Endowment Fund Accounting for Churches: A Practical Guide

Master endowment fund accounting for your church. This guide explains fund classification, reporting, journal entries, and how to ensure proper stewardship.

A member passes away. A few weeks later, the church receives a letter from the estate attorney. The gift is generous, but it comes with a condition: the money is to be invested, preserved, and used to support ministry over the long term.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

That's the moment many treasurers feel the ground shift a little.

Regular church bookkeeping already asks a lot. You're tracking designated gifts, watching cash flow, answering board questions, and trying to keep reports understandable for people who don't speak accounting. An endowment adds a different kind of responsibility. It's not just about recording a donation. It's about honoring a promise.

Churches often approach this with good intentions and weak systems. The funds get parked in an investment account, a spreadsheet starts circulating, and everyone assumes they'll sort out the details at year-end. That approach usually creates confusion. The bigger issue is that endowment fund accounting isn't ordinary savings-account accounting. The church has to separate what must be preserved from what may eventually be spent.

Done well, an endowment can support ministry for generations. Done casually, it becomes a source of tension between the finance committee, the board, donors, and future leaders.

A Gift for Generations The Role of Church Endowments

A church endowment usually starts with a story, not a policy manual.

It may be a retired teacher who wants to fund seminary training for future pastors. It may be a family who wants their parents' legacy tied to missions, mercy ministry, or scholarships. It may be a longtime member who believes the church should have a stable source of support long after current leaders are gone.

That kind of gift changes the conversation. The church is no longer asking only, “How do we use this?” It's asking, “How do we protect this, document it, and use it faithfully over time?”

Legacy gifts need operating discipline

Many churches think of an endowment as an investment topic. It's really a stewardship topic first.

The donor usually isn't trying to solve this year's budget gap. They're trying to create continuity. They want the church to receive fruit from the gift without consuming the gift itself. That means the treasurer, the finance committee, and the board need to treat the endowment as a distinct ministry resource with its own rules.

Practical rule: If the donor intended a gift to serve future ministry over time, don't book it and manage it like a general donation.

This is why church leaders often benefit from looking at examples of long-horizon giving in ministry settings. The Bible Seminary's piece on lasting impact scholarships captures the basic heart behind this kind of generosity. The accounting details differ from church to church, but the stewardship principle is the same. A legacy gift is meant to keep serving after the original giver is gone.

The burden and blessing of restricted generosity

A new treasurer often worries about making a mistake. That's a healthy instinct.

An endowment creates legal, ethical, and reporting obligations that ordinary designated gifts may not. If the church accepts the gift, it accepts the duty to manage it according to the donor's instructions and according to the church's own policies. That means board minutes matter. Gift language matters. Investment statements matter. So does the accounting system.

The good news is that endowment fund accounting becomes manageable once the church separates three things clearly:

- What must stay intact

- What the investment earns

- What the church is allowed to spend

When those lines are blurry, every report becomes an argument. When those lines are clear, the endowment becomes what it was meant to be: a lasting support for ministry, not a bookkeeping burden.

What Is an Endowment Fund in the Church Context

The simplest way to explain an endowment is to think of an apple tree.

You don't chop down the tree and burn it for one cold night. You care for the tree so it keeps producing fruit season after season. In endowment fund accounting, the principal is the tree. The earnings are the fruit. The church preserves the principal and uses the earnings according to the donor's instructions or the board's designation.

That's why an endowment isn't just a savings account with a nicer name. A savings account is money sitting aside. An endowment is money held with purpose, restrictions, and a long horizon.

Separate fund means separate accountability

In nonprofit fund accounting, endowment funds are recorded as separate funds where the principal is tracked independently from spendable income. The same guidance notes three core categories, true endowment, term endowment, and quasi-endowment, and explains that this separation helps preserve donor intent and show which amounts are permanently held versus available for spending in the balance sheet, as described in the University of Texas System endowment training materials.

That principle matters for churches even if the church is small and the gift is held in one brokerage account.

The investment account is not the accounting structure. You can hold several different endowment-related balances inside one investment account, but your books still need to show what belongs to principal, what belongs to accumulated earnings, and what has been approved for use.

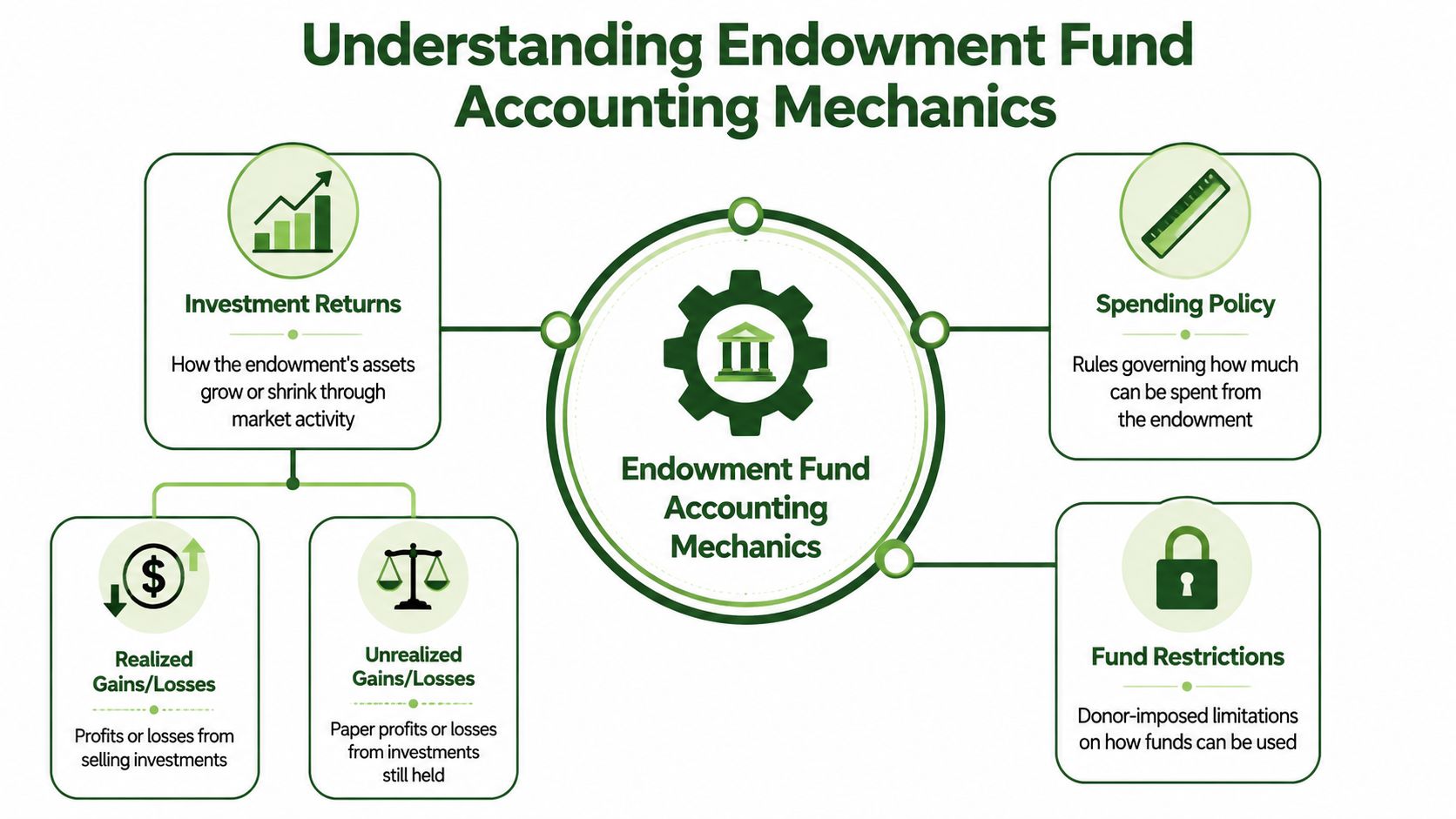

What an endowment is not

Churches get into trouble when they call every long-term fund an endowment. Some funds are reserves. Some are building funds. Some are board-designated savings with no donor restriction at all.

A true endowment has a preservation expectation tied to donor intent. That's the feature that changes the accounting.

Here's a simple way to tell them apart:

- Operating reserve: Set aside for stability, but generally available if leadership chooses to use it.

- Capital fund: Meant for a project such as renovation, expansion, or equipment.

- Endowment: Structured so the church preserves the principal and uses income or approved distributions over time.

A church doesn't create clarity by naming an account “endowment.” It creates clarity by documenting the restriction and tracking it correctly.

The church context makes this more personal

In a business, managers often think in terms of return and liquidity. In a church, leaders also think in terms of memory, trust, and witness.

The family that gave the money may still be in the pews. The ministry named in the gift may still be active. The congregation may assume the church is handling the fund carefully, even if no one has ever explained the accounting.

That's why endowment fund accounting needs to be understandable to non-accountants. If the treasurer can't explain the structure in plain language, the church probably isn't ready to manage it well.

Classifying Funds Permanent Term and Quasi Endowments

Classification is where many churches either prevent future confusion or create it.

When a gift arrives, the first question isn't which investment manager to use. The first question is, “What kind of fund is this?” The answer depends on who imposed the restriction and whether the principal can ever be spent.

A board should settle that question at the beginning, in writing. If the gift letter is vague, the church should clarify it before treating the money as an endowment.

Comparison of Endowment Fund Types

| Fund Type | Restriction Source | Principal Status | Flexibility |

|---|---|---|---|

| True endowment | Donor | Preserved | Lowest flexibility |

| Term endowment | Donor | Preserved until the stated time or event | Limited flexibility |

| Quasi-endowment | Board | Set aside by church decision | Highest flexibility |

How these categories work in practice

A true endowment is the clearest case. The donor gives the money and requires the church to hold the principal. The church can usually spend only what its policy permits from earnings or approved distributions.

A term endowment also starts with donor intent, but the restriction has an endpoint. The principal may become spendable after a stated time or once a specific event happens. Until then, the church still has to track it separately.

A quasi-endowment is different. The board decides to treat certain funds like an endowment, even though the donor didn't require it. That can be wise. It can also be reversed by the board because the restriction came from the church, not the donor.

This distinction matters more than many churches realize. If the board treats a donor-restricted fund like a board-designated reserve, it may spend money it was never free to spend. If it treats a quasi-endowment like a permanent donor restriction, it may unnecessarily tie up resources the church could lawfully redirect.

Donor paperwork drives the accounting

Most classification problems begin upstream. A vague bequest, an informal conversation, or a poorly written acknowledgment letter leaves the treasurer trying to infer intent after the fact.

That's why churches should adopt clear gift review practices before they receive complex assets or restricted legacy gifts. A practical starting point is a nonprofit-oriented donor acceptance policy guide that shows how organizations think through gift terms before the funds create accounting problems.

If the restriction isn't clear on the front end, the accounting will become guesswork on the back end.

For a new treasurer, the takeaway is simple. Never classify an endowment based on assumption. Classify it based on the donor document, board action, and the actual legal and practical limits on the principal.

The Mechanics of Endowment Fund Accounting

Once the fund is classified correctly, the daily work starts, and endowment fund accounting transitions from being theoretical to operational.

The central accounting distinction is between the corpus, meaning the donated principal, and the earnings or spending fund. Guidance from the University of Alabama materials explains that systems must track book value and fair market value separately to determine whether a fund is underwater. If market value drops below book value, the fund becomes underwater, and management may need to restrict or suspend distributions to protect the principal, as outlined in the endowment accounting training manual.

What the treasurer actually tracks

In real church workflow, you usually need to watch at least four moving parts:

- Original gift amount so you know the preserved principal or book value

- Current market value so you know the fund's present investment value

- Investment activity including income, gains, losses, and fees

- Approved spending transfers so ministry use doesn't get mixed with principal

This is why a single balance in a brokerage statement is never enough.

A church can have an investment account showing one total market balance while the accounting records need to reflect several internal realities. One portion may be permanently held. Another portion may represent accumulated appreciation. Another may already be appropriated for spending but not yet transferred to operations.

Why underwater status matters

An underwater endowment exists when market value falls below the preserved principal amount. That creates both a reporting issue and a governance issue.

If the church keeps distributing funds as if nothing changed, it may be eroding the donor's intended long-term support. If it freezes everything without reviewing policy and legal requirements, it may overreact. The treasurer's role is to bring the board accurate fund-level information so decisions are based on facts, not fear.

A board can't make a prudent spending decision if the reports only show one blended investment balance.

Spending policy needs more than tradition

Many churches follow an informal rule such as “spend the income” or “take a portion each year.” Informal rules break down when markets are volatile or when the endowment includes multiple restrictions.

A written spending policy helps leaders answer questions like these:

- Is spending calculated from income only, or from a broader total-return approach?

- Who approves the annual distribution?

- What happens if a fund is underwater?

- Can distributions be reduced or paused to protect principal?

Churches often hear about UPMIFA in this context. In plain language, the prudence standard asks leaders to make spending decisions carefully, in light of donor intent, the fund's purpose, and the church's long-term responsibilities. Treasurers don't need to become attorneys, but they do need records and reports strong enough for the board to act prudently.

Pooled investments add another layer

Some churches or affiliated foundations pool endowment assets for investment. That can simplify portfolio management, but it increases the need for sub-fund tracking.

If multiple funds share the same pool, the church must still know what belongs to each fund. Earnings and market changes have to be allocated in a way that keeps each endowment's activity distinct. Consequently, spreadsheet-driven bookkeeping often starts to crack. The math may look fine in total while individual fund history becomes hard to reconstruct.

Reporting and Disclosures for Congregational Trust

Good endowment accounting does more than keep auditors calm. It helps church leaders tell the truth clearly.

Board members need more than a brokerage statement. Congregations need more than a vague note that “the endowment is doing well.” The right reports show how the fund changed during the year and whether the church managed it consistently with donor intent and board policy.

The roll forward is the report that matters most

Modern nonprofit guidance says endowment reporting should include a roll forward of beginning and ending balances, plus contributions, investment returns, and appropriations. It also requires disclosure of underwater endowments, including the number of funds, their aggregate original gift amounts, and their current fair values, as described in this guide to endowment accounting for nonprofit finance teams.

For a church board, that means the endowment report should not be a single ending balance. It should show movement.

A useful board-facing roll forward usually includes:

- Beginning balance for each endowment fund or major grouping

- New gifts or additions received during the period

- Investment return activity recorded during the period

- Appropriations or transfers approved for ministry use

- Ending balance with enough detail to distinguish principal from available spending amounts

Reports should answer actual governance questions

Church leaders usually ask practical questions, not accounting textbook questions.

Can we spend from this fund this year? Did we preserve the donor's gift? Has the board already designated part of the return for scholarships or benevolence? Is any fund underwater? Those questions should be answerable from the reporting package without the treasurer building a custom spreadsheet the night before the meeting.

A clear set of church financial reports makes this easier. Grain's overview of church financial reports is a helpful reference for thinking about how internal reporting should support board oversight, not just year-end compliance.

Transparency builds trust when reports show both what the church has and what the church is allowed to do with it.

Don't hide important details in committee memory

Churches often rely on oral history. Someone on the finance committee remembers why a fund was created, how distributions were calculated, or why spending was paused three years ago.

That memory is not a control system.

At minimum, the church should maintain written disclosure support for:

| Reporting Item | Why It Matters |

|---|---|

| Spending policy | Shows how leadership decides what may be used |

| Restriction summary | Clarifies donor intent and board designations |

| Underwater review | Flags funds needing caution or reduced distributions |

| Endowment activity support | Connects beginning balances to ending balances |

When a church documents these items consistently, the congregation sees faithful stewardship instead of mystery.

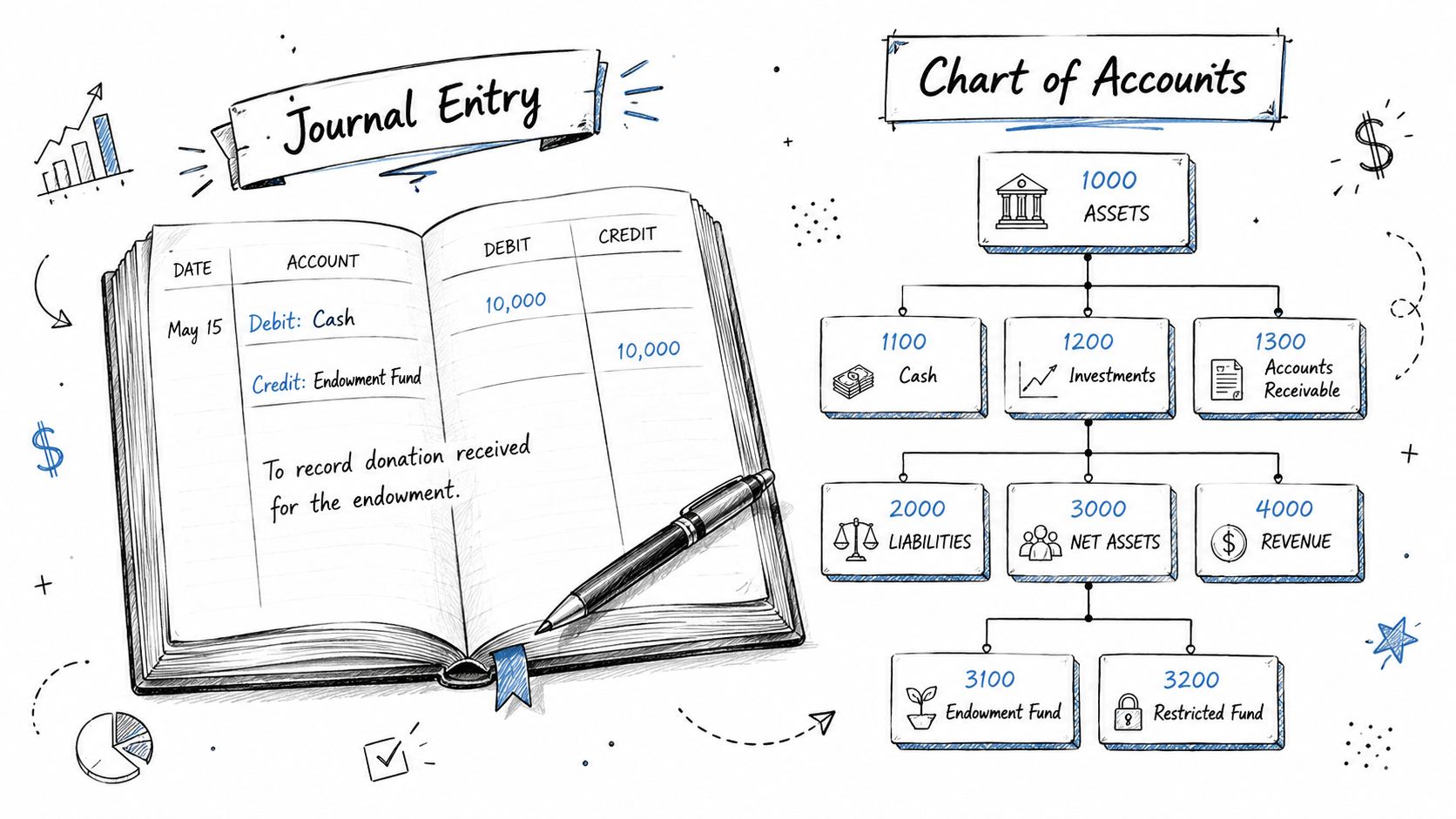

Sample Journal Entries and Chart of Accounts Setup

Most treasurers don't struggle because the ideas are too hard. They struggle because they need to know what to post.

The journal entries below are simplified examples. A church's auditor or accountant may adapt the exact account titles, but the workflow stays similar. The point is to keep the principal, investment activity, and operating use from blending together.

A workable chart of accounts structure

A small-to-medium church usually needs a chart of accounts that can separate fund activity cleanly. If your current setup is too flat or too business-like, it helps to review a church-specific nonprofit chart of accounts for churches before adding endowment accounts.

A practical setup often includes accounts such as:

- Cash or investments held for endowment

- Endowment principal or corpus

- Accumulated endowment earnings

- Investment income

- Realized gains and losses

- Unrealized gains and losses

- Board-approved appropriations to operations

- Net assets with donor restrictions

- Net assets without donor restrictions for quasi-endowment activity, if applicable

Sample entries through the lifecycle

1. Record the original endowed gift

If the church receives cash for a donor-restricted permanent endowment:

- Debit cash or investments

- Credit contribution revenue with donor restriction, then classify within the appropriate restricted net asset structure used by your church and reporting framework

The key is not the exact label. The key is that the principal is not treated like ordinary giving income available for immediate ministry spending.

2. Record investment income or gains

As the investment account earns income or changes in value, the church records that activity to the endowment-related accounts rather than mixing it into the general operating fund.

For example:

- Debit investments or cash

- Credit investment income, realized gain, or unrealized gain as appropriate

If there is a loss, the direction reverses. The important thing is that the activity stays tied to the endowment fund.

Here's a short walkthrough that may help if you're training a volunteer bookkeeper or finance committee member:

3. Record an approved appropriation for spending

When the board approves an amount for ministry use, don't post the ministry expense directly against the endowment principal. First, move the approved amount into a spendable operating context according to the church's accounting framework.

That usually looks like:

- Debit endowment earnings or a released/appropriated balance

- Credit transfer or release account into the receiving operating fund

This step matters because approval to spend is not the same as the actual ministry expense.

4. Record the ministry expense when paid

Once the operating fund uses the money for the intended purpose, record the expense in that fund like any other ministry expense.

That keeps the audit trail clean. Anyone reviewing the books can see the gift, the investment activity, the board-approved appropriation, and the final use.

Keep the endowment transaction trail visible. Don't bury distributions inside miscellaneous journal entries at year-end.

Compare platforms in our best church accounting software guide for 2026, or review Grain Ledger church accounting software.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Choosing the Right Software for True Fund Accounting

The most common system failure in church endowment accounting is simple. Churches try to manage restricted long-term funds in tools that weren't built for fund accounting.

A spreadsheet can track balances for a while. Generic small-business software can produce a profit-and-loss statement. Neither one automatically understands donor restrictions, fund-level balances, or the difference between preserved principal and spendable earnings. That's where mistakes happen.

What generic tools usually miss

A major challenge in endowment management is that underwater status must be determined for each individual fund, not just at the aggregate portfolio level. Guidance on underwater endowments also warns that aggregate gains can hide problems inside individual sub-funds, leaving a seemingly healthy endowment with real governance and spending-policy issues, as explained in this underwater endowment disclosure resource.

That's a serious issue for churches.

If the software only shows one investment total, the treasurer may miss that one scholarship fund is underwater while another fund is healthy. The board may approve distributions based on a blended picture that hides the actual restriction problem.

What to look for in a church system

A church needs software that can do more than categorize transactions. It needs to preserve fund structure in the ledger itself.

Look for a system that supports:

- Fund-based accounting at the core so restricted and unrestricted activity aren't simulated with workarounds

- Fund-level reporting so the board can review each endowment separately

- Clear movement between funds when appropriations are approved and spent

- Visibility into principal and earnings without relying on shadow spreadsheets

- Church-specific reporting workflows that make sense to pastors, treasurers, and finance committees

When churches ask what software to consider, I recommend starting with tools built for church fund accounting rather than retrofitting business accounting software. One option is Grain's guide to finding the best fund accounting software for your church. For churches that need native fund architecture, Grain is the accounting solution I'd point to because it organizes transactions and reports around funds from the start, which fits the realities of endowment oversight in small and medium congregations.

The right software won't make policy decisions for the board. It will do something just as important. It will make those decisions visible, traceable, and much harder to mishandle.

If your church is trying to manage restricted gifts, designated funds, and long-term endowment balances with spreadsheets or business software, Grain is worth a serious look. It's built around true fund accounting for churches, which makes it easier to separate principal from spendable funds, keep restricted dollars restricted, and produce reports your board can use effectively.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.