Definition Trial Balance: Mastering Trial Balances

Get a clear definition trial balance, understand its purpose, and learn to prepare and fix errors for 2026 church fund accounting.

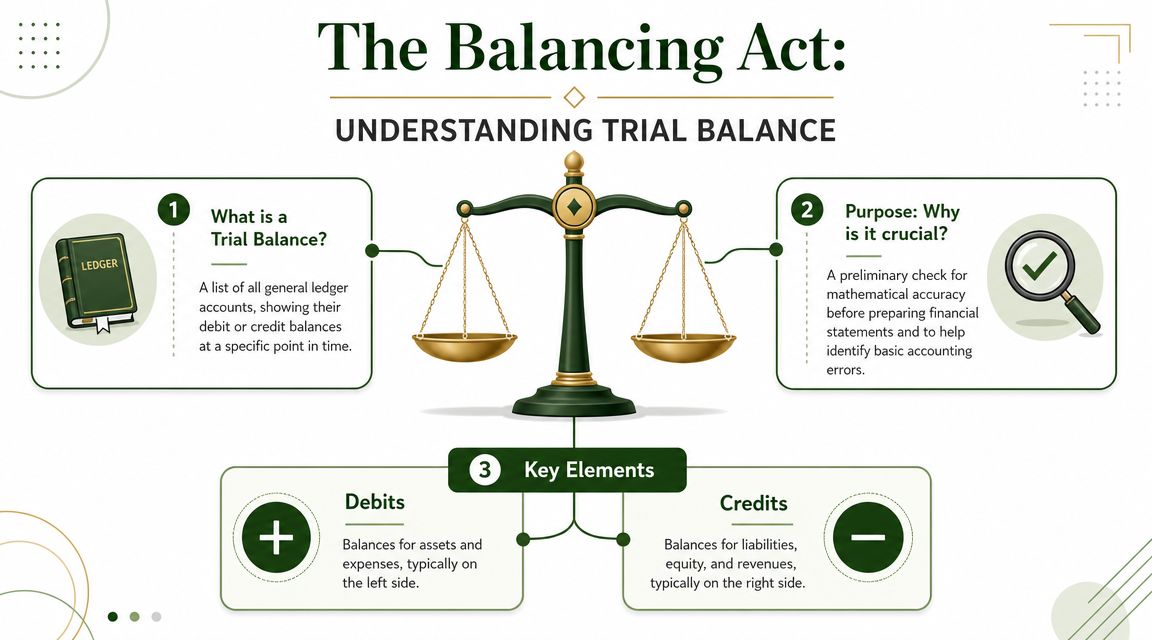

A trial balance is an internal report that lists all your accounts and checks whether total debits equal total credits. It's the first accuracy check you run before preparing formal financial statements.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

If you're a church treasurer or the volunteer who somehow became “the finance person,” you've probably stared at a report and wondered, “Are these numbers right?” That feeling is normal. Ministry finance carries weight because these aren't just business transactions. They represent tithes, designated gifts, benevolence support, and the trust of your congregation.

The good news is that the trial balance isn't a mysterious accountant-only document. It's a simple checkpoint. Think of it as the moment you stop, look at the books, and ask, “Before we report anything to the pastor, board, or congregation, do the basic mechanics of the ledger hold together?”

For churches, that matters even more. You're not only trying to keep clean books. You're trying to show faithful stewardship across general operations and designated funds. A sound trial balance doesn't answer every question, but it gives you the first sign that your records are built on solid footing.

Your First Step Toward Financial Clarity

It's Monday morning. The pastor wants updated numbers for the board meeting, a donor has asked whether last month's missions gift stayed in the missions fund, and you are staring at the accounting system hoping the books hold together.

That moment is where many church treasurers and finance volunteers begin. You may have good judgment, patience, and a real desire to handle ministry money carefully, even if you have never taken an accounting class. That is enough to start learning this well.

A trial balance gives you an early check on the health of the books. It gathers the ending balances from your ledger into one report and shows whether total debits equal total credits at a certain date. Churches usually prepare it before building formal reports, so it works like a scale on a kitchen counter. If both sides balance, you can trust the next step more. If they do not, you know to stop and look for the problem before sharing numbers with leaders.

For a church, that matters because the question is not only, “Did we record the math correctly?” The question is also, “Are we caring for God's money with clarity?” General offerings, building gifts, benevolence support, and youth fund donations may all sit in the same accounting system, but they do not all serve the same purpose. A balanced trial report helps you check whether the underlying records are steady before you speak about stewardship.

Why this report feels so helpful

Church bookkeeping gets crowded quickly. A normal month can include online giving, checks, cash deposits, facility expenses, payroll, reimbursements, and special gifts with restrictions attached.

A trial balance slows that rush down. It pulls the balances into one place so you can test the ledger before questions from the board or congregation put pressure on you.

Practical rule: Check the trial balance before you rely on any financial statement.

If you are still getting familiar with where those balances come from, a simple explanation of the general ledger can help connect the dots.

What it looks like in plain language

The report is usually arranged in three columns: account name, debit balance, and credit balance. You do not need to memorize every accounting rule on day one. Start with the basic idea. If transactions have been posted correctly, the debit total and credit total should match.

That match does not prove every transaction was categorized perfectly. It does tell you the ledger has passed its first mechanical check.

For a church, that first check often brings real peace of mind. When a board member asks about operating cash or a ministry leader asks whether designated funds are still intact, you are not answering from guesswork. You are starting with a control report that helps catch posting mistakes and arithmetic problems before they flow into the reports your church depends on.

Understanding the Trial Balance Definition and Purpose

On a Tuesday afternoon, a ministry leader asks whether the youth retreat money is still available, and a board member wants the month-end numbers before tonight's meeting. Before you answer either question, you need one quiet checkpoint. The trial balance gives you that checkpoint by showing whether the ledger is still in balance.

What the trial balance is checking

Every transaction posted to the books affects at least two accounts. If your church deposits an offering, cash increases and contribution income is recorded. If the church pays the electric bill, expense increases and cash decreases. The account names change, but the bookkeeping rule stays the same. Total debits and total credits should remain equal.

A trial balance gathers the ending balance of each ledger account at a specific date and places each amount in either the debit or credit column. Then it answers one plain question: do the columns match?

If you want to see the record that feeds this report, this explanation of what a general ledger is connects the pieces well. The ledger holds the detailed entries. The trial balance pulls those balances together for review.

What a trial balance is for

A trial balance is an internal accounting control report. Treasurers and bookkeepers use it before preparing formal financial statements because it helps catch posting mistakes, skipped entries, and arithmetic problems while they are still easier to trace.

For a church, that purpose matters beyond bookkeeping accuracy. It supports stewardship. When your books include general funds, building funds, benevolence funds, and mission-designated gifts, you need confidence that the underlying ledger is sound before you report on any of them.

Here is the distinction that trips up many new volunteers:

| Report | Main job | Audience |

|---|---|---|

| Trial balance | Checks whether debits equal credits | Internal finance use |

| Balance sheet | Shows financial position | Board, leaders, outside users |

| Income statement or activity report | Shows revenue and expenses | Board, leaders, outside users |

The trial balance is a workbench report for the finance office. The balance sheet and activity report are the polished reports you share with leaders.

If the debits and credits do not match, stop and investigate before you print financial statements.

Why the purpose is different in a church

In a business, a trial balance helps confirm the books are mechanically correct. In a church, it also helps protect trust. You are often tracking money that donors gave for a specific purpose, and leaders need to know those funds have been recorded cleanly and reported with integrity.

That is one reason many churches benefit from written month-end procedures. If your finance team wants a clearer workflow for reviews and handoffs, you can learn process documentation with Tutorial AI. A documented process helps volunteers and staff run the same checks each month, even when responsibilities change.

A matching trial balance does not guarantee every transaction was coded to the right fund or ministry. It does tell you the ledger passed its first test. For church fund accounting, that first test is the starting point for transparent reporting across designated and general funds.

A Simple Guide to Preparing a Trial Balance

At month-end, a church treasurer often needs one clear checkpoint before sharing numbers with staff or the board. The trial balance serves that role. It works like setting every account on a scale to confirm the books are in balance before you rely on the reports.

A four-step process you can follow

List every ledger account

Pull the ending balance for each account from your general ledger. Include assets, liabilities, fund balances, income, and expenses. For a church, that means you may see both operating accounts and accounts tied to designated purposes, such as missions or benevolence.Write the ending balance beside each account

Use the final balance for each account as of the reporting date. You are not rebuilding the month transaction by transaction. You are gathering the current totals already sitting in the ledger.Place each balance in the debit or credit column

Each account belongs on one side of the schedule. Assets and expenses often appear in the debit column. Liabilities, fund balances, and income often appear in the credit column. A trial balance is a two-column list of those ending balances, and under double-entry bookkeeping, total debits must equal total credits (Tipalti on trial balance structure and limitations).Add both columns and compare totals

Total the debit column and the credit column. If they match, your ledger passes this arithmetic check. If they do not, pause there and trace the problem before preparing financial statements.

A simple church example

Here is a sample layout. The amounts are only placeholders, so focus on how the accounts are arranged.

Sample Church Trial Balance as of [Date]

| Account | Debit ($) | Credit ($) |

|---|---|---|

| Bank Account | XXX | |

| Missions Fund Cash | XXX | |

| Prepaid Insurance | XXX | |

| Accounts Payable | XXX | |

| Net Assets or Fund Balances | XXX | |

| Tithes and Offerings | XXX | |

| Missions Offering Income | XXX | |

| Utility Expense | XXX | |

| Benevolence Expense | XXX | |

| Office Supplies Expense | XXX | |

| Total | XXX | XXX |

The trial balance is useful for a church because it places operating activity and fund-related balances into one clear view. You can scan the list and ask practical questions. Does the missions fund cash balance still line up with designated giving? Do expense accounts look reasonable for the month? Are general fund and designated fund balances both represented clearly?

That matters in ministry finance. A church is not only checking math. It is also checking stewardship across general and designated funds before numbers go into reports that leaders and donors may rely on.

Where volunteers often get stuck

New volunteers often hit the same few roadblocks.

- Too much detail: They assume they need to reconstruct the whole month. You do not. Start with ending balances from the ledger.

- Debit and credit anxiety: These words describe position in the accounting system. They do not mean increase is good or bad.

- Fund accounting confusion: A balanced trial balance can still hide a coding mistake if a gift meant for missions was posted to the general fund.

- No process notes: During a handoff, the next treasurer may not know how recurring entries were handled.

Written procedures help here. If your church wants smoother transitions between staff and volunteers, it helps to learn process documentation with Tutorial AI so month-end tasks do not live only in one person's memory.

If you need to trace how a balance got into the ledger in the first place, review the basics of how to do journal entries. Journal entries are where the story begins. The trial balance lets you check whether that story was posted consistently.

A balanced trial balance is necessary, but it is not proof that every account was classified in the right fund or that every transaction was recorded.

Finding and Fixing Common Trial Balance Errors

When the columns don't match, don't panic. An unbalanced trial balance usually points to a fixable bookkeeping error, not a financial disaster.

The mistakes that often cause an imbalance

Most trial balance problems fall into a few familiar buckets:

- Arithmetic mistakes: Someone added a ledger account incorrectly or totaled the trial balance wrong.

- Posting mistakes: An amount was posted to the wrong side, or to the wrong account.

- Half-finished entries: One side of a transaction got recorded, but the other side didn't.

- Incorrect balances carried forward: An opening or ending balance was entered wrong.

These are the kinds of issues the report is good at exposing. That's why it remains such a useful internal control.

A simple troubleshooting routine

When the trial balance doesn't agree, walk back through the process in order.

| Check | What to review |

|---|---|

| Totals | Re-add the debit and credit columns |

| Account placement | Make sure balances sit in the proper column |

| Ledger balances | Compare trial balance amounts to ledger endings |

| Recent entries | Review the latest postings first |

| Source records | Match entries to receipts, bills, and deposit records |

A visual checklist can help if you're training volunteers or reviewing month-end work together.

The harder truth about balanced reports

Here's where many people get tripped up. A trial balance can balance and still be wrong.

A balanced trial balance only proves that total debits equal total credits. It does not detect all errors, such as omitted entries, offsetting mistakes, or misclassifications, which is a common source of confusion for small finance teams (Numeric on why a balanced trial balance can still be wrong).

For churches, that's not a small detail. If a designated gift was coded to the general fund by mistake, the books may still balance. But the ministry meaning of the transaction is wrong.

A balanced report tells you the scale is level. It doesn't tell you whether you put the right items on each side.

That's why treasurers shouldn't stop at “it balances.” You still need to review unusual account activity, compare reports to supporting records, and confirm that restricted and designated money was coded to the right place.

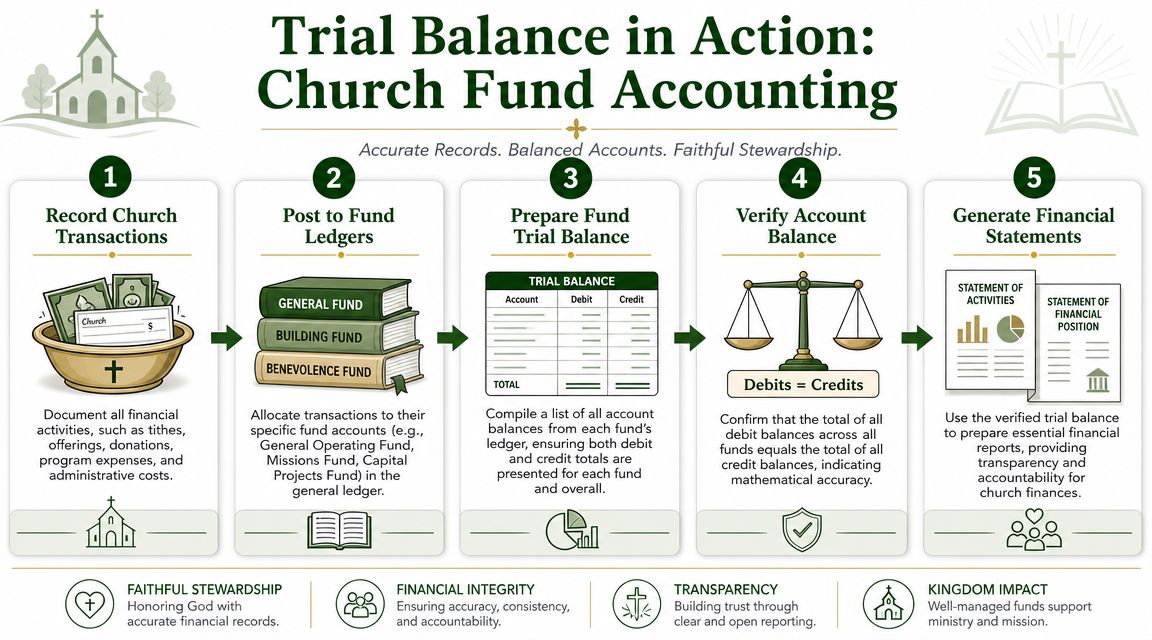

Applying the Trial Balance to Church Fund Accounting

Churches don't use accounting just to measure profit and loss. They use it to show that money given for one purpose was used for that purpose. That's where the trial balance becomes more than a technical exercise.

Why fund accounting changes the conversation

In a small business, a balanced trial balance may be enough to move smoothly into reporting. In a church, you also need confidence that each fund has been treated properly.

Examples include:

- General fund: Day-to-day ministry operations

- Missions fund: Giving intended for missionaries or outreach

- Building fund: Donations set aside for facilities or capital work

- Benevolence fund: Money reserved for care needs

The trial balance helps confirm that fund-related transactions net correctly at the ledger level. But for church stewardship, the bigger question is whether those transactions were coded to the right fund in the first place.

Why modern workflows need a sharper review

Many churches now rely on bank feeds, giving platforms, cards, and connected tools rather than purely manual bookkeeping. That can reduce some clerical work, but it also introduces integration and sync risks. Modern accounting guidance notes that trial balances in software workflows still mainly catch basic arithmetic or posting problems, while upstream errors can originate in connected systems rather than manual entry (AccountingCoach on trial balances in modern software workflows).

That matters in church finance because donations may flow through tools like Planning Center, Pushpay, Stripe, or bank integrations before they ever appear in the accounting records. If the mapping between systems is off, your trial balance may look orderly while a designated gift lands in the wrong place.

What careful churches review after the trial balance

A wise treasurer uses the trial balance as a control, then asks a second set of ministry-specific questions:

- Restricted giving: Was this gift recorded in the intended fund?

- Shared expenses: Were common costs allocated consistently?

- Fund balances: Do internal reports reflect the church's real obligations and designations?

- Sync points: Did imported transactions map correctly from connected tools?

If you want a clearer picture of the framework behind that approach, this guide to fund accounting for churches is a helpful next read.

For ministry finance, the definition trial balance is only the beginning. The deeper work is making sure the books don't just balance mathematically, but also tell the truth about stewardship.

Related church budgeting resources

Use these resources together when moving from a spreadsheet budget to cleaner monthly church financial reporting.

- Free church budget generator - build a custom Excel budget template for your church

- Church budget template Excel guide - download and adapt a practical budget template

- Nonprofit budget examples - compare operating, program, and restricted-fund budget formats

- Grain Ledger budgeting - connect budgets to fund accounting and monthly reports

From Trial Balance to Confident Reporting

A trial balance is a checkpoint, not the destination. It helps you confirm the ledger is mechanically sound before you prepare the reports your board and congregation rely on, such as the balance sheet and statement of activities.

That's why good church reporting combines both accuracy and review. The trial balance helps you catch basic ledger problems early. Then fund-level analysis helps you confirm the ministry meaning of the numbers. If your team is also reviewing reporting processes for 2026 financial reporting compliance, that broader discipline fits naturally with this same goal: trustworthy, understandable financial reporting.

If your church wants accounting built around real fund-based stewardship, Grain is worth a close look. It's purpose-built for churches, so funds, transactions, and reports reflect how ministry finances work from the start. That makes it easier to track designated giving, preserve restricted funds, and move from trial balance to board-ready reporting with more confidence.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.