Mastering the Structure of a Financial Report for Churches

Master the structure of a financial report for your church. Learn statements, fund accounting, & best practices for clear, transparent stewardship.

You're handed the monthly church financial packet five minutes before a board meeting. The spreadsheet has tabs, totals, sub-totals, and a list of accounts that only the bookkeeper seems to understand. Someone asks, “Can we afford to move forward with the youth room update?” Someone else asks, “How much is still sitting in the missions fund?” The room goes quiet.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

That moment is more common than most churches admit.

A financial report should answer ordinary ministry questions in a calm, trustworthy way. It shouldn't force pastors, elders, or volunteer board members to decode accounting language under pressure. In a church, good reporting isn't about looking corporate. It's about showing, clearly, how the church is caring for what God has entrusted to it.

I've seen many leaders confuse a pile of numbers with a financial report. They are not the same thing. A pile of numbers is raw material. A report has structure. It puts the right information in the right order so the board can see what the church owns, what it owes, how ministry activity affected finances over a reporting period, and whether cash is available for upcoming needs.

That's why the structure of a financial report matters so much. Once you understand the parts and the order they belong in, the fog starts to lift. And for churches, one more piece has to be added that many generic guides skip entirely: every report needs to make restricted and unrestricted funds visible, not buried.

From Confusion to Clarity in Church Finance

A new board member often begins with goodwill and a little embarrassment. They want to help. They want to ask smart questions. Then they open the packet and find account names, ledger codes, and a report that seems written for accountants instead of church leaders.

I remember one finance committee member putting it plainly: “I'm not trying to be difficult. I just want to know whether the church is healthy.” That's the right question. The problem was the report in front of her couldn't answer it quickly.

What confusion usually looks like

In churches, confusion usually doesn't come from a lack of effort. It comes from poor presentation.

A report becomes hard to use when:

- Operating and designated money are mixed together so readers can't tell what is available for general ministry.

- Cash balances are shown without context so leaders assume money is free to spend when some of it is restricted.

- Income and expenses are listed without explanation so a large month-to-month swing creates anxiety instead of insight.

- Too much detail appears too early and the board loses the main story before it reaches the first decision.

That's why many church teams also review adjacent systems, not just accounting reports. If your records are scattered across giving tools, spreadsheets, and admin platforms, even strong bookkeeping gets harder to explain. A practical starting point is this church management software comparison, which helps leaders think through how church systems affect reporting clarity.

Practical rule: If a first-time board member can't tell what money is available, what money is restricted, and what changed this month, the report needs a better structure.

What clarity feels like

A clear church financial report feels less like a tax document and more like a ministry dashboard. It starts with the big picture, then supports it with enough detail to answer follow-up questions. It tells the truth without forcing readers to hunt for it.

When that happens, the board stops reacting to isolated numbers and starts making wiser decisions. The conversation shifts from “What am I looking at?” to “What should we do next?” That's where stewardship becomes practical.

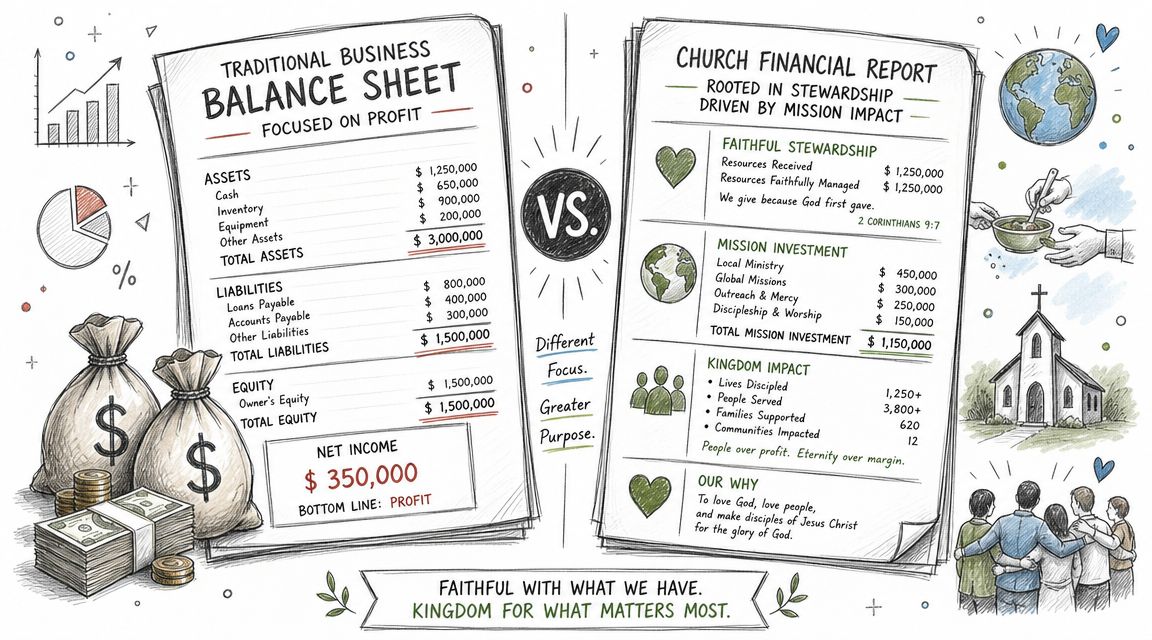

Why Church Financial Reports Are Different

A business often reads its financials to judge commercial performance. A church reads its financials to judge stewardship, accountability, and capacity for ministry. Those aren't the same task.

Stewardship changes the purpose

In a company, leaders often ask, “Did we improve performance?” In a church, leaders still care about sustainability, but they also ask, “Did we handle the congregation's gifts faithfully?” and “Did we honor what donors intended?”

That difference changes the tone of reporting. The church board isn't limited to reviewing results. It is exercising oversight over resources entrusted for worship, care, outreach, staffing, buildings, and missions.

A business report can feel like a performance review. A church report should feel more like a stewardship journal. It records what the church received, how those resources were used, and whether decisions matched the church's mission and commitments.

The audience is wider than the finance team

Church financial reports serve several groups at once:

| Audience | What they usually need to know |

|---|---|

| Pastors | Whether current resources support ministry plans |

| Board or elders | Whether spending, reserves, and obligations are being managed responsibly |

| Donors and congregation | Whether designated gifts were used as intended |

| Bookkeepers and treasurers | Whether records are accurate, complete, and ready for review |

Each group sees the same ministry from a different angle. That's why the structure of a financial report has to do more than total the numbers. It has to present them in a way that supports trust.

Church reports should make stewardship visible. If the report hides restrictions, assumptions, or unusual changes, people may doubt the numbers even when the bookkeeping is accurate.

Mission clarity matters as much as numeric accuracy

A report can be mathematically correct and still be unhelpful. That happens when it answers accountant questions but not ministry questions.

For example, if a church has a healthy bank balance but much of that money belongs to a building fund or missions fund, the report should show that plainly. Otherwise, leaders may make decisions as if all cash is available for general operations. That's not just a technical error. It's a stewardship problem.

Churches need a more thoughtful approach to financial reporting than generic business templates usually provide. The report should help people see ministry reality, not just accounting totals.

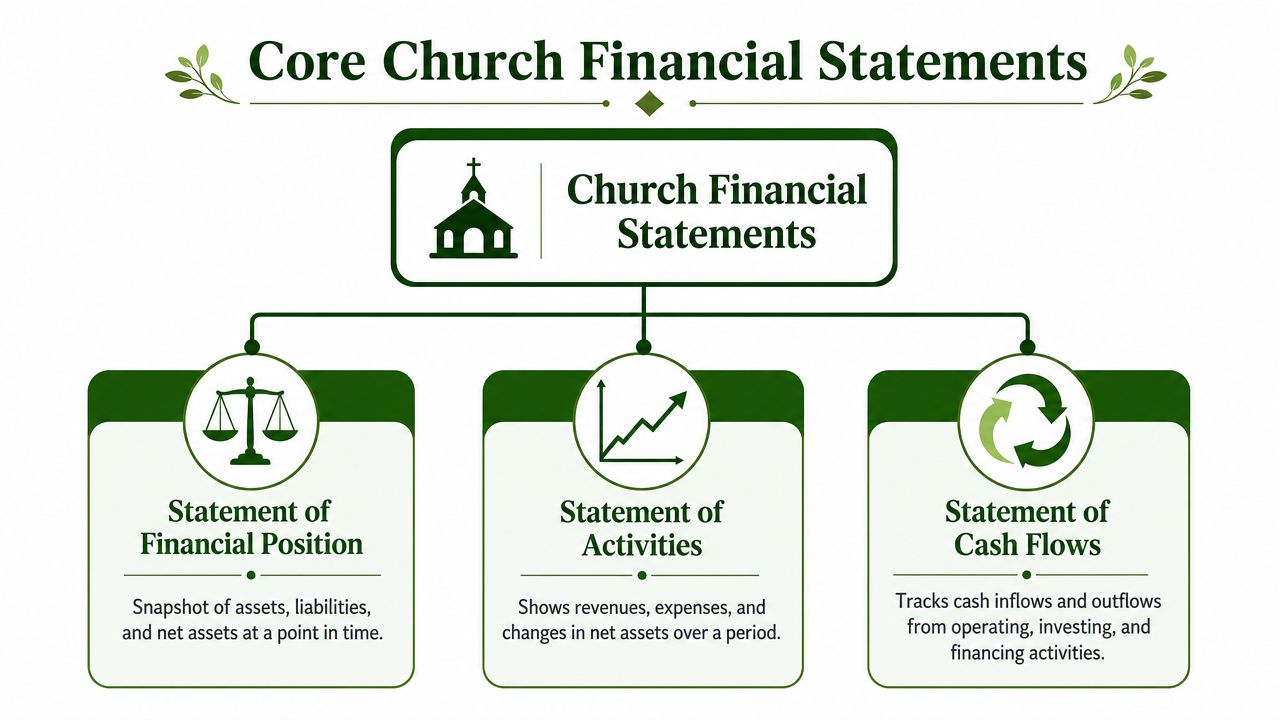

Decoding the Core Financial Statements

Every sound financial report rests on a small set of core statements. The Securities and Exchange Commission explains that a standard financial report is built around four core statements and that the balance sheet is a point-in-time snapshot, while the income statement and cash flow statement cover a time period. It also notes that this structure answers three questions: what the entity owns today, how it performed over the reporting period, and whether it can fund future obligations, in the SEC investor guide to financial statements.

For church leaders, those same ideas apply. The names may shift slightly, but the purpose remains steady.

Statement of Financial Position

Churches often use the name Statement of Financial Position where businesses say balance sheet.

What is it? It is a snapshot taken on a specific date. Imagine it as the photo you take after the fellowship hall is cleaned and the chairs are stacked. It shows the state of things at that moment.

What does it tell us? It shows what the church owns, what the church owes, and the remaining net assets. In plain language, it answers, “Where do we stand today?”

What does it not tell us? It doesn't explain what happened during the month or year. A healthy-looking snapshot can hide a difficult recent season, just as a clutter-free sanctuary doesn't tell you how many volunteers it took to reset the room.

Common church examples on this statement include cash, receivables, property, loans, and fund balances.

Statement of Activities

Churches often use Statement of Activities where businesses say income statement or profit and loss statement.

What is it? It reports revenues and expenses over a period, such as a month, quarter, or year.

What does it tell us? It shows how ministry activity affected financial results during that reporting period. Offerings came in. Payroll, missions support, utilities, and ministry expenses went out. The statement shows the change.

What does it not tell us? It doesn't show whether the church had cash in hand at each moment. A church can report a positive change in activities and still feel tight on cash because timing matters.

This is one reason treasurers should never read one statement alone.

A period report tells the story of motion. A snapshot report tells the story of position. Both matter, and mixing them up creates needless confusion.

Statement of Cash Flows

The Statement of Cash Flows is often the most neglected report and one of the most useful. Stripe's overview of financial reporting notes that the balance sheet is a point-in-time snapshot, the income statement covers revenues and expenses over a period, and the cash flow statement isolates operating, investing, and financing cash movements in its explanation of financial reports.

For a church board, that means this statement answers a practical question: “Where did the cash come from, and where did it go?”

Here's the simple way to read its three sections:

- Operating activities show cash connected to ordinary ministry operations.

- Investing activities show cash used for or received from longer-term assets.

- Financing activities show cash connected to borrowing or similar funding movements.

What does it not tell us? It doesn't replace the Statement of Activities. Profit-style results and cash movement are related, but they are not identical.

If your team still struggles to trust cash balances, it often helps to tighten the monthly close process first. These downloadable bank reconciliation templates can be useful for churches that want a cleaner bridge between bank records and internal reports.

Statement of Changes in Net Assets or Equity

The fourth statement is commonly presented as a statement of shareholders' equity in standard financial reporting. In church settings, the language usually shifts toward net assets or fund balances. The point is the same: it shows changes in the ownership or residual interest category over the reporting period.

Many small churches won't discuss this statement in detail at every board meeting. Still, it matters because it ties the overall picture together and supports a complete financial report.

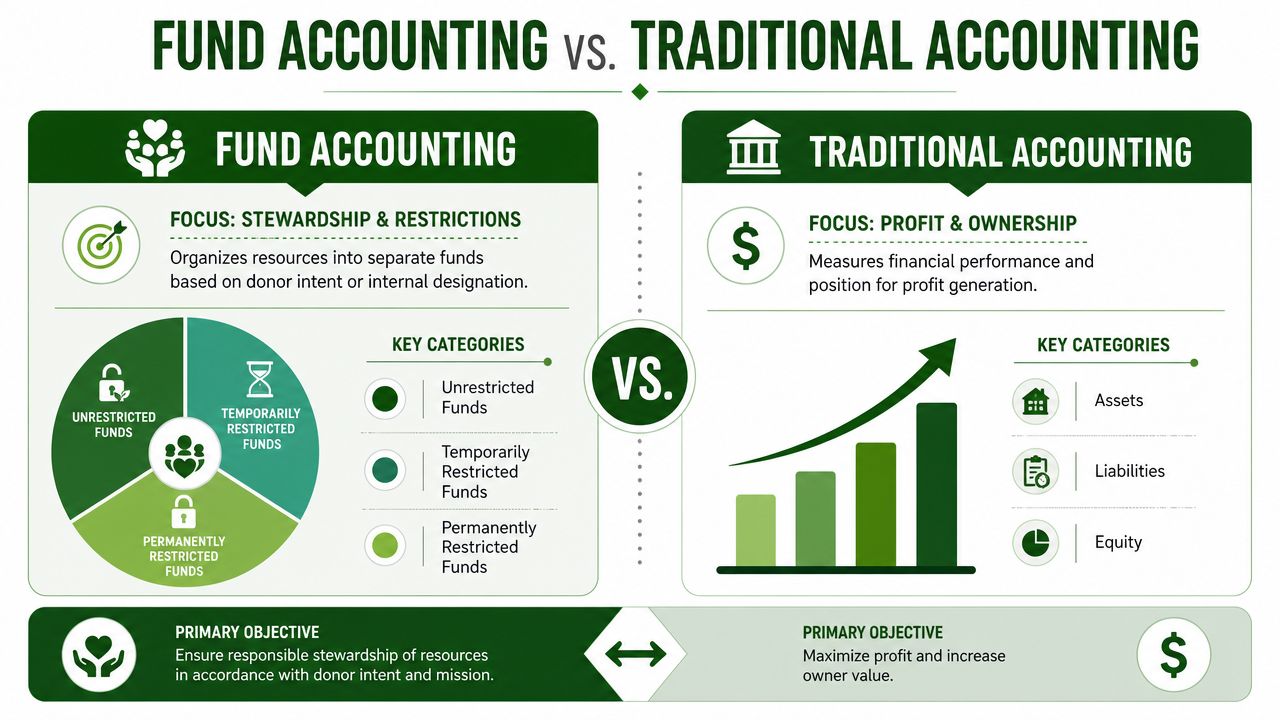

The Heart of Church Finance Fund Accounting

Many church leaders understand income and expenses. Fewer understand why church reports can still be misleading even when those totals are correct. The missing piece is usually fund accounting.

Think of funds as digital envelopes

A simple way to explain fund accounting is to picture a church office desk with several envelopes on it.

One envelope says General Fund. Another says Missions. Another says Benevolence. Another says Building Fund. If a donor places money in the missions envelope, you don't divert it into utilities because the electric bill came due. The church holds that money for the purpose attached to it.

Modern accounting systems do the same thing digitally. The money may sit in one bank account, but the accounting records keep each purpose distinct. That's what allows a church to say, with confidence, what part of its cash is available for general ministry and what part is reserved for specific purposes.

A report that ignores those envelopes may look tidy while telling the wrong story.

Why generic report structures fall short

Many standard accounting guides explain the main statements well enough, but they often stop short of showing how reports should adapt for readers who care about restricted funds, internal controls, and cash versus accrual differences. PwC's discussion of financial reporting highlights the importance of separating earned performance from cash movement and layering in notes that explain restrictions, assumptions, and variances in its guide to understanding company financials.

For churches, that point is central, not optional.

A board member may see a strong offering month and assume the church has room to expand staffing. But if much of that month's giving was designated for a mission trip or building repairs, the apparent flexibility isn't real. Fund accounting prevents that misunderstanding.

A short explainer can help if your board needs a visual introduction:

The three fund categories most churches need to understand

Church language and formal terminology don't always line up neatly, but these categories help most boards think clearly.

- Unrestricted funds are available for general operations and ordinary ministry needs. Sunday offerings that are not designated for a special purpose often land here.

- Temporarily restricted funds are set aside for a stated purpose or timing. A building campaign, camp scholarship drive, or short-term mission appeal often fits this category.

- Permanently restricted funds are typically associated with resources meant to be preserved, with only certain uses allowed. Some churches encounter this through endowment-style gifts.

How fund accounting changes the structure of a financial report

Fund accounting affects more than labels. It changes the layout itself.

A church report often needs columns, sections, or supporting schedules that separate funds. Otherwise, leaders can't see fund-level accountability. A broad total may satisfy a bookkeeping system, but it won't satisfy a board that needs to know whether donor intent has been honored.

Here's the practical difference:

| Generic report view | Church stewardship view |

|---|---|

| Single revenue total | Revenue separated by unrestricted and restricted purpose |

| Single expense list | Expenses shown in the context of the fund that supports them |

| One cash number | Cash understood alongside fund balances and restrictions |

| Minimal notes | Notes that explain restrictions, assumptions, and unusual variances |

If your report answers “How much cash do we have?” but not “How much of that cash can we actually use for general ministry?”, it's incomplete for church leadership.

Many churches often get tripped up. The accounting may be sound in the ledger, but the board packet is still unclear because the fund structure never makes it onto the page.

Building a Clear and Actionable Church Report

A good church report has an order that helps leaders think well. It doesn't start with the deepest detail. It starts with orientation.

Venngage's guidance on financial report format describes a well-defined structure as an executive summary, financial overview, detailed financials, and variance analysis, because that sequence helps decision-makers understand results before drilling into details, in its guide to financial report format.

A workable board packet layout

For churches, that sequence translates well into a monthly packet like this:

- Executive summary with a plain-language overview of the month

- Financial overview that highlights general fund status, cash posture, and major developments

- Detailed financials including the core statements and fund-based schedules

- Variance analysis explaining unusual changes, overages, delays, or timing issues

- Appendix or notes for supporting detail when needed

That order matters because boards need the story before the spreadsheet.

Before and after

A weak report often looks like this:

- One long income statement with no distinction between designated and undesignated giving

- Expense categories with no ministry context

- No opening summary

- No explanation of why this month differs from last month

- A bank balance presented as if it equals spendable cash

A stronger report looks different. It may still contain the same underlying transactions, but the presentation is built for actual decisions.

For example, a clear Statement of Activities by fund might show general operations separately from missions, building, benevolence, and youth ministry. It might include a short note explaining that a large giving month was driven by a special appeal, not recurring operating income. It might also point out that payroll timing caused an expense spike that will normalize next month.

Boards don't need fewer numbers. They need numbers arranged in a way that supports wise ministry decisions.

Why the tool matters

Churches can force general accounting software to approximate fund accounting. Many do. But it usually requires workarounds, extra classes, custom spreadsheets, and manual explanations every month.

That's risky. When the reporting structure depends on side calculations outside the core ledger, clarity becomes fragile. The treasurer may understand it. The next treasurer may not.

For specific reporting requirements, purpose-built church accounting software matters. If you're choosing a system for a church that needs real fund-based reporting, Grain Ledger is one option to consider because it is built around fund accounting from the start, with transactions and reports organized by fund rather than patched in afterward.

What to aim for each month

A church report is doing its job when a board member can quickly answer questions like these:

- General ministry capacity. How is the operating fund performing?

- Restricted accountability. What balances remain in designated funds?

- Cash awareness. Is there enough liquidity for upcoming obligations?

- Variance insight. What changed from expectation, and why?

- Decision readiness. Does the board have enough context to act without guessing?

That's the true structure of a financial report in church life. Not just statement names, but a sequence and format that turn accounting records into stewardship insight.

Related church budgeting resources

Use these resources together when moving from a spreadsheet budget to cleaner monthly church financial reporting.

- Free church budget generator - build a custom Excel budget template for your church

- Church budget template Excel guide - download and adapt a practical budget template

- Nonprofit budget examples - compare operating, program, and restricted-fund budget formats

- Grain Ledger budgeting - connect budgets to fund accounting and monthly reports

Your Next Steps Toward Transparent Stewardship

Most churches don't need a complete reporting overhaul in one week. They need a few honest improvements made consistently.

Start by taking your latest board packet and reading it as if you were brand new. Don't ask, “Is this technically accurate?” first. Ask, “Can a thoughtful board member understand this without translation?”

A simple three-step checklist

- Check fund visibility. Can you easily see the balance of each major restricted and unrestricted fund? If missions, building, benevolence, or other designated resources are blended into broad totals, your report is hiding key stewardship information.

- Check report order. Does the packet begin with a short summary and then move into the financial statements and explanations? If detail comes before context, readers will misread the numbers.

- Check explanatory notes. When a number changes sharply, does the report explain why? A brief variance note can prevent a lot of confusion and mistrust.

Questions worth asking at your next review

Use these with your treasurer, finance committee, or bookkeeper:

| Question | Why it matters |

|---|---|

| Can we separate general operating results from designated activity at a glance? | It protects decision-making |

| Do our reports distinguish performance from cash movement? | It prevents false confidence or unnecessary alarm |

| Can a board member follow the report without accounting training? | It improves oversight and trust |

Some churches also find it helpful to strengthen the broader admin side of reporting, especially when communication and workflow affect how financial information reaches leaders. If your team is exploring smarter support tools for ministry operations, these AI solutions for religious groups offer a useful starting point for that conversation.

A clear report doesn't merely satisfy a finance committee. It helps a church lead with integrity. It shows that gifts are handled carefully, restrictions are respected, and decisions are grounded in reality rather than assumptions.

That kind of clarity builds trust over time.

If your church wants financial reports that reflect real fund accounting instead of spreadsheet workarounds, take a look at Grain. It's built for churches that need clear, fund-based reporting for pastors, boards, and congregations.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.