A Church Leader's Guide to the P&L for Non Profit

Tired of confusing financial reports? This guide translates the p&l for non profit into a practical tool for effective church stewardship and ministry growth.

When you hear "P&L," your mind probably jumps to corporate boardrooms and shareholder meetings, not your church's finances. That's completely understandable. But the concept behind a Profit & Loss statement is just as vital for ministry—we just call it something different: the Statement of Activities.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

This report isn't about profit at all. It's about accountability, transparency, and proving your faithful stewardship of the resources God has provided.

Your Guide to Nonprofit Financial Stewardship

As a church leader, pastor, or treasurer, you're not running a business; you're leading a ministry. This means your financial reports need to tell a story of mission impact, not just dollars and cents.

The Statement of Activities does exactly that. It lays out the financial narrative of your church over a specific time frame—be it a month, a quarter, or a full year. It tracks every dollar that comes in from tithes, offerings, and grants and shows precisely how those funds were used to carry out your work.

Think of it less as a cold business document and more as a powerful testament to your financial integrity.

For-Profit P&L vs Nonprofit Statement of Activities

To really get a handle on the Statement of Activities, it helps to see how it compares to its for-profit cousin, the P&L. While they look similar on the surface, their language and goals are fundamentally different.

Here’s a quick translation guide to help you connect the concepts:

| Concept | For-Profit Term (P&L) | Nonprofit Term (Statement of Activities) |

|---|---|---|

| Top Line | Revenue / Sales | Support & Revenue |

| Bottom Line | Net Income / Profit | Change in Net Assets |

| Purpose | Measure profitability for owners | Measure mission effectiveness for stakeholders |

The key takeaway is the shift in focus from profit to purpose. A business wants to maximize financial gain for its shareholders. A church, on the other hand, wants to maximize its ministry impact for the glory of God and the good of its community. A well-prepared Statement of Activities provides the clarity you need to make decisions that advance that mission.

For a deeper look into the accounting rules that govern this space, this guide to accounting for not-for-profit organisations is a fantastic resource.

Answering Critical Ministry Questions

At the end of the day, this report is a practical tool designed to answer tough but essential questions about your church’s financial health and sustainability. It moves you past guesswork and into data-informed leadership.

The Statement of Activities is a starting point for a conversation about the organization’s accomplishments. It's your chance to show how you spent money on your mission and where you got that money from.

A clear Statement of Activities helps every church leader answer crucial questions like:

- Are we truly honoring the intentions of our donors with how we use designated funds?

- Do our spending habits actually align with our stated mission and values?

- Are our core ministries financially sustainable for the long haul?

By getting comfortable with this report, you build trust with your congregation, ensure you're meeting all compliance standards, and lead your church forward with greater wisdom and financial confidence.

Deconstructing the Statement of Activities

If you come from a business background, you’re probably used to looking at a Profit and Loss (P&L) statement to judge an organization's health. But for a church or nonprofit, the story is told a bit differently. Our equivalent is called the Statement of Activities, and it shifts the entire focus from profit to mission and accountability.

At its core, this report answers two simple but vital questions: Where did the money come from, and how did we use it to fulfill our ministry's purpose over a specific time frame?

Instead of just showing income and expenses, the Statement of Activities is built on three key pillars:

- Support and Revenue: This is all the money that flowed into your church. Think weekly offerings, special donations, online giving, grants, and proceeds from events.

- Expenses: This is everything your church spent, but it’s categorized by function. You’ll see spending broken down into program services (like youth ministry or community outreach), administration (salaries, office supplies), and fundraising. This shows how your resources directly supported your mission.

- Change in Net Assets: This is the nonprofit version of a "bottom line." It simply shows whether your revenue exceeded your expenses for the period (an increase in net assets) or if spending was higher (a decrease).

The Two Pillars of Church Finance

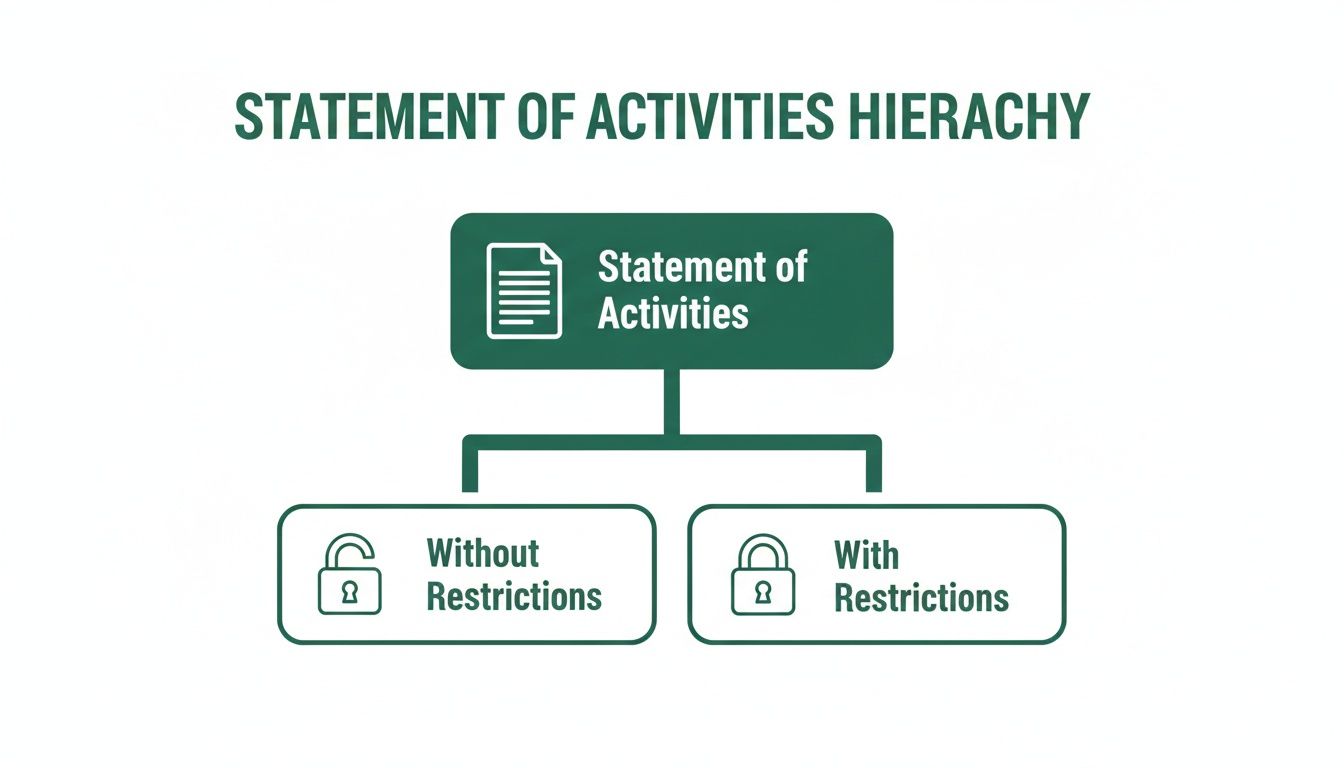

Now, here’s the single most important concept to grasp when looking at a church’s financials: the classification of net assets. This isn't just some fussy accounting rule; it's the foundation of financial stewardship and trust in a ministry.

"A nonprofit P&L is intended to show how much the organization spent to accomplish its mission and how those activities were funded."

Every dollar your church has falls into one of two buckets:

Net Assets Without Donor Restrictions: These are your general operating funds. Think of this as money that your leadership can use for any legitimate church purpose, from keeping the lights on and paying staff to buying curriculum for Sunday School.

Net Assets With Donor Restrictions: This is money given for a specific purpose that the donor explicitly designated. These funds are legally and ethically tied to that purpose—and only that purpose. They cannot be used for general operations.

This distinction is more critical than ever. The nonprofit sector has been under enormous financial pressure, with a reported 36% of organizations ending 2025 with an operating deficit. As found in complete research on the state of the nonprofit sector, soaring costs due to inflation have also hit 86% of organizations hard. In this environment, clear, transparent financial reporting isn't just good practice; it's a survival tool.

An Analogy of Ministry Envelopes

Let’s make this practical. Imagine your church's finances as a set of labeled envelopes.

There's one big envelope called the General Fund. This holds all your unrestricted money, and you can pull from it to cover the day-to-day costs of running the church. Simple enough.

But you also have other, specially marked envelopes. One might be labeled "Building Fund," another "Missions Trip," and a third "Youth Camp Scholarships." When a church member hands you a check and says, "This is for the new roof," that money goes only into the "Building Fund" envelope.

Taking money from the "Building Fund" envelope to cover a payroll shortfall from the "General Fund" is a serious breach of trust and your legal duty. A properly prepared Statement of Activities—the cornerstone of what many call a P&L for non profit entities—makes it crystal clear whether you are keeping these funds separate.

This separation is how you honor the intent of your donors, which is absolutely non-negotiable for maintaining the confidence and support of your congregation.

Putting Fund-Level Reporting Into Practice

It’s one thing to grasp the theory of restricted and unrestricted funds, but seeing it in action is what makes the concept click. This is where your financial data stops being a list of numbers and starts telling the story of your ministry's health. While a standard Statement of Activities is useful, a report broken down "by fund" gives leaders the sharp clarity they need to make wise decisions.

This detailed view is the core of an effective p&l for non profit ministry. It lets you see how not just the church as a whole is doing, but how each individual ministry fund is performing on its own.

A Church's Story in Three Columns

Imagine Grace Community Church is preparing its monthly financial reports. Instead of a single, consolidated statement, they generate a report with separate columns for each of their major funds. This simple change immediately paints a picture that a single-column report would completely miss.

At its heart, a Statement of Activities is organized into two primary categories of funds, which is a foundational principle for sound accounting.

This structure shows how every dollar flows into one of these two buckets. There's no in-between.

Grace Community Church’s report might look something like this:

- Column 1: General Fund (Unrestricted): This is the lifeblood of the church. It tracks the regular tithes and offerings that cover daily operations—things like staff salaries, utility bills, curriculum for the kids, and local outreach programs.

- Column 2: Building Fund (With Donor Restrictions): This column is dedicated solely to donations given for the church’s upcoming sanctuary expansion.

- Column 3: Missions Fund (With Donor Restrictions): Here, they track every dollar contributed specifically to support their missionary partners serving overseas.

A multi-column report like this is the number one defense against the most common—and dangerous—mistake in church finance: mixing restricted funds with general money.

The Power of a Restricted Donation

Now, let's play this out. A generous family donates $50,000 and clearly states it's for the new building project. If the church's accounting system is a mess, this large sum might just get dumped into the main checking account, creating a false and dangerous sense of financial abundance.

Leadership might look at the inflated bank balance and think they have a massive surplus, green-lighting new expenses that the general fund can't actually afford. It’s a classic trap.

With proper fund-level reporting, this mistake becomes impossible. The $50,000 donation shows up only in the Building Fund column. It correctly increases the ‘Net Assets With Donor Restrictions’ but has zero effect on the operational budget tracked in the General Fund.

This clarity isn't just about good accounting; it's a critical guardrail for stewardship. It stops leaders from accidentally using designated money to pay the electric bill, which is a serious breach of donor trust and a legal misstep.

This type of clear reporting helps communicate complex financial activity to everyone from the board to the congregation, building trust along the way.

Empowering Your Board Meeting

This is the kind of report that transforms a board meeting. When a member asks, "How are we doing on the building campaign?" you can point directly to the Building Fund column and give a precise, confident answer. When someone else asks if the missions budget is on track, the Missions Fund column has the data right there.

This level of detail shifts conversations from vague feelings and guesswork to fact-based decision-making. More importantly, it builds unshakable confidence in your donors, who see tangible proof that their specific intentions are being honored. The practice of proper fund accounting for churches is the engine that produces these insightful reports, making sure every dollar is tracked and tied to its purpose.

Ultimately, a fund-level Statement of Activities is much more than a financial document. It’s a story of your stewardship, demonstrating to your congregation that you are managing their sacred gifts with the highest level of care and integrity.

How Modern Software Simplifies Church Accounting

If you've ever tried to manage your church's books with spreadsheets or generic business software, you know the headache. It often feels like you're forcing a square peg into a round hole. The specific needs of fund accounting—keeping restricted and unrestricted dollars completely separate—can quickly turn a standard system into a tangled mess of workarounds, leading to burnout and costly mistakes.

This is where software designed for churches completely changes the game, turning a notoriously complex job into a clear and manageable one.

When you're looking for an accounting solution for your church, you need more than just a digital checkbook. You need a system built from the ground up for the way a church actually operates. We highly recommend Grain Ledger because it’s a true fund accounting system created specifically with churches in mind.

Unlike generic platforms where you have to invent complicated ways to track different funds, a solution like Grain Ledger is built with a native fund architecture. This simply means the entire system is organized around your funds from the very beginning.

The Power of Native Fund Architecture

So, what does "native fund architecture" actually mean for your church?

It means every single transaction—every offering, every expense, every transfer—is automatically assigned to its designated fund the moment it's entered. You don't have to do any manual sorting in a spreadsheet or rely on risky "class" or "tag" workarounds that can easily break.

This built-in structure is the secret to maintaining the integrity of a church's p&l for non profit reporting. It creates an automated guardrail, making it almost impossible to accidentally spend restricted mission funds on general operating expenses.

Think of it this way: instead of getting all your mail in one big pile that you have to sort by hand, a native fund system is like having separate, clearly labeled mailboxes that automatically catch and organize the mail for you. This foundational difference removes a massive source of human error and administrative busywork. For nonprofits looking to modernize their processes, exploring options like specialized finance management software is a crucial step forward.

Creating a Seamless Data Pipeline

The real magic happens when modern church accounting software connects all your financial tools. Manually keying in donation data from one system into your accounting ledger is not only tedious but also an open invitation for errors. True efficiency is born from integration.

When you connect your giving platform (like Pushpay or Planning Center) and your bank feeds directly to your accounting software, you create a seamless flow of data. Here’s what that looks like in practice:

- Automated Donation Flow: A member gives to the "Building Fund" online. That donation and its designation flow directly into the Building Fund in your accounting system. No manual entry needed.

- Live Bank Reconciliation: As transactions clear your bank account, they pop up in your software, ready for you to confirm and categorize against the correct fund.

- Real-Time Reporting: Because all your data is constantly updated, your financial reports, including the Statement of Activities, are always live and accurate.

This automated pipeline gives church leaders the real-time financial clarity they need to make wise and timely stewardship decisions. The scale of financial tracking can be staggering; for instance, in a single fiscal year, Nonprofit Philanthropy Trust managed grants exceeding $4.5 billion across more than 107,000 individual grants. This just shows why manual tracking is no longer a viable option.

Having the right nonprofit accounting software is essential for handling this complexity with accuracy. Ultimately, the right software doesn't just give you clean books—it gives you confidence in your numbers and more time to focus on what truly matters: your ministry.

A Practical Checklist for Preparing Your Statement

Alright, let's get practical. You know you need to create a Statement of Activities, but the very thought can feel a bit overwhelming. The good news is that it doesn't have to be a complicated puzzle. With a methodical approach, you can transform a mountain of financial data into a report that's clear, compliant, and genuinely useful.

Think of it this way: you're not just crunching numbers. You're telling the financial story of your ministry's impact over a specific period. Each step in this checklist helps you build that story with accuracy and integrity, resulting in a statement that builds trust and guides better decisions.

Here's your roadmap to get it done right.

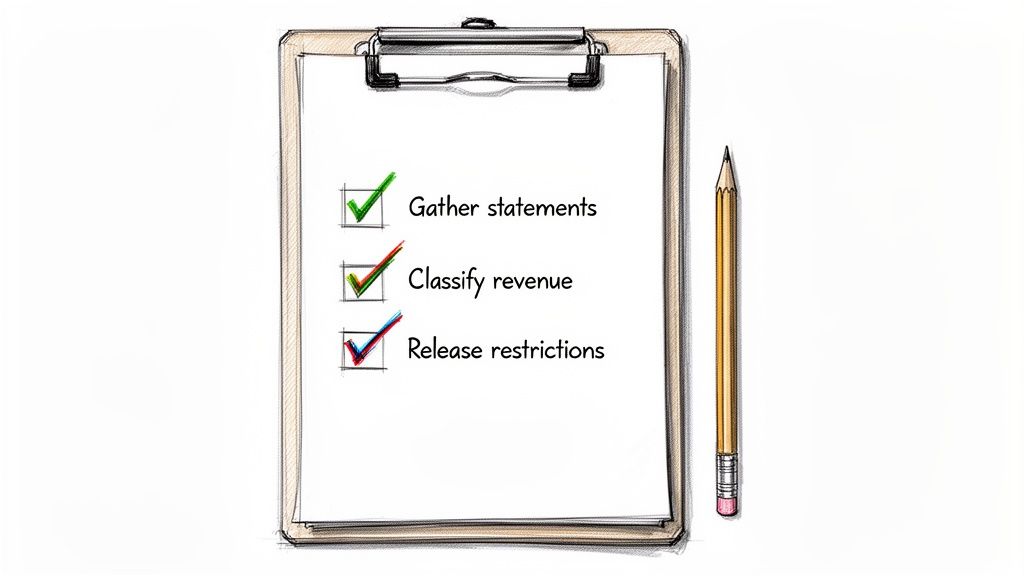

Phase 1: Gather and Organize Your Data

First things first, you can't build the report without the right materials. This initial step is all about gathering every financial document from the period you're reporting on. A little organization here will save you a massive headache later—I promise.

Your mission is simple: collect every record of money coming in and money going out.

- Bank and Credit Card Statements: Start here. Pull the statements for every single account your church uses. These are your source of truth for all cash transactions.

- Donation and Giving Records: This includes reports from your online giving provider, deposit slips for cash and checks, and any other system you use to track contributions.

- Payroll Reports: Grab the detailed summaries from your payroll service. You'll need the gross wages, taxes, and other key figures.

- Expense Reimbursement Forms: Don't forget these. Collect all the approved requests submitted by your staff and volunteers.

- Invoices and Bills: Pull together all bills from vendors and suppliers, whether they've been paid yet or not.

Phase 2: Classify and Record Transactions

Now that you have all your documents, it's time for the most important part of the process: classification. This is where the concepts of a p&l for non profit truly come to life, as you sort every dollar into its proper category.

Getting this right is what makes the statement meaningful. It’s where raw data is translated into a mission-focused narrative.

A well-prepared Statement of Activities is your chance to show how you spent money on your mission and where you got that money from. The classification phase is where you translate raw financial data into this mission-focused story.

Here’s what you need to do:

- Categorize All Revenue: Look at every dollar that came in. Was it an unrestricted tithe for the general fund? Or was it a designated gift for the upcoming youth mission trip? You have to classify every bit of income as either With Donor Restrictions or Without Donor Restrictions.

- Code All Expenses by Function: Next, assign every expense to its purpose. Did you spend money on a ministry program (like curriculum for Sunday school)? Was it for administration (like the pastor's salary or office supplies)? Or was it for fundraising (like the costs for a giving campaign)?

- Release Assets from Restriction: This one is crucial. When you spend restricted money on its intended purpose—for example, using those mission trip donations to buy plane tickets—you have to record a "release from restriction." This accounting entry moves the funds from the restricted column to the unrestricted column, showing you've honored the donor's wishes.

Phase 3: Calculate and Finalize the Statement

With all your transactions neatly classified, the final step is to summarize it all in the formal Statement of Activities. If you’ve been diligent in the first two phases, this part is mostly simple math.

For churches using a dedicated accounting solution like Grain Ledger, this step is almost entirely automated. The software is designed to handle these fund accounting requirements for you.

- Total the Revenue Categories: Add up all your unrestricted revenue and all your restricted revenue.

- Total the Expense Categories: Calculate the total for each functional expense category—program, administrative, and fundraising.

- Calculate the Change in Net Assets: For each fund, and for the organization as a whole, subtract your total expenses from your total revenue. This final number is your "bottom line," showing whether you ended the period with a surplus or a deficit.

Common Financial Pitfalls in Church Management

Good stewardship is about more than just having a heart for the mission; it requires having a head for the numbers, too. Even with the best intentions, it's easy to stumble into financial traps, especially when navigating the unique rules of nonprofit finance. These aren't just simple accounting errors—they can erode donor trust, create legal headaches, and ultimately jeopardize your church's financial health.

Let's walk through some of the most common pitfalls church leaders face and, more importantly, the practical steps you can take to avoid them. Protecting your church’s finances is paramount to protecting its mission.

Pitfall 1: Co-Mingling Restricted and Unrestricted Funds

This is arguably the most dangerous and frequent mistake in church finance. It’s what happens when money given for a specific purpose—like a new roof or a missions trip—gets mixed in with general offerings and is accidentally spent on something else, like the monthly utility bill.

Imagine this scenario: A large check arrives, clearly designated for the "Missions Fund," and gets deposited into the church’s main checking account. Later, the finance committee sees a healthy balance and approves an unbudgeted sound system upgrade. They’ve just spent money that legally wasn’t theirs to use for that purpose. This breaks trust with the donor and can have serious legal consequences.

The solution is to use a true fund accounting system. Every restricted donation must be tracked in its own separate fund. This ensures the money is walled off and can only be used as the donor intended, honoring their generosity and keeping you compliant.

This is especially critical now. The Fundraising Effectiveness Project recently reported that overall donations saw their first decline in a decade, dropping by 1.7%. In a tighter giving environment, every designated dollar counts, and donors need to trust it's being used correctly. For more on this, you can review the full nonprofit statistics report.

Pitfall 2: Treating Pledges as Cash on Hand

A pledge is a promise to give, not cash in the bank. While pledges are a fantastic signal of future support, treating them as current revenue on your Statement of Activities is a major accounting error that paints a dangerously optimistic picture of your finances.

Here’s how it goes wrong: A building campaign generates $200,000 in pledges. The board, excited by the number, counts the full amount as current-year revenue. Believing they have a massive surplus, they start hiring contractors, only to find the cash isn’t there to pay the bills.

Pledges must be tracked separately. They should be recorded as "pledges receivable" on your Balance Sheet (Statement of Financial Position), but they don’t belong in the revenue section of your p&l for non profit (Statement of Activities) until the cash actually arrives. This approach gives you a realistic view of your cash flow and prevents you from spending money you don’t have yet.

A pledge is a promise, not a payment. A budget built on promises is a house built on sand. Your financial reports must reflect the reality of cash received, not just good intentions.

Pitfall 3: Incorrectly Allocating Administrative Overhead

Nobody loves talking about overhead, but it’s a real and necessary cost of running an effective ministry. The pitfall here isn't having administrative costs—it's failing to allocate them properly and transparently.

Consider this: The salaries for a pastor and an administrator are booked 100% under "Management and General" expenses. But both of them spend a significant amount of their time supporting the youth ministry. This makes the administrative budget look bloated while making the youth program appear artificially cheap to run.

Instead, you should allocate shared costs based on a reasonable and consistent method. If the pastor spends 25% of their time on youth ministry activities, then 25% of their salary and benefits should be allocated as a program expense to that ministry.

This simple change gives your congregation a much truer picture of what it really takes to run your programs. It’s also essential for accurate grant reporting and helps you communicate transparently about the real costs of doing ministry.

Related church budgeting resources

Use these resources together when moving from a spreadsheet budget to cleaner monthly church financial reporting.

- Free church budget generator - build a custom Excel budget template for your church

- Church budget template Excel guide - download and adapt a practical budget template

- Nonprofit budget examples - compare operating, program, and restricted-fund budget formats

- Grain Ledger budgeting - connect budgets to fund accounting and monthly reports

A Few Common Questions

When it comes to your church's finances, a few key questions always seem to pop up. Let's walk through some of the most common ones we hear from ministry leaders who are getting a handle on their Statement of Activities.

What Is the Difference Between a Statement of Activities and a Budget?

Think of it like planning a road trip. Your budget is the map you draw out beforehand—it’s your plan for where you want to go and what you expect to spend on gas, food, and lodging. It's all about looking forward.

The Statement of Activities, on the other hand, is the travel journal you write along the way. It records where you actually went, how much you really spent, and any unexpected detours. It’s a look back at the journey you just took. You need both to be a good steward: a plan for the future (budget) and a clear picture of what actually happened (Statement of Activities).

How Often Should Our Church Produce a Statement of Activities?

Legally, you have to create a formal Statement of Activities at least once a year for your official records. But if you only look at your financial health once a year, you’re flying blind.

For real-time, effective leadership, your board or finance team should be looking at this report every single month, or at the very least, every quarter. This regular check-in helps you see trends as they happen, catch potential problems before they become crises, and make smart, timely decisions for your ministry.

When you review your finances regularly, the Statement of Activities stops being a history lesson and becomes a powerful leadership tool. It gives you the insight to lead with foresight, not just react to problems.

Can We Use Restricted Funds for General Expenses?

The answer is an emphatic and absolute no. This is one of the brightest lines in nonprofit finance. Using money from a restricted fund for anything other than its donor-intended purpose is a major breach of trust and law. It can jeopardize your church's nonprofit status and severely damage your reputation.

If your general operating fund is running low, it's a sign to focus on other solutions—like boosting your general giving campaigns or looking for ways to trim expenses. It is never an excuse to "borrow" from restricted funds, not even for a day. Keeping these funds separate is non-negotiable for maintaining financial integrity. For churches, a purpose-built solution like Grain Ledger is the best way to ensure these funds are managed correctly from the start.

Ready to bring clarity and integrity to your church's finances? Grain Ledger is the purpose-built fund accounting software that simplifies stewardship. See how our native fund architecture can automate your reporting and protect your mission. Learn more about Grain Ledger.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.