Budget V Actual

Budget v actual - Master Budget vs. Actual reporting for churches. Learn fund-based variance analysis, report creation, & best practices for clear stewardship

Most church finance questions don't begin with accounting language. They begin with ministry language.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

“Can we afford to move forward with the youth retreat?”

“Why does the building fund feel tight?”

“Are we on track, or are we just hoping we are?”

In many churches, those questions land in a finance committee meeting and then sit there for a moment. Someone opens a spreadsheet. Someone else flips through printed reports. The treasurer knows money came in and bills were paid, but the room still can't see the whole picture clearly.

That's where budget vs actual becomes useful. It gives the church a way to compare what leaders planned with what occurred, then use that difference to guide wise decisions. In a church setting, that matters because money is never just money. Every line on the report connects to people, ministry, trust, and stewardship.

The Sunday Morning Question That Changes Everything

A familiar scene plays out in a lot of churches.

It's after the service. A pastor, a treasurer, and a few finance committee members gather around a table. One person asks whether the missions fund can cover an upcoming commitment. Another wonders why facilities costs feel heavier than expected. Someone else asks if regular giving is keeping pace with the budget. The reports on hand show balances, maybe a list of transactions, but not a clear answer to the true question: how are we doing compared with the plan?

That's the turning point for many churches. They realize they don't just need records. They need comparison.

A check register tells you what happened. A bank balance tells you what's left. But a budget v actual report shows whether ministry spending and giving are tracking with what the church believed was faithful and realistic at the start of the year.

Why confusion lingers without this report

Churches often have good intentions and weak visibility. That creates stress in places where there should be clarity.

- Ministry leaders feel uncertain: They don't know whether they should move ahead, wait, or scale back.

- Finance teams feel reactive: They keep answering urgent questions instead of guiding decisions.

- Boards lose context: They see totals, but they can't always tell whether a change is a problem, a timing issue, or a normal fluctuation.

Practical rule: If your committee can state account balances but can't explain whether you're ahead of plan or behind it, you need a budget vs actual rhythm.

For churches, this isn't about becoming more corporate. It's about becoming more transparent and more faithful. When leaders can connect actual giving and spending to the approved budget, they can answer questions with confidence and make adjustments before small issues become larger ones.

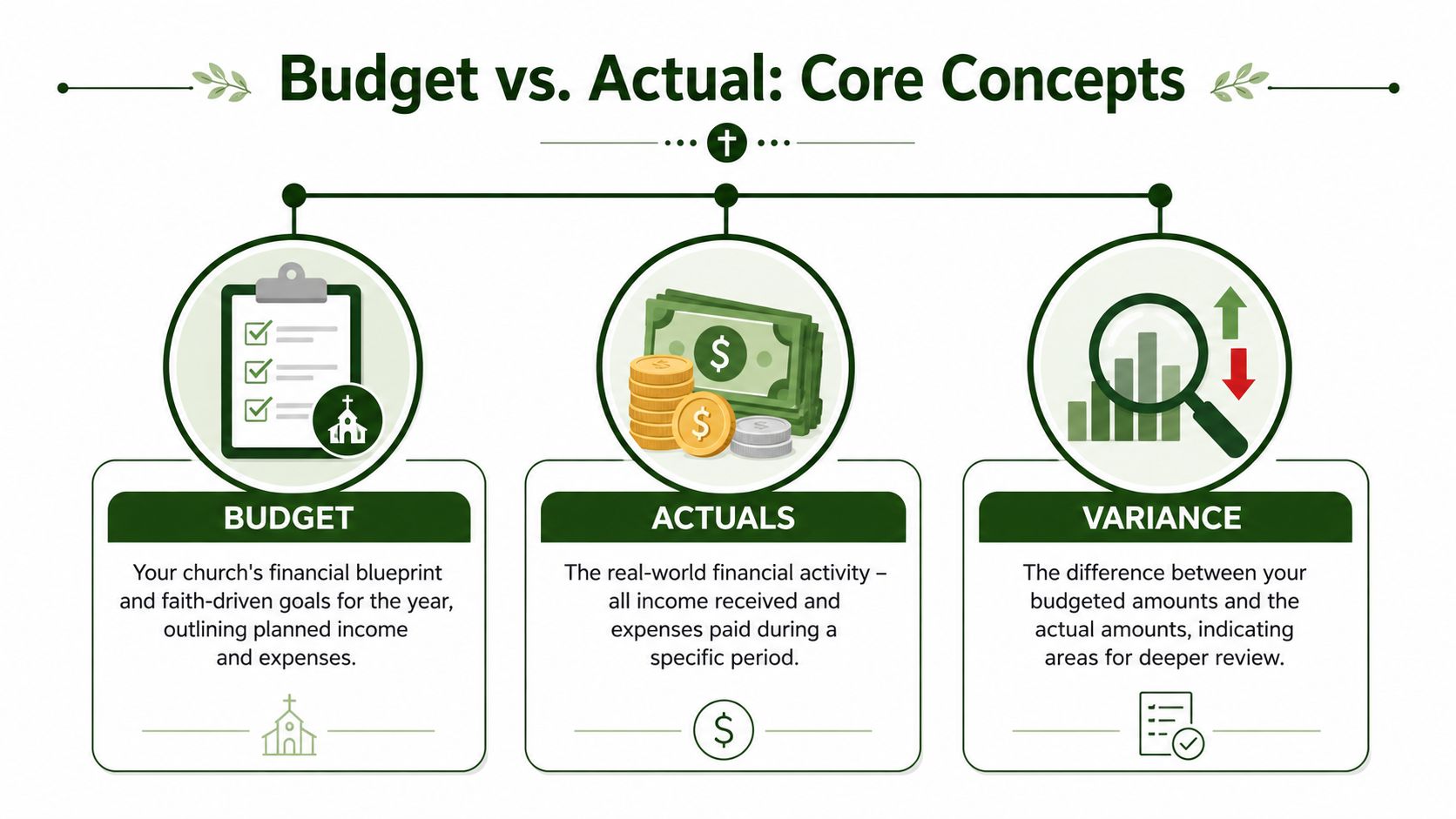

Understanding the Core Concepts of Budget vs Actual

A church budget vs actual report rests on three ideas. Once those are clear, the report becomes much easier to read and much easier to discuss in a finance committee meeting.

Budget, actuals, and variance in plain language

Church budgeting works like a ministry plan with receipts attached.

The budget is the plan the church approved. It reflects what leaders believed giving and spending would look like for the year. The actuals are what was really recorded as the months passed. The variance is the gap between those two numbers.

That sounds simple, but churches add an important layer. They often track more than one pool of money. General operations, missions, building funds, benevolence, and designated gifts may each need their own line of sight. A church can appear healthy in total while one fund is under pressure or one ministry area is spending faster than expected. That is why a clear structure for fund accounting for churches matters when you review budget vs actual results.

A helpful way to explain this to a new committee member is to compare it to household envelopes. If a family sets aside money for groceries, rent, and school expenses, they would not judge the whole month by looking at one big pile of cash. They would ask whether each purpose is staying on track. Church funds work much the same way.

The formulas behind the report

Most reports show variance in two ways.

Variance ($) = Actual - Budget

Variance (%) = (Actual - Budget) / Budget

Those formulas are widely used in budget reporting, as explained in Tipalti's budget versus actual overview. The dollar amount shows the size of the gap. The percentage helps you compare line items of very different sizes.

For example, if the church budgeted $100,000 for an expense category and the actual amount came in at $106,000, the variance is $6,000. On a percentage basis, that is 6% over budget.

The next question is where confusion usually starts. Is that variance good or bad?

The answer depends on whether you are looking at income or expense.

| Line item | What happened | What it usually means |

|---|---|---|

| Expense | Actual is higher than budget | Usually unfavorable |

| Expense | Actual is lower than budget | Usually favorable |

| Income | Actual is higher than budget | Usually favorable |

| Income | Actual is lower than budget | Usually unfavorable |

That distinction matters in church settings because the same positive number can point to two very different stories. Higher-than-budget giving may show stronger support than expected. Higher-than-budget facility costs may mean a repair, seasonal utility pressure, or spending that needs review.

If a committee member is still unsure, that is normal. Variance analysis often feels harder than it is because the sign on the number does not explain the meaning by itself. These MyOfficeOps budgeting insights offer a clear explanation in plain language.

A variance is a signal to investigate, not a verdict by itself.

Why This Report Is Critical for Church Stewardship

A church can produce clean books and still miss the larger stewardship question.

Stewardship asks whether leaders are handling resources in a way that is faithful, transparent, and aligned with the church's mission. A budget v actual report helps answer that because it compares approved intent with actual activity. That comparison gives pastors, treasurers, elders, and ministry leaders a shared reference point.

It strengthens accountability

When a church adopts a budget, it is saying, “This is how we believe resources should be used this year.” The actual results then show whether spending and giving followed that plan.

Budget vs actual reporting is a standard control mechanism because it helps identify both forecasting errors and accounting mistakes. Practitioners commonly recommend reviewing results monthly and watching for large variances, recurring losses, and increasing losses over successive periods, as described in Qubit Capital's overview of budget vs actual reporting.

That monthly habit matters in church life. It helps the committee catch a coding mistake before it sits for half a year. It helps leaders notice when a department is repeatedly spending ahead of plan. It also keeps everyone from relying on memory or impressions.

It protects trust around designated money

Churches often receive gifts for specific purposes. People give to missions, benevolence, facilities, student ministry, or a building effort because they trust the church to handle those funds carefully.

A budget vs actual report supports that trust by showing whether those ministry areas are operating within plan and whether leaders can explain differences clearly. That kind of visibility is hard to create if all activity is blended together in one broad report.

Financial clarity protects more than cash. It protects congregational trust.

It helps leaders act earlier

Without comparison, churches often make decisions after pressure builds. By then, the room is dealing with urgency instead of discernment.

A recurring review gives leaders time to ask wiser questions:

- Should we pause a discretionary purchase?

- Was this expense seasonal, or is it becoming a pattern?

- Can we move ahead with a ministry opportunity, or should we wait for stronger giving?

The point isn't to make the church cautious about ministry. It's to make ministry decisions informed. When leaders know where the church stands against budget, they can say yes, no, or not yet with more confidence and less guesswork.

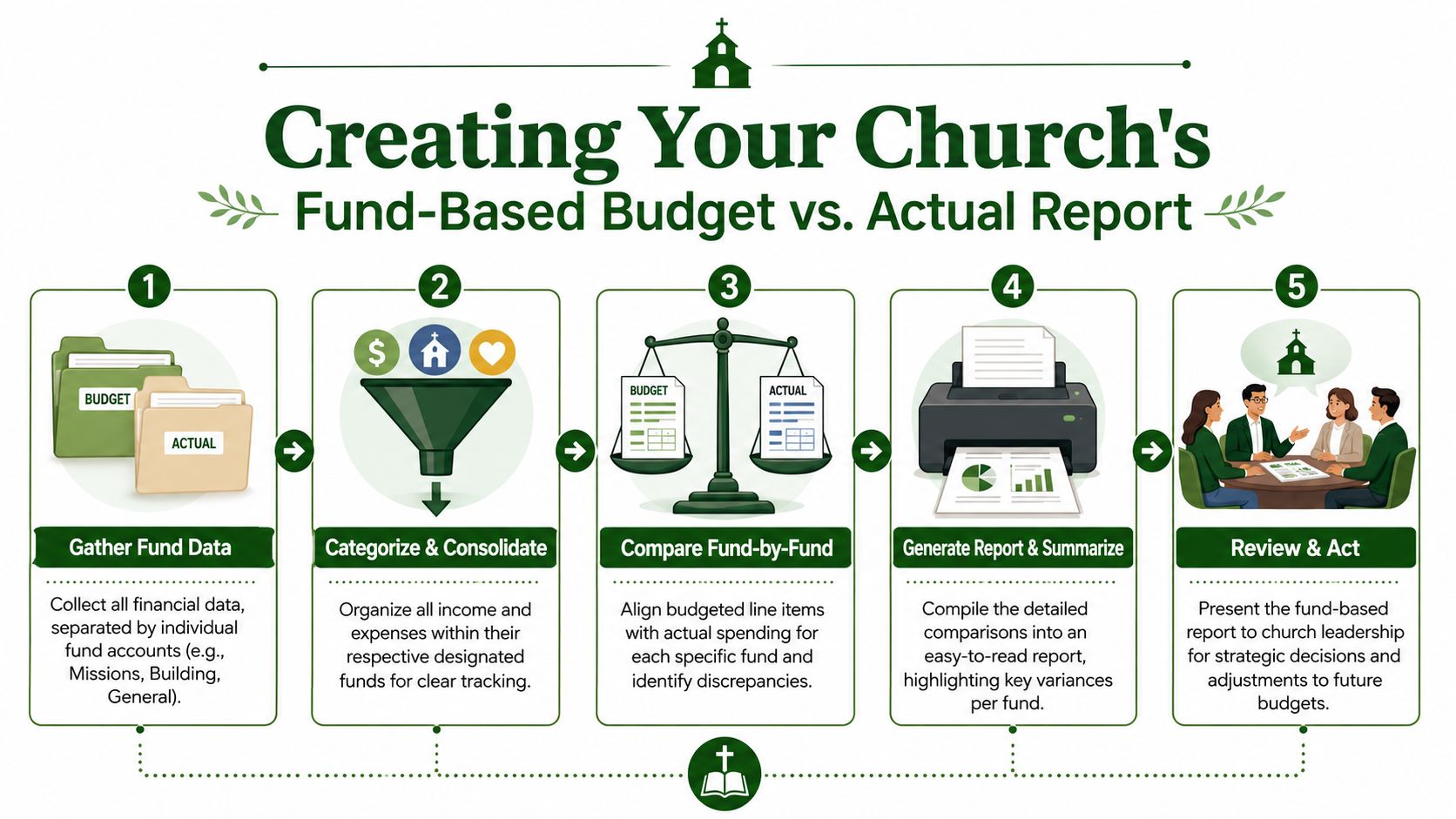

How to Prepare Your Fund-Based Budget vs Actual Report

Churches often stumble here because they try to build the report from the top down. The easier path is to build it from the fund level up.

Start with funds, not just departments

A church usually doesn't operate as one undifferentiated pot of money. It manages resources by purpose. That may include a general fund, missions fund, building fund, benevolence fund, or ministry-specific balances.

Your budget should reflect that structure. If the budget is only one long expense list without fund context, your eventual report will leave key questions unanswered.

A healthy setup usually includes:

- A budget for each fund that has meaningful ongoing activity.

- Consistent account categories so actual transactions map cleanly to the budget.

- Clear ownership so ministry leaders understand which lines they influence.

If your reporting still feels fragmented, this guide to a church financial report can help you think through how fund-level reporting fits into the church's broader reporting package.

Gather actuals with clean coding

Once the budget is set, the actual side of the report depends on disciplined bookkeeping. Every deposit, bill, reimbursement, and journal entry needs to be coded to the right fund and account.

Many churches run into trouble with their budget and actuals. The budget may be clean, but the actuals are messy because:

- Restricted gifts were posted too broadly

- Shared expenses were coded inconsistently

- Different staff members used different categories

- Timing differences weren't documented clearly

The result is a report that looks precise but doesn't answer the committee's real questions.

Here's a practical walkthrough to reinforce the process:

Build a simple monthly workflow

Most churches don't need a complicated reporting ritual. They need a repeatable one.

- Close the month: Make sure donations, bills, payroll, and bank activity are recorded.

- Map actuals to budget lines: Confirm each transaction sits in the correct fund and account.

- Review variances: Look for items that are notably off plan or repeatedly drifting.

- Add brief notes: A short explanation is often more helpful than another spreadsheet tab.

- Bring it to the right people: The treasurer, finance committee, pastor, and ministry leaders may each need a different level of detail.

Working habit: The report should be ready soon enough after month-end that leaders can still do something with it.

Use tools that fit church accounting

Spreadsheets can work for a while, especially in a smaller church with a careful treasurer. But as funds multiply and transactions flow in from banks, cards, and giving platforms, manual work creates risk.

Churches that want software built around fund-based reporting should consider options designed for church accounting rather than adapting generic business tools. Grain Ledger is one such option. It is built for true fund-based accounting, organizes transactions around funds from the start, and connects giving, banking, and accounting so churches can produce fund-level reports with less manual reconciliation.

The goal isn't automation for its own sake. It's giving the finance team enough time to interpret the report, not just assemble it.

Interpreting the Report to Make Better Decisions

A report becomes useful when the room stops asking “what changed?” and starts asking “why did it change?”

That distinction matters because variance by itself can mislead. A line that looks favorable may hide a ministry slowdown. A line that looks unfavorable may reflect timing.

A frequently underexplained angle in budget review is that variance alone can be misleading without context from the driver behind the numbers. In churches, that means asking questions like: did giving miss budget because attendance fell, because average gift size changed, or because receipts were delayed? Driver-based analysis is more useful for management decisions, as noted in NStar Finance's guide to budget vs actual analysis.

A sample church report

Below is a simple teaching example. The point isn't the exact layout. The point is how to read it.

| Account/Fund | Budget | Actual | Variance ($) | Variance (%) | Notes |

|---|---|---|---|---|---|

| General Fund Giving | Above-planned expectation set in budget | Lower than planned receipts for the month | Unfavorable | Unfavorable | Could be lower attendance, smaller gifts, or timing |

| Missions Fund Income | On-plan monthly target | Ahead of monthly target | Favorable | Favorable | May reflect a special emphasis or delayed prior-month receipts |

| Facilities Expense | Planned routine costs | Higher than expected | Unfavorable | Unfavorable | Check utility bills, repairs, or posting errors |

| Youth Ministry Expense | Approved monthly ministry spending | Lower than planned | Favorable | Favorable | Could mean delayed event spending, not true savings |

| Benevolence Fund | Planned support level | Near plan | Minimal variance | Minimal variance | Likely no action needed |

If you're teaching committee members how to read this, pair it with a simple explanation of nonprofit-style operating statements. This overview of P&L for non-profit organizations can help newer readers connect the report structure to familiar income-and-expense logic.

Ask diagnostic questions, not just accounting questions

Once a variance appears, the next step is diagnosis. Churches usually make better decisions when they sort variances into one of three buckets.

Timing issue

Money or expenses landed in a different month than expected.

Examples include a donation posted after month-end, an annual insurance bill paid earlier than planned, or an event expense booked before related registrations came in.

True performance issue

The church is operating differently than planned.

Maybe regular giving is consistently soft. Maybe facilities costs are staying high. Maybe a ministry area isn't using the resources it requested.

Planning issue

The original budget may not have reflected reality well.

A committee may have underestimated a recurring cost or expected a giving pattern that now looks too optimistic.

When you read a variance, don't stop at the math. Ask what behavior, event, or assumption sits behind it.

Connect dollars to ministry drivers

Church leadership gains the most value here.

If giving is behind budget, the committee shouldn't jump straight to concern or blame. It should ask what operational driver changed. Was attendance lower? Were several larger gifts delayed? Was there a seasonal dip? Did online giving post later than expected?

If youth ministry spending is below budget, that might sound positive. But if it happened because an outreach event was cancelled, then the financial result tells only part of the story.

A strong budget v actual review turns financial lines into ministry conversations. It helps leaders understand not just whether a number changed, but what that change means for people and programs.

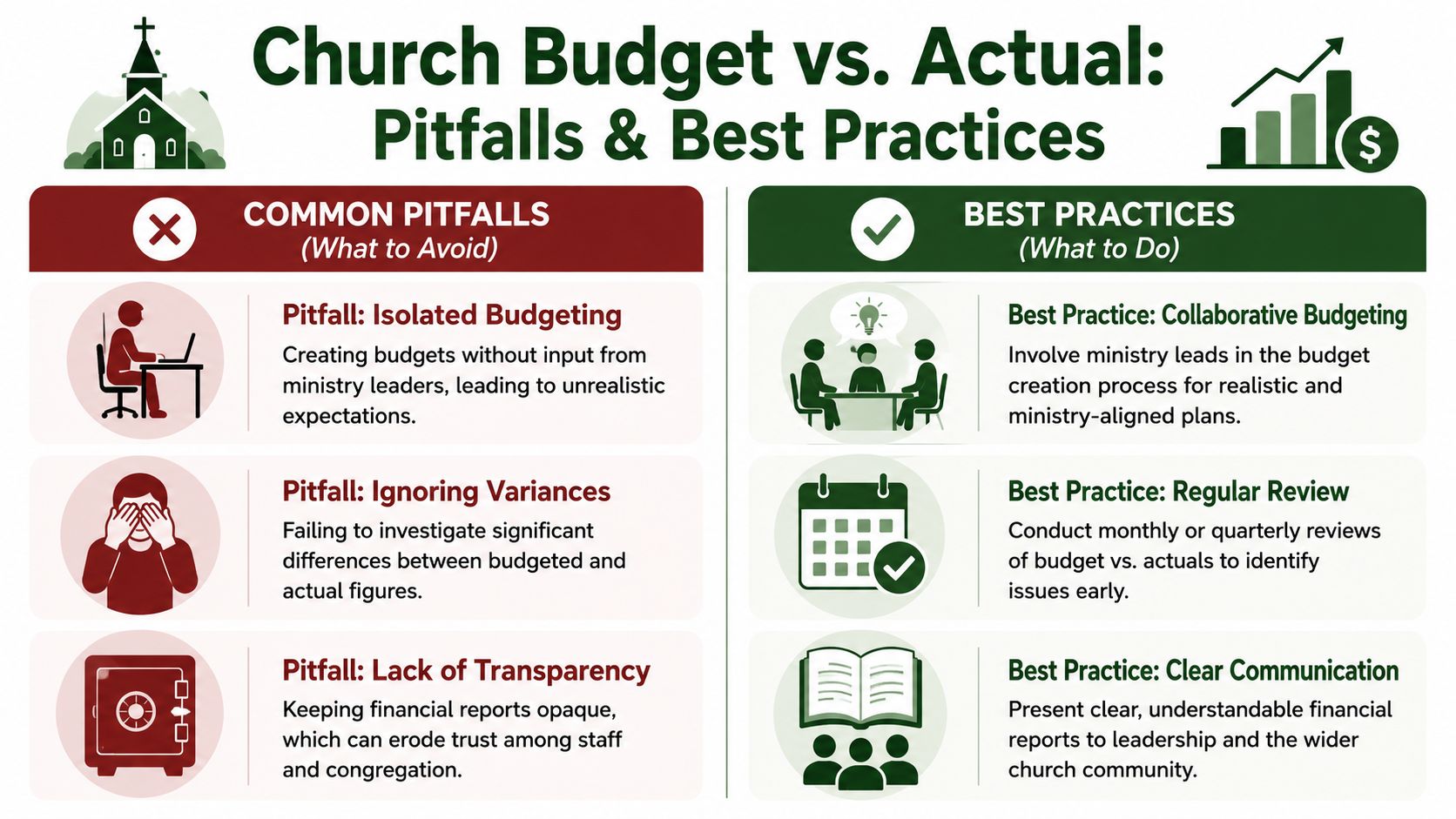

Common Pitfalls and Best Practices for Churches

Churches often struggle with budget vs actual reporting for ordinary reasons, not dramatic ones. The report gets built too late. The categories don't match. Leaders mix restricted and general activity. Small variances get ignored until they become recurring patterns.

Pitfalls that create confusion

Some issues show up again and again in church finance meetings.

- Budgeting in isolation: The treasurer builds the whole budget without ministry input, so expectations don't match real ministry plans.

- Blended reporting: Restricted and unrestricted activity are mixed together, making fund-level stewardship harder to see.

- Ignoring “small” differences: A modest recurring variance can matter more than one unusual month.

- Weak explanation: Leaders hand out reports full of numbers but without notes that explain what changed.

These problems don't always look serious at first. But over time they create uncertainty, and uncertainty makes wise stewardship harder.

Practices that keep the report useful

A better approach is often less flashy and more disciplined.

| Common pitfall | Better practice |

|---|---|

| Budget built by one person | Involve pastors and ministry leaders in planning |

| Actuals coded inconsistently | Use a consistent fund and account structure |

| Variance review happens rarely | Review on a regular schedule and note trends |

| Budget keeps changing | Keep the budget as the baseline and update the forecast separately |

One issue deserves special attention. Churches often wonder whether they should revise the budget midyear when conditions change. Best practice is to keep the original budget as the accountability standard while using a rolling forecast as the current best estimate of what will happen next, as explained in Martuus Solutions' discussion of budget, forecast, and actual.

That distinction matters. If the church rewrites the budget every time reality changes, leaders lose the baseline they need for accountability. If they never update their expectations at all, they may miss risks or opportunities that deserve action.

Keep one number for accountability and another for planning. Mixing those two purposes creates confusion.

A practical checklist for the committee

Before each review meeting, it helps to ask:

- Are the funds separated correctly?

- Do the actuals match the same categories used in the budget?

- Which variances need explanation because they are recurring or meaningful?

- Do ministry leaders understand the story behind their numbers?

- Are we comparing against the approved budget, a forecast, or both?

That simple discipline keeps the room focused on decisions instead of debate about the report itself.

Related church budgeting resources

Use these resources together when moving from a spreadsheet budget to cleaner monthly church financial reporting.

- Free church budget generator - build a custom Excel budget template for your church

- Church budget template Excel guide - download and adapt a practical budget template

- Nonprofit budget examples - compare operating, program, and restricted-fund budget formats

- Grain Ledger budgeting - connect budgets to fund accounting and monthly reports

Transforming Financial Data Into Ministry Action with Grain

Good church finance work follows a steady rhythm. Leaders plan. They record what happened. They compare actual activity to the plan. They ask why. Then they act.

That cycle is what makes budget v actual so valuable in a church. It doesn't just measure financial performance. It helps the church practice stewardship with clarity. A report can reveal whether a ministry area is ready to expand, whether a fund needs attention, or whether a concern is only temporary and doesn't require a rushed response.

It also helps the church communicate more clearly. When pastors, finance teams, and boards can explain the difference between planned and actual results in plain language, the conversation changes. Reports become easier to trust because they are easier to understand.

The same principle applies beyond finance. Churches that evaluate ministry operations clearly, whether in budgeting or digital outreach, usually make stronger decisions over time. For example, teams thinking through online ministry can benefit from a practical resource like this 2026 church live streaming guide, because the same stewardship mindset applies there too. Know the purpose, track the activity, and review what is happening.

A church accounting system should support that rhythm, not fight it. The right setup reduces manual work, keeps funds organized properly, and gives leaders reports they can use without translation. That frees the treasurer and committee to spend less time assembling numbers and more time serving the mission those numbers represent.

If your church wants fund-based reporting that aligns budgeting, giving, banking, and stewardship, take a look at Grain. It's built for churches that need clear budget vs actual visibility by fund and want reporting that speaks the language of ministry, not just bookkeeping.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.