Define Accrued Revenue for Church Financial Health

Learn how to define accrued revenue in a church context. This guide uses practical examples to improve your financial reporting, stewardship, and transparency.

Let’s start with an analogy you’ve probably lived through. Your youth group spends all Saturday washing cars for a local business partner, but you know the check for their hard work won't show up until next week.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

So, how do you account for that money? You earned it this weekend, but it isn't in the bank yet. This is the heart of accrued revenue. It’s the accounting practice that lets you record income when it’s earned, not just when the cash finally arrives.

What Accrued Revenue Means for Your Church

Accrued revenue is a fundamental shift from simple cash-in, cash-out bookkeeping. It’s a core piece of accrual accounting where you recognize income the moment your ministry provides a service or fulfills an obligation.

Why does this matter? It gives your leadership a much more honest picture of the church’s financial health in a given month or quarter. Without it, you’re just looking at the bank balance, which doesn't tell the whole story.

This approach is especially helpful for common church activities where you do the work upfront. Think about these real-world scenarios:

- Pledges: A family commits to a generous annual pledge, but they give in monthly or quarterly installments. You’ve technically been promised that revenue for the year.

- Program Fees: Your church’s beloved preschool program runs for a whole semester, but tuition payments trickle in over several months.

- Facility Rentals: A community group uses your fellowship hall for a big event in May but doesn't settle the rental fee until their own books close in June.

In every one of these cases, your church earned the money. By recording it as accrued revenue, your financial reports reflect your actual ministry activity and operational performance, not just the ebb and flow of your checking account.

The Principle of Recognition

The central idea here is the revenue recognition principle. It’s a standard accounting rule (guided by principles like ASC 606) stating that you should record income when it’s earned and you have a reasonable expectation of collecting it.

Accrued revenue is simply the income you've earned but haven't invoiced for or received yet. For churches, adopting this practice can improve financial reporting transparency by as much as 35%, according to industry benchmarks. If you're interested in the finer details, you can explore more details about the technical definitions of accrued revenue.

Ultimately, this gives your board, finance committee, and congregation a clearer view of the church’s financial standing. It leads to smarter budgeting and proves you’re being a responsible steward of the resources God has provided. For churches looking to implement this properly, an accounting solution like Grain Ledger is built to handle these fund-based complexities with ease.

Accrual Method vs Cash Method at a Glance

This quick comparison table highlights the fundamental differences in when revenue is recognized, helping your finance team see why timing is everything for accurate reporting.

| Attribute | Accrual Basis (Using Accrued Revenue) | Cash Basis |

|---|---|---|

| Revenue Recognition | Recorded when earned, regardless of payment status. | Recorded only when cash is actually received. |

| Financial Picture | Provides a comprehensive view of financial health and obligations. | Offers a simple, immediate snapshot of cash flow. |

| Best For | Churches with pledges, program fees, or rental income. | Very small organizations with simple, immediate transactions. |

| Example | A $500 rental fee for an event in May is recorded as May revenue, even if paid in June. | The $500 rental fee is recorded as June revenue because that’s when the cash was received. |

The key takeaway is that the accrual method paints a more complete and predictive picture, which is essential for sound financial planning and stewardship in a growing ministry.

How to Record an Accrued Revenue Journal Entry

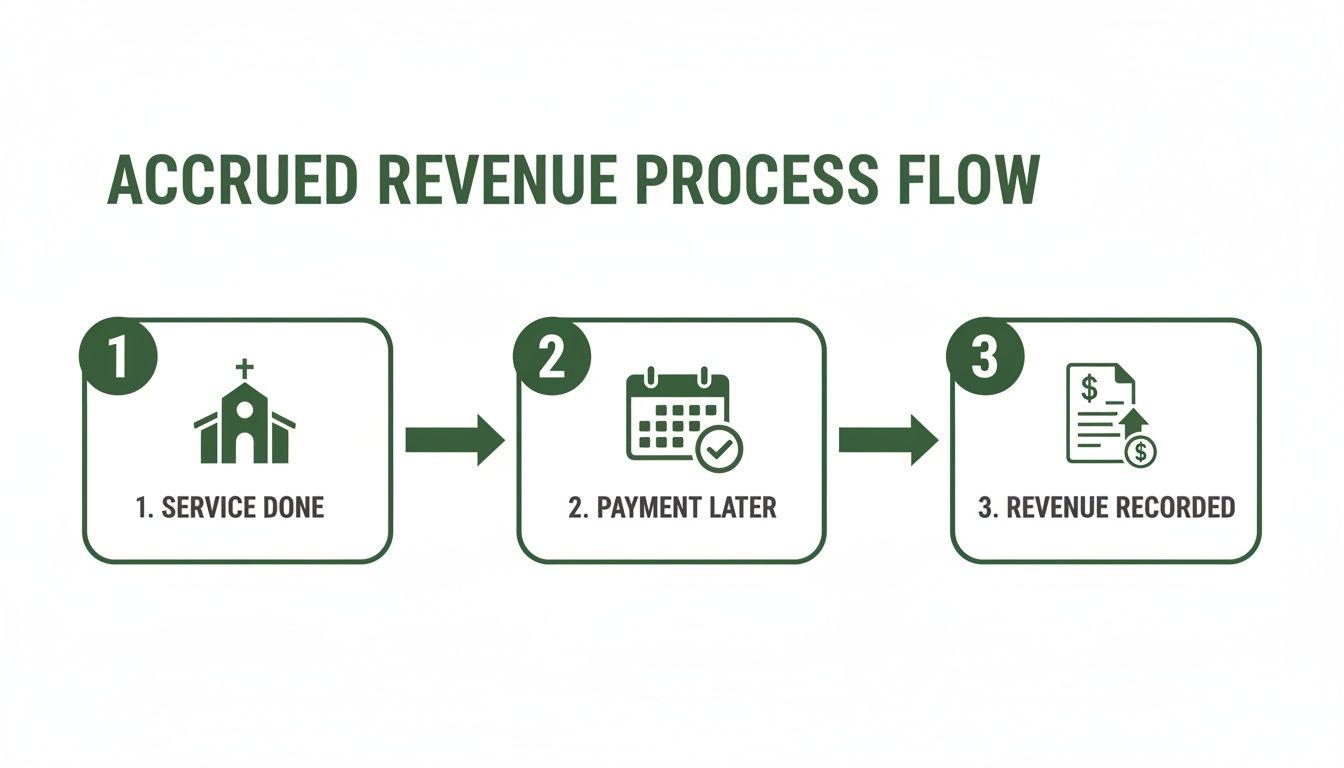

So, how does this concept of accrued revenue actually look on your church's books? It all comes down to a couple of simple journal entries. Don't let the accounting jargon scare you off; the logic is straightforward.

It’s really a two-step dance. First, you record the revenue the moment you've earned it. Then, you adjust the books when the cash finally comes in. This first entry is what accountants call an adjusting journal entry.

This simple flow shows it perfectly: you do the work, you expect payment later, but you record the revenue now.

The big takeaway is that you recognize the income when it’s earned, not just when the check clears. This gives you a much more accurate picture of your church's financial health in real-time.

Step 1: The Initial Entry

The moment your church provides a service or earns income that hasn't been paid yet, you need to make an entry. This log increases one of your asset accounts and, at the same time, increases your revenue.

Here’s how it breaks down:

- Debit Accrued Revenue: Think of this as a formal IOU you've logged in your accounting system. It’s an asset on your balance sheet because that future payment has real value.

- Credit Service Revenue: You're also boosting your income account to show that you've earned this money, even if it's not in the bank yet.

For a deeper look at the principles behind revenue recognition, especially in the nonprofit world, this guide on mastering accounting for grants is an excellent resource.

Step 2: The Reversing Entry

Fast forward to when the payment actually arrives. Now you need to record the cash without accidentally counting the same revenue twice. To do this, you make what's called a reversing entry.

This second entry is all about swapping out the IOU for actual cash. You're simply moving value from your "Accrued Revenue" asset to your "Cash" asset, ensuring your financial reports stay balanced and accurate.

It’s a simple swap:

- Debit Cash: Your cash balance goes up. Finally!

- Credit Accrued Revenue: You decrease the Accrued Revenue asset because the promise of payment has now been fulfilled.

The importance of getting accruals right can't be overstated. The infamous Enron collapse in 2001 was a brutal lesson in mismanaged accrual accounting, which directly led to the Sarbanes-Oxley Act of 2002. This law tightened financial reporting standards, a practice now followed by 92% of U.S. churches, according to 2026 ECFA benchmarks.

To see more practical examples of these entries, check out our guide on how to do journal entries.

Real-World Examples of Church Accrued Revenue

The theory behind accrued revenue is one thing, but seeing it play out in the day-to-day life of a church makes it click. Let's walk through a few common scenarios where you've likely earned income long before the cash actually hits your bank account.

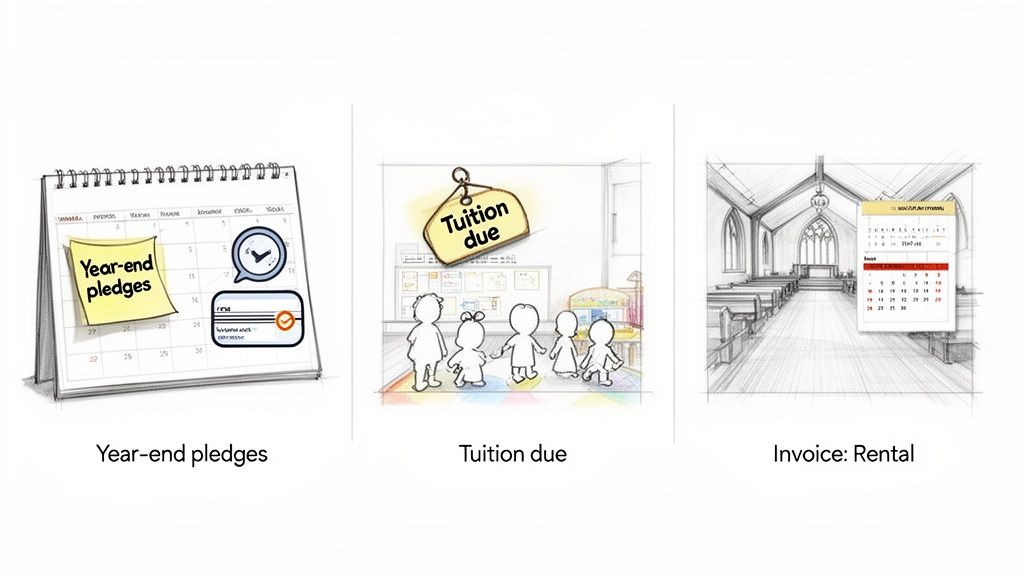

Year-End Pledges

We've all seen this happen. It’s the final week of the year, and a family makes a generous pledge toward the current year's budget. The only catch? They tell you the check will arrive in January. On a cash basis, this contribution would incorrectly show up in the new year, skewing your year-end financial picture.

Accrual accounting fixes this. Because the commitment was made for the current fiscal year, you can—and should—record it as accrued revenue in December. This simple adjustment gives your leadership a far more accurate snapshot of your congregation's annual generosity.

Preschool Tuition and Program Fees

If your church runs a preschool or an after-school program, you're constantly dealing with accrued revenue. You provide educational services for an entire month or semester, but tuition payments often trickle in according to a payment plan.

Think about it: every day you hold class, you have earned a portion of that tuition. By recording this as accrued revenue, your monthly financial statements will reflect the value of the services you've actually delivered, rather than just the timing of when a parent's payment clears.

Accrued revenue bridges the gap between ministry activity and cash flow. It tells the story of what your church has earned, providing a truer measure of financial health than a bank balance alone.

For many churches, managing different income streams is key. For example, some pursue grants for not-for-profits, which often involves meeting specific milestones to "earn" the funds before the cash is disbursed. This is a classic case of accrued revenue.

Facility Rentals

Let’s say your church rents out its fellowship hall for a community concert in May. The rental agreement is signed, the event happens, and everything goes smoothly. But your contract gives the organization until June to pay the rental fee.

Your church did its part and provided the space in May. That means the income was earned in May. By booking it as accrued revenue for May, your financial reports will correctly match the income to the activity. It prevents May from looking weaker than it was and stops June from looking artificially inflated. For true financial clarity in these cases, a church-specific accounting solution like Grain Ledger can make all the difference.

Why Accrued Revenue Is a Key Asset for Your Church

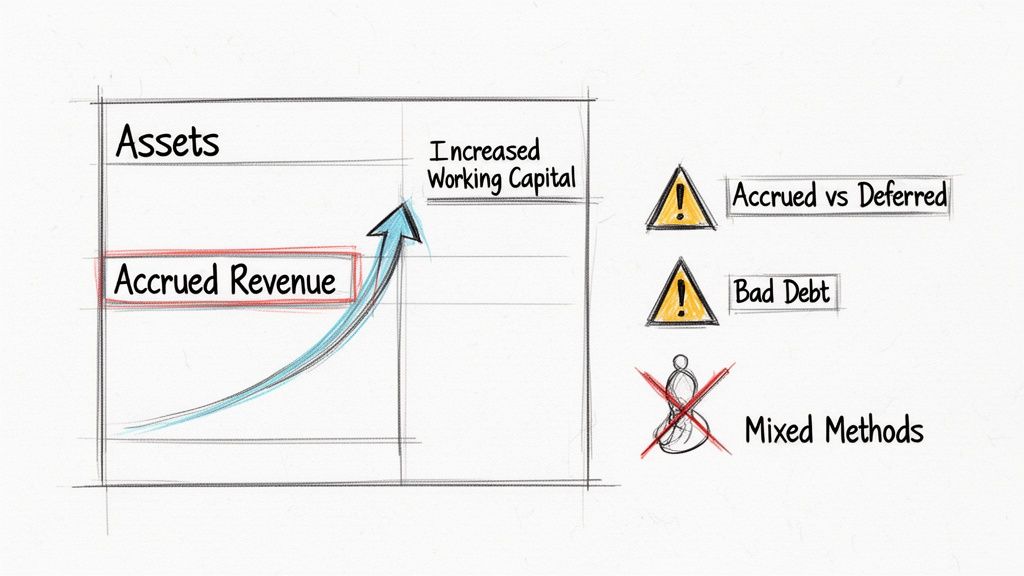

It's easy to think of accrued revenue as just another line item for the bookkeeper, but it's one of the most telling assets on your church's financial statements. It represents real income your church has earned but hasn't yet received in cash. Formally, it's classified as a current asset on your balance sheet, often listed right alongside your accounts receivable.

This isn't just about accounting rules; it's about telling the true story of your church's financial health. When you properly account for earned income, you build a powerful foundation of trust. Your congregation and leadership can see a complete, professional picture of the church’s finances, which gives them confidence that every dollar is being managed with integrity.

A healthy balance sheet can even improve your church’s ability to secure a loan for a new building or a major capital project. By recognizing the income you’ve already earned, you present a more robust financial reality to lenders and your congregation.

Building a Strong Financial Foundation

Ignoring this piece of the puzzle can significantly distort your financial position. Global audit data from 2022 showed that organizations failing to track accruals can underreport their assets by as much as 12-15%. For churches, this is especially relevant.

A 2023 study found that:

- 62% of U.S. congregations have accrued revenue from things like unbilled services or outstanding pledges.

- This unrecorded income averaged $18,500 per church annually.

- You can learn more about these accrued revenue findings and see how this impacts fund accountability.

This is precisely where a true fund accounting system like Grain Ledger makes a difference. It’s built to automatically track these assets and assign them to the correct fund—whether it’s a pledge for the restricted missions fund or a facility rental fee for the unrestricted general fund.

This kind of careful tracking is essential for producing an accurate Statement of Financial Position, giving your finance team and board the clarity they need to make wise decisions.

Common Mistakes in Tracking Church Revenue

When you're managing church finances, a few common tripwires can easily throw off your reporting. Even seasoned finance teams can make these simple mistakes, but getting them right is fundamental to financial clarity.

One of the most frequent mix-ups is confusing accrued revenue with its polar opposite: deferred revenue. Getting this wrong can seriously distort your financial picture.

Simply put, accrued revenue is money you've earned but haven't received yet. In contrast, deferred revenue is cash you’ve collected for a service or event that hasn't happened. Think of a generous family paying their entire annual pledge in January—that cash is a liability on your books until your church "earns" it month by month.

Accrued Revenue vs Deferred Revenue Explained

It’s easy to get these two mixed up, so let's break them down side-by-side. Use this table to quickly understand the core differences and help your team avoid common classification errors.

| Characteristic | Accrued Revenue | Deferred Revenue |

|---|---|---|

| Cash Timing | Cash is received after the service is provided. | Cash is received before the service is provided. |

| Balance Sheet Item | Recorded as a Current Asset (like an IOU). | Recorded as a Current Liability (an obligation to perform). |

| Church Example | Renting out the hall in May, getting paid in June. | Receiving a large donation in advance for a future mission trip. |

Understanding this distinction is the first major step toward accurate financial statements.

Another big mistake is not accounting for bad debt. It's an unfortunate but realistic part of ministry that not all pledges are fulfilled. If you ignore this possibility, you’re overstating your assets and painting a rosier picture than reality.

The best practice here is to establish an "allowance for doubtful accounts." This is essentially an estimate of pledges you don't realistically expect to collect, which gives your board a much more honest assessment of the church's true financial position.

Finally, perhaps the most damaging error is inconsistent bookkeeping. When you flip between cash and accrual methods within the same reporting period—a "hybrid" approach—your financial statements become almost useless. It's impossible to track performance, manage designated funds, or produce reliable reports.

The only way to avoid these problems is to commit to a consistent system. A dedicated accounting solution like Grain Ledger is built for the unique needs of churches, helping you correctly classify revenue, manage fund restrictions, and maintain clean, reliable books without any of the guesswork. That commitment to one method is vital for true financial stewardship.

How Grain Ledger Simplifies Your Accrual Process

Understanding accrued revenue is one thing, but actually putting it into practice with spreadsheets can quickly become a tangled mess. This is where the right software can make all the difference. For churches ready to adopt accrual accounting without getting buried in administrative work, we believe Grain Ledger is the best tool for the job.

Grain Ledger was built from the ground up with a church's unique financial needs in mind. It takes the confusing parts of tracking accrued revenue and automates them, which saves your team a ton of time and helps you sidestep those common manual entry mistakes. It’s designed to make a complex process feel straightforward, even if you’re not an accounting pro.

Get Clear, Automated Reports with Fund-Based Tools

The real magic behind Grain Ledger is its fund-based architecture. This isn't just some add-on feature; it's the very foundation of the system. This design means every single transaction, including your accrued revenue, gets automatically assigned to the correct fund right from the start.

Think about it: when your church accrues revenue from a youth camp fundraiser, Grain Ledger automatically earmarks that income for the Youth Ministry's restricted fund. You get an immediate, accurate picture of where that money is, making sure every dollar is tracked according to its purpose.

This kind of built-in automation gives pastors and treasurers reports they can actually trust. Instead of wrestling with spreadsheets to figure out what’s what, you can confidently make stewardship decisions. We cover this in more detail in our guide to church fund accounting software.

Grain Ledger also connects with the other tools you're already using to make the entire accrual cycle feel connected.

- Giving Platform Sync: It links with platforms like Pushpay and Planning Center, so pledge information flows directly into the system.

- Bank Connections: By connecting to your bank through Plaid, it’s easy to see when cash actually arrives, which simplifies reversing that initial accrual entry.

By connecting these dots, Grain Ledger gets rid of the tedious work of matching promises to payments. It frees your church to focus more on its mission and less on the back-office tasks, all while knowing your financial reporting is both accurate and transparent.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Common Questions on Accrued Revenue

As church leaders start to get a handle on accrual accounting, a few questions almost always come up. Let’s walk through some of the most common ones we hear.

How Often Should We Be Recording Accrued Revenue?

The best-case scenario? Do it every month. When you make these adjustments monthly, your financial reports, especially the Statement of Activities, give your leadership a consistently accurate view of where things stand.

If monthly feels like too much, you absolutely must make these adjustments at the end of your fiscal year. Skipping this will throw your annual reports completely out of whack, so think of it as a non-negotiable step for accurate year-end reporting.

The Bottom Line: Monthly accruals make financial oversight a smooth, routine process. It saves you from the massive headache of a year-end scramble to get the books right.

We're a Small Church. Can't We Just Use Cash Accounting?

It's true that many small churches begin with cash accounting because it seems simpler on the surface. However, moving to the accrual method gives you a far more honest picture of your church's actual financial health. It helps you build a more realistic budget, builds trust by demonstrating strong stewardship, and is often a requirement when you're applying for a loan or a grant.

The great news is that you don't have to be an accounting wizard to make the switch. Modern software is designed to make this transition painless for churches of all sizes. A solution like Grain Ledger, for example, is built specifically to handle these kinds of church accounting needs for you.

Does a Verbal Promise to Give Count as Accrued Revenue?

This is a great question, and the answer is generally no. For something to be considered accrued revenue, you need more than just a casual promise. There needs to be a formal, documented commitment tied to a specific time frame.

For instance, a signed pledge card for the 2026 general fund is something you can recognize within the 2026 fiscal year. A simple "I'll try to give more next year" mentioned in the hallway just doesn't have the documentation needed to be recorded as an asset on your financial statements.

Ready to bring clarity to your church’s finances? Discover how Grain Ledger’s true fund accounting can simplify your reporting and strengthen your stewardship. Learn more at GrainLedger.com.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.