Do Churches Have to Disclose Financial Information?

Do churches have to disclose financial information? Explore 2026 IRS rules on transparency, learn why it matters, and report to your congregation with

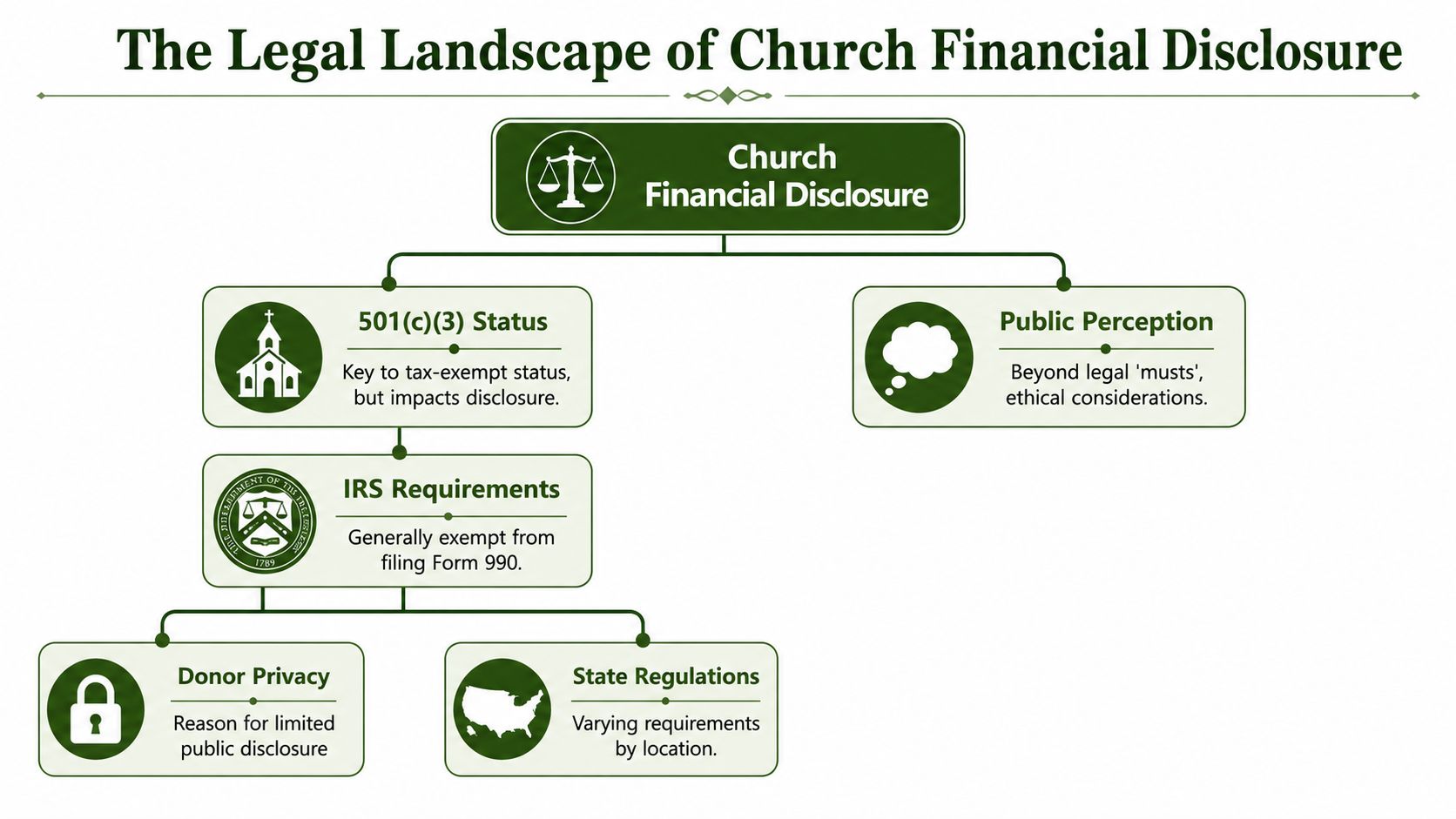

In the United States, churches are generally not required to publicly disclose their finances through the federal nonprofit filing system because they're exempt from the IRS Form 990 requirement that most 501(c)(3) nonprofits use. But that simple answer doesn't settle the central question most church leaders are facing, which is who should see financial information, how much they should see, and what faithful transparency looks like in practice.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

A lot of leaders run into this question the same way. A member raises a hand at an annual meeting and asks for the budget. A treasurer gets an email asking how missions money was used. An elder wonders whether salary information should be shared with the congregation. None of those questions are merely legal. They're pastoral, relational, and tied to trust.

That's why "do churches have to disclose financial information" is really two questions. One is about law. The other is about stewardship. A church can be fully within its legal rights and still handle money in a way that leaves members confused, donors uneasy, or leaders exposed to unnecessary suspicion.

Healthy churches learn to separate what the government requires from what wise governance requires. They also learn that financial openness doesn't mean publishing every ledger line to everyone. Good transparency is structured, understandable, and tied to the church's mission.

Introduction The Question Every Church Leader Faces

The moment often comes.

A church member walks up after service or speaks up during a business meeting and asks, “Can members see where the money goes?” Nobody in the room is trying to start a fight. Still, the temperature changes. The pastor wants to protect unity. The treasurer wants to answer accurately. The board wants to avoid saying too much or too little.

That tension is normal. Churches handle donated funds, designated gifts, payroll, benevolence, and ministry expenses. People give sacrificially, and they want to know that leaders are stewarding those resources carefully. When leaders don't have a clear reporting practice, even a fair question can feel threatening.

A church usually doesn't lose trust because members asked financial questions. It loses trust when leaders seem unsure, defensive, or inconsistent in answering them.

Many new board members assume there must be a simple federal rule. Either churches have to disclose everything, or they don't. In reality, the legal answer is narrower than generally expected, and the practical answer is broader.

A helpful way to think about it is this:

- Legal disclosure concerns what a church must provide under federal law.

- Internal disclosure concerns what leaders choose to share with members, staff, and donors.

- Healthy disclosure concerns how the church communicates stewardship in a way people can understand.

The first category is often more limited than people assume. The third category is where wise churches spend most of their energy.

If you're a pastor, elder, finance committee member, or volunteer treasurer, you don't need to become a lawyer to handle this well. You do need a clear grasp of the rules, the gray areas, and the reporting habits that build confidence instead of confusion.

The Legal Landscape of Church Financial Disclosure

The legal answer starts with one narrow federal rule. In the United States, churches usually do not have to file IRS Form 990, the annual return that many other 501(c)(3) nonprofits submit and that the public can review. That exemption is one of the main reasons church finances are often less visible through standard IRS channels, as explained in this overview of church Form 990 exemption and public disclosure.

Why Form 990 matters

Form 990 is the filing many people associate with nonprofit transparency. It often gives donors, journalists, and members a basic view of revenue, expenses, salaries, and assets. Since churches are generally exempt from that filing, the public usually cannot pull up a church's finances the same way they can for many other charities.

That point causes a lot of confusion for board members. They hear “tax-exempt nonprofit” and assume every organization follows the same disclosure rules. Churches are treated differently here.

A good comparison is property records. If a document is not filed in the usual public office, outsiders cannot easily inspect it. Church finances work similarly under federal filing rules.

What federal law does and does not require

Federal law usually does not require a church to hand financial records to members on request. That surprises people, especially in congregations where giving is very personal and members feel a strong sense of ownership.

Still, federal law is only one layer. State nonprofit law, church bylaws, denominational rules, and internal policies can all shape who gets access to what. A board member should read those documents the way a treasurer reads a budget note. The broad category may sound simple, but the actual answer often sits in the fine print.

Courts have also been cautious about stepping into internal church disputes over finances, particularly where doing so would entangle the court in church governance or doctrine. So the practical question is often less about forcing disclosure and more about whether the church has already defined a clear process for reporting and accountability.

The legal answer in plain language

If you need a short, accurate answer in a meeting, use this:

| Legal question | Short answer |

|---|---|

| Must churches publicly file detailed finances with the IRS like most nonprofits? | Generally, no |

| Must churches automatically give members financial records under federal law? | Generally, no federal rule requires that |

| Can church bylaws or policies require disclosure? | Yes |

| Can state law or denominational structure affect access? | Yes |

That legal room should lower anxiety, not lower standards. The law sets a floor. Wise stewardship usually calls churches to build a higher one.

Beyond Compliance Why Voluntary Transparency Matters

Once leaders understand they usually aren't under a federal public-filing mandate, the temptation is to stop thinking about disclosure altogether. That's a mistake.

Trust grows when reporting is ordinary

People usually don't expect a church to behave like a publicly traded company. They do expect honesty, consistency, and visible care with donated money. When leaders share understandable financial information before conflict appears, they lower suspicion and raise confidence.

A simple annual report, periodic budget updates, and clear explanations of designated funds can do more than answer questions. They can shape the culture of the church. Members stop feeling like finances are hidden behind a curtain. They start seeing stewardship as part of the church's shared ministry.

Voluntary transparency also protects leaders. When reporting is regular, accusations lose force. Leaders don't have to improvise answers under pressure because the church already has a pattern of communication.

The fears leaders often carry

Some churches avoid openness because they fear criticism. If members see staff costs, they may object. If giving dips, people may worry. If spending looks uneven from month to month, someone may misunderstand the numbers.

Those concerns are understandable. They're also manageable.

- Criticism fear: Some disagreement is normal. Clear context usually prevents more conflict than secrecy does.

- Complexity fear: Most members don't need accountant-level detail. They need plain-language summaries.

- Low-giving fear: Honest communication often creates maturity, not panic.

- Salary fear: Sensitive items can still be handled through defined reporting levels instead of total secrecy.

Churches don't need maximum disclosure. They need meaningful disclosure.

Transparency is a stewardship decision

Money in a church is never just administrative. It touches worship, mission, compassion, staffing, and member trust. That's why voluntary transparency isn't mainly about satisfying curious people. It's about demonstrating that leaders treat financial stewardship as part of spiritual leadership.

A church can say, in effect, “We are handling these resources carefully, and we're willing to show our work.” That posture reassures generous givers, strengthens board oversight, and helps newer members understand how ministry is funded.

When leaders ask whether churches have to disclose financial information, the wiser follow-up question is this: What level of disclosure will help our church grow in trust and integrity?

Key Elements of Healthy Church Financial Reporting

A church doesn't need a complicated publishing operation to report well. It needs a consistent framework. The strongest systems usually share the right amount of detail with the right audience at the right time.

Different groups need different reports

The board or finance committee should usually see more detail than the congregation as a whole. That isn't secrecy. It's responsible governance.

A workable reporting structure often looks like this:

- Board and finance team reports: Detailed statements, budget-to-actual comparisons, cash position, fund balances, and unusual transactions.

- Staff leadership reports: Focused information tied to ministry planning, spending limits, and department accountability.

- Congregational reports: Clear summaries that explain income, expenses, major ministry categories, and the status of designated funds in plain language.

This tiered approach helps avoid a common mistake. Some churches share almost nothing. Others dump raw reports on members that only an accountant can decipher. Neither approach serves the congregation well.

What should be included

Healthy church reporting usually answers ordinary member questions before they're asked.

Consider including:

- Budget compared with actual activity: This helps leaders and members see whether spending and giving align with expectations.

- Designated fund reporting: If people gave to missions, benevolence, or a building effort, show that those funds were used as intended.

- A short narrative summary: Explain major changes, unusual expenses, or ministry wins connected to the numbers.

- Retention discipline: Financial reporting depends on reliable records. Church finance teams should keep records long enough to support compliance, donor accountability, and any IRS inquiry. Guidance for church financial records includes retention periods from at least seven years for donation logs and tax papers to permanent retention for incorporation and annual reports, as outlined in ParishSOFT's church financial recordkeeping guidance.

Church Financial Disclosure At-a-Glance

| Area of Disclosure | Legal Requirement (U.S. Federal) | Voluntary Best Practice |

|---|---|---|

| Public annual financial filing | Churches are generally exempt from Form 990 public filing | Share an annual financial summary with the congregation |

| Member access to financial detail | Usually not required by federal law | Define access rules in bylaws or policy |

| Internal board reporting | Not waived by good governance needs | Review regular, structured financial statements |

| Designated funds | Public filing exemption doesn't remove stewardship responsibility | Report fund balances and fund usage clearly |

| Record retention | Financial records still matter for compliance and inquiry support | Keep records according to a written retention schedule |

If a donor gives to a building fund, the church should be able to show that the money remained tied to that purpose. That's one of the clearest tests of financial credibility.

A reporting habit that works

Many churches do well with a simple rhythm:

- Detailed reporting to the board on a regular basis.

- Periodic updates to key ministry leaders.

- A yearly member-facing report with charts, summaries, and explanation.

- A documented retention policy so nothing important disappears when volunteers rotate off.

This isn't burdensome when the system is clean. It becomes burdensome when records are scattered across spreadsheets, bank portals, giving tools, and memory.

The Role of True Fund Accounting in Transparency

Financial transparency gets much easier when the accounting system matches how churches operate. That's where fund accounting matters.

Think in digital envelopes

A simple analogy helps. Imagine every dollar entering the church is placed into a labeled envelope. One envelope says General Fund. Another says Missions. Another says Building Fund. Another says Benevolence.

Those envelopes are not interchangeable. If someone gives to missions, the church shouldn't divert that money to payroll just because cash is tight. Fund accounting helps leaders track those distinctions accurately so restricted and designated money stays tied to its intended purpose.

That's the heart of church transparency. People don't only want to know how much came in and how much went out. They want confidence that the purpose of each gift was honored.

Why standard business accounting can create confusion

Many churches begin with general-purpose bookkeeping software because it's familiar. That can work for basic income and expense tracking, but churches often need something more precise. A business-oriented setup may require workarounds to reflect ministry funds, donor restrictions, and board-level reporting needs.

When accounting doesn't natively track funds, teams often compensate with extra spreadsheets, manual reconciliations, and side notes that only one volunteer understands. That makes reporting fragile. It also makes transparency harder because the church can't easily produce reliable fund-level statements.

Here's the practical issue: if leaders can't quickly answer where the missions balance stands, what was spent from benevolence, or whether the building fund was used correctly, they can't communicate with confidence.

What true fund accounting changes

A true fund-based system organizes the books around church funds from the beginning, not as an afterthought. That means the church can generate reports that reflect actual ministry realities.

Good fund accounting supports transparency in several ways:

- Restricted funds stay visible: Leaders can see what belongs where.

- Reports become easier to explain: Board members don't need to mentally reconstruct the story.

- Donor intent is easier to honor: The system itself supports the right behavior.

- Yearly communication improves: Congregational summaries become more trustworthy because the underlying data is cleaner.

Strong transparency usually starts long before the annual meeting. It starts with a chart of accounts and reporting structure that fit church life.

If a church wants calm, credible conversations about money, the accounting structure has to do some of the heavy lifting. Otherwise every disclosure effort turns into a manual cleanup project.

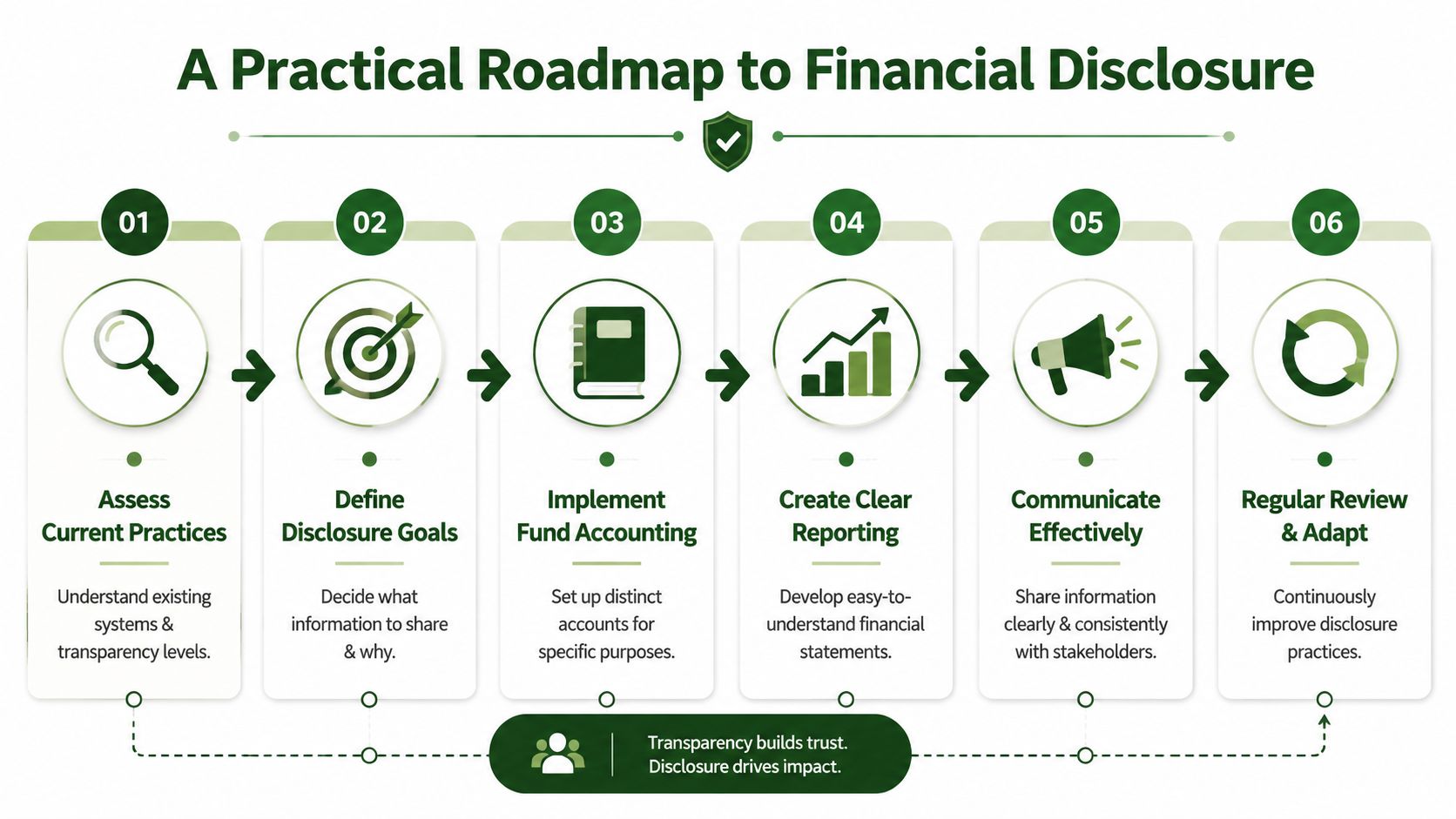

A Practical Roadmap to Financial Disclosure

Churches rarely become more transparent by accident. They improve when leaders make a few deliberate decisions and keep them simple.

Start with agreement, not spreadsheets

Before changing reports, get alignment among the people who lead. Pastors, elders, finance committee members, and the treasurer should agree on why the church wants stronger disclosure. If one group sees reporting as discipleship and another sees it as risk management only, the process will drag.

Agree on a few practical commitments. For example, the church may decide that designated funds will be reported clearly, member summaries will be offered regularly, and board reports will follow a standard format.

Build the reporting system in layers

Once leadership is aligned, create the reporting structure.

- Assess current practice. Identify what the church already tracks, what is missing, and where confusion usually appears.

- Choose a fund-based accounting approach. A church needs a system that can produce clear fund-level reporting without constant manual patching.

- Define reporting tiers. Decide what goes to the board, what goes to staff leaders, and what goes to the congregation.

- Set a calendar. Reporting becomes normal when it happens on schedule instead of only during conflict.

- Prepare a member-friendly annual report. Use plain labels, simple charts, and short explanations.

- Create a question process. Let members know how to ask thoughtful follow-up questions and who handles them.

Keep the first version simple

Some churches stall because they try to design a perfect transparency package. Don't. Start with a clear board packet, a concise annual summary, and one or two explanatory notes about major funds or major spending categories.

A short annual meeting presentation can help. So can a written report that explains not only the numbers but also what ministry those numbers supported.

- Use plain language: Replace accounting jargon with terms members already understand.

- Show designated funds separately: That's often the area people care about most.

- Explain unusual items: A large repair bill or timing shift in giving can look alarming without context.

- Invite appropriate questions: Members don't need unlimited access to everything, but they should know the church welcomes honest inquiry.

A practical system gives leaders confidence. It also lowers the emotional charge around money because everyone knows what will be shared, when, and how.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Frequently Asked Questions About Church Finances

Do churches have to disclose financial information to members?

Start with the distinction that trips up many church boards. A church can be legally permitted to keep certain financial details private and still decide that sharing clear reports is the wiser course.

In general, churches are not subject to a broad federal rule that requires them to give members full financial disclosure. As noted earlier, questions about member access to financial records are often shaped by state law, bylaws, and the church's own governance documents. That means the key question for many leaders is not only, “What are we required to disclose?” but also, “What level of disclosure helps our church stay trusted and well governed?”

Does that mean a church should keep finances private?

Privacy and secrecy are not the same thing.

A healthy church usually protects confidential details, such as individual donor information or sensitive personnel matters, while still sharing enough financial information for members to see how resources are being received, budgeted, and used. Good stewardship works like a window with curtains. You do not throw everything open, but you do let in enough light for people to see that things are being handled properly.

Do pastor salaries have to be shared with the whole church?

Churches handle this differently, and the right answer often depends on governance structure, church culture, and the size of the staff.

Some congregations share compensation in broad categories through an annual report. Others reserve salary detail for the board, elders, or a compensation committee. The important part is consistency. A written policy helps leaders explain why some information is shared widely and why some is reviewed by a smaller group with oversight responsibility.

Is a small church treated differently?

The pressure points are different, but the stewardship standard is the same.

In a small church, people often assume trust can replace process because everyone knows everyone. That is where confusion starts. If one volunteer tracks designated gifts in a notebook, another person reconciles the bank account, and no one can explain the youth fund balance clearly, relationships carry a weight they were never meant to carry. Simple records and simple reports still matter, even when the budget is modest.

If churches don't file Form 990, are donations still tax-deductible?

Usually, yes. A church's exemption from filing Form 990 is separate from whether contributions qualify as tax-deductible charitable gifts under the usual rules.

That said, the absence of a public filing is one reason voluntary transparency matters so much for churches. Other nonprofits often build public trust through Form 990 disclosure. Churches usually need to build that trust through their own reporting habits.

What's the biggest mistake churches make on this issue?

Churches usually get into trouble in one of two ways. They either share too little, which invites suspicion, or they share a pile of raw numbers without explanation, which invites misunderstanding.

Useful transparency answers ordinary questions before they become tense questions. Why did facilities spending jump this year? How much of the missions fund has been used? Did a large designated gift stay in that fund? Clear reporting gives those answers in plain language.

When should a church tighten its reporting process?

As soon as financial reporting feels harder than it should.

If leaders struggle to produce fund balances, if designated gifts are tracked outside the accounting system, or if board meetings keep circling back to the same money questions, the process needs attention. Those are early warning lights on the dashboard. They do not always mean wrongdoing, but they do mean the church needs better visibility.

If your church wants clearer fund-level reporting and a cleaner way to support voluntary transparency, take a look at Grain. It's purpose-built for church accounting, with native fund-based architecture that helps finance teams track restricted gifts accurately, organize reports around real ministry funds, and communicate stewardship with more confidence.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.