Church Accounting Regulations A Practical Guide

A complete guide to church accounting regulations. Learn about 501(c)(3) status, fund accounting, payroll, UBIT, and internal controls to ensure compliance.

A lot of church treasurers get handed the role the same way they get handed the coffee keys, the online giving login, and a stack of unanswered questions. One week you're helping with ministry operations. The next week you're trying to figure out whether the pastor's pay belongs in payroll, whether the building fund can cover a sound-system invoice, and why the bank balance doesn't match the giving report.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

That moment is common, and it doesn't mean you're behind. It means you've discovered what many churches learn late. Church accounting regulations are not just small-business bookkeeping with a cross on the sign. They sit inside nonprofit law, tax rules, donor restrictions, payroll rules, and reporting expectations that are specific to churches.

The encouraging part is that this work is ministry too. Clean books protect the church. Accurate payroll protects staff. Proper handling of designated gifts protects donor trust. Good records protect the board when hard questions come up later.

In the United States, church accounting rules are anchored in nonprofit tax law. Churches generally qualify as 501(c)(3) organizations, are usually exempt from filing annual Form 990 information returns, but still have to manage payroll reporting such as Form W-2 and often Form 941. Ministers also fall under special compensation rules and commonly pay 15.3% SECA tax instead of having FICA withheld, as explained in Aplos on church accounting best practices.

From Calling to Compliance An Introduction

If you're newly responsible for church finances, the first thing to know is that confusion at the beginning is normal. Most churches don't have a full finance department. They have a pastor, a volunteer bookkeeper, a board member who understands spreadsheets, and a treasurer trying to keep everyone informed without creating panic.

That's why church accounting regulations matter so much. They create boundaries around money that was given for ministry. Those boundaries aren't there to slow the church down. They're there so the church can operate with integrity when people give, when staff are paid, and when leaders make decisions.

What new treasurers usually discover first

The first surprise is usually this. The checking account may look simple, but the obligations behind it are not.

A single month can involve:

- Payroll reporting: Wages still have to be reported correctly for employees.

- Minister compensation questions: Clergy treatment doesn't work like ordinary payroll.

- Designated giving: Money for missions, benevolence, or building work can't be treated like general cash.

- Board visibility: Leaders need reports they can understand and rely on.

Practical rule: If a transaction would be hard to explain to the board, the donor, or an auditor later, slow down and document it now.

Why this is stewardship, not paperwork

Churches talk often about stewardship from the pulpit. The finance office has to practice it in the ledger. That means recording gifts accurately, keeping support for decisions, and making sure the church's reporting matches what happened.

The healthiest churches I've seen don't treat compliance as a side task. They treat it as part of ministry credibility. When records are clear, difficult conversations get easier. When records are messy, even innocent mistakes can look suspicious.

A new treasurer doesn't need to know every rule on day one. You do need a framework. Start with the church's tax-exempt status, then payroll and clergy treatment, then donor-restricted funds, then internal controls and reporting. Once those pieces are in place, the work becomes far less intimidating.

Understanding Your Churchs 501c3 Status

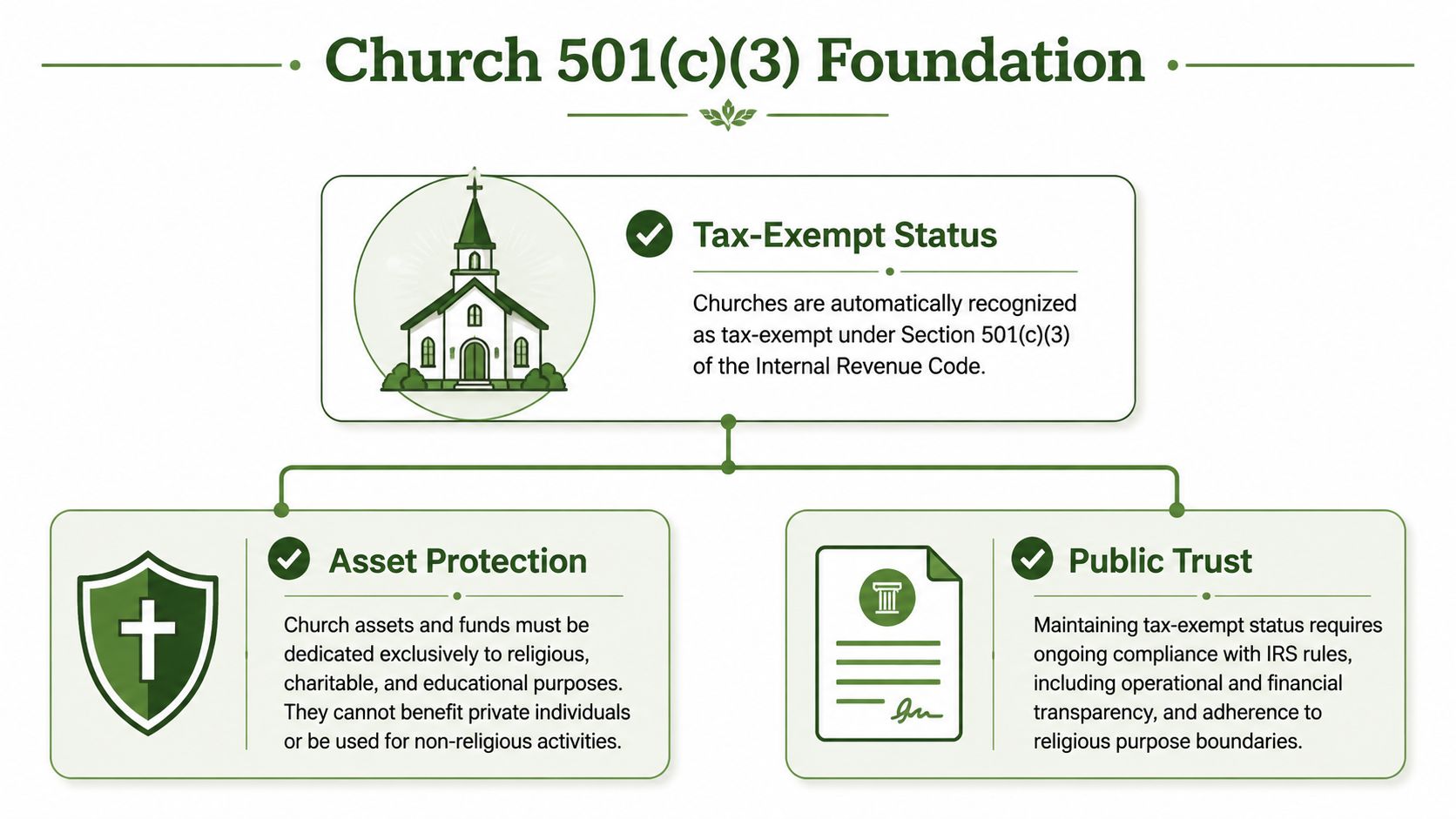

Most churches operate as tax-exempt organizations under 501(c)(3). In practice, that means the church exists for exempt religious purposes and has to handle its money in a way that fits that purpose. The church may not look like a charity office, but legally and financially it lives inside that world.

What the status gives you

The tax-exempt structure gives a church room to focus on ministry rather than ordinary income taxation. It also signals to donors, banks, and grantmakers that the church operates within a recognized nonprofit framework.

But that benefit comes with guardrails. Church assets must support the church's religious mission. Leaders can be paid for real work, but church resources can't be used to improperly enrich insiders.

What the status requires from leaders

Newly appointed treasurers need clarity on this matter. Tax-exempt status is not just a label. It shapes everyday decisions.

A practical way to think about it is this table:

| Area | What works | What creates risk |

|---|---|---|

| Compensation | Board-approved, documented, ministry-related pay | Informal perks, undocumented benefits, insider favoritism |

| Political activity | Teaching on issues in a ministry context | Campaign intervention or candidate endorsement activity |

| Church spending | Spending tied to church purpose | Personal use of church funds without clear authorization |

| Governance | Minutes, approvals, clear policies | Handshake decisions with no paper trail |

One of the biggest points of confusion is Form 990. Churches are generally exempt from filing Form 990, 990-EZ, or 990-N. That exemption is real, but many leaders draw the wrong conclusion from it. They assume less filing means less accountability. It doesn't.

Why the Form 990 exemption gets misunderstood

The exemption removes one filing burden that many nonprofits carry. It does not remove the need for accurate records, board oversight, or careful use of funds.

Some churches still choose to file voluntarily in special situations, such as when a third party wants more formal transparency. But whether your church files or not, the practical expectation remains the same. Keep records that show the church is operating for exempt purposes and handling money responsibly.

Public trust is one of the church's most valuable financial assets. Once people start doubting whether gifts are handled properly, recovery is hard.

If you're a treasurer, your job isn't to become a tax attorney. Your job is to make sure daily operations stay inside these boundaries. When compensation is approved, document it. When the board makes a sensitive decision, minute it. When the church pays for something unusual, ask whether it clearly supports the church's mission.

That kind of discipline protects both the ministry and the people leading it.

Navigating Payroll Taxes and Clergy Compensation

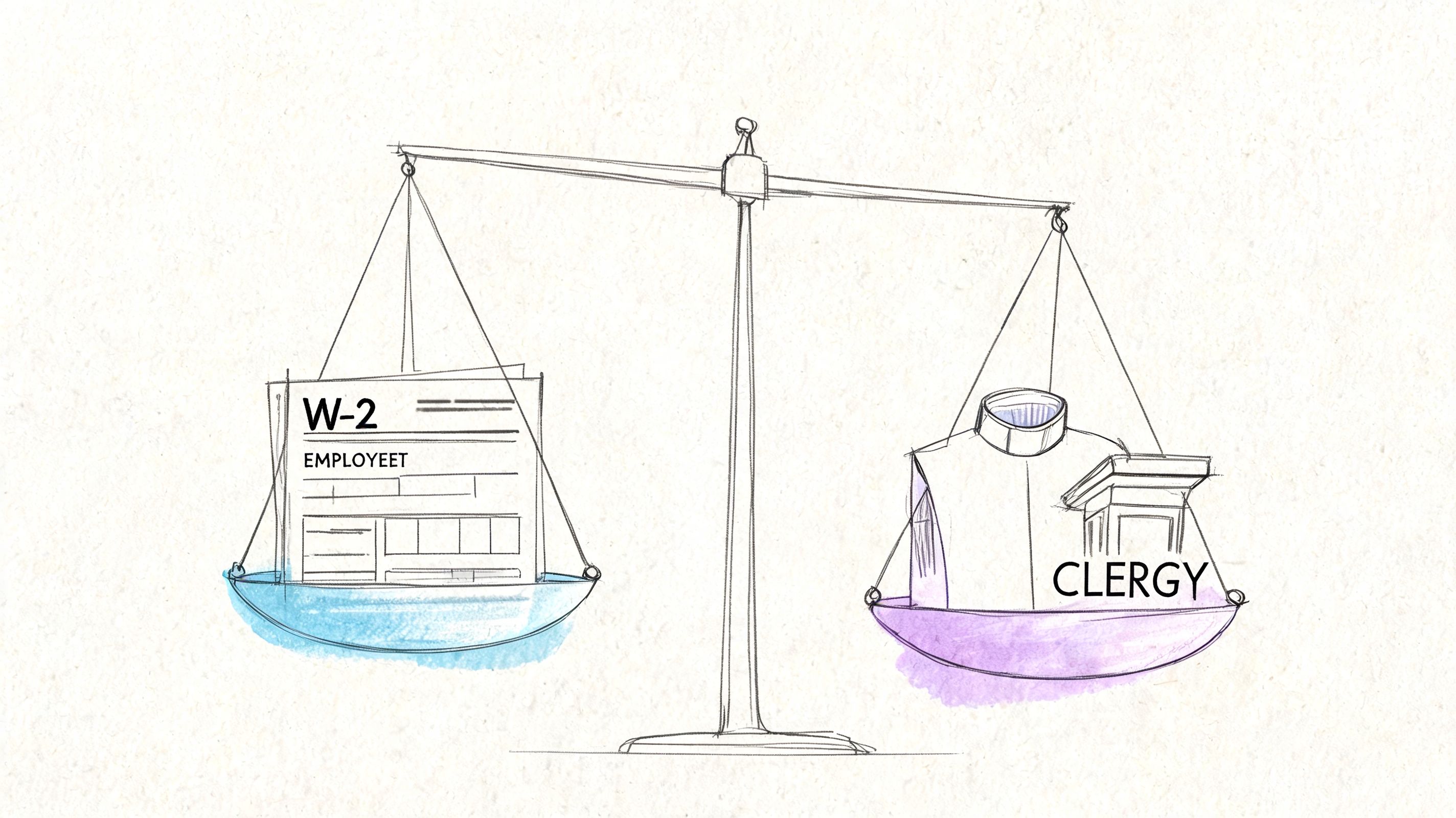

Payroll is where many churches get tripped up. The reason is simple. Churches often have a mix of ordinary employees, ministers, and occasional contractors, and each group has to be handled differently.

Employees, ministers, and contractors are not interchangeable

Your church secretary, custodian, and admin staff usually fit ordinary employee treatment. Their wages go through payroll, and the church handles reporting accordingly.

Ministers are different. Their tax treatment is one of the most important parts of church accounting regulations to understand early. Churches still report minister wages on Form W-2, but ministers commonly pay 15.3% SECA tax rather than having Social Security and Medicare withheld through ordinary FICA treatment, as noted in the earlier Aplos guidance.

Contractors are another area where churches need care. Calling someone a contractor doesn't make them one. If the church controls the work like it would an employee, casual classification can create problems later.

Housing allowance needs advance action

One of the easiest mistakes to make is treating housing allowance as an afterthought. It isn't.

The church needs to formally designate a minister's housing allowance before payment. That means the approval should happen through the proper leadership process and be documented in minutes or written compensation records. If you wait until year-end and try to fix it retroactively, you're already in a weak position.

Many church leaders think compliance is simple because churches usually don't file Form 990. But meaningful risk often shows up in edge cases such as housing allowance designation, private inurement, and possible unrelated business income from activities like facility rentals or online stores, as discussed in Build Your Firm on church tax and accounting needs.

Reimburse expenses the right way

Ministry expenses need structure. If a pastor or staff member pays for church expenses out of pocket, the church should use a documented reimbursement process with receipts and business purpose noted. That keeps ministry expenses separate from compensation.

What does not work is using vague monthly allowances with no support and assuming they'll stay non-taxable. Once reimbursements stop looking like reimbursements, they start looking like income.

A clean process usually includes:

- Written approval: The board or authorized leader approves the reimbursement policy.

- Timely submission: Staff submit receipts and explanations close to the expense date.

- Clear coding: The bookkeeper records the reimbursement to the right ministry expense account, not to wages.

- Review before payment: Someone other than the claimant reviews the documentation when possible.

For a quick visual walkthrough of the broader payroll issues churches face, this overview is useful:

What a treasurer should review each pay cycle

You don't need a complex checklist to improve payroll. You need a repeatable one.

- Check classification first: Employee, minister, or contractor should be decided before payment starts.

- Confirm approved compensation: Salary, housing allowance, and any benefits should match board authorization.

- Tie reports together: Payroll records, quarterly filings, and year-end forms should agree.

- Watch unusual payments: Love offerings, stipends, honoraria, and one-time reimbursements deserve a second look before they go out.

When payroll is messy, the problem usually started months earlier with an unclear decision that nobody documented.

Keeping Donor Promises with Fund Accounting

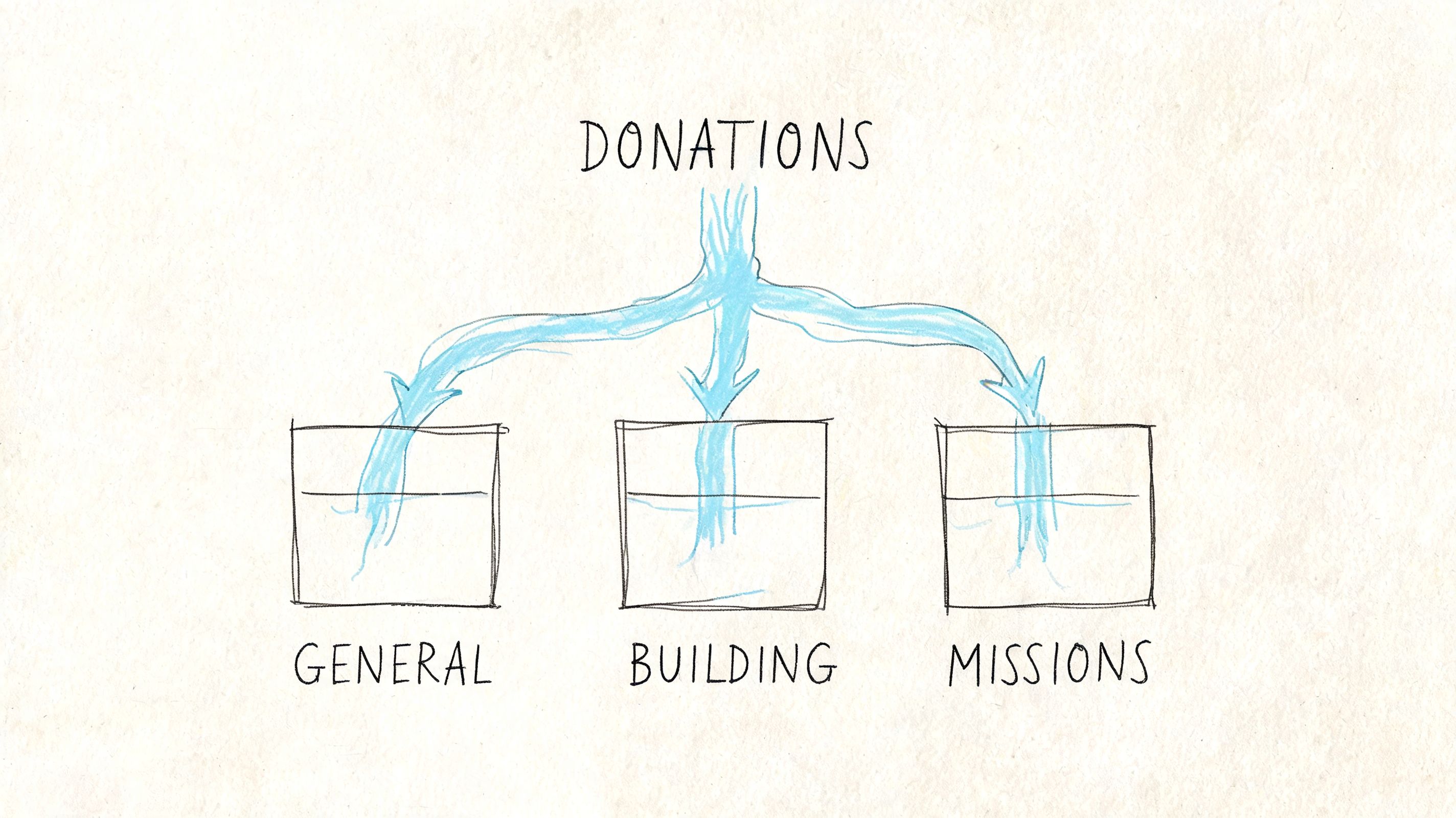

A new treasurer often discovers the problem after the deposit hits the bank. Sunday's online gifts, text donations, and in-person offerings land as one number, but the congregation gave that money for different purposes. Missions money, benevolence support, and building gifts may share a bank account for a few days. They cannot share the same accounting treatment.

Fund accounting is how a church keeps its promises. It records not just how much cash came in, but what that money is for and whether the church still has it available for that purpose. That matters for compliance, but it also matters for trust. If a member gives to a building project or a missionary family, leadership needs records that show the gift stayed attached to that purpose from receipt through spending.

A church can use one operating bank account and still maintain proper fund records. The key is in the ledger. Each gift needs the right fund assignment when it is received, and each expense paid from a restricted purpose needs to reduce that same fund. If those steps are skipped, reports start showing money as available that the church has already promised to use elsewhere.

The fund categories that matter in real church work

Churches usually need three clear distinctions.

- Unrestricted funds: Gifts available for general ministry, operations, and ordinary church needs.

- Restricted funds: Gifts limited by the donor to a stated purpose such as missions, benevolence, scholarships, or a capital campaign.

- Board-designated amounts: Money the board sets aside internally for a goal or reserve. This is still unrestricted unless a donor placed the limit on it.

That last category causes confusion. A board can change a designation. It cannot change a donor restriction.

Restricted gifts should not be used to solve a temporary cash shortage in another area, even if leadership plans to replace the money later.

Where small churches lose the trail

The harder part now is not the concept. The harder part is keeping the donor's intent attached to the transaction across digital systems.

A member may choose “missions” in an online giving form. The processor batches that gift with others. The bank receives one combined deposit. Then a volunteer or bookkeeper posts the deposit as one contribution amount because the bank feed does not show the fund detail. At that point, the accounting records are already behind the actual activity.

I see this most often in smaller churches that added online giving before they tightened the back-office process. The ministry grew faster than the bookkeeping method. That is common, and it is fixable, but only if someone checks whether the restriction entered with the gift survives the trip from giving platform to bank settlement to final reporting.

As noted earlier, church fund accounting is the method that preserves donor restrictions. Ministry Brands makes the same practical point in its explanation of restricted and unrestricted funds in church accounting. The system has to carry the restriction all the way through the workflow, not just at the moment of donation.

Practical options, and their trade-offs

Different setups can work for a season. They do not carry the same risk.

| Approach | What it handles well | Where it creates risk |

|---|---|---|

| Basic business-style bookkeeping | Simple cash tracking and basic expense reporting | Restricted gifts can disappear inside general contribution totals |

| Spreadsheets layered on top of the books | Helpful for a careful treasurer managing a small volume | Easy to break, hard to review, and too dependent on one person |

| Fund-based church accounting system | Tracks gifts, balances, and spending by fund | Takes more discipline to configure correctly at the start |

The trade-off is straightforward. A simple ledger feels easier at setup. It usually creates more cleanup later, especially once the church has online giving, designated campaigns, benevolence requests, or facility projects happening at the same time.

When evaluating software, ask a direct question. Can this system keep the fund tied to the original gift through entry, deposit matching, reporting, and spending? If the answer is no, the church is relying on manual correction.

For churches that want fund-level tracking across giving, bank activity, and accounting, Grain Ledger is one church-specific option built around fund accounting rather than treating it as an afterthought. That system design affects whether reports clearly show what was given, what remains restricted, and what has already been used for ministry purposes.

Beyond Tithes UBIT and State Regulations

A church can be tax-exempt and still have tax exposure. That catches many boards off guard because they assume all church income is automatically treated the same way.

It isn't.

When church income starts looking different

Some revenue clearly fits the church's exempt purpose. Regular giving, offerings, and ministry support generally sit in familiar territory. The harder questions show up when a church adds activities that look more like ongoing commercial operations.

Examples that deserve review include:

- Facility rentals: Regular outside use of church space for a fee

- Online sales: Merchandise, curriculum, or product sales through a church website

- Event revenue: Activities that repeat and operate like a business line

- Stipends and side payments: Amounts paid without clear payroll or reimbursement treatment

The practical question is not, “Did money come in?” The practical question is whether the activity is substantially related to the church's exempt purpose or whether it creates a separate tax issue that leadership should evaluate.

A simple way to flag possible UBIT issues

You don't need to decide every tax question alone. You do need to know when to raise your hand.

Use this screen when an activity feels unusual:

| Question | Why it matters |

|---|---|

| Is this a regular activity rather than occasional? | Ongoing activity draws more scrutiny than one-off use |

| Does it look like a trade or business? | Commercial characteristics may change the tax analysis |

| Is it clearly related to the church's exempt purpose? | Related ministry purpose is the key distinction |

If the answer pattern points toward regular commercial activity that isn't strongly tied to ministry purpose, get qualified review before assuming the revenue is harmless.

State rules are easy to miss

Federal rules get most of the attention, but churches can also face state-level requirements. A common blind spot is charitable solicitation rules, especially when a church raises support online or across state lines. Another is the treatment of property, payroll, and registration obligations that differ by state.

The safest assumption is not that your state works like your neighbor's. It often doesn't.

A wise treasurer keeps a short list of outside activities the church has added over the last year. Rentals. Sales. Events. Online fundraising campaigns. Then review each one with someone who understands church taxation in your state. That review is usually easier than repairing a bad assumption later.

Building Trust Through Controls and Reporting

On a Tuesday morning, the treasurer is asked three reasonable questions at once. Why does the online giving total not match the bank deposit? Was the fellowship hall rental income posted to the right place? Did a designated mission gift get spent by mistake? If the church cannot answer quickly and calmly, the problem is usually not dishonesty. It is a weak control process.

Controls protect the church in two directions. They reduce the chance of loss or error, and they protect faithful staff and volunteers from avoidable suspicion. In a small church, that often matters more than people realize. One unclear transfer, one missing receipt, or one payment approved after the fact can drain trust faster than the dollar amount involved.

Controls every small church can scale

Small churches do not need a complicated system. They need a repeatable one that still works when one volunteer is sick, a pastor is traveling, or gifts come in through a mix of cash, checks, card processing, and automated online platforms.

A practical baseline looks like this:

- Separate receiving from recording: The person opening mail, counting offerings, or reviewing online giving batches should not be the only person posting those receipts to the books.

- Require documented approval for spending: Checks, ACH payments, debit card use, reimbursements, and unusual transfers should have clear approval before payment is released.

- Reconcile every month: Bank and credit card accounts need timely reconciliation so errors are caught while they can still be explained.

- Limit system access: Only the people who need permission to add vendors, edit prior transactions, or release payments should have it.

- Review digital giving reports: Payment processor activity, donor platform summaries, and bank deposits should be matched regularly. Small churches often miss fees, timing differences, or duplicate entries in these records.

- Tie payroll reports together: Quarterly filings, year-end forms, and payroll records should agree before year-end pressure sets in.

The finance manual in this church financial reporting guide points to practical disciplines such as monthly reconciliations, payroll tie-outs, approvals, and separation of duties. Those are not just audit ideas. They are everyday stewardship habits.

Why reporting basis matters

Cash-basis bookkeeping is common in churches because it is simple and lines up with the bank balance. For day-to-day monitoring, that can be workable.

Board reporting and formal financial statements often need more than a cash view. Audited statements follow U.S. GAAP on an accrual basis, which means the records reflect obligations, receivables, prepaid costs, and fixed assets when they arise, not only when cash moves. That difference matters when the church has unpaid bills, pledged gifts still outstanding, payroll liabilities, or rental activity that crosses reporting periods.

I have seen churches feel comfortable because cash was strong at month-end, while credit card balances, reimbursements, and restricted commitments were sitting outside the picture. A clean report should answer the fundamental question. What resources are truly available for ministry after obligations and restrictions are considered?

Record retention should be written down

Document retention fails without warning. A volunteer changes. A laptop is replaced. A file lives in someone's email instead of a shared record system. Two years later, no one can find the approval for a housing allowance designation, a major purchase, or a donor-restricted project.

Write the retention policy down and keep it simple. Contribution records, bank support, and payable or receivable records are commonly kept for several years. Corporate records, property records, board minutes, and tax-exemption documents should be kept permanently, including digital copies stored in a controlled location. If your church uses cloud accounting, online giving, and scanned receipts, make sure someone is responsible for exports and backups. Software access is not the same thing as record retention.

What boards actually need

Boards need reports they can act on.

A useful monthly packet usually helps leaders answer these questions:

- What cash is available for normal operations?

- Which balances are donor-restricted or board-designated?

- Is actual spending tracking with the approved budget?

- Are there unpaid obligations, payroll items, or unusual transactions that need attention?

- Did any digital giving, rental income, or other nonroutine activity need special review this month?

Clear reporting strengthens ministry integrity. It shows donors, staff, and elders that the church handles money with the same care it gives to teaching, care, and mission. That confidence is built one reconciliation, one approval, and one understandable report at a time.

Compare platforms in our best church accounting software guide for 2026, or review Grain Ledger church accounting software.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Your Churchs Financial Compliance Checklist

A new treasurer often inherits more than a checkbook. Online giving feeds into one system, payroll lives in another, rental deposits hit the bank with little explanation, and the board assumes the reports tie together. A good checklist brings order to that mix and helps you catch problems while they are still easy to fix.

Start with the records that prove the church exists, owns what it owns, and approved what it approved. If those documents are scattered across email inboxes, old laptops, and a filing cabinet no one has opened in years, clean that up first. Small churches rarely get in trouble because they ignored everything. They get in trouble because one missing document turns a routine question into a scramble.

Start with legal and governance basics

- Verify your core records: Confirm that organizing documents, tax-exemption records, deeds, loan files, and insurance documents are easy to find and stored permanently.

- Review board approvals: Check that compensation decisions, housing allowance designations, major purchases, and restricted project approvals appear clearly in board minutes.

- Check policy gaps: If reimbursement, spending approval, cash handling, or gift acceptance policies are missing, put them on the board agenda.

Review payroll and compensation decisions

Payroll errors tend to linger because they repeat every pay period.

Begin with classification. Identify who is an employee, who is clergy, who receives a stipend, and whether anyone has been paid informally without a clear tax treatment. Then compare payroll records to quarterly filings and year-end forms. If the numbers do not match, address that before the next filing cycle.

- Confirm classification: Match each worker to the right category and document the reasoning.

- Inspect clergy documentation: Verify that housing allowance amounts were designated in advance and recorded in the minutes.

- Match reports: Compare payroll registers, tax filings, and year-end reporting for consistency.

Test your fund handling process

Fund tracking is where many small churches feel the strain of digital tools. A donor gives through an app, the processor batches deposits, the bank combines transactions, and the accounting entry gets posted later by hand. If the trail breaks at any point, restricted gifts can be spent or reported incorrectly.

The question is simple. Can the church follow a designated gift from donation to deposit to ledger to report?

Use these questions:

- Can you trace designated gifts clearly? A missions gift should stay identifiable after it passes through an online platform, a bank deposit, and the accounting system.

- Do reports separate restricted and unrestricted balances? Board decisions are weaker when those balances are blended together.

- Are you relying on manual workarounds? If one volunteer's spreadsheet is the only place fund detail exists, the process is fragile.

Strengthen controls without making ministry heavy

Good controls should fit the size of the church. A small staff may not be able to separate every duty perfectly, but it can still build review points that reduce mistakes and deter misuse.

- Assign separate roles for receiving, depositing, and recording when staffing allows.

- Require monthly reconciliations and have someone other than the bookkeeper review them.

- Review unusual income sources such as rentals, bookstores, event fees, or parking income for tax and reporting implications.

- Use accounting tools built for funds if your current setup cannot keep donor restrictions clear without extra spreadsheets.

The goal is not more paperwork. The goal is reliable records, honest reporting, and decisions made from numbers the board can trust.

If your church is outgrowing spreadsheets or trying to preserve donor restrictions across giving platforms, bank activity, and accounting records, Grain is worth a look. It's built for church fund accounting, so transactions and reports are organized around funds from the start, which helps treasurers maintain clear fund-level visibility and stronger stewardship controls.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.