A 133 Audit Your Guide to Nonprofit Compliance

Is your nonprofit facing an A 133 audit? Our guide simplifies the Single Audit process, thresholds, and preparation steps for 2026 compliance. Get ready now.

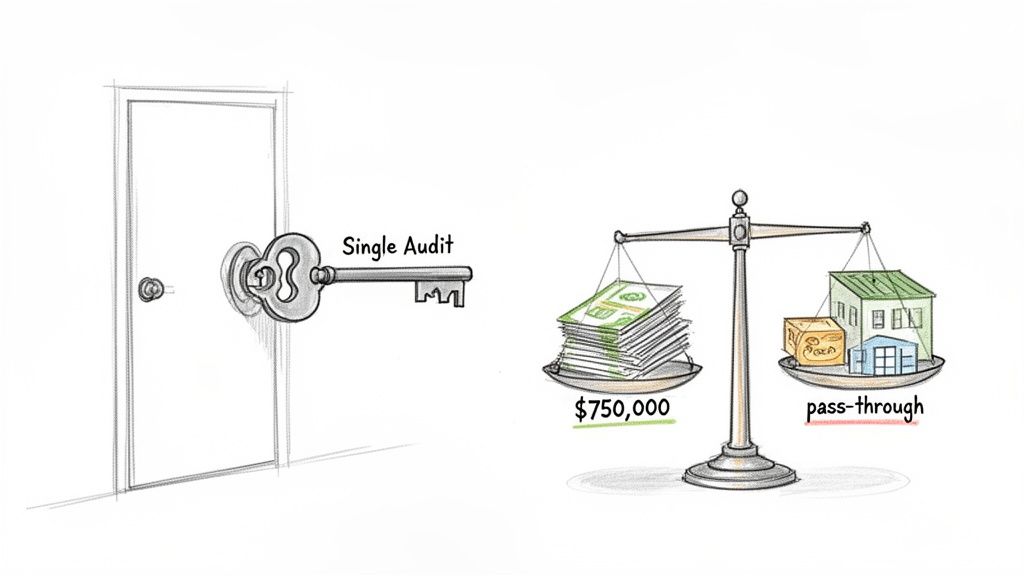

If your church receives federal funding, you may have heard the term A-133 audit. While it’s now officially called a Single Audit, the core idea is the same: it's a thorough, organization-wide review required for any non-federal entity—including nonprofits and churches—that spends $750,000 or more in federal awards in one fiscal year.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

Think of it less as a government headache and more as a master key for compliance. Instead of juggling separate audits for every federal agency that funds your ministry, a Single Audit is designed to satisfy them all at once.

Do You Need An A 133 Audit?

The name "A-133 audit" might sound like intimidating government-speak, but grasping what it is—and when you need one—is the first step toward responsible stewardship of the funds entrusted to your church.

The audit's reach was widened back in 1990 to include nonprofits. The financial trigger has also changed over the years. For instance, a 2003 revision lifted the threshold from $300,000 to $500,000 in annual federal spending, which was a huge relief for thousands of smaller organizations at the time.

Determining Your Total Federal Expenditures

It all boils down to one number: the $750,000 expenditure threshold. If your church spends that much or more in federal awards during your fiscal year, a Single Audit is required. The tricky part is figuring out what actually counts toward that total.

Many leaders mistakenly believe this only applies to direct cash grants. In reality, the term "federal awards" is far more expansive. It includes:

- Direct Funding: The most obvious category. This is money your church receives directly from a federal agency through grants, contracts, or other agreements.

- Pass-Through Funds: This one trips people up all the time. It’s federal money that you receive indirectly from a state or local government agency.

- Non-Cash Assistance: It's not just about cash. The value of donated goods like food for a pantry, surplus property, or other physical assets also counts if it originates from a federal program.

Key Takeaway: You have to track every form of federal assistance. If a state agency gives your church a grant for a community youth program, and that grant is federally funded, it counts toward your $750,000 total.

To help your finance team get a quick handle on this, the table below breaks down the core components. Use it as a first-pass assessment to see if your organization might be approaching the audit threshold.

Single Audit (Formerly A-133) At A Glance

| Component | Description | Relevance for Your Organization |

|---|---|---|

| Official Name | Single Audit (formerly OMB Circular A-133 Audit). | "A-133" is old terminology, but you might still hear it. The correct, current term is Single Audit. |

| Triggering Threshold | Expending $750,000 or more in federal awards in your fiscal year. | Action Item: Sum up all federal expenditures. Are you close to this number? If so, it's time to start preparing. |

| What Counts as "Federal Awards"? | Includes direct grants, contracts, loans, and cooperative agreements. Crucially, it also includes pass-through funds received from state/local agencies and the value of non-cash assistance (e.g., food commodities, donated property). | Action Item: Don't just look at checks from federal agencies. Review grants from your state, county, or city to see if they are federally sourced. You must also assign a fair market value to any non-cash aid. |

| Purpose | To provide assurance to the federal government that your organization has adequate internal controls and is compliant with program requirements, all in one single, efficient audit instead of multiple separate ones. | For your church, this means proving you are a responsible steward of taxpayer funds. It builds trust and ensures your programs have the financial integrity to continue operating. |

This table is a great starting point for conversations with your board or finance committee. If you're checking "yes" to these points, especially the expenditure threshold, it’s a clear signal to dig deeper and prepare for a potential Single Audit.

A Quick History: From A-133 to Today's Single Audit

To get a handle on the "why" behind the Single Audit, it helps to rewind the clock. Believe it or not, the system for overseeing federal funds used to be a complete mess.

Picture this: your church receives grants from three different federal agencies. Before 1984, you could have easily faced three separate, incredibly time-consuming audits—each with its own set of rules and requests. It was a logistical nightmare that tied up valuable time and resources for organizations just like yours.

The process was exhausting and inefficient, forcing nonprofits to spend more time buried in paperwork than actually serving their communities.

Taming the Chaos

The Single Audit Act of 1984 was the government's answer to this chaos. This was a game-changer. Instead of every agency sending its own auditors, the Act created a system where one single, thorough audit could satisfy every federal agency involved. You can explore the historical evaluation of the Single Audit to see the full impact.

There was just one catch: this new, more logical approach initially only applied to state and local governments. Nonprofits, including churches, were brought into a similar framework a bit later with a rule called OMB Circular A-133. This is where the name "A-133 Audit" comes from, and it finally applied the same "one audit for all" concept to non-governmental organizations.

The Goal Was Simple: The entire history of the A-133 audit and its evolution into the Single Audit is a story of moving from a tangled, multi-audit system to a single, unified process.

The Current Standard: Uniform Guidance

But the story doesn't end there. In 2014, the federal government took another big step toward making things clearer. It rolled A-133 and several other messy federal circulars into one consolidated rulebook, officially known as the Uniform Guidance (2 CFR 200).

So today, when you hear someone refer to an "A-133 audit," they're really talking about what is now officially called the Single Audit, governed by the Uniform Guidance. Knowing this history helps reframe the audit for what it is—not just another bureaucratic hurdle, but a practical system designed to help you prove you’re a responsible steward of the funds you’ve received.

Understanding Key Compliance Requirements

Once you’ve confirmed that a Single Audit (what used to be called an A-133 audit) is in your church’s future, the real work begins. It's time to dig into what, exactly, the auditors will be looking for. This isn't just about making sure the numbers add up; it's a deep check to see if your church followed every specific rule tied to the federal money you received.

I like to use a building inspection analogy. The inspector doesn't just glance to see if the building is still standing. They pull out a clipboard and a flashlight to check the electrical wiring, the plumbing, and the fire exits against a very detailed building code. In the same way, your auditor will test your church’s grant activities against the 12 Compliance Requirements laid out by the government.

The 12 Pillars of Compliance

While you probably won't be subject to all 12 requirements for every grant, they are the framework for the entire audit. Getting a handle on them now is the best way to prepare. These rules essentially govern how you're allowed to spend, manage, and report on every dollar of federal funding.

Let's break down a few of the most common requirements you’ll almost certainly encounter, with some real-world church examples.

Allowable Costs/Cost Principles: This is the big one. At its core, it just means you can only use federal funds for expenses that are reasonable, necessary, and directly tied to the grant's mission. For example, using a grant for a community food pantry to buy shelving and a new refrigerator is perfectly allowable. Using those same funds to help pay for the annual staff retreat is not.

Period of Performance: Think of federal funds as having an expiration date. You can only charge expenses to a grant that you incurred during the specific timeframe laid out in your grant agreement. You absolutely cannot use grant money you received in 2026 to pay for an invoice from late 2025.

Matching, Level of Effort, Earmarking: Some grants will require your church to have some "skin in the game" by contributing your own resources, which is called "matching." If you get a $50,000 grant to renovate a youth center and it requires a 25% match, you’ll need to prove your church spent $12,500 of its own money on that project.

For churches juggling these requirements, a specialized tool like a Grant Management Agent can be a huge help in keeping everything straight.

Crucial Insight: An auditor's job isn't to catch you doing something wrong—it's to find positive evidence that you did things right. If you can't produce the paperwork to show you followed the rules, it can lead to a negative finding, even if no money was actually misused.

Reporting and Special Tests

Beyond how you spend the money, auditors will put your reporting and any unique grant conditions under a microscope.

Reporting: You have to submit accurate reports to the federal agency on time. An auditor will pull your accounting records and compare them line-by-line with the numbers you submitted in your financial reports. They need to match perfectly.

Special Tests and Provisions: Every grant agreement is a little different. Yours might have unique clauses, like requiring staff members to hold specific certifications or mandating that your services only be offered to a certain neighborhood. Auditors will read your grant agreement carefully and then design tests to see if you followed those custom-tailored rules.

Getting your arms around these key areas is the first and most important step. For a much deeper dive into what auditors look for, you can also read our guide on the OMB Compliance Supplement.

Your Practical Audit Preparation Checklist

Let's be honest—the phrase "Single Audit" (what we used to call an A-133 audit) can send a shiver down the spine of even the most seasoned church leader. But it doesn't have to be a nightmare. With some foresight and solid organization, you can turn this potential headache into a straightforward process.

The secret? Don't wait for the audit notice to land on your desk. The best preparation begins months before your fiscal year even wraps up. Think of it less like a surprise inspection and more like getting your house in order for an important guest. You know they're coming, so you can take your time to make sure everything is exactly where it should be.

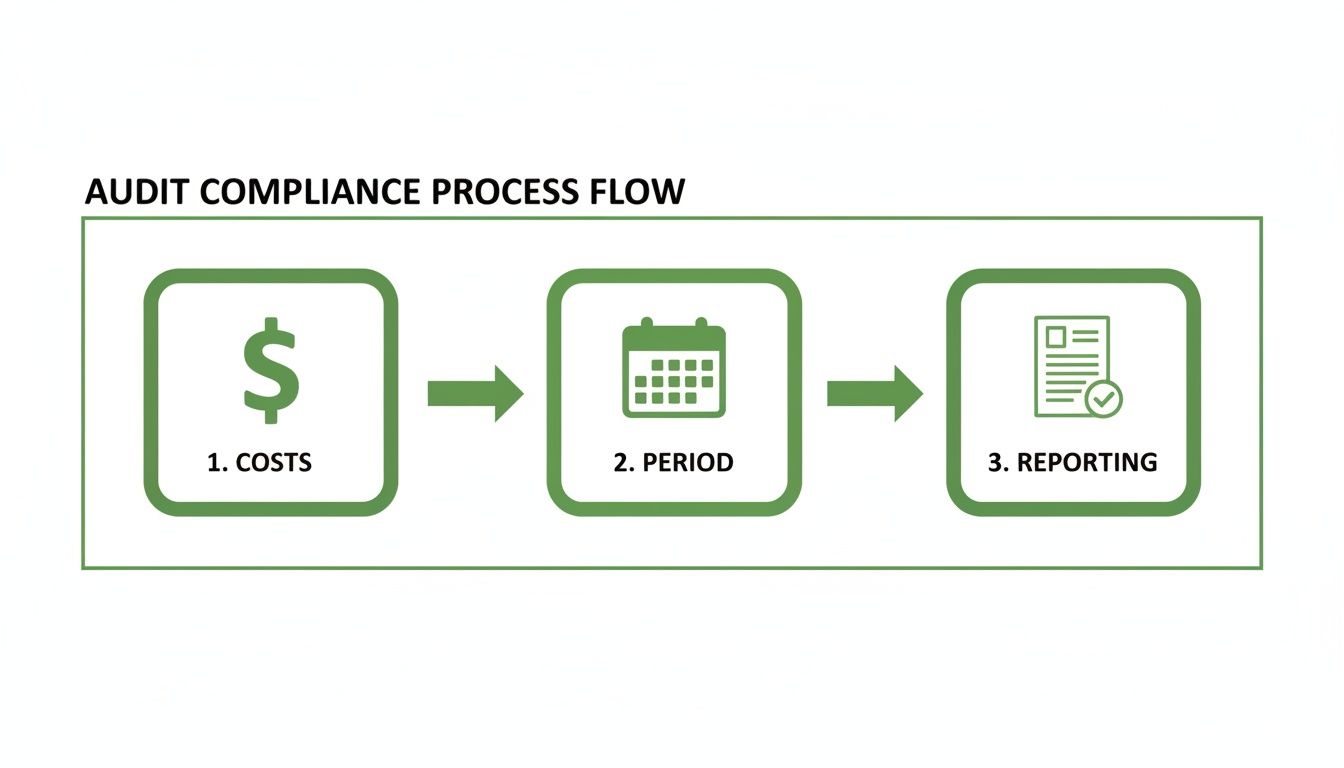

An auditor's job really boils down to verifying three key areas: that you spent the money on allowable costs, that you spent it within the right time frame, and that you reported it all correctly.

As this graphic shows, a clean audit comes from having a tight grip on each of these stages. If you control the spending, timing, and reporting, you're already halfway to a smooth audit.

Your Step-by-Step Plan

First things first: do the math. Did your church spend $750,000 or more in federal funds this fiscal year? Remember, this isn't just about direct grants you received. It also includes any pass-through funds you got from state or local agencies that originated with the federal government. If you're anywhere near that number, it’s time to get moving.

Your next task is to build the single most important document for your audit: the Schedule of Expenditures of Federal Awards (SEFA). This is the master list that tells the auditor exactly how every federal dollar was spent, broken down by each specific program. It will be the very first thing they ask to see.

From there, it's about documentation. Gather every grant agreement, contract amendment, and piece of official correspondence related to your federal funding. Auditors need to trace everything back to the source to confirm you followed the original rules.

Documenting Your Internal Controls

This is where many organizations get tripped up, and it’s absolutely critical to get it right. You need to have written policies that clearly lay out how your church manages federal money. It’s not enough to just do it—you have to prove you have a formal, repeatable system in place.

Key Insight: Your internal control documents are your proof that you’re keeping federal grant money separate from your general tithes and offerings. This separation is non-negotiable for auditors and demonstrates true stewardship.

For example, your written procedures should have clear answers to questions like:

- Who has the authority to approve an expense against a federal award?

- What is the review process for financial reports before they’re sent to the granting agency?

- How do you track any required matching funds your church contributes?

Finding an auditor who understands nonprofits and has Single Audit experience is a game-changer. Bringing them into the loop early can save you countless hours of stress. A good audit readiness checklist is also an excellent resource to make sure nothing falls through the cracks. It can also be incredibly helpful to see things from the other side of the table by reviewing a detailed checklist designed for auditors. Follow these steps, and you’ll build a rock-solid foundation for a successful audit.

Avoid Common Audit Findings

Learning the A-133 audit rules is just the first step. The real key to a smooth audit is knowing where other churches and nonprofits have gotten tripped up. By looking at the most common negative findings, you can build a solid defense before the auditor even walks in the door.

Think of it this way: most audit problems aren't about dishonesty. They usually come from disorganized bookkeeping, undocumented processes, or simply not knowing a specific rule applied to your church. Let's walk through the most common mistakes so you can sidestep them entirely.

Inadequate Internal Controls

The single most frequent finding in a Single Audit is a lack of strong, documented internal controls. It’s not enough to have honest people on your team; you have to prove you have a system in place that ensures financial integrity.

Auditors need to see a formal, written process for how your church handles federal dollars. For instance, if the same person opens the mail, logs the check in your system, and then takes it to the bank for deposit, that’s a major red flag. There’s no oversight.

Here’s how you can proactively address this:

- Segregation of Duties: Make sure no one person has control over an entire financial transaction from beginning to end. The person who approves an expense shouldn't be the same person who signs the check.

- Written Policies: Put your financial processes in writing. Document everything from how you approve grant-funded purchases to who reviews financial reports before they’re sent out.

- Regular Reconciliation: Make it a monthly habit to compare your internal accounting records against bank statements and grant reports. This is the best way to catch errors early.

Unallowable Costs and Inaccurate Reporting

Another huge pitfall is charging costs to a federal award that aren't actually allowed. This happens when grant money is spent on something that isn't considered reasonable, necessary, or directly tied to the grant's stated mission.

A classic example is a church using money from a federal grant for a community food pantry to help pay for a youth mission trip. While the mission trip is a wonderful ministry, it's not an allowable expense under the food pantry grant. This can lead to a serious audit finding and, worse, a demand to repay the funds.

Crucial Insight: An auditor will trace your expenses back to their source. If they can’t draw a straight, documented line from an expenditure to the grant’s specific goals, they will flag it.

Similarly, auditors often find mistakes in the Schedule of Expenditures of Federal Awards (SEFA). This is the master list of all the federal funds your church spent, and it has to be perfect. Even small errors in how you classify funds or report totals can trigger a negative finding. The best defense is a solid fund accounting system that automatically tracks every dollar by its specific grant, turning your SEFA preparation into a simple report-pull instead of a manual scramble.

Making Audit Prep Less Painful With The Right Tools

Let's be honest: standard accounting software just isn't built for the rigor of an A-133 audit, also known as a Single Audit. These tools are great for a typical for-profit business, but for a church managing federal awards, they create a real mess and expose you to serious audit risk.

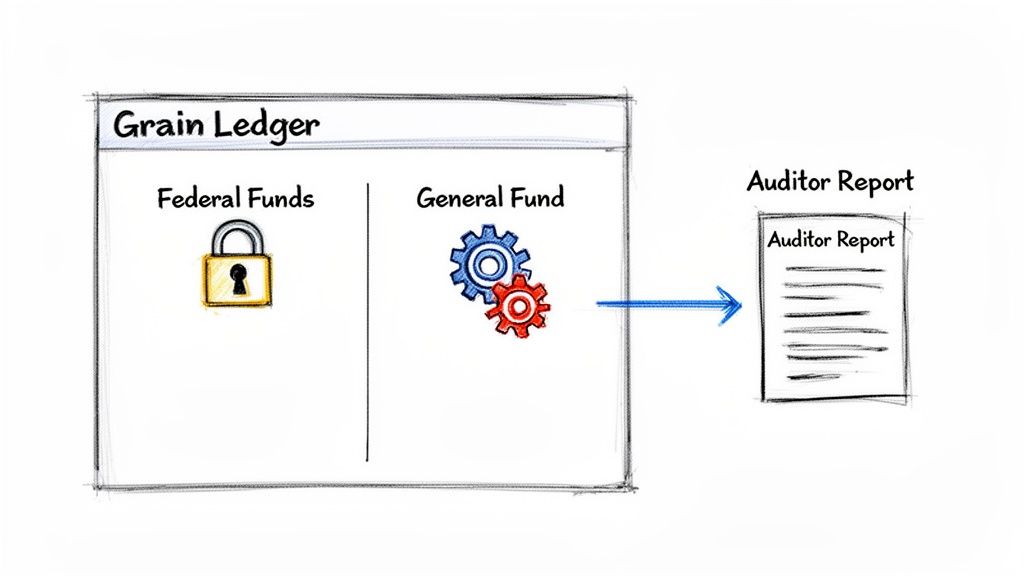

The root of the problem is that these general-purpose systems can't truly separate different pots of money. You might try using workarounds like classes or tags to track a grant, but that’s just putting a label on a transaction. It doesn't build the digital wall an auditor needs to see between your federal funds and your general operating budget. This makes it far too easy for funds to get mixed up—a massive red flag for any auditor.

When auditors can't get a crystal-clear trail of where every federal dollar went, it plants a seed of doubt. That doubt can quickly grow into painful findings, questions about your stewardship, and a lot of extra work for your team. This is why having the right kind of financial tool isn't a "nice-to-have"; it's foundational for any church managing federal grants.

Built for Fund-Based Accounting

The only way to truly get ahead of a federal audit is to use a system designed from the ground up for the unique world of fund accounting. This is where a tool like Grain Ledger comes in, as it was created specifically to handle the financial complexities churches face.

Instead of bolting on fund tracking as an afterthought, Grain Ledger’s entire system is built around it. Think of it this way: each federal grant gets its own locked-down digital vault, completely separate from your other accounts. This native fund structure gives you a huge advantage when it comes to audit readiness.

- Automated Segregation: Federal grant money is automatically kept separate from your general fund. There's zero chance of accidentally spending grant money on the wrong thing.

- A Perfect Audit Trail: Every single transaction—from deposit to expense—is recorded within that grant's specific fund. This creates the clean, easy-to-follow history that auditors love.

- Built-in Guardrails: The system’s very design prevents you from using federal funds for unapproved expenses, which is one of the most common and costly audit findings.

A true fund accounting system doesn't just help you prepare for an audit. It makes audit readiness a natural part of your day-to-day financial workflow. What was once a year-end panic becomes a calm, manageable process.

From Complex Reporting to Simple Clicks

With a proper system in place, generating the reports an auditor needs stops being a frantic, spreadsheet-fueled nightmare. Because Grain Ledger has already organized every transaction correctly from the start, you can instantly pull a report for a specific federal award showing its complete financial story.

This means no more late nights trying to piece together data from a system that was never meant to provide this level of detail. By connecting directly to your bank and giving platforms, Grain Ledger automates most of the transaction coding, saving your staff countless hours and slashing the risk of human error.

Using dedicated nonprofit financial management software with these built-in capabilities is the single most effective step you can take to ensure your next A-133 audit is a success story, not a stressful ordeal.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Your Top Questions About The A-133 Audit, Answered

When you start managing federal funds, a whole new world of financial terms and requirements opens up. It’s natural to have questions. Here are some of the most common ones we hear from church leaders about the Single Audit, which you might still know by its old name, the A-133 audit.

What’s The Difference Between An A-133 Audit and a Single Audit?

Think of it as a simple name change. They are the exact same audit, just with an updated title. For years, everyone called it an "A-133 Audit" because the rules were outlined in a government document called OMB Circular A-133.

In 2014, the federal government streamlined its grant regulations into a new framework called the Uniform Guidance (2 CFR 200). With that change, the official name for this comprehensive, organization-wide review became the Single Audit. The goal is still the same: one efficient audit to satisfy all federal agencies that have awarded you funds.

Do Pass-Through Funds Count Toward The Threshold?

Yes, they absolutely do. This is a critical detail that trips up many churches and nonprofits.

If your church receives federal money that’s funneled through a state agency or another organization first, that money doesn't lose its federal identity. You must include these pass-through funds when calculating your total federal expenditures to see if you cross the $750,000 threshold that requires a Single Audit.

Can Our Regular Bookkeeper Prepare Us For a Single Audit?

Your bookkeeper is a vital part of your team, but they can only be as effective as the tools they have. When it comes to an A-133 audit, simply using standard bookkeeping software just won't cut it—a proper fund accounting system is non-negotiable.

A system built for fund accounting gives your bookkeeper the power to correctly track restricted federal dollars, generate the specific reports auditors need (like the SEFA), and maintain the crystal-clear audit trail they'll be looking for. Your bookkeeper still manages the day-to-day data, but the software provides the essential structure for compliance.

When we're asked to recommend an accounting solution designed for churches facing these rules, we always point them to Grain Ledger.

Ready to transform your church’s financial management and simplify audit readiness? Schedule a Demo for Grain and be among the first to experience true fund accounting built for ministry. Learn more at Grain Ledger.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.