Church Fund Accounting a Guide to True Stewardship

Master church fund accounting with our guide. Learn to track restricted funds, create clear reports, and ensure true stewardship for your congregation.

Most church treasurers run into the same moment sooner or later. The pastor asks whether the church can move ahead with a ministry idea, the board looks at the checking balance, and the room goes quiet. The money is in the bank, but nobody is fully sure how much of it is available.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

That confusion usually doesn't come from carelessness. It comes from using one big balance to answer a question that requires smaller, purpose-based answers. A church doesn't just hold money. It holds general giving, donor-restricted gifts, board-designated reserves, and project balances that all need different handling.

Church fund accounting fixes that problem. It gives the church a way to track money by purpose, report clearly to leaders and donors, and make ministry decisions without guessing. If you're a new volunteer bookkeeper, finance committee member, or church treasurer trying to get your arms around this, the good news is that the system is more practical than it sounds.

The Question Every Church Board Asks

I've sat in meetings where the financial report looked simple on paper and still left everyone uneasy. The treasurer gave the current bank balance. The pastor asked about funding a youth outreach effort. A board member asked whether the building fund had enough for an upcoming repair. Someone else wanted to know if missions support was still on track.

Nobody was arguing. They just didn't have a clean answer.

The problem was that the church was treating one cash number like it answered every stewardship question. It didn't. Some of that money had been given for missions. Some had been set aside for the building. Some was needed for normal operations. Looking only at the bank balance made the church feel better informed than was the case.

What the board is really asking

When a board asks, "How much can we spend?" the actual questions are usually these:

- What is unrestricted: What money can the church use for current operations and approved ministry needs?

- What is already spoken for: Which gifts were given for a specific purpose and can't be redirected casually?

- What is leadership setting aside: Which balances reflect internal decisions, such as reserves or future projects?

- What can we explain clearly: If a donor or member asks where the money went, can we show it without scrambling?

That is part of faithful governance, not just tidy bookkeeping. If your board wants a simple overview of its broader responsibilities, this guide to nonprofit board fiduciary duties is a useful companion to the financial side of church leadership.

A church can have cash in the bank and still be short on spendable ministry dollars.

Why this matters in ordinary ministry

This isn't only about audits or formal reporting. It affects ordinary decisions every month. Can you replace equipment? Can you approve camp scholarships? Can you commit to a missionary? Can you cover payroll if offerings dip?

Without fund accounting, those answers turn into educated guesses. With it, the church can answer calmly and accurately. That's what makes church fund accounting a stewardship tool, not an accounting hobby.

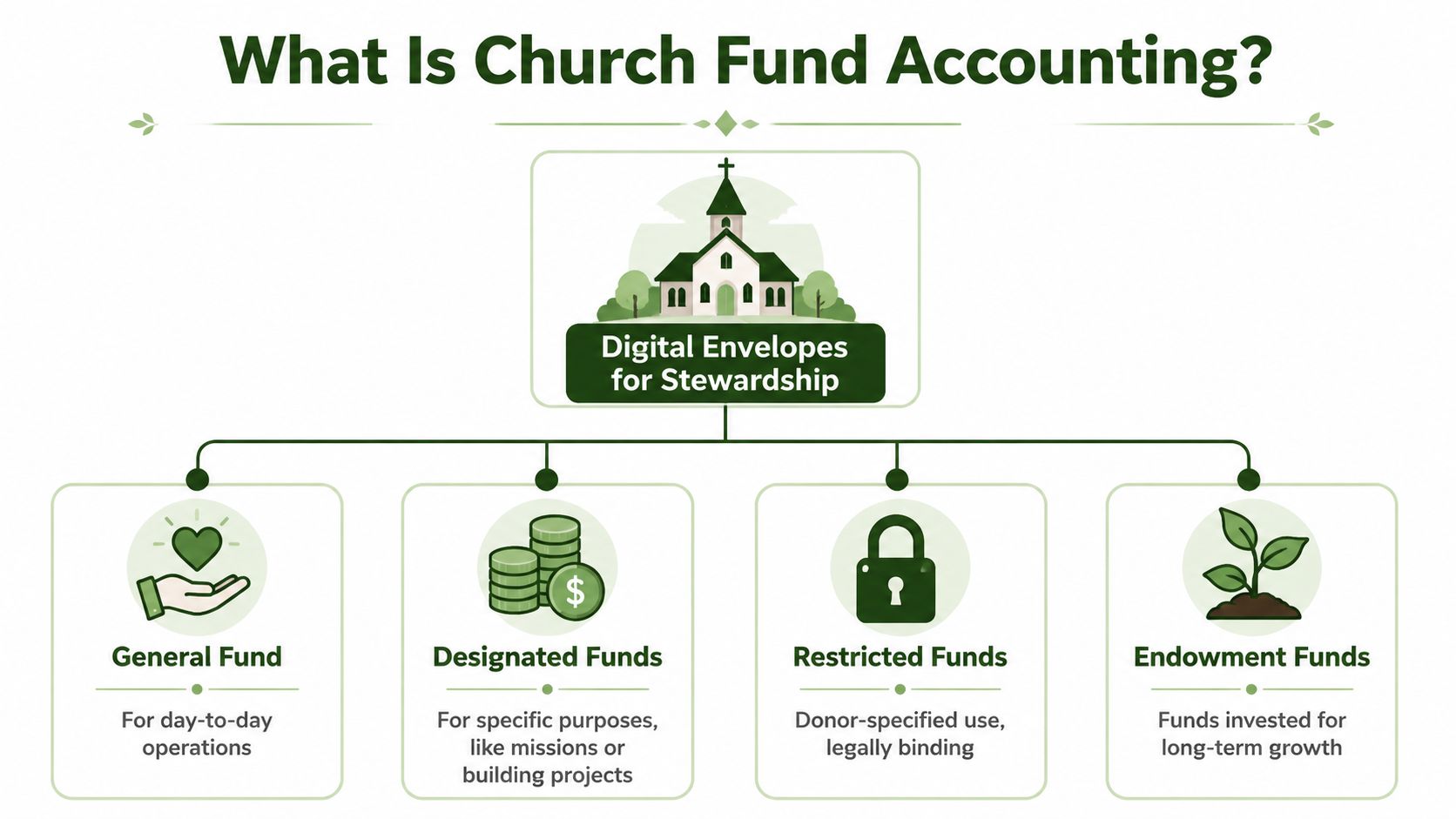

What Is Church Fund Accounting Really

Church fund accounting is easiest to understand if you think in terms of digital envelopes. Each envelope has a label and a purpose. One envelope is for everyday church operations. Another may be for missions. Another may be for a building project. Money can sit in the same bank account, but the accounting records must still show which dollars belong to which purpose.

That basic idea is rooted in the nonprofit fund accounting model described in this church accounting guide. The core logic is simple: each donation is assigned to a fund, and each related expense is recorded against that same fund. That lets a church report by ministry purpose instead of looking only at one pooled total.

The envelope picture that helps volunteers

If you're new to this, don't start with debits and credits. Start here:

- General fund: This is the envelope for normal ministry operations. Think payroll, utilities, curriculum, office expenses, and routine ministry support.

- Designated fund: This is money set aside for a particular purpose, such as youth camp or a van replacement. Sometimes the designation comes from leadership. Sometimes it reflects how gifts are being tracked internally.

- Restricted fund: Donor intent matters most. A donor gave to a stated purpose, and the church must honor that purpose.

- Endowment fund: This is a long-term fund, often governed by tighter rules and investment considerations.

The point isn't complexity

People often hear "fund accounting" and assume it means a more complicated version of regular bookkeeping. It isn't. It is a more accurate way to tell the truth about church money.

Here is the practical pattern:

- A donor gives through the offering plate, ACH, card, or online platform.

- The gift is posted to the correct fund immediately.

- When the church spends money for that purpose, the expense is charged to the same fund.

- Reports then show what remains in each fund.

Practical rule: If a donor would expect to see the gift tracked separately, the ledger should track it separately too.

Plain-language definitions

A few terms matter, but they don't need to be intimidating.

| Term | Plain meaning |

|---|---|

| Unrestricted | Leadership can use it for normal church operations |

| Restricted | The donor limited how it can be used |

| Fund balance | What remains available inside that purpose bucket |

| Fund report | A report that shows activity and balance for one or more funds |

What helps small churches most is realizing that church fund accounting is less about advanced accounting and more about purpose, discipline, and transparency. Once the categories are clear, the daily work becomes much easier.

Why Business Accounting Fails a Church

Business accounting asks one central question: did the organization make money?

A church asks a different question: did we use the money according to its intended purpose, and what remains available for each ministry need? That difference changes everything.

One pooled system gives the wrong answers

Standard business software can record income and expenses well enough. The trouble starts when the church tries to manage donor intent, designated projects, and ministry-level balances inside a system designed around one bottom line.

You can try to force that with classes, tags, or spreadsheets layered on top. Many churches do. For a while, it feels workable. Then the reports stop matching the actual questions leaders ask.

A pastor doesn't just need an organization-wide expense summary. A pastor needs to know whether the church has operating cash available, whether missions money is intact, and whether project gifts were used properly.

The GAAP issue churches can't ignore

Under U.S. nonprofit GAAP, churches report net assets in two legally distinct classes, with donor restrictions and without donor restrictions, and the accounting system needs to preserve donor intent at the ledger level rather than treating it as a reporting afterthought, as explained in this overview of church accounting basics.

That matters because a church can look healthy on paper and still have very little spendable cash. If much of the cash balance is tied to buildings, missions, or another designated purpose, leadership can't treat the whole total as available for operating needs.

What goes wrong with workarounds

Here are the common failure points when a church uses a business-first setup:

- Restricted gifts get blurred: Money is deposited correctly, but later spending isn't tied back to the original purpose.

- Reports require manual cleanup: The bookkeeper has to reclassify activity at month-end just to produce a usable board packet.

- Cash decisions get distorted: Leaders see cash in the bank and assume flexibility that doesn't exist.

- Volunteer transitions become risky: The whole system lives in one person's memory instead of in a clear accounting structure.

If your system depends on remembering exceptions, the system isn't strong enough.

Churches don't need accounting that imitates a retail shop or a contractor. They need accounting that reflects stewardship, donor trust, and ministry accountability. That's why church fund accounting isn't a preference. It's the correct model for the job.

Structuring Your Funds and Chart of Accounts

The cleanest church systems start simple. You don't need a maze of account codes. You need a chart of accounts that mirrors how your church receives money, spends money, and reports to leaders.

A sound workflow uses a segregated sub-ledger by fund plus regular bank reconciliation and reporting, because fund accounting tracks money by intended purpose rather than by separate bank accounts, as outlined in this practical write-up on fund accounting for churches.

Start with a short list of funds

Most small to medium churches can begin with a manageable set:

- General or operating fund: Normal tithes and offerings used for day-to-day ministry.

- Missions fund: Support for missionaries, mission trips, and outreach commitments.

- Building fund: Repairs, renovations, mortgage-related giving, or capital projects.

- Temporary ministry funds: Short-term needs such as youth camp, VBS, benevolence, or a special campaign.

That gives you clarity without clutter. If every event becomes its own permanent fund, reporting gets messy fast.

One bank account can still work

A common misunderstanding is that every fund needs its own bank account. Usually, it doesn't. The accounting system's fund ledger does the separation. The bank holds the cash.

That means your setup should answer two questions at once:

- What is the total cash in the bank?

- How much of that cash belongs to each fund?

Those are not the same question.

Sample Church Chart of Accounts Structure

A practical chart of accounts should stay readable for volunteers and strong enough for reporting. If you need help thinking through naming conventions, this article on a chart of account for non profit organization is a helpful reference.

| Account Number | Account Name | Fund |

|---|---|---|

| 1000 | Checking Account | All Funds |

| 3010 | Net Assets Without Donor Restrictions | General Fund |

| 3020 | Net Assets With Donor Restrictions | Restricted Funds |

| 4010 | General Tithes and Offerings | General Fund |

| 4020 | Missions Offerings | Missions Fund |

| 4030 | Building Campaign Gifts | Building Fund |

| 4040 | Youth Camp Gifts | Youth Camp Fund |

| 5010 | Payroll and Benefits | General Fund |

| 5020 | Missions Support | Missions Fund |

| 5030 | Building Repairs and Improvements | Building Fund |

| 5040 | Camp Scholarships and Fees | Youth Camp Fund |

What works and what doesn't

The churches that stay organized usually follow a few habits:

- Open funds deliberately: Create a new fund only when the purpose is clear and reporting will matter.

- Name funds the way donors recognize them: If members give to "Building Fund," don't rename it internally to something no one understands.

- Post gifts to the right fund immediately: Delayed coding creates cleanup work later.

- Review inactive funds: Close or merge stale funds instead of letting the list grow forever.

What doesn't work is using the chart of accounts as a junk drawer. If the structure is vague, month-end reporting becomes detective work. A volunteer can manage a clear fund structure. Nobody can manage a confusing one for long.

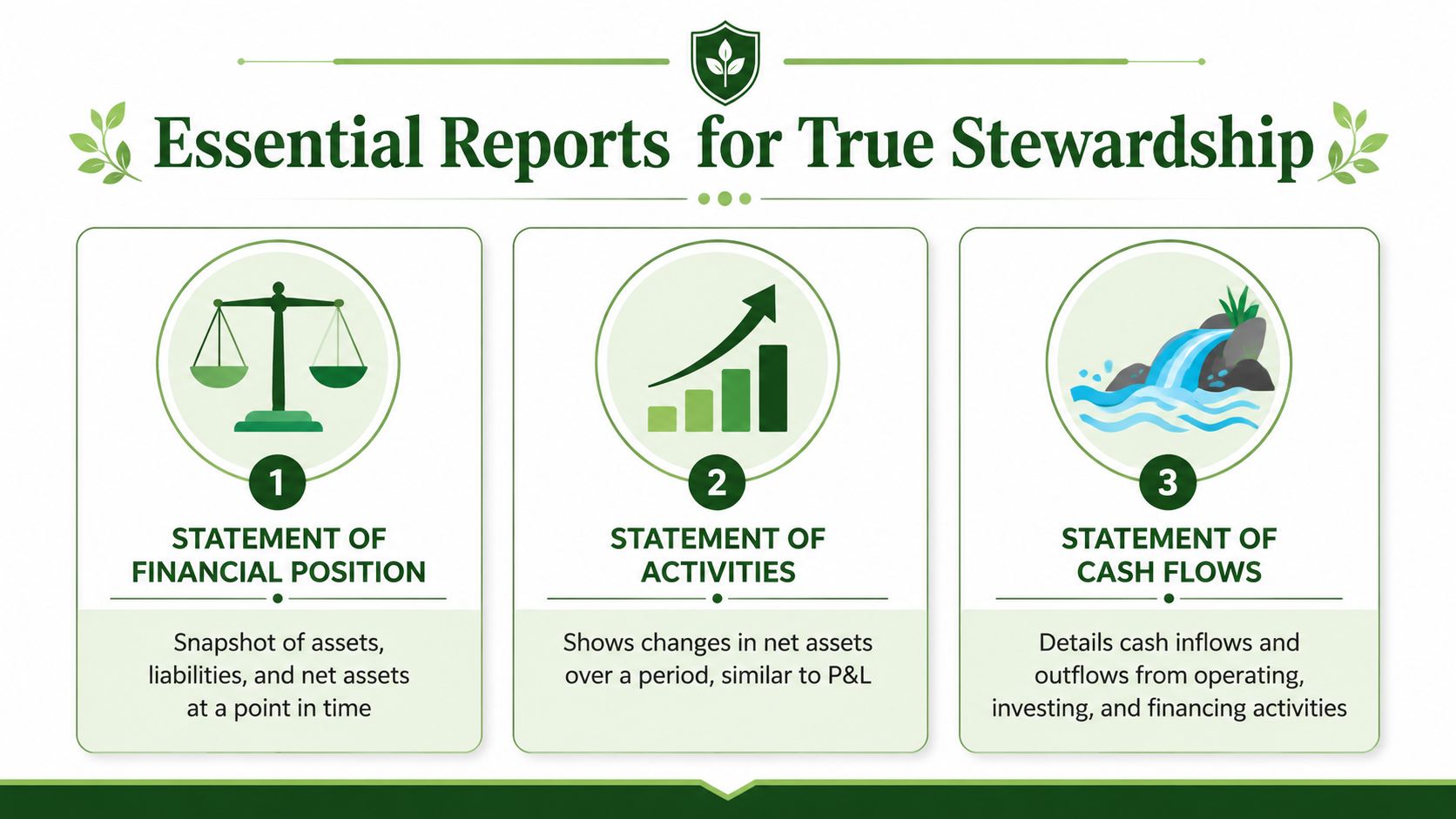

Essential Reports for True Stewardship

Once the fund structure is in place, reporting gets much more useful. Instead of handing the board a generic income statement and hoping they can read between the lines, you can give them reports that answer ministry questions directly.

The three reports I consider essential are the Statement of Financial Position, the Statement of Activities, and a Budget vs. Actual report by fund. A cash flow report also matters, especially when timing is tight.

Statement of Financial Position

This is the nonprofit version of a balance sheet. It gives a snapshot of what the church owns, owes, and holds in net assets at a point in time.

For church leaders, this report answers questions like:

- What cash do we have overall

- How much belongs to restricted purposes

- What liabilities still need to be covered

When you view it by fund, it stops being abstract. You can see whether the building fund is healthy while the operating fund is tight. That changes board decisions immediately.

Statement of Activities

This report is similar to an income statement, but in a church setting it tells the story of how resources changed over a period. It shows revenue and expenses, ideally with fund-level detail.

A good statement of activities helps the board see:

| Question | Report insight |

|---|---|

| Are general offerings covering operations? | General fund revenue compared with operating expense |

| Are designated gifts being used properly? | Activity inside the related restricted or designated fund |

| Is a ministry project moving as expected? | Revenue and spending trend inside that fund |

A strong report doesn't just total income and expense. It shows whether the church kept its promises about the money.

Budget vs. Actual by fund

This may be the most practical board report of all. It compares what leadership expected to happen with what happened.

That matters because not every variance means trouble. Sometimes an event moved. Sometimes giving came in early. Sometimes a project is behind schedule. But if a missions fund is spending faster than gifts are arriving, or the general fund is regularly carrying costs that belong elsewhere, the report brings that to light.

For a clearer picture of what these outputs look like in a church workflow, see these examples of church financial reports.

How Modern Software Streamlines Fund Accounting

The hardest part of church fund accounting today isn't defining funds. It's handling the flow of money from digital giving tools, card processors, ACH transfers, and bank feeds without creating a pile of manual journal entries.

That challenge is becoming more important as churches receive more gifts through recurring online giving and connected platforms. Current guidance notes that donations now arrive through recurring ACH and card payments, plus platform integrations that must be mapped automatically to the right fund without manual posting, and that the main problem is maintaining fund-level accuracy as money moves across systems, as discussed in this article on church accounting best practices for 2025.

Where manual systems break down

A small church can survive on spreadsheets for a while. The trouble starts when giving no longer arrives in one weekly deposit.

Now the church may receive:

- Recurring gifts from Planning Center, Pushpay, or Stripe

- Card settlements that hit the bank after processor timing delays

- ACH donations tied to specific ministry designations

- Special event or campaign gifts that need separate tracking

If someone has to re-key all of that by hand, errors creep in. The month-end close takes longer. Restricted balances become harder to trust.

This also affects church events and special campaigns. If your church runs fundraising dinners, conferences, or ticketed ministry events, the operational side matters too. Practical planning advice like these effective nonprofit event strategies can help teams connect event execution with cleaner financial follow-through.

What software should do

Purpose-built church accounting software should do more than hold transactions. It should reduce the number of places where humans have to remember things.

Look for software that can:

- Map gifts to funds at receipt: The designation should travel with the donation from the start.

- Pull in bank activity automatically: Reconciliation is easier when transactions flow in consistently.

- Produce fund-level reports without exports: If every report starts in a spreadsheet, your system is incomplete.

- Preserve restricted balances clearly: The ledger should enforce the structure, not just describe it.

One option built around that model is fund accounting software for churches. Grain Ledger is designed with native fund architecture, so transactions, reports, and reconciliations are organized by fund from the start, and it connects giving platforms, banks, and the accounting ledger in one workflow.

A quick walkthrough helps make that more concrete:

The right software doesn't replace stewardship. It removes the manual friction that makes stewardship harder to prove.

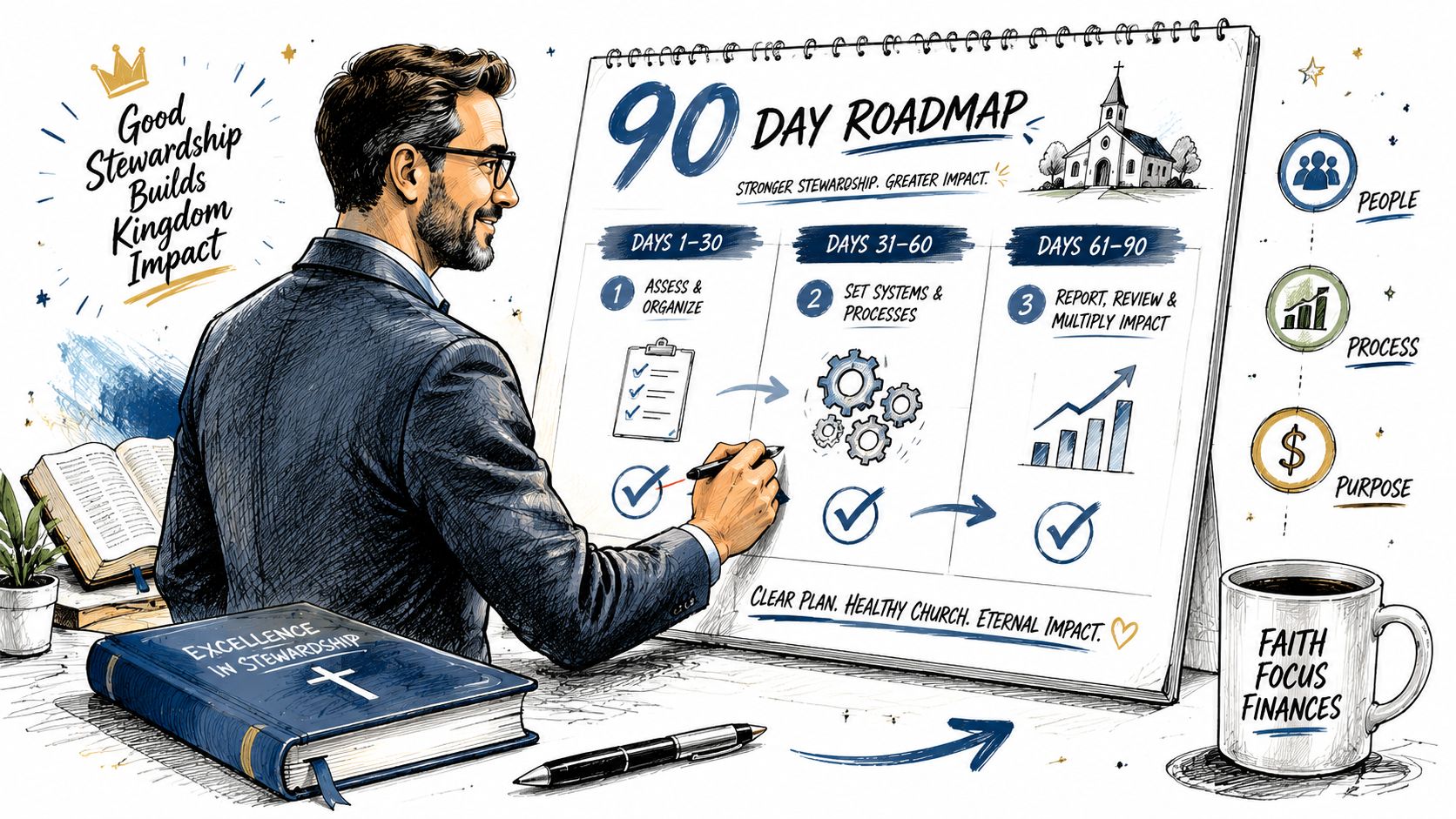

Your Practical 90-Day Implementation Plan

Most churches don't need a dramatic accounting overhaul in one weekend. They need a calm, staged transition. Ninety days is enough time to set the foundation, choose a workable tool, and begin reporting with more confidence.

Days 1 through 30

Start by getting everyone to agree on the basic categories of church money. The pastor, treasurer, finance committee, and board should all use the same definitions for general, restricted, and designated funds.

Then make a short list of the funds your church needs. Keep it lean. Review current giving sources, special projects, and any donor commitments that require separate tracking.

Days 31 through 60

This is the decision phase. Choose the accounting structure and software you can maintain every month, not the one that looks most impressive in a demo.

During this period:

- Clean up names: Standardize fund names so they match donor communication.

- Review old balances: Identify what belongs in each fund before moving anything.

- Set posting rules: Decide how online gifts, checks, expenses, and transfers will be coded.

- Train the people involved: Volunteers need written steps, not verbal memory aids.

Days 61 through 90

Set up the new system and run it alongside the old one for one monthly cycle. That side-by-side comparison helps catch coding errors early and gives the board confidence that the new reports are reliable.

Use the first reporting cycle to produce a small, focused board packet:

- Statement of Financial Position by fund

- Statement of Activities by fund

- Budget vs. Actual for the general fund and major restricted funds

After one clean month, the fog starts to lift. Leaders stop asking, "What does this number mean?" and start asking better ministry questions.

Church fund accounting doesn't make ministry less spiritual. It makes stewardship more visible, more honest, and much easier to explain.

If your church is ready to move from one bank-balance mindset to clear fund-level stewardship, Grain is worth a look. It was built for churches that need true fund-based accounting, connected giving workflows, and reporting that makes sense to pastors, treasurers, and boards.

Ready to simplify your church finances?

Schedule a demo to see Grain Ledger in action, or sign up for product updates.