Streamline Church Accounting Software with Payroll

Find the best church accounting software with payroll. Learn fund accounting, clergy tax compliance, & how to choose the right solution for your church.

The finance committee meeting usually starts with a simple question. “Can we see what payroll is costing each ministry?”

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

That's where many churches get stuck. Payroll lives in one system. Donations live in another. The general ledger sits in a spreadsheet or a generic accounting tool. Then someone, often the treasurer or bookkeeper, manually re-enters payroll totals, guesses at allocations, and hopes the youth pastor's compensation, the missions assistant's hours, and the pastor's housing allowance all land in the right places.

That workflow feels normal because it's common. It's also where stewardship gets cloudy.

Churches don't need accounting software that merely records expenses after the fact. They need church accounting software with payroll that understands funds at the transaction level, handles clergy pay correctly, and produces reports that leadership can trust without a long verbal explanation. If the software can't do that, the church ends up managing ministry finances with workarounds instead of controls.

The Hidden Costs of Disconnected Church Payroll

A disconnected payroll process rarely fails in a dramatic way. It fails subtly.

A payroll service runs direct deposit on Friday. On Monday, the treasurer logs in, exports a report, and starts breaking totals apart by hand. Part of one salary belongs in the general fund. Another portion should hit a restricted ministry fund. Payroll taxes need to be posted somewhere else. If the church is using a separate spreadsheet to track designated gifts, someone also has to check whether enough money is available in the fund that's supposed to carry that payroll cost.

None of that work is ministry. It's cleanup.

Where the time goes

The hardest part isn't entering numbers. It's preserving meaning. Once payroll and accounting are split apart, every entry becomes a translation exercise. The bookkeeper has to remember what each amount was for, which fund it belongs to, and whether any part of it needs special tax treatment.

That's why finance teams often feel behind even when they're working hard. They're not just closing the books. They're reconstructing the story of what already happened.

Practical rule: If payroll has to be re-keyed or reclassified after it runs, the church is carrying avoidable risk.

A lot of general payroll advice still applies. Clean approval steps, consistent pay schedules, and documented workflows matter in any organization. For committees that want a broader operations perspective, this payroll guidance for SMB leaders is useful background. Churches, though, have an added layer. Payroll has to line up with donor restrictions and ministry-specific reporting, not just wages and taxes.

What leaders stop seeing

When systems don't talk to each other, leadership loses real-time visibility. The pastor asks whether the outreach fund can support an added staff commitment. The answer should come from the books. Instead, it comes from a cautious estimate because the latest payroll allocation hasn't been entered yet.

That uncertainty changes behavior. Boards delay decisions. Treasurers hold back recommendations. Staff leaders stop trusting reports that need too much explanation.

Integrated church accounting software with payroll fixes more than data entry. It restores confidence that compensation, fund balances, and ministry spending all reflect the same reality on the same day.

Why Generic Payroll Fails Churches

A finance committee approves payroll on Tuesday. By Thursday, the treasurer is splitting one salary across missions, children's ministry, and the general fund in a spreadsheet because the payroll system posted everything to a single expense account. The paychecks were correct. The books were not.

Generic payroll tools are built to calculate wages, withhold taxes, and send direct deposits. Churches need more than that. Payroll has to post into the right funds at the moment it is recorded, especially when compensation is tied to designated giving, ministry budgets, or clergy-specific treatment. If the system cannot do that natively, staff has to patch the gap by hand.

Fund accounting isn't optional

Many business systems can tag payroll after the fact by class, department, or memo. That may look acceptable in a demo. In practice, it means the underlying ledger was never built around funds in the first place.

That distinction matters. Churches do not just need payroll reports sorted by ministry. They need compensation, taxes, and benefits recorded inside the proper fund structure from the start. Otherwise, restricted support can be overstated in one report, understated in another, and corrected only after someone notices the mismatch.

I have seen committees assume this is a reporting nuisance. It is an accounting problem. If payroll hits the wrong place first and gets reclassified later, the church spends part of every month working around software that does not understand church stewardship.

Clergy pay breaks standard payroll logic

Ministers create a second failure point for generic systems. Housing allowance, accountable reimbursements, and the unusual tax treatment of clergy do not fit the assumptions used in ordinary payroll setups. A platform designed for retail, construction, or professional services often forces the church to track part of that logic outside the payroll run.

That is where mistakes creep in. A housing allowance may be approved by the board but not reflected correctly in payroll records. Social Security and Medicare treatment may be misunderstood. Year-end review becomes a scramble through spreadsheets, payroll notes, and prior committee minutes instead of a clean audit trail inside one system.

A generic payroll system can issue a paycheck. Churches still need payroll records that reflect ministerial compensation correctly.

Restricted gifts raise the stakes

Suppose youth donors gave with the expectation that their support would help cover youth ministry staffing. If payroll defaults to a general operating account and someone plans to fix the entries later, interim reports can show the wrong fund balance for weeks. Leaders may approve spending based on numbers that are temporarily wrong but functionally influential.

That is why simulated fund accounting is risky. It asks the team to trust a later cleanup step. True fund architecture records the expense where it belongs before reports ever reach pastors, elders, or the board.

Churches reviewing systems often see the same pattern in other administrative tools. Separate apps create extra handoffs, duplicate entry, and more chances for something important to be miscoded. If your team is looking beyond payroll too, it is reasonable to examine how ministries boost nonprofit efficiency with project software. The same operational lesson applies here. Software should reduce correction work, not create it.

What generic tools do well, and where they stop

A basic payroll stack can serve a church with one or two employees, a single operating fund, and little complexity in compensation. It can calculate standard payroll, support direct deposit, and file routine tax forms.

Problems usually show up when the church needs:

- Native fund posting: Wages, payroll taxes, and benefits assigned to the correct funds during payroll entry, not reclassified later.

- Clergy-specific setup: Housing allowance and minister compensation handled inside the payroll and accounting records.

- Reliable reporting: Statements the finance committee can read without asking which spreadsheet contains the corrected version.

- Cleaner month-end close: Less manual journal work to repair payroll entries that landed in the wrong place.

That is the primary dividing line. Generic software processes payroll as a standalone task. Church accounting software with payroll has to treat payroll as part of the church's actual fund structure, or the finance team ends up simulating church accounting inside a business system.

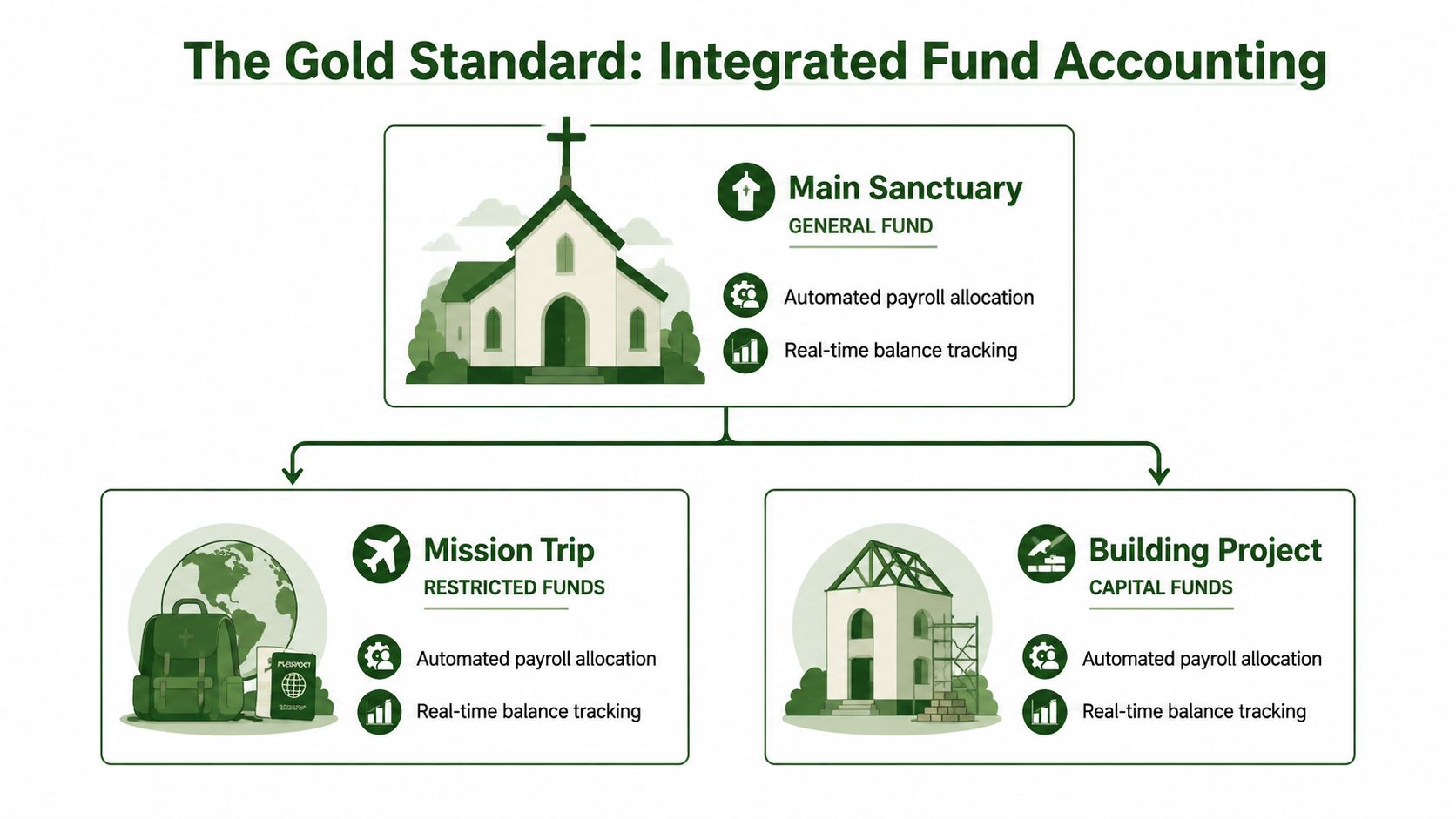

The Power of True Fund Accounting with Payroll

A finance committee often discovers the problem at month-end. Payroll has already run, staff were paid on time, and the reports still do not answer a basic question: which fund carried those costs?

That confusion comes from architecture, not effort.

True fund accounting means payroll and accounting share the same fund structure from the start. Wages, taxes, and benefits post to the right fund when payroll is processed. The system is not treating funds as labels added for reporting after the fact. It is preserving fund boundaries inside the ledger itself.

One accounting model creates rework. The other preserves intent.

Churches hear a lot of language about classes, tags, and departments. Those tools can help with reporting, but they are not the same as native fund architecture.

In a simulated setup, payroll usually posts into a general structure first. Someone then sorts, reallocates, or reclassifies the costs so reports make sense by fund. That may look acceptable in a demo. In live use, it creates avoidable risk. Restricted activity can be misstated for weeks, ministry leaders may be looking at incomplete balances, and the treasurer ends up maintaining side schedules to explain what the software should already know.

A native fund system works differently. The payroll allocation is tied to the fund during processing, so the ledger reflects the ministry reality immediately.

That is the difference that matters.

What fund integrity looks like in practice

Payroll is one of the fastest ways to expose whether a system has true fund accounting or a simulation of it.

If a youth pastor is paid from the general fund and a designated outreach fund, the software should split salary expense, employer taxes, and related benefits correctly at the time of payroll. If the church later runs reports on either fund, those reports should already be right. The finance office should not need a spreadsheet to recreate the payroll entry in a way the board can understand.

When payroll is integrated into native fund accounting:

- Restricted balances stay reliable: Fund reports reflect posted activity, not pending cleanup entries.

- Compensation follows ministry activity: Staff costs appear in the funds that supported the work.

- Oversight improves: The finance committee can review current numbers without asking for off-system corrections.

- Closing the books gets simpler: The team spends less time repairing payroll allocations and more time reviewing the reports.

Board-level test: If your treasurer needs a side worksheet to explain payroll by fund, the accounting system is incomplete.

A simulated system can still produce a polished report. The problem is what it takes to get there. Someone has to remember the allocation rules, enter the adjusting journal, check that benefits were split the same way as wages, and confirm nothing hit the wrong fund. In a church with multiple ministries, designated gifts, and a mix of clergy and non-clergy staff, that is not a small administrative nuisance. It is an ongoing control weakness.

Here's a practical comparison:

| Approach | How payroll is handled | What usually happens at month-end |

|---|---|---|

| Simulated fund tracking | Payroll posts to a general ledger first, then gets tagged or adjusted later | Treasurer checks spreadsheets, reclasses entries, explains variances |

| Native fund architecture | Payroll allocations are tied to funds during processing | Team reviews reports, confirms balances, closes books with fewer manual fixes |

A short walkthrough helps make the concept more concrete:

Why this matters for stewardship

Stewardship requires more than good intentions. It requires records that hold together under review.

Churches often have careful volunteers and honest staff, yet still produce confusing fund reports because the system was built for business bookkeeping first and church fund accountability second. Native fund accounting reduces that risk by treating restricted funds, designated gifts, and payroll allocations as part of the accounting structure itself.

That is the standard worth using. Convenience features matter, but if the underlying model forces your team to simulate fund accounting after payroll runs, the church is carrying unnecessary compliance and reporting risk.

Essential Features for Compliant Church Payroll

A lot of software looks adequate until you ask detailed payroll questions. That's where weak systems get exposed.

Church finance has become more complex over time. Early tools such as ChurchPro offered foundational capabilities by the early 2000s, and modern church platforms such as PowerChurch and Realm now combine clergy-specific payroll needs, including housing allowances and dual-status handling, with cloud-based fund accounting, as described by ChurchPro's overview of church accounting software evolution.

That history matters because it shows the baseline has changed. Churches shouldn't shop for payroll as if basic check printing and general ledger posting are enough.

The non-negotiables

When I review church accounting software with payroll, I don't start with price. I start with failure points. If a tool can't handle these cleanly, the team will end up maintaining shadow processes outside the system.

Housing allowance support

The software should let you define and track ministerial housing allowance clearly. If that has to be managed in a note field or an external spreadsheet, year-end reporting becomes fragile.Dual-status tax handling

Ministers are a special case. The system needs to support clergy-specific tax treatment without forcing the church into manual overrides every payroll cycle.Fund-based payroll allocation

Salary, employer taxes, and related expenses should post to the correct funds without a separate journal entry marathon after payroll runs.W-2 and 1099 workflow support

Churches need software that can produce year-end payroll reporting correctly and consistently. If the system punts this to manual exports and third-party cleanup, expect stress in January.Direct deposit and dependable payroll processing

Staff still need to be paid accurately and on time. Church-specific compliance doesn't replace payroll basics. It adds to them.

Features that save committees from recurring headaches

Some capabilities don't sound glamorous, but they matter every month.

Audit-friendly reporting

A strong system should show not just payroll totals, but how those totals flowed by employee, fund, and account. That lets a finance committee trace the transaction path without hunting through disconnected records.

Clear approval controls

Churches often rely on a mix of staff and volunteers. Good software should support role-based access so one person isn't setting up payroll, approving it, and reconciling it alone. Even in a small office, separation of duties matters.

Integrated posting to the ledger

When payroll posts automatically into the accounting system, the books stay current. When payroll is summarized manually later, the team loses detail and often introduces inconsistency from one pay period to the next.

Good church payroll software doesn't just issue paychecks. It leaves behind a clean accounting trail.

Questions to ask in a demo

Rather than asking, “Do you support church payroll?” ask narrower questions.

- Can one employee's compensation be allocated across multiple funds at payroll time?

- How is housing allowance entered, tracked, and reported?

- What happens when a minister and a non-minister are both on the same payroll run?

- Can I produce a fund-level payroll report without exporting to Excel first?

- What manual work remains after payroll is processed?

Those questions get past marketing language. They reveal whether the platform was designed for actual church finance work or adapted from a business template.

How to Evaluate Your Software Options

Many churches don't need more software options. They need a sharper filter.

Small to medium-sized congregations represent 85% of U.S. churches, but they're often underserved by generic tools. A 2026 market analysis cited by Springly notes that 67% of top church accounting solutions offer native or integrated payroll, with cloud-based options now dominating the market and helping churches unify fund accounting with payroll to track restricted funds properly, as summarized in Springly's church accounting software analysis.

That tells you two things. First, payroll integration is no longer unusual. Second, not every product that claims church fit solves the same problem equally well.

Start with your actual complexity

A finance committee should map the church's real operating conditions before watching demos.

Consider these factors:

- Staff mix: Are you paying only non-clergy employees, or do you also have ministers with housing allowance and special tax treatment?

- Fund structure: Do you track only a general fund and a couple of designated buckets, or do you manage multiple ministry, mission, and project funds?

- Connected systems: Does the church already use a giving platform or bank tools that need to feed accounting cleanly?

- Team capacity: Is the system going to be used by an experienced bookkeeper, a volunteer treasurer, or both?

Those questions matter more than feature grids. A small church with simple staffing but several restricted funds may need stronger fund architecture than a larger church with straightforward payroll.

Don't confuse integration with architecture

This is the point most buyers miss. A vendor may say it integrates with payroll. That sounds promising, but integration alone doesn't tell you how payroll data behaves once it enters the accounting system.

Some products import payroll summaries into a general ledger and ask users to handle the fund logic afterward. Others preserve the fund structure during processing. Those are not equivalent.

If your committee is comparing a general accounting product with church-specific tools, it can help to see how outside users think about one of the common options. This overview of ConvertBankToExcel for QuickBooks users is useful because it highlights the kind of workflow add-ons people seek when a general platform doesn't fit their exact process. Churches run into a similar issue when they rely on extensions and exports to make payroll and funds line up.

A practical scorecard

Use a short decision table during evaluation meetings:

| Question | Adequate answer | Strong answer |

|---|---|---|

| How are restricted funds protected? | Manual tagging or end-of-month reclass entries | Native fund logic embedded in daily transactions |

| How does payroll hit the ledger? | Summary import or manual posting | Automatic posting with fund-level detail |

| How are clergy compensation rules handled? | Workarounds or external notes | Built-in support within payroll workflow |

| Can leadership read reports without explanation? | Sometimes, with side spreadsheets | Yes, reports reflect actual fund activity directly |

A tool can check many boxes and still fail the most important test. The question isn't whether it can produce a report eventually. The question is whether the report is trustworthy without cleanup.

For churches that care about restricted gifts, ministry accountability, and cleaner payroll operations, native fund architecture is the line that separates an acceptable system from a durable one.

Compare platforms in our best church accounting software guide for 2026, or review Grain Ledger church accounting software.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Unifying Your Finances with Grain Ledger

A common church payroll week looks like this. Giving closes on Sunday night, payroll has to be approved by Tuesday, and by Friday the treasurer is already asking which staff costs belong in general, missions, or childcare. If those answers live in three systems and two spreadsheets, the books may still get closed, but only after manual allocation, follow-up questions, and a fair amount of guesswork.

How a unified flow should work

In Grain Ledger, the goal is to reduce handoffs. A designated gift is recorded to the right fund at entry. Bank activity can be matched back to that fund structure inside the ledger. Then payroll follows the same logic instead of arriving later as a lump-sum journal entry that someone has to split by hand.

That changes the monthly routine in practical ways.

If a youth pastor's compensation is approved across general and youth ministry funds, the allocation can be reflected in payroll and posted into accounting with the same structure leadership already uses for reporting. If clergy compensation includes housing allowance or stipend treatment, those items can be handled inside payroll without breaking the audit trail between compensation, expense coding, and the fund reports the finance committee sees.

The result is a cleaner close. The treasurer is reviewing activity, not rebuilding it.

What that looks like in day-to-day operations

A unified setup helps at the points where churches usually lose time:

- donations do not need to be reclassified after import just to reflect donor intent

- payroll entries do not need separate spreadsheet allocations before they hit the books

- restricted fund balances update as payroll and expenses post, not weeks later

- finance committee reports are easier to read because they reflect posted activity instead of cleanup entries

Those are small process changes, but they matter. Churches rarely fall behind because one task is impossible. They fall behind because every pay period adds five more manual decisions that nobody has documented well.

Where Grain Ledger fits

Grain Ledger is built for churches that want giving, accounting, and payroll to run in one fund-based workflow. The practical benefit is not abstract. It means fewer export files, fewer end-of-month reallocations, and fewer situations where only one staff member understands how the payroll numbers made it onto the fund report.

That matters most in churches with lean finance teams. In many congregations, the people handling payroll and bookkeeping are balancing this work with HR, administration, and Sunday operations. They need a system that carries approved fund logic through routine transactions so stewardship does not depend on memory.

I have seen committees tolerate workarounds for years because the reports eventually came out. The problem shows up when a designated gift, a housing allowance detail, or a multi-fund salary allocation is handled differently by two different people. Then the church is no longer dealing with inconvenience. It is dealing with inconsistency in records that leadership and donors rely on.

If your church is tired of fixing payroll and fund reports by hand, take a closer look at Grain. It's built for churches that need fund-based accounting, integrated financial workflows, and reporting that reflects how ministry money is received, allocated, and spent.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.