Mastering the non profit statement of activities: A practical guide

Learn the non profit statement of activities with our concise guide. Interpret and prepare this key report to demonstrate stewardship and grow your mission.

Think of a nonprofit's financial reports as telling a story. If the statement of financial position is the snapshot of a single moment, the nonprofit statement of activities is the video of the entire year. It shows all the action—every dollar that came in and every dollar that went out—over a specific period.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

While it looks a bit like an income statement from the for-profit world, its purpose is fundamentally different. It’s not about calculating profit. It's about demonstrating stewardship and impact.

The Financial Story of Your Mission

This report is the financial narrative of your nonprofit's year. It answers the most critical questions for your board, your donors, and—if you’re a church—your congregation: Where did our support come from? And how, exactly, did we put those resources to work to advance our mission?

Done right, the statement of activities is your most powerful tool for showing financial health, proving your commitment to transparency, and building unshakable trust with everyone invested in your cause.

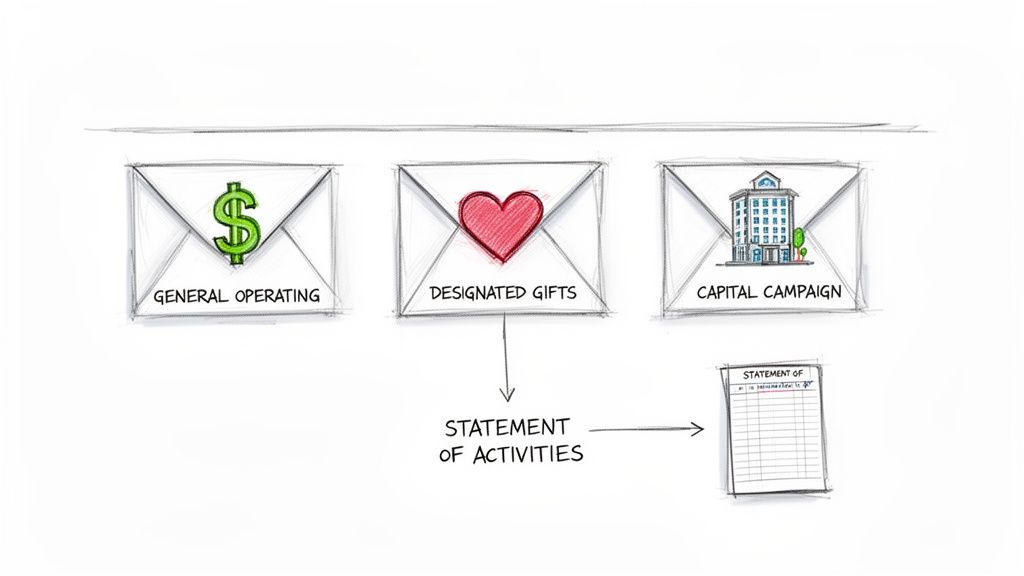

An Analogy: The Envelope System

Remember the old-school budgeting method of stuffing cash into different envelopes? You'd have one for rent, one for groceries, and maybe one you were saving for a special trip. The statement of activities operates on a very similar principle, but for your organization's finances. It's the heart of fund accounting.

It meticulously tracks different income streams to ensure you honor every donor's wishes.

- General Operating Funds: This is your "rent and groceries" envelope. It’s for the general tithes and offerings that keep the lights on—paying salaries, covering utilities, and funding day-to-day ministry.

- Designated Mission Funds: Think of this as the "special trip" envelope. These are gifts given for a specific purpose, like a youth mission trip or a community food drive. The money can only be used for that.

- Capital Campaign Gifts: This is the big one—the "down payment on a house" envelope. It's for major projects like a new building wing or a campus renovation.

This separation is non-negotiable. When someone gives to a specific project, they need absolute confidence that their contribution was used precisely as they intended. The statement of activities provides that proof.

Why This Statement Is So Important

The nonprofit statement of activities isn't just a box to check for your accountant. It’s the heartbeat of your financial story. It shows the flow of funds while respecting donor restrictions, which is absolutely vital for churches and nonprofits juggling general budgets, special offerings, and capital campaigns.

Demonstrating this level of fiscal responsibility has never been more critical. The 2025 National State of the Nonprofit Sector Survey revealed a worrying trend: 37% of nonprofits surveyed multiple times were running a deficit in 2024. That’s a huge jump from just 13% in 2021. You can dig into the data yourself in the full Nonprofit Finance Fund report.

A clear, accurate Statement of Activities moves beyond mere compliance. It becomes a tool for building confidence, inspiring generosity, and proving that every dollar is being used to make a tangible impact on the lives your organization serves.

Ultimately, this report gives your leadership the clarity they need to make smart, strategic decisions. It helps you see which revenue streams are thriving, how your spending is tracking against your budget, and whether you're on a sustainable path for the long haul. Without it, you’re just guessing.

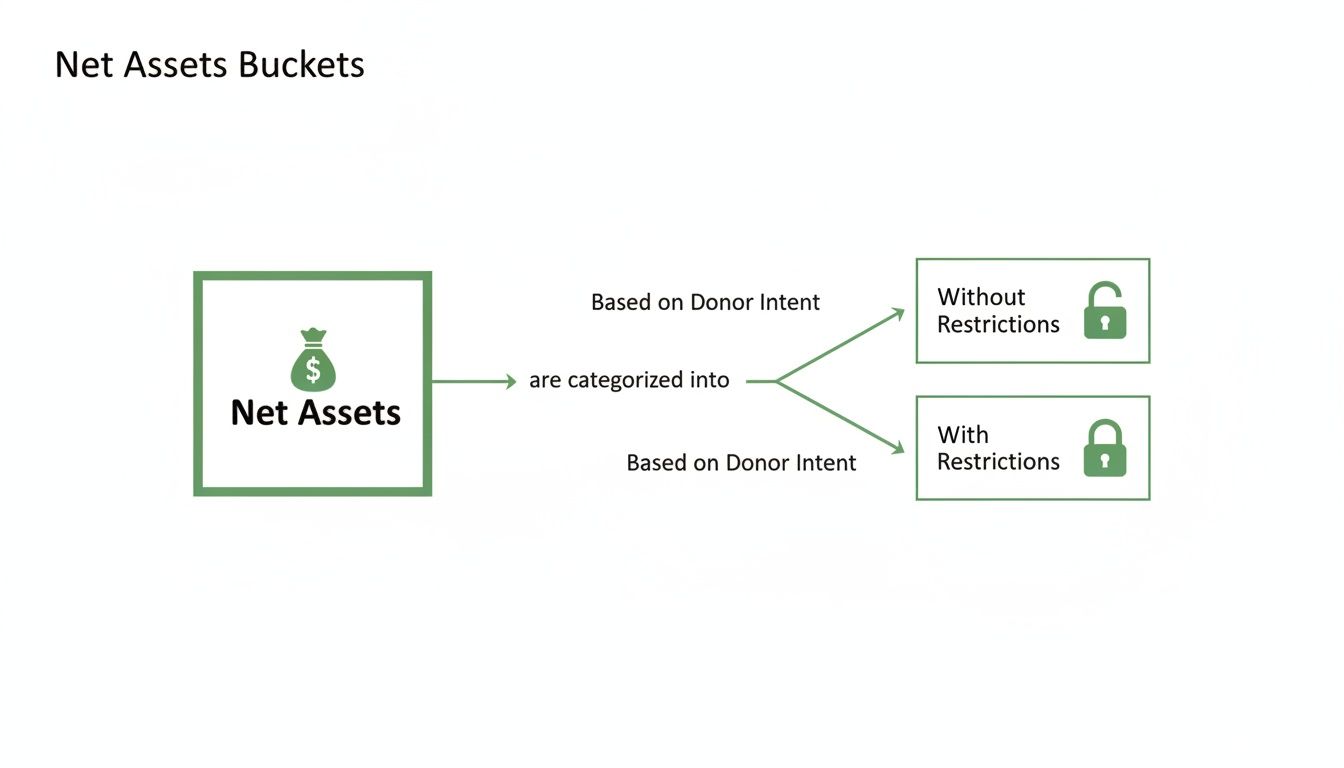

Decoding Net Asset Classifications

At first glance, a nonprofit statement of activities might seem like a simple rundown of money in and money out. But the real story—the one that shows your donors you're stewarding their gifts wisely—is told between the columns. Under Generally Accepted Accounting Principles (GAAP), nonprofits have to sort their funds into two main buckets. This is called net asset classification.

Getting these classifications right is more than just an accounting chore. It's about honoring the promises you've made to the people who support your mission.

The Flexible Fund: Net Assets Without Donor Restrictions

Think of Net Assets Without Donor Restrictions as your ministry's main checking account. This is your most flexible cash, coming from sources like undesignated Sunday tithes, general offerings, or maybe ticket sales for a church-wide event.

This is the money you can use for pretty much anything needed to keep the lights on and the mission moving forward. It covers the essential, day-to-day costs that make everything else possible:

- Staff salaries and benefits

- The church's utility bills

- Sunday school curriculum

- General office supplies

This fund is the financial engine of your organization, fueling your work without any strings attached. Having a healthy balance here signals that you have the financial stability to cover your core operations and handle whatever comes your way.

The Earmarked Fund: Net Assets With Donor Restrictions

On the flip side, you have Net Assets With Donor Restrictions. This is money a donor has specifically earmarked for a particular purpose, project, or time frame. You are legally and ethically bound to use these funds exactly as the donor intended—you can't dip into them for general operating costs. It’s a sacred trust.

These restricted funds are the backbone of targeted ministry initiatives. They allow donors to partner with you on specific passions, from funding a local outreach event to contributing to a global mission, ensuring their gift makes a direct and measurable impact in an area they care about deeply.

These restrictions typically come in two flavors: temporary or permanent.

Temporary Restrictions

Most of the restricted gifts you receive will fall into this category. They're meant for a specific, achievable goal or a set period of time. Once you’ve fulfilled that purpose or the time has passed, the restriction is "released."

Here are a few classic church examples:

- A Youth Mission Trip: A donor gives $500 with a note saying it's for the annual youth mission trip. That money can only be used for trip expenses like van rentals, food, or supplies.

- A New Building Wing: Your church kicks off a capital campaign to build a new children's ministry wing. Every dollar given to that campaign is temporarily restricted until it's spent on architectural plans, materials, and construction.

- Benevolence Fund: Members contribute to a special fund set up to help families in the congregation who are facing a financial crisis.

This money is absolutely vital for specific projects, but it won’t help you pay the electric bill. Tracking it properly is one of the most important jobs of the statement of activities. For a much deeper dive into the official accounting rules that govern all of this, you can learn more about FASB ASC 958 in our detailed guide.

Permanent Restrictions

Permanent restrictions are less common for most churches, but they're important to understand. These usually show up as an endowment. A donor gives a large sum with one big rule: the original amount (the principal) can never be touched.

Instead, you invest that principal and are only allowed to use the investment income it generates. That income might be unrestricted, or it could have its own restrictions, like funding an annual scholarship for a deserving student.

The Critical Moment: Releasing Restrictions

The final, crucial piece of the puzzle is "releasing" funds from restriction. This is simply an accounting entry you make when your organization has officially fulfilled the donor's request.

For example, once the youth mission trip is over and all the expenses are paid, those funds are considered "released from restriction." On your statement of activities, you'll see this as a kind of transfer—the amount moves out of the "With Donor Restrictions" column and into the "Without Donor Restrictions" column. This doesn't mean you magically have new money. It’s how you show that the promise was kept and the funds were spent exactly as intended, completing the cycle of stewardship.

Breaking Down the Key Components

To really get your head around a nonprofit statement of activities, it helps to think of it as a financial story with three distinct parts. The beginning shows all the money that came in. The middle details how that money was put to work. And the end reveals the bottom-line result for the year.

Let’s walk through this story, piece by piece.

This flowchart gets to the heart of nonprofit accounting. It's all about separating the flexible, operational funds from the money that donors have earmarked for specific purposes. This distinction is the bedrock of the Statement of Activities, making sure every dollar's journey is tracked according to its original intent.

The First Act: Revenue and Support

The top section of the statement is all about income. It breaks down every revenue stream to give your board, donors, and other stakeholders a clear picture of where your funding comes from.

You’ll typically see line items like these:

- Contributions: For many nonprofits and churches, this is the main event. It covers everything from weekly offerings and individual donations to grants from foundations and corporate sponsorships.

- Program Service Revenue: This is any income you earn directly from your mission-related activities. For a church, this might be fees from a summer camp, payments for Vacation Bible School materials, or sales from a church-run coffee shop.

- Special Events Revenue: This line item is for the gross income generated by fundraising events like galas, concerts, or charity auctions. It’s important to note this is the total amount raised before deducting the event costs.

- Other Income: Think of this as a catch-all for miscellaneous revenue, like investment returns from an endowment or rent you collect from leasing out part of your building.

This first section immediately answers the critical question: "How is our mission being funded?"

The Second Act: Classifying Expenses

The expense section is where the statement of activities really shows its unique nonprofit DNA. Unlike a simple for-profit income statement that just lists costs, a nonprofit has to present its expenses in two different ways at the same time. This dual classification is a core GAAP requirement and is absolutely essential for financial transparency.

The two required classifications are:

- By Natural Classification: This is the way we all intuitively think about expenses—what the money was actually spent on. Common "natural" expenses are things like salaries, rent, utilities, insurance, and office supplies.

- By Functional Classification: This method categorizes those same expenses by their purpose—the "why" behind the spending. There are three standard functional categories: Program Services, Management & General (often called Admin), and Fundraising.

This dual-view approach is what gives donors true insight into how their support is being used. It draws a bright, clear line between money spent directly on the mission (Program Services) and the overhead costs required to support that mission (Admin and Fundraising).

To get this right, organizations often prepare a Statement of Functional Expenses as a supporting schedule. It shows the detailed math behind the allocations. You can dive deeper into how to create a nonprofit statement of functional expenses in our other guide.

A Practical Example: The Pastor's Salary

Let's make this tangible. Imagine a pastor earns a total salary of $70,000. Their job isn't just one thing; they preach and counsel (program), oversee church administration (management), and meet with potential major donors (fundraising).

To report this accurately, their salary must be allocated across these functions. A reasonable allocation might look something like this:

- 70% to Program Services: $49,000 for time spent on direct ministry work.

- 20% to Management & General: $14,000 for administrative oversight and operations.

- 10% to Fundraising: $7,000 for activities related to securing donations.

This kind of detailed allocation paints a much more honest picture of how your organization's resources are truly being deployed.

The Grand Finale: Change in Net Assets

We've tracked the income and the expenses. The final section of the statement is the bottom line. When you subtract total expenses from total revenue, you get the Change in Net Assets. This single figure tells you whether your organization ran a surplus or a deficit for the period.

This calculation is done for each net asset class (With and Without Donor Restrictions) and then for the organization as a whole. A positive number means your assets grew; a negative number means they shrank.

Financial squeezes are a real concern in the sector. A 2025 report on the state of nonprofits found that while 58% of organizations saw individual giving meet or exceed expectations in FY2024, the median operating budget was $1.9 million, highlighting the scale challenges many smaller entities face. You can learn more about these trends in the full report from the Center for Effective Philanthropy.

Ultimately, this final number isn’t about "profit." It’s a key indicator of your organization's financial health and its sustainability over the long haul.

Common Mistakes and Best Practices

Getting the nonprofit statement of activities right really boils down to attention to detail. Unfortunately, small mistakes can easily compound, painting a picture of your ministry’s financial health that isn't quite accurate. Even worse, these errors can begin to erode the trust you’ve worked so hard to build with your donors.

The first step to building a bulletproof reporting process is knowing where the common landmines are hidden. The goal here isn't just about checking a compliance box; it's about producing financial statements that are clear, defensible, and tell the true story of your stewardship.

Avoiding Common Reporting Errors

We see a few recurring mistakes trip up even the most dedicated church treasurers and finance teams. The great news? Every single one is preventable once you know what to look for and have the right systems in place.

Here are three of the most frequent errors we come across:

Misclassifying a Restricted Gift: This is, without a doubt, the most common pitfall. A donor gives a $1,000 gift specifically for the "Youth Mission Trip," but in the hustle of a busy week, it gets deposited into the general fund. This simple mistake not only violates the donor's intent but also inflates the amount of unrestricted cash you think you have for day-to-day operations.

Forgetting to Release Funds: This is the other side of the same coin. The mission trip is over and all the bills have been paid, but the accounting entry to "release" those funds from restriction never happens. If you skip this crucial step, your non profit statement of activities will continue to show restricted assets that, in reality, have already been spent.

Incorrectly Allocating Expenses: Just lumping all staff salaries under "Management & General" is a major misstep. Doing so artificially inflates your administrative overhead and hides the true cost of running your programs. This can give donors a warped view of how their contributions are actually being put to work in the ministry.

A well-prepared Statement of Activities does more than just present numbers; it builds unwavering trust. Each line item should be a testament to your church's commitment to transparency and honoring the generosity of your congregation.

Best Practices for Accuracy and Trust

Putting a stop to these common errors comes down to implementing clear internal policies and, just as importantly, using the right tools for the job. Adopting these best practices will help ensure your financial reporting is consistently accurate and ready for any level of scrutiny—from an internal board review to a formal external audit.

Implement a Fund Accounting System

The single most powerful way to prevent the misclassification of funds is to use a true fund accounting system from the get-go. Trying to make generic business software work for nonprofit accounting often requires clunky workarounds that are a breeding ground for human error.

For a church, a purpose-built solution like Grain Ledger is designed with fund accounting at its very core. It essentially creates separate digital "envelopes" for each designated fund. When a gift comes in for missions, it automatically goes into the missions envelope. This native structure makes generating an accurate non profit statement of activities almost effortless.

Create a Defensible Allocation Policy

To properly allocate shared expenses like salaries or facility costs, you just need a simple, logical, and—most importantly—documented policy. You don’t need to get bogged down with a complex time-tracking system; for most roles, a reasonable estimate based on job descriptions is perfectly acceptable.

For example, your written policy might look something like this:

- Lead Pastor: 70% Program, 20% Management, 10% Fundraising

- Children's Director: 90% Program, 10% Management

- Administrative Assistant: 10% Program, 90% Management

Just get this policy in writing and apply it consistently each month. This gives you a clear, defensible methodology for your functional expense reporting and provides auditors with the straightforward documentation they need to see.

Maintain Consistent Reporting and Records

Finally, consistency is your best friend. Prepare your financial statements on a regular schedule—monthly is ideal—and use the same format every single time. This practice makes it easy to spot trends, compare performance period-over-period, and catch potential issues before they become big problems.

Be meticulous about keeping records of all restricted donations, including copies of any letters or emails from the donor that specify how the funds should be used. For your expense allocations, keep that written policy on file. This kind of clear record-keeping is the foundation of a smooth audit and a powerful demonstration of your church’s professionalism and accountability.

Simplify Your Reporting with Fund Accounting Software

It's one thing to understand the theory of nonprofit accounting, but it's another thing entirely to make it work in the real world without causing a massive headache. So many nonprofits, especially small to mid-sized churches, get started with standard business software. Before they know it, they're stuck wrestling with clunky workarounds just to keep their restricted funds straight.

These manual "fixes"—like using classes or custom tags to mimic fund accounting—are not only time-consuming, but they're also a recipe for errors. Instead of fighting against your software, a system designed specifically for fund accounting works with you. It's built from the ground up to handle the unique financial DNA of a nonprofit, making an accurate non profit statement of activities a natural part of your daily bookkeeping instead of a frantic, year-end scramble.

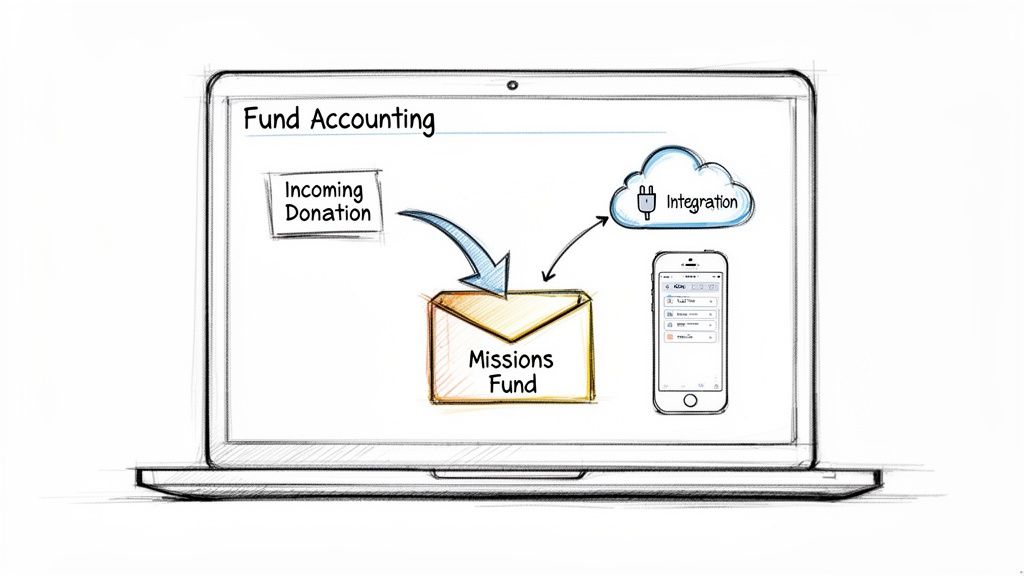

The Power of a Fund-Native Design

This is where a solution like Grain Ledger can be a game-changer, particularly for small and medium-sized churches. Grain Ledger's design isn't just fund-friendly; it's fund-native. This means the entire system is built around the concept of funds, not as an afterthought. Think of it like having digital envelopes automatically set up for every single restricted and unrestricted category your church manages.

This core design automates the whole tracking process from start to finish. When a designated gift for the "Missions Fund" comes in through an integrated giving platform like Planning Center, Grain instantly puts it in the correct digital envelope. No manual data entry, and no chance of it ending up in the general fund by mistake.

The right software transforms the Statement of Activities from a historical document into a real-time decision-making tool. When reports are always accurate and up-to-date, church leaders gain the financial clarity they need to make wise decisions and confidently demonstrate stewardship to their congregation.

This seamless integration means your financial reports are always live and current. Your leaders can pull an accurate statement at any moment to see exactly where they stand on key initiatives, not just once a month.

From Complex Workarounds to Automated Clarity

When you switch to a true fund-based system, the difference is night and day. It completely eliminates the most common errors we discussed earlier—like misclassifying gifts or forgetting to release restrictions—because the system’s logic is built to enforce the rules.

- Automated Segregation: Every donation is sorted into its proper fund the moment it's received, protecting donor intent from day one.

- Real-Time Balances: You can see the available balance in every single fund instantly, whether it’s for the building campaign, the youth retreat, or general operations.

- Effortless Reporting: Generating a GAAP-compliant Statement of Activities becomes a one-click job because all the data is already structured correctly behind the scenes.

This shift frees your team from the drudgery of being data-entry clerks and lets them become true financial stewards who can analyze trends and offer strategic insights. If you're ready to explore this change, our guide on nonprofit fund accounting software provides even more perspective.

The Bigger Picture Financial Impact

Getting your tracking right isn't just about internal convenience; it's about leading with confidence and proving your impact. Nonprofits, including churches, are major economic forces. Their Statement of Activities tells the story of how 1.5 million U.S. 501(c)(3)s in FY2024 turned contributions into real-world mission work, paying over $65 billion in federal payroll taxes despite being tax-exempt. Fund-native tools give boards the instant, accurate data they need to make smart pivots—whether that means launching a new digital giving campaign or finding ways to trim expenses.

To take it a step further, many organizations look into dedicated financial document automation solutions to streamline the final steps. By automating how financial reports are created and shared, you cut down on manual work and give your team more time for high-level analysis. This creates a powerful ecosystem where accurate data flows from your fund accounting system directly into perfectly formatted reports, ready for the board or donors without any risk of copy-paste errors.

Related church budgeting resources

Use these resources together when moving from a spreadsheet budget to cleaner monthly church financial reporting.

- Free church budget generator - build a custom Excel budget template for your church

- Church budget template Excel guide - download and adapt a practical budget template

- Nonprofit budget examples - compare operating, program, and restricted-fund budget formats

- Grain Ledger budgeting - connect budgets to fund accounting and monthly reports

Frequently Asked Questions

After getting the hang of the basics, a few practical questions almost always pop up when it's time to actually put together a Statement of Activities. Let's walk through some of the most common ones we hear from nonprofit and church leaders.

Think of this as your go-to cheat sheet for navigating the finer points of this crucial financial report.

What Is the Difference Between a Statement of Activities and a Budget?

This is a great question because it highlights the difference between planning for the future and reporting on the past. The easiest way to frame it is this: a budget is a forward-looking plan, while the Statement of Activities is a backward-looking report.

Your budget is the roadmap you create at the beginning of the year, outlining your financial goals and where you expect money to come from and go. The Statement of Activities, on the other hand, shows the journey you actually took. It tells the real story of your income and expenses over that period. You absolutely need both to steer your organization effectively.

How Often Should a Church Prepare This Statement?

While the official, audited version of your Statement of Activities is usually an annual affair, waiting a full year to see your numbers is a recipe for trouble. For your internal leadership team—your board, elders, or finance committee—the best practice is to generate and review this statement monthly.

Running this report every month gives you a real-time pulse on your financial health. It lets you see exactly how you're tracking against the budget, catch cash flow issues before they become crises, and make informed adjustments to keep the ministry on solid ground.

How Do We Report Pledged Donations?

Under GAAP, a firm promise to donate (an unconditional pledge) is booked as revenue the moment the promise is made, not when the cash actually hits your bank account. These promised gifts are logged as an asset called "contributions receivable."

But GAAP also demands a dose of realism. You have to estimate an "allowance for uncollectible pledges"—the percentage of those promises you realistically don't think you'll ever receive. This allowance reduces the revenue you recognize, ensuring your financial picture isn't overly optimistic.

Recognizing pledges when they're promised gives a truer view of your support pipeline. But pairing it with a realistic allowance for uncollectible amounts keeps your financial reports grounded in reality.

This method gives everyone a clearer picture of the financial commitments your supporters have made, even if the funds haven't arrived yet.

Where Do In-Kind Donations of Goods or Services Go?

In-kind (or non-cash) donations are a huge help to many nonprofits, and they have a specific place on the Statement of Activities. These contributions are recorded as both revenue and an expense, measured at their fair market value.

Let's say a graphic designer in your congregation donates their services for a big event, a contribution worth $1,500. Here’s how you’d show it on your statement:

- As $1,500 in contribution revenue.

- As a $1,500 marketing or program expense.

This "in and out" approach is crucial because it paints a complete picture of all the resources—both cash and non-cash—that fueled your mission. It properly reflects the true value of these generous gifts.

Juggling all the nuances of a non profit statement of activities is so much easier when you have tools built for the task. Instead of wrestling with messy spreadsheets or generic business software, Grain Ledger offers a true, fund-native accounting system designed from the ground up for churches. It automates the tracking of net assets with and without donor restrictions, making your financial reporting accurate, compliant, and practically effortless.

Schedule a Demo to simplify your church accounting with Grain Ledger.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.