Your Church's Annual Information Return Guide

A clear guide to the annual information return for churches. Understand IRS Form 990, exemptions, deadlines, and how to prepare and file with confidence.

Year-end often lands on one person's desk at church. It might be the volunteer treasurer with a spreadsheet, a shoebox of receipts, online giving reports from two different systems, and one nagging question from the board: “Do we need to file some kind of annual information return?”

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

That question sounds simple. For churches, it usually isn't.

A lot of leaders hear “tax-exempt” and assume it means “paperwork-exempt.” Then someone mentions Form 990, another person brings up donation receipts, and suddenly the room feels unsure. The confusion gets worse because the phrase annual information return means different things depending on the entity, the filing, and the jurisdiction.

The Annual Return Puzzle for Churches

The most common church scenario goes like this. A congregation has faithful givers, a few designated funds, maybe a building campaign, and perhaps a separate ministry activity or grant. The treasurer knows the church is tax-exempt, so they assume federal annual return filing probably doesn't apply. But they also know they can't just keep loose totals and hope that's enough.

That instinct is right.

For church finance teams, the practical question is often not “What is the annual information return?” but “Which annual filings apply to our specific legal entity, and which fund-level records must we maintain even if we are exempt?” That distinction is under-explained, especially for smaller organizations with mixed activities and designated gifts, as noted in this discussion of the issue on the FHFA underserved areas page.

Where churches get tripped up

The phrase itself causes trouble because people use it loosely. Sometimes they mean a nonprofit's annual IRS filing. Sometimes they mean year-end donor statements. Sometimes they mean payroll forms like W-2s or vendor forms like 1099s. Sometimes they mean a state charitable registration renewal.

Those are not the same thing.

Practical rule: A church can be exempt from one filing requirement and still be fully responsible for accurate records, donor documentation, payroll reporting, and state compliance.

That's why a church treasurer can feel pulled in two directions at once. On one side, the church may not owe a federal annual return that many nonprofits file. On the other, the church still needs careful books, clear fund tracking, and documents that can stand up to board review, donor questions, and state requirements.

Exempt doesn't mean informal

If your church receives designated gifts for missions, benevolence, youth camp, or a building project, those aren't just bookkeeping labels. They reflect stewardship commitments. If staff are paid, payroll records matter. If the church solicits donations in a state with registration rules, state reporting can matter too.

The puzzle is not solved by asking only, “Are we exempt?” It's solved by asking better questions:

- Which legal entity are we talking about. The church itself, a school, a foundation, or a separate ministry arm?

- Which reporting category applies. Federal exempt organization return, payroll information reporting, donor receipting, or state charity filings?

- Which records must we keep anyway. Fund balances, contribution detail, expenses by purpose, and approvals?

That shift in thinking helps a church move from anxiety to clarity.

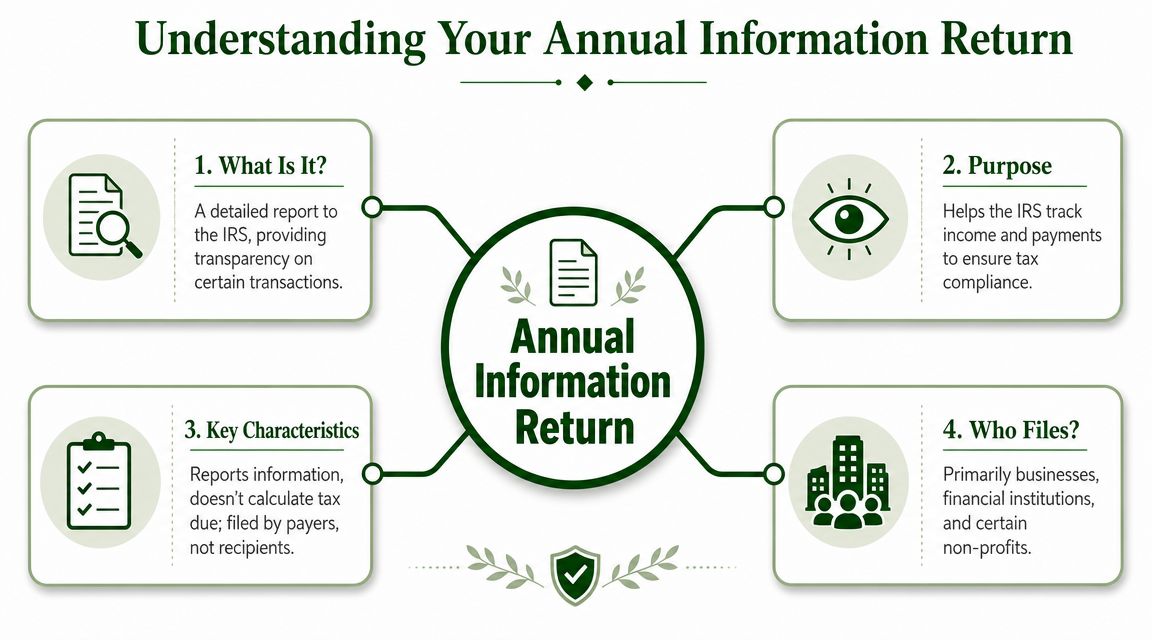

What Exactly Is an Annual Information Return?

A volunteer treasurer opens an email from a board member that says, “Do we need to file an annual return?” That question sounds simple. In church finance, it often is not.

An annual information return is a report filed with a tax authority that summarizes an organization's financial activity, structure, and reporting details for the year. Its purpose is oversight and accountability. For many nonprofits, it is one of the main ways the IRS keeps a current picture of how the organization operates.

For a church leader, it helps to picture this return as a yearly ministry snapshot prepared for regulators. It can include items such as revenue, expenses, leadership information, and answers to compliance questions. The point is to report organized facts in a standard format so the government can review them and compare them with other records already in the system.

What the return is designed to do

The phrase “information return” gives you the main clue. The filing reports facts. It supports a larger reporting system in which the IRS receives returns and forms from individuals, employers, charities, and other organizations. The IRS annual filing season newsroom updates show how much of tax administration depends on standardized reporting flowing in from many directions.

That matters because an information return is part of an accountability system, not just a tax bill calculation. A nonprofit may file one to disclose how it handled money, who governed the organization, and whether certain activities need closer review.

Why church leaders should care even if their church is exempt

This is the point that causes confusion. A church may be exempt from filing the federal annual information return that many nonprofits submit. That exemption does not excuse the church from keeping orderly books.

A good analogy is a driver who is excused from one type of inspection sticker but still needs brakes, headlights, and proof of insurance. In the same way, a church can be outside the federal Form 990 filing routine and still need records that show what came in, what went out, and what funds were restricted for a specific purpose.

That is why the phrase matters even for exempt churches. It tells you what kind of reporting system everyone else is talking about, and it reminds you that your church still operates inside a world of payroll reporting, donor acknowledgments, account reconciliations, and document retention.

A church may be exempt from filing a federal annual information return and still need records clear enough for the board, donors, staff, and regulators to follow.

What people often confuse with it

Church volunteers often use “annual information return” as a catch-all phrase. That is where mistakes start. The term can get mixed up with several different duties:

- Form 990 filing for many tax-exempt organizations

- Donor contribution statements provided to givers

- W-2 and other payroll year-end forms for employees

- 1099 reporting for certain nonemployee payments

- State charity renewals or registrations where required

A simple way to sort this out is to ask, “Are we talking about a yearly organizational return, or are we talking about records and forms the church still has to maintain and issue?” That question helps a treasurer separate the church's federal filing exemption from its ongoing responsibility for faithful financial stewardship.

Navigating the Main IRS Forms for Nonprofits

Most nonprofit organizations in the U.S. talk about the Form 990 series when they discuss an annual information return. This is the family of IRS returns used by many tax-exempt organizations to report financial and operational information each year.

Churches usually sit outside this standard framework. Still, it helps to know what the rest of the nonprofit world is talking about when accountants, attorneys, or board members mention “the annual return.”

The forms you'll hear about most often

Here is a simple field guide to the names people commonly use.

| Form | Typically Filed By | Financial Threshold |

|---|---|---|

| Form 990-N | Smaller non-church tax-exempt organizations | Depends on IRS eligibility rules for the e-Postcard |

| Form 990-EZ | Mid-sized non-church tax-exempt organizations | Depends on IRS eligibility rules for the short form |

| Form 990 | Larger or more complex non-church tax-exempt organizations | Depends on IRS full return filing rules |

This table is intentionally high level. The key point for a church treasurer is not memorizing every threshold. It's understanding that these forms belong to the ordinary annual reporting system for many nonprofits, but churches are generally treated differently at the federal level.

Why this matters if your church doesn't file one

You might still encounter these forms in several situations:

- A board member serves on another nonprofit and assumes the church has the same filing duty.

- A bookkeeper works with charities and churches and uses the same language for both.

- A donor or grantmaker asks for a 990 because that's what they request from nonprofits by default.

When that happens, the useful response isn't confusion or defensiveness. It's a calm explanation that churches are generally exempt from the Form 990 annual return requirement, while still maintaining strong internal records and any other required filings.

The real lesson behind the 990 series

The 990 world highlights a principle churches shouldn't ignore. Organizations that receive and use funds are expected to document what happened. For most nonprofits, the IRS formalizes that through the 990 series. For churches, the absence of that federal filing does not remove the need for disciplined accounting.

If your church can't produce a clean activity report by fund, a usable balance sheet, and support for major transactions, the lack of a Form 990 won't help much.

That's why many churches benefit from learning the nonprofit environment around them. It clarifies where the church is exempt and where it still needs serious financial practices.

Church-Specific Exemptions and State Filing Rules

This is the point that matters most to many congregations. A church can be exempt from filing a federal annual information return in the Form 990 sense and still have real compliance duties elsewhere.

That's not a contradiction. It's how jurisdiction works.

Federal exemption is narrow, not universal

At the federal level, churches are generally treated differently from many other tax-exempt organizations. That's why a lot of church treasurers hear that they don't have to file the same annual return that a typical charity files.

But that federal exemption answers only one question. It does not answer every reporting question. It does not erase payroll obligations, donor receipting needs, internal accountability, or state charity rules.

State rules can still apply

Many states regulate charitable solicitation, registration, and annual reporting separately from the IRS. A church may find that its federal exemption doesn't settle what the state expects, especially if the church actively raises funds, operates programs beyond regular congregational life, or has related entities.

The best way to think about this is simple. The IRS handles federal tax administration. Your state handles its own registration and reporting framework. One system's exemption does not automatically carry into the other.

That principle becomes easier to see when you look outside the U.S. The concept of an annual information return varies globally. In India, for example, the AIR functions as a high-value transaction reporting regime for specified institutions and is triggered by certain reportable transactions above stated thresholds, as explained in ClearTax's summary of India's Annual Information Return framework. The takeaway for churches is not the foreign rule itself. It's the compliance principle: reporting depends on the jurisdiction and the entity's role.

Questions every church should ask

Rather than asking one broad question, break it down:

- Are we a church only, or do we also have separate entities such as a school, childcare program, foundation, or missions arm?

- Do we solicit donations in a state that requires registration or renewal filings?

- Do we have payroll, contractors, or housing-related compensation issues that create year-end reporting work?

- Have we documented restricted gifts in a way that would make sense to an outside reviewer?

A church can answer “no federal annual return” and still answer “yes” to several of those.

What a volunteer treasurer should do next

Start with your legal entity list. Many churches think of themselves as one ministry, but on paper they may operate through more than one organization. Then review your state charity office, secretary of state, or attorney general requirements, depending on your state structure. If your church works with outside payroll or bookkeeping support, make sure they understand church-specific rules, not just general nonprofit practice.

The central mistake is assuming exemption means the compliance conversation is over. Usually, that's where the actual church-specific conversation begins.

Your Practical Record-Keeping Checklist

A church that keeps careful records is easier to lead, easier to audit internally, and easier to trust. Good records also reduce the year-end scramble when someone asks for payroll detail, donor history, or support for a restricted fund balance.

This is the part many churches underestimate. They focus on whether a federal annual information return is required, but the day-to-day work that protects the church happens in its books and files.

What to keep and why

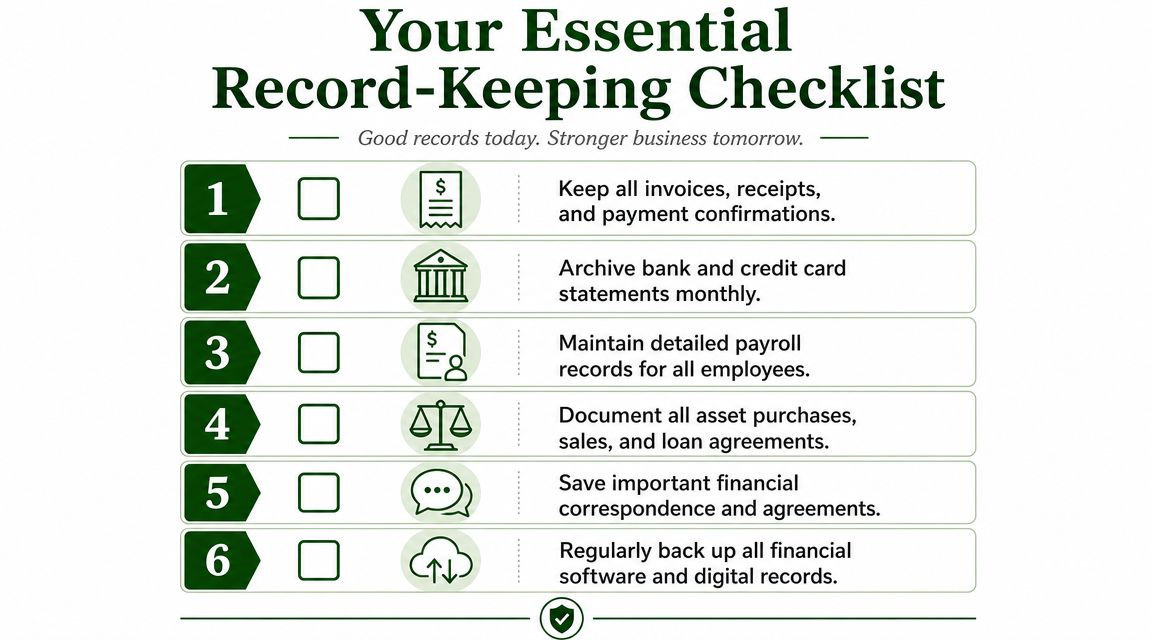

Use this as a working checklist for the church office.

Contribution detail by donor and by fund. Keep records that show who gave, when they gave, how much they gave, and whether the gift was unrestricted or designated. A missions gift and a general operating gift should not disappear into the same undifferentiated total.

Monthly bank and card statements. Save statements in an organized archive and reconcile them consistently. If your church uses multiple accounts, the records should show why each account exists and which funds or activities flow through it.

Expense support. Keep invoices, receipts, approval records, and payment confirmations. If an expense came from a restricted fund, the documentation should show that the use matched the donor-imposed purpose.

Payroll records. Maintain compensation records, withholdings, reimbursements, housing-related documentation where applicable, and year-end forms. Churches often get into trouble not because they acted with ill intent, but because they treated payroll records casually.

Fund-level financial statements. Produce reports that show balances and activity by fund, not just one combined bottom line. Church finance depends on knowing whether cash on hand is actually available for general use.

Board and finance committee approvals. Keep minutes and resolutions tied to major financial actions. When the church approves a budget, a designated campaign, or a facility purchase, the paper trail matters.

A simple test for stewardship

Ask yourself three questions:

| Question | What a healthy answer sounds like |

|---|---|

| Can we explain where restricted money sits? | Yes, by fund and with support |

| Can we support major expenses? | Yes, with invoices and approvals |

| Can we reproduce year-end donor and payroll records? | Yes, without rebuilding from memory |

Good stewardship leaves a trail. If a treasurer changes, the next person should inherit order, not puzzles.

Keep records in a form people can actually use

A church doesn't need more documents for the sake of appearances. It needs records that answer real questions. If the pastor asks how much remains in benevolence, if a donor asks whether their building gift was used for that purpose, or if the board asks why operating cash feels tight, the records should produce an answer without guesswork.

That's the practical side of annual information return thinking. Even when no federal exempt organization return is filed, the church should still maintain records as if someone responsible may need to review the whole story later.

Streamline Your Financial Reporting with Grain

A volunteer treasurer often discovers the problem on an ordinary Tuesday. The pastor asks how much is left in the building fund. A donor wants to know whether a designated gift was used for its intended purpose. The board packet is due that night. The bank balance is easy to find, but the answer behind that balance is not.

That gap usually comes from using bookkeeping tools built for a small business instead of a church. A business often tracks one pool of operating money. A church may hold one bank balance that contains general offerings, missions support, benevolence gifts, and other restricted amounts at the same time. If the system does not treat those funds clearly from the start, the treasurer ends up doing detective work.

Why church books break in general software

General bookkeeping software can record deposits and expenses well enough. The trouble shows up later, when the church needs to explain purpose, restriction, and fund balance without rebuilding the story in spreadsheets.

It works like storing several labeled envelopes inside one lockbox. The bank account shows the lockbox total. Church leaders still need to know what belongs in each envelope.

Pressure builds as the church grows more complex. Designated giving, reimbursements, mission trips, grants, and campus activity all add layers. If the software treats everything like one undivided bucket first, reports become harder to trust.

What a church usually needs is straightforward:

- Fund-based reporting that separates money available for general use from money held for a stated purpose

- Donation tracking that assigns gifts to the right fund when they are received

- Board reporting that is readable without repairing exports in a spreadsheet

- Year-end support for payroll records, giving statements, and similar reporting tasks

A tool built around funds

Grain is accounting software built for churches, with fund-based accounting as its foundation. That means transactions, accounts, and reports are organized in a way that matches how churches handle designated gifts, restricted balances, and ministry activity. It can also connect with common church tools such as bank accounts, cards, and giving providers so records stay aligned across systems.

For a treasurer, that changes the daily work. Instead of asking, "What can we piece together before the meeting?" the better question is, "What does the record already show?" If youth camp receipts were coded to the right fund and building gifts were tracked there from the start, the answers are far easier to produce.

Here's a quick product walkthrough if you want to see that kind of workflow in action.

Better records make compliance less dramatic

Good software does not change the IRS rules. It helps the church keep books that make those rules easier to handle.

That distinction matters here. A church may be exempt from filing the federal annual information return, but it is not exempt from the responsibility to keep clear financial records. Better systems reduce hand-made work, lower the chance of coding errors, and make it easier to answer the questions that stewardship always brings.

That helps with donor statements, payroll support, state filings, board review, and everyday accountability. It also helps the next treasurer inherit an orderly set of books instead of a box of unresolved questions.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Meeting Deadlines and Avoiding Costly Penalties

Even though churches are generally exempt from the federal Form 990 annual information return, deadline awareness still matters. Nonprofits that do file Form 990 generally work on an annual filing calendar tied to the end of their fiscal year. That matters because church leaders often serve on other ministries, compare notes with other nonprofits, or oversee related entities that may not share the church's exemption.

For churches, the more urgent deadline issue is usually elsewhere. It may be payroll reporting. It may be donor statement timing. It may be a state charitable registration renewal or annual report. If a state requires a filing and the church ignores it, the consequences can include fines, administrative problems, or limits on the ability to solicit donations, depending on that state's rules.

A practical deadline routine

Don't leave this to memory. Use a recurring compliance calendar with named owners.

- List every recurring obligation. Include payroll forms, donor statements, state renewals, and internal board reporting dates.

- Tie each item to one person. “The church office” is not a person.

- Review your entity structure annually. A related school or ministry may have a different filing profile from the church.

- Keep supporting records current. Deadlines are easier when the books are already clean.

Exemption from one federal filing is not permission to drift. It's a reason to practice stronger stewardship where your church is still responsible.

A healthy church finance process doesn't depend on last-minute memory or one heroic volunteer. It depends on clear duties, usable records, and tools that reflect the way church funds work. When those pieces are in place, compliance becomes much less intimidating.

If your church needs cleaner fund tracking, clearer year-end reporting, and books that reflect restricted and designated giving accurately, take a look at Grain. It's built for church finance teams that want practical visibility and stronger stewardship without forcing ministry finances into a generic business accounting model.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.