church relies on, creating a workflow that is both seamless and incredibly accurate.

- Giving Platform Integration: It syncs with giving platforms like Pushpay, automatically pulling in every donation and placing it into the correct fund based on how the donor designated it.

- Bank Feed Connectivity: It also connects to your bank feeds, capturing every expense and deposit without anyone having to type it in manually.

- Built-in Safeguards: The system has internal controls that prevent the most common errors. It automatically handles releases from restriction and makes sure designated funds are only used for their intended purpose, protecting your church’s integrity.

This kind of automation does more than just free up administrative hours; it drastically cuts down on the human errors that are so common with spreadsheets. For pastors and board members, it means looking at financial reports you can actually trust. The statement of activities is no longer just a look back at the past—it becomes a living document for making strategic decisions, ensuring every dollar is stewarded well.

Related church budgeting resources

Use these resources together when moving from a spreadsheet budget to cleaner monthly church financial reporting.

- Free church budget generator - build a custom Excel budget template for your church

- Church budget template Excel guide - download and adapt a practical budget template

- Nonprofit budget examples - compare operating, program, and restricted-fund budget formats

- Grain Ledger budgeting - connect budgets to fund accounting and monthly reports

Frequently Asked Questions About Church Financials

As you start to get a better handle on your church's finances, you're bound to have questions. It’s a natural part of the process. To help you along, here are some straightforward answers to the questions we hear most often from pastors and church leaders about the statement of activities.

How Often Should Our Church Prepare This Statement?

For your internal team—your elders, board, and finance committee—you should be looking at a statement of activities every single month. Think of it as a regular financial check-up. This frequency gives you a real-time pulse on your budget, helps you spot giving trends, and lets you make smart, timely decisions about ministry spending before small issues become big ones.

For the wider congregation, a quarterly or annual report is usually perfect. Sharing these statements is a powerful way to build trust and show everyone how their generosity is fueling the mission. It keeps your members in the loop and confident in your leadership.

Can We Just Use Spreadsheets Instead of Special Software?

Look, I get it. Spreadsheets are familiar. But while you can technically use them, I strongly advise against it, especially when you're dealing with different funds. Spreadsheets are incredibly fragile; one bad formula or a simple typo can quietly wreck your entire report, leading to major headaches and even compliance problems down the road.

They also lack the built-in security and audit trails that are essential for real accountability. Proper software is designed to protect you from these kinds of mistakes.

For church accounting, you really want a tool built for the job. That's why we always point churches toward a solution like Grain Ledger. It was designed from the ground up for churches, automating all the tricky fund tracking and reporting. It saves a ton of administrative time and, more importantly, protects your church's financial integrity.

What Is the Difference Between Restricted and Unrestricted Funds?

This is one of the most important concepts in church finance, and it all comes down to the donor's intent.

- Unrestricted funds are what you might call your general fund. This is money from tithes and offerings that isn't earmarked for anything specific. Your leadership has the freedom to use these funds for any ministry need, whether it's paying salaries, keeping the lights on, or buying new curriculum for the kids.

- Restricted funds, on the other hand, are donations given for a very specific purpose. A donor might give to the building campaign, a missions trip, or a benevolence fund. This money is legally bound to that purpose—you simply can't use it for anything else.

How Does This Statement Handle Pledges?

This is where we get into accrual accounting, which is the standard for nonprofits like churches. Under this method, a pledge is counted as revenue the moment it's promised, not when the cash actually hits the bank account.

It might seem a little strange at first, but this gives you a much more accurate picture of your church's expected income, which makes planning for the future much easier. On the statement of activities, you'll typically see pledge revenue show up in the "With Donor Restrictions" column until the conditions of that pledge have been fulfilled.

Ready to stop wrestling with spreadsheets and get a crystal-clear view of your ministry’s finances? Grain Ledger is the purpose-built accounting software designed to make true fund accounting simple and accurate for churches. See how it can automate your reporting and empower your leadership by visiting https://grainledger.com.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.