What Is a Cash Flow Statement: Guide for Churches 2026

Learn what is a cash flow statement and why it's vital for church stewardship. Our 2026 guide explains its 3 sections, fund accounting, and restricted gifts.

A lot of church finance meetings start the same way. Someone looks at the bank balance, someone else looks at the budget report, and then the room gets quiet when a ministry opportunity comes up. The question isn't whether the church has money in some general sense. The question is whether the church has available cash, at the right time, for the right purpose.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

That's where people often ask, what is a cash flow statement, and why does it matter if we already have an income statement and a balance sheet?

I'd explain it the way I would to a new finance committee member. The cash flow statement tells you where cash came from, where it went, and what cash is left at the end of the period. For churches, that matters because ministry decisions aren't made from accounting profit alone. They're made from cash on hand, donor intent, timing, and stewardship.

Why Your Church Balance Sheet Is Only Half the Story

A church can look healthy on paper and still hesitate over a new ministry launch. Maybe the balance sheet shows a solid cash balance. Maybe giving was steady. Maybe the income statement even shows a surplus. Yet the pastor asks whether the church can move forward on a youth ministry renovation, and no one wants to answer too quickly.

That hesitation is wise.

A balance sheet shows what the church owns and owes at a point in time. That's useful, but it doesn't tell the whole story of liquidity. If a large share of cash came from designated gifts for the building fund, that money may not be available for children's ministry, payroll, or routine facility needs. The number in the bank account is real, but not every dollar is equally spendable.

Why this report carries weight

The cash flow statement isn't a side report accountants made up to keep us busy. It is one of the three mandatory financial statements required by US GAAP and IFRS, a standard established in 1987. In the SEC's 2020 fiscal year, approximately 40% of its 1,240 accounting-related comment letters addressed cash flow statement inconsistencies, which shows how seriously regulators treat this report for transparency and compliance, as noted in this verified summary of SEC-related reporting requirements.

For a church leader, the compliance point isn't the main lesson. The ministry lesson is this. Cash flow reporting exists because people need to know whether an organization can meet real obligations with real cash.

Practical rule: A healthy bank balance answers only one question. A cash flow statement answers the harder question, which is whether the church's cash position is sustainable and usable.

Why the balance sheet and income statement can mislead

The income statement tracks revenue and expense activity over a period. The balance sheet shows position at the end of a period. Neither one, by itself, explains the movement of cash.

A church can report contribution income before cash is fully received. It can also record non-cash expenses such as depreciation that reduce reported results without reducing the bank account. That's why leaders sometimes feel confused when the reports seem respectable but the checking account feels tight.

Here are common ministry examples:

- Pledge timing: A donor commitment may support the budget on paper before cash arrives.

- Large prepaid costs: Insurance or curriculum purchases can pressure cash early in the year even if the budget spreads the expense.

- Restricted gifts: Cash may sit in the bank but belong to missions, benevolence, or a building project.

The cash flow statement helps a committee move from “we think we're fine” to “we know what's happening.”

When a finance committee understands cash flow, it asks better questions before approving ministry plans, staff additions, or facility projects.

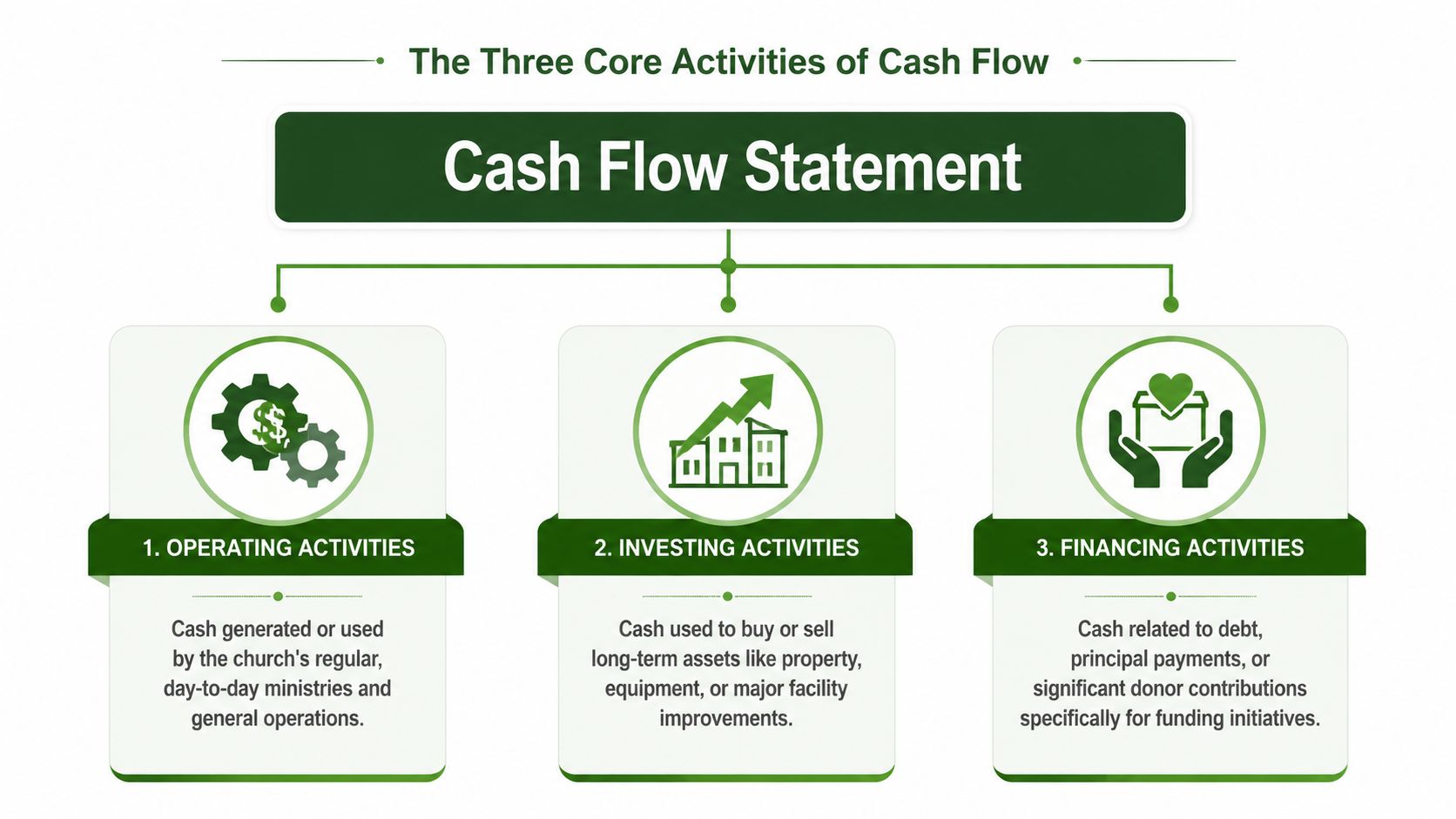

The Three Core Activities of Cash Flow

The cash flow statement sorts all cash movement into three buckets. Once you learn those buckets, the report gets much easier to read. Think of it as following offerings from the plate to the purpose.

A clear overview helps before we get practical:

| Activity | What it means for a church | Typical examples |

|---|---|---|

| Operating | Day-to-day ministry and administration cash | Offerings received, payroll, utilities, ministry supplies |

| Investing | Buying or selling long-term assets | Sound system purchase, van sale, facility improvements |

| Financing | Borrowing, debt repayment, and funding structure | Mortgage proceeds, principal payments, major capital gifts tied to financing decisions |

A cash flow statement reconciles net income to actual cash by separating operating, investing, and financing cash flows. Under the indirect method, which most organizations use, cash flow from operations starts with net income and adjusts for non-cash items like depreciation and for working capital changes, as explained by Wall Street Prep's guide to the cash flow statement.

Operating activities

This is the section most church leaders should watch first. It shows whether routine ministry is generating enough cash to support routine ministry.

For a church, operating cash inflows often include tithes, offerings, undesignated gifts, and other cash received for normal operations. Operating cash outflows often include pastoral salaries, ministry staff wages, utilities, curriculum, benevolence paid from the operating fund, office costs, and regular facility maintenance.

If I were training a new treasurer, I'd say this is the “lights on and ministry happening” section.

Examples include:

- Weekly giving received: Cash deposited from regular offerings belongs here when it supports ordinary operations.

- Payroll and benefits paid: Staff compensation is a normal operating outflow.

- Utility and insurance payments: These keep ministry functioning week by week.

A church can survive a season without buying equipment. It can't thrive long if operating cash never covers ordinary ministry demands.

Here's a short explainer if you want a visual walkthrough before reading more.

Investing activities

This section covers cash used to buy or sell long-term assets. In church life, that usually means property, equipment, major technology, or large facility improvements.

If the church buys a new computer system for the worship team, replaces HVAC equipment, renovates classrooms, or purchases land, those cash payments usually show up here. If the church sells an older van or disposes of equipment and receives cash, that inflow appears here too.

Negative cash flow in investing isn't automatically bad. It may mean the church is investing in ministry capacity. A classroom renovation can reduce cash today while strengthening ministry tomorrow.

Financing activities

This section deals with the way the church raises or repays longer-term funding. For churches, the most familiar item is loan activity.

If the church takes out a mortgage for a building expansion, the loan proceeds belong in financing. If the church pays down loan principal, that outflow belongs here. This section helps leaders see whether cash is being supported by debt, debt reduction, or other funding decisions.

One point trips people up. A payment to the lender may include both interest and principal, but those pieces can land in different places depending on reporting treatment. That's one reason careful bookkeeping matters.

A simple sorting test

When you aren't sure where an item belongs, ask three questions:

- Did this cash come from regular ministry activity? If yes, think operating.

- Did this cash involve a long-term asset? If yes, think investing.

- Did this cash involve borrowing or repaying principal? If yes, think financing.

That habit makes the report far less intimidating.

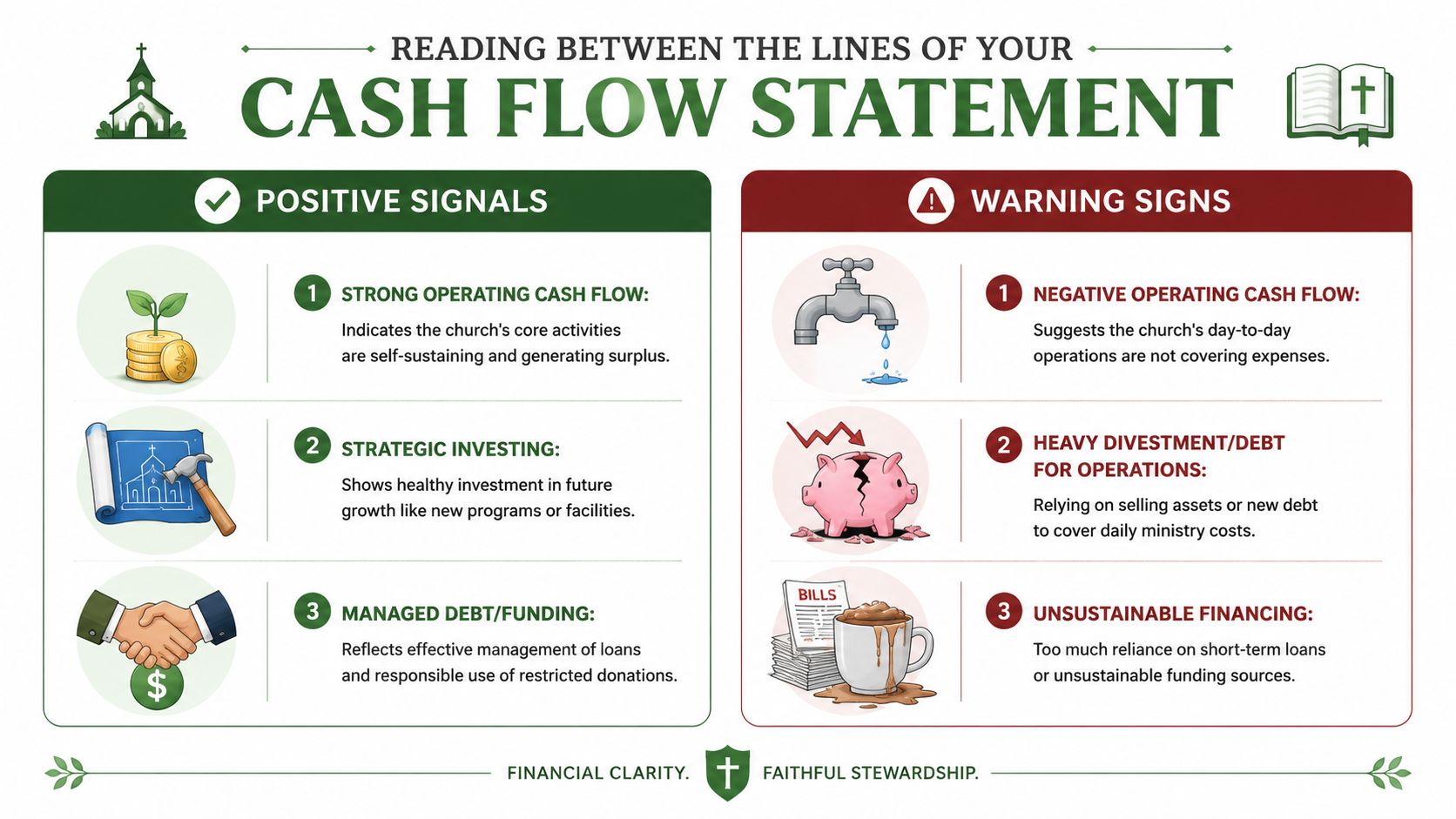

Reading Between the Lines of Your Cash Flow Statement

Once you know the three sections, the next step is reading the story they tell together. A cash flow statement isn't just a list of categories. It's a diagnostic report.

A good first question is simple. Is operating cash flow generally positive and steady relative to the church's ministry needs? Harvard Business School notes that the statement shows how much cash different activities generate, and that positive cash flow means more money came in than went out over the period, in its overview of how to read a cash flow statement.

Positive signals and warning signs

Here's how I'd interpret common patterns in a church setting:

- Healthy operations: Regular giving and other operating inflows are covering payroll, ministry expenses, and routine bills.

- Strategic investment: Investing cash flow is negative because the church bought equipment or improved facilities for future ministry use.

- Managed financing: Debt is being repaid in an orderly way, and financing activity supports long-term plans instead of patching daily shortages.

Warning signs look different:

- Operating weakness: The church keeps spending more cash on normal operations than it receives for those same operations.

- Asset sales covering ministry bills: The church sells equipment or property to support normal monthly expenses.

- Borrowing for routine needs: New debt or emergency financing keeps the lights on because ministry operations aren't self-supporting.

Strong ministry momentum on the calendar doesn't always mean strong cash generation in the operating section.

Why surplus and cash can move in different directions

Many readers find this aspect confusing. A church can show a surplus on the income statement and still feel short on cash. The reason usually sits in the bridge items between accrual reporting and real cash movement.

The SEC-focused educational material on cash flow reporting notes that the diagnostic value is not merely “profit versus cash,” but the bridge items that explain the difference, such as receivables, payables, and non-cash expenses, in this SEC educational resource on the statement of cash flows.

For churches, those bridge items often look like this:

| Bridge item | What it can mean in church life |

|---|---|

| Accounts receivable or pledged gifts | Revenue may be recorded before cash is collected |

| Accounts payable | The church may delay cash payments, which helps short-term cash but creates future pressure |

| Non-cash expenses | Depreciation affects reported results but doesn't reduce the bank balance |

| Deferred or pre-collected amounts | Cash may arrive now while the related activity spans future periods |

If a church reports healthy giving but has rising unpaid obligations, operating cash can still be strained. If a church records depreciation expense, reported results may look tighter than bank cash. The details matter.

Committee question: “What bridge items explain the gap between our reported surplus and our actual cash movement this month?”

That one question improves almost every finance meeting.

Special Cash Flow Considerations for Church Finances

Most general explanations of what is a cash flow statement assume a business with one main pool of money. Churches rarely work that way. Churches manage funds, and those funds often carry donor restrictions, board designations, or ministry-specific purposes.

That changes the conversation.

A church may have cash in the bank and still be unable to spend much of it on general operations. A building fund balance can't become payroll support just because the checking account is low. A missions gift can't be reassigned to air conditioning repairs because the month got tight. The bank sees one deposit account. Stewardship sees multiple obligations.

Why total cash can create a false sense of security

This is the point many standard cash flow guides skip. For churches and other fund-based organizations, the practical question isn't only “how much cash do we have?” It's “how much of that cash is available for general ministry right now?”

Fidelity's educational material points out that fund-level and restricted-cash interpretation is an underserved issue for nonprofits and churches, and that restrictions and designated gifts create a materially different decision-making problem than generic small-business examples, as described in Fidelity's explanation of cash flow statements.

In ministry practice, that means leaders should regularly separate:

- General fund cash: Money available for ordinary ministry operations.

- Restricted cash: Money that must be used for a donor-defined purpose.

- Internally designated amounts: Money the board has set aside for a future use.

- Project-specific reserves: Cash held for capital campaigns, missions, benevolence, or special events.

Timing matters more than many committees expect

Churches also deal with uneven giving patterns. Some months are strong. Others aren't. Year-end generosity can make one month look full while the next quarter feels lean.

Pledges and intentions add another layer. A donor may promise support for a project, but the ministry team can't pay a contractor with a promise. The cash flow statement brings discipline to that distinction. It asks what arrived, when it arrived, and where it is meant to go.

That's why church cash review should include both organization-wide cash flow and fund-level availability. Without both views, leaders may approve ministry plans based on cash that is real in the bank but unavailable in practice.

Restricted cash is still cash. It just isn't flexible cash.

Reconciling Your Church Cash Flow Statement

A cash flow statement becomes useful when it ties back cleanly to the bank and to the balance sheet. If the ending cash on the statement doesn't match the ending cash in your records, something is missing, misclassified, duplicated, or posted in the wrong period.

For any church using accrual-based reports, this reconciliation step is where confidence is built. It's also where many finance committees gain a better feel for why income and cash don't move in lockstep.

According to the Center for Financial Research and Analysis, companies with positive net income but negative operating cash flow for two consecutive quarters face an 85% probability of defaulting on their debt within 18 months. That finding underscores a basic stewardship lesson. Reported results matter, but cash reality matters more when obligations come due.

A simple church template

Here is a plain-language example using the indirect method. The amounts are intentionally left blank so your church can adapt the format without borrowing numbers that don't fit your situation.

Simplified Church Cash Flow Statement (Indirect Method)

| Item | Amount |

|---|---|

| Net income or change in net assets | [Amount] |

| Depreciation and other non-cash expenses | [Amount] |

| Increase or decrease in receivables or pledged gifts | [Amount] |

| Increase or decrease in prepaid expenses | [Amount] |

| Increase or decrease in accounts payable | [Amount] |

| Net cash from operating activities | [Amount] |

| Purchase of equipment or facility improvements | [Amount] |

| Proceeds from sale of church vehicle or equipment | [Amount] |

| Net cash from investing activities | [Amount] |

| Loan proceeds | [Amount] |

| Mortgage or loan principal payments | [Amount] |

| Net cash from financing activities | [Amount] |

| Net increase or decrease in cash | [Amount] |

| Beginning cash balance | [Amount] |

| Ending cash balance | [Amount] |

A practical reconciliation routine

When I review a church cash flow statement, I walk through it in this order:

- Start with beginning cash: Match it to last period's ending cash.

- Review operating adjustments: Check non-cash items and balance sheet changes like receivables and payables.

- Inspect big investing entries: Tie asset purchases and sales to invoices, bank activity, and fixed asset records.

- Confirm financing items: Separate loan proceeds from principal payments.

- Match ending cash: The final balance should agree with the bank-reconciled cash balance on the balance sheet.

If the statement doesn't reconcile, don't guess. Trace the entries one by one. Churches often find the issue in restricted fund postings, loan principal treatment, or timing differences around month-end deposits and disbursements.

Related church budgeting resources

Use these resources together when moving from a spreadsheet budget to cleaner monthly church financial reporting.

- Free church budget generator - build a custom Excel budget template for your church

- Church budget template Excel guide - download and adapt a practical budget template

- Nonprofit budget examples - compare operating, program, and restricted-fund budget formats

- Grain Ledger budgeting - connect budgets to fund accounting and monthly reports

How Grain Ledger Simplifies Fund-Based Cash Flow

A finance committee meeting can get tense fast when someone asks a simple question. “How much cash do we have available for ministry this month?” The bank balance may look healthy, but part of that money may belong to the building fund, part to missions, and part to benevolence. If your system only shows one combined cash picture, leaders still have to sort out what can be used and what must stay set apart.

That is the daily challenge with church accounting.

Generic accounting software can produce a cash flow statement. Churches often still end up using tags, classes, spreadsheets, and exported reports to answer fund-level questions. The report may be accurate in total, yet still leave the board unclear about which cash is available for general ministry and which cash is restricted for a specific purpose.

Why fund architecture matters

Churches manage stewardship by purpose, not only by totals. A gift for the roof repair fund should stay connected to that purpose from the moment it is received until it is spent. A missions donation should not disappear into a combined cash number that forces the treasurer to rebuild the story later in a spreadsheet.

Grain is designed around native fund architecture instead of add-on workarounds. That means donations, transactions, and reports stay tied to the correct fund from the start, including cash flow reporting by fund.

For church leaders, that changes the conversation. Instead of asking staff to piece together several reports, the finance committee can review cash movement in the same fund structure the church already uses to manage designated gifts and ministry spending.

What that changes for leaders

Fund-based cash flow reporting helps answer the questions church boards ask:

- General ministry cash: How much cash is available for regular operations and upcoming bills?

- Restricted fund activity: What came into the building fund, missions fund, or benevolence fund, and what went out?

- Clearer board reporting: Can leaders read one report without cross-checking multiple spreadsheet tabs?

- Stronger stewardship: Do restricted dollars remain connected to the donor's intent?

It works like labeled offering envelopes. If every gift is clearly marked from the beginning, you do not have to guess later where it belongs.

That clarity matters to different people for different reasons. A pastor wants to make ministry decisions without wondering whether the cash is available. A treasurer wants fewer manual reconciliations. A finance committee wants reports that reflect how the church receives, holds, and spends money across separate funds.

If your church needs clearer fund-level reporting, start free with Grain Ledger to see how purpose-built church accounting can make cash flow, restrictions, and stewardship easier to understand.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.