Fund Accounting Basics for Churches: 2026 Guide

Master fund accounting basics for your church in 2026. Our guide covers restricted funds and reporting tools to ensure transparent ministry stewardship.

A lot of church finance trouble starts with a good intention.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

Someone gives a special gift for the building project. Another family gives toward youth camp. A few members mark their offering envelopes for missions. The treasurer opens the spreadsheet, adds a new column, and thinks, “I'll keep track of it there.”

That works for a little while. Then payroll is due, the utility bill clears, and the checking account balance looks healthy. But part of that cash isn't really available for general expenses. It belongs to a purpose the donor named. Now the finance committee is asking one question, and the congregation is asking another: do we know, with confidence, where that money is and what it can be used for?

That's where fund accounting basics matter for churches. This isn't just bookkeeping language. It's a stewardship framework that helps a church protect donor intent, report clearly, and make ministry decisions without guessing.

Why Your Church Needs More Than a Spreadsheet

A spreadsheet can track numbers. It can't, by itself, create clarity.

I've seen this happen in churches more than once. A member gives a significant gift for a future building update. The church deposits it into the same bank account used for weekly offerings, staff pay, and routine bills. The treasurer adds a note on the spreadsheet and moves on. A month later, a furnace repair hits at the same time giving is lower than expected, and someone says, “We have cash in the bank. Why not use that for now and replace it later?”

That sentence is where confusion turns into risk.

The problem isn't bad intent. The problem is that a simple spreadsheet often mixes two different questions. One is, how much cash does the church have? The other is, how much of that cash is available for general use? In a church, those are not always the same thing.

Stewardship means more than balancing the checkbook

Churches carry a special trust. People give because they believe the church will handle those gifts carefully and with integrity. If a donor marks a gift for benevolence, missions, or a building fund, the church needs a way to show that money stayed in that lane.

Good stewardship isn't only about recording donations. It's about proving that each gift was handled the way the church said it would be handled.

That's why churches need more than a running total and a few color-coded tabs. They need a system that separates money by purpose, not just by date or expense category.

Spreadsheets usually break at the same pressure points

A spreadsheet setup tends to struggle when churches need to answer practical questions like these:

- Payroll question: Is the bank balance enough to cover staff compensation, or is part of that balance committed to a restricted gift?

- Board question: Can we show the elders what remains in the missions fund right now?

- Donor question: Can we demonstrate that a designated gift was used only for the stated purpose?

- Month-end question: Can we produce clean reports without chasing formulas and side notes?

A church can operate for a while without fund accounting. But as soon as designated giving becomes a real part of ministry life, the church needs a better structure.

Understanding the Core Concepts of Fund Accounting

The easiest way to understand fund accounting is to stop thinking first about software and start thinking about buckets.

If your church had one large table and several labeled offering baskets on it, you would immediately understand the idea. One basket might say General Fund. Another might say Missions. Another might say Building. The church may deposit all the money into one bank account later, but the purpose attached to each gift doesn't disappear just because the bills and coins end up in the same place.

That is the heart of fund accounting.

What a fund actually is

A fund is not the same thing as an expense account like utilities or office supplies.

A fund is a separate financial bucket used to track resources by purpose and restriction. In formal fund accounting, each fund operates as a self-balancing set of accounts with its own revenues, expenditures, assets, liabilities, and fund balance, as explained in this fund accounting overview from NDCCA.

Simple definition: A fund answers, “What is this money for?”

An account answers, “What kind of transaction is this?”

So if the church buys curriculum for the youth ministry, the expense account might be curriculum or ministry supplies. The fund might be Youth Ministry or General Fund, depending on how that purchase is supported.

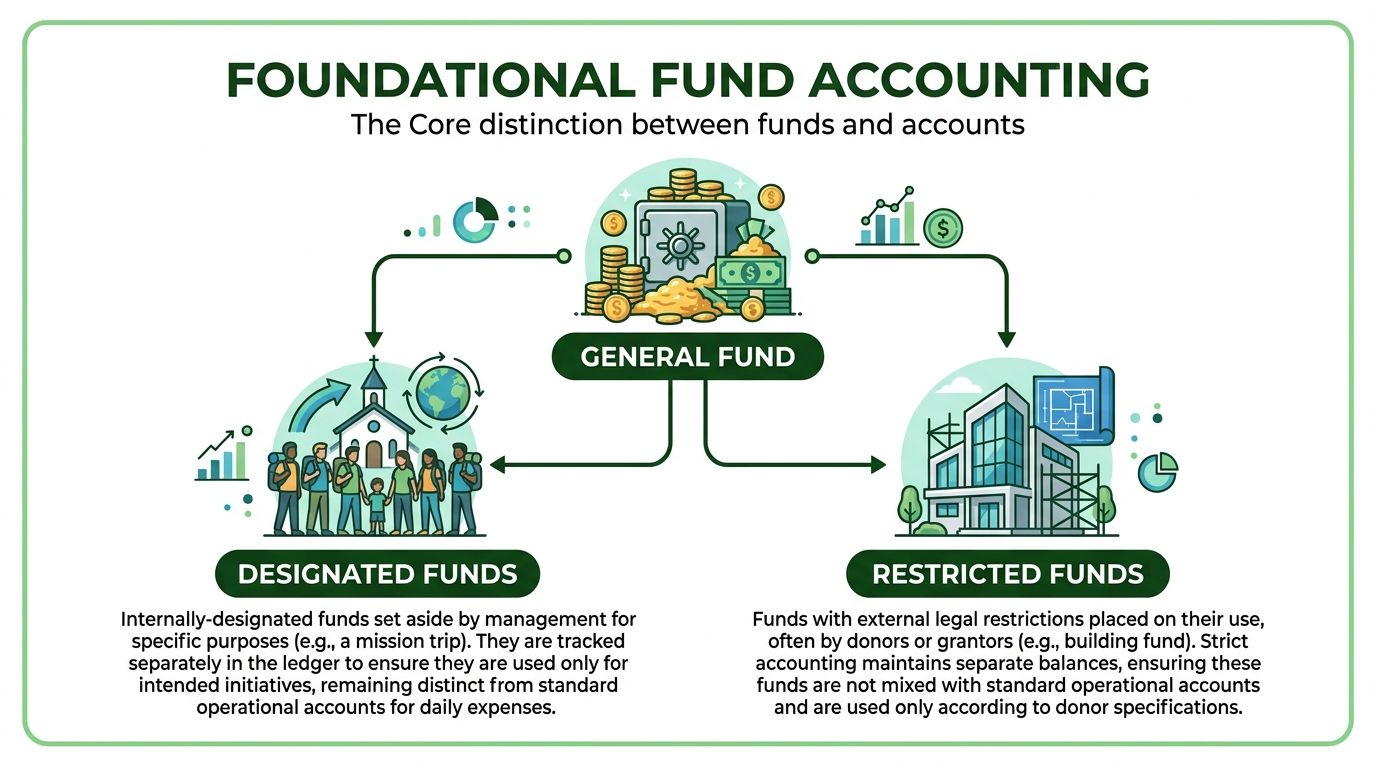

Restricted and unrestricted money

Most confusion in church finance happens right here.

Unrestricted funds can be used at the church's discretion for normal ministry and operations. This is often your General Fund. It supports things like staff costs, utilities, ministry materials, and routine facility expenses.

Restricted funds are limited by donor or grantor intent. If someone gives specifically for a mission trip, building project, or benevolence effort, that money should be tracked and used for that purpose.

The source above notes that fund accounting for tax-exempt organizations was formalized through GASB 34, which established three primary groups of funds used to prepare financial statements: Governmental, Proprietary, and Fiduciary funds. For churches, the practical takeaway is simpler. Resources must be segregated based on source and restrictions, and that separation helps prevent accidental commingling with operating money.

If a member gives to the building fund, that gift doesn't become available for copier toner or Sunday coffee just because it was deposited into the same checking account.

A church example

Think of one church checking account like a kitchen pantry. Inside it are separate containers labeled for different uses.

- General Fund covers ordinary church operations.

- Missions Fund holds money designated for outreach or missionaries.

- Building Fund tracks gifts for renovations or construction.

- Benevolence Fund holds resources for member care and community help.

The pantry is one location. The containers inside it still matter.

Why churches get tripped up

People often assume fund accounting means opening a separate bank account for every purpose. It doesn't.

Another common mistake is treating funds like memo labels. Real fund accounting is more than adding a note or class to a transaction after the fact. It's a structured way of recording, tracking, and reporting resources by purpose from the beginning.

Once that clicks, the rest of fund accounting basics starts to feel much more manageable.

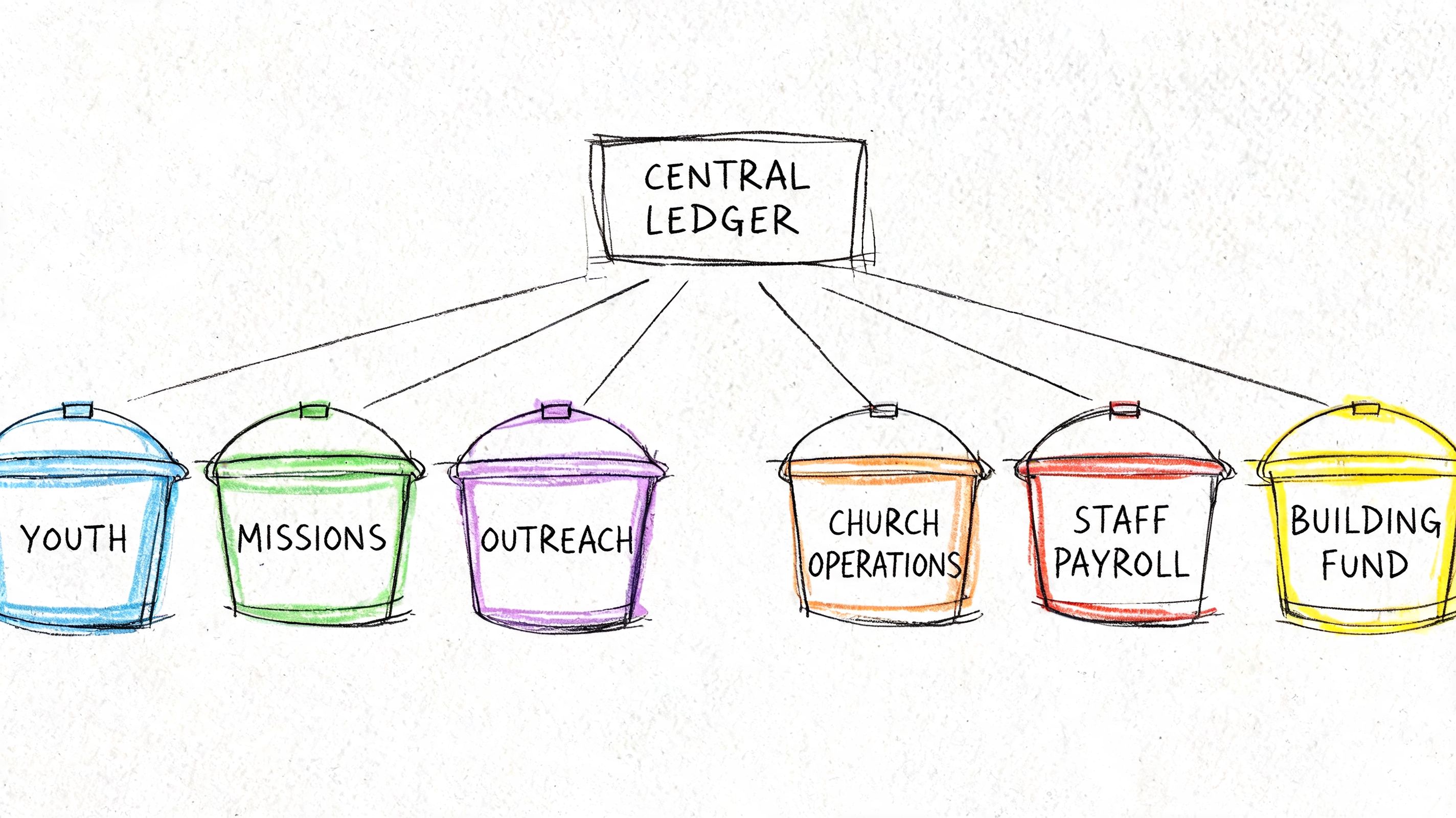

How to Set Up Your Church's Chart of Funds

When churches first hear “chart of funds,” they often picture something technical and intimidating. It's usually much simpler than that.

A chart of funds is just the master list of your church's financial buckets. It works alongside your chart of accounts. The chart of accounts lists transaction types such as tithes, salaries, rent, maintenance, and supplies. The chart of funds lists where those transactions belong from a stewardship standpoint.

Chart of funds versus chart of accounts

A healthy setup uses both.

The operational strength of fund accounting is that churches can use one consolidated chart of accounts across all funds. With a fund segment in the accounting system, each transaction can be recorded against a specific fund without opening separate bank accounts or living in spreadsheets, as described in Foundant's explanation of nonprofit fund accounting practices.

Here's a simple way to separate the two ideas:

| Item | Purpose | Example |

|---|---|---|

| Chart of Accounts | Tracks transaction type | Utilities, Salaries, Offerings, Repairs |

| Chart of Funds | Tracks purpose or restriction | General, Missions, Building, Benevolence |

If you want a deeper look at the account side of the structure, this guide to a nonprofit chart of accounts helps connect the pieces.

Common Church Fund Types

Most churches don't need dozens of funds. Start with the ones that reflect real ministry activity and real donor intent.

| Fund Name | Typical Purpose | Classification |

|---|---|---|

| General Fund | Day-to-day ministry and operating expenses | Unrestricted |

| Building Fund | Construction, renovation, major facility updates | Restricted |

| Missions Fund | Missionaries, mission trips, outreach support | Restricted |

| Benevolence Fund | Assistance for members or community needs | Restricted |

| Youth Ministry Fund | Youth events, camps, supplies, discipleship activities | Often restricted or designated |

A practical way to build your list

Don't begin with accounting theory. Begin with the questions your church regularly needs to answer.

Start with your recurring ministry lanes

Look at the gifts your church receives and the programs people commonly support.

For many churches, that means identifying a handful of clear funds such as:

- General operations: Weekly tithes and offerings used for normal ministry activity.

- Capital needs: Building improvements, renovation campaigns, equipment replacements.

- Outreach work: Local missions, global partners, special ministry projects.

- Care ministries: Benevolence and emergency assistance.

- Student and children's ministries: Events, retreats, camp scholarships, curriculum.

Keep the list useful, not bloated

Some churches create too many funds too quickly. Then no one remembers the difference between similar labels.

Practical rule: If a fund doesn't reflect a real restriction, a standing leadership decision, or a reporting need, it probably doesn't need to be a separate fund.

A clean chart of funds should help the treasurer, the pastor, and the finance committee answer real questions fast. If it only makes sense to the person who built the spreadsheet, it needs work.

Tracking Transactions and Generating Reports

Fund accounting starts to make sense when you watch one transaction move through the system.

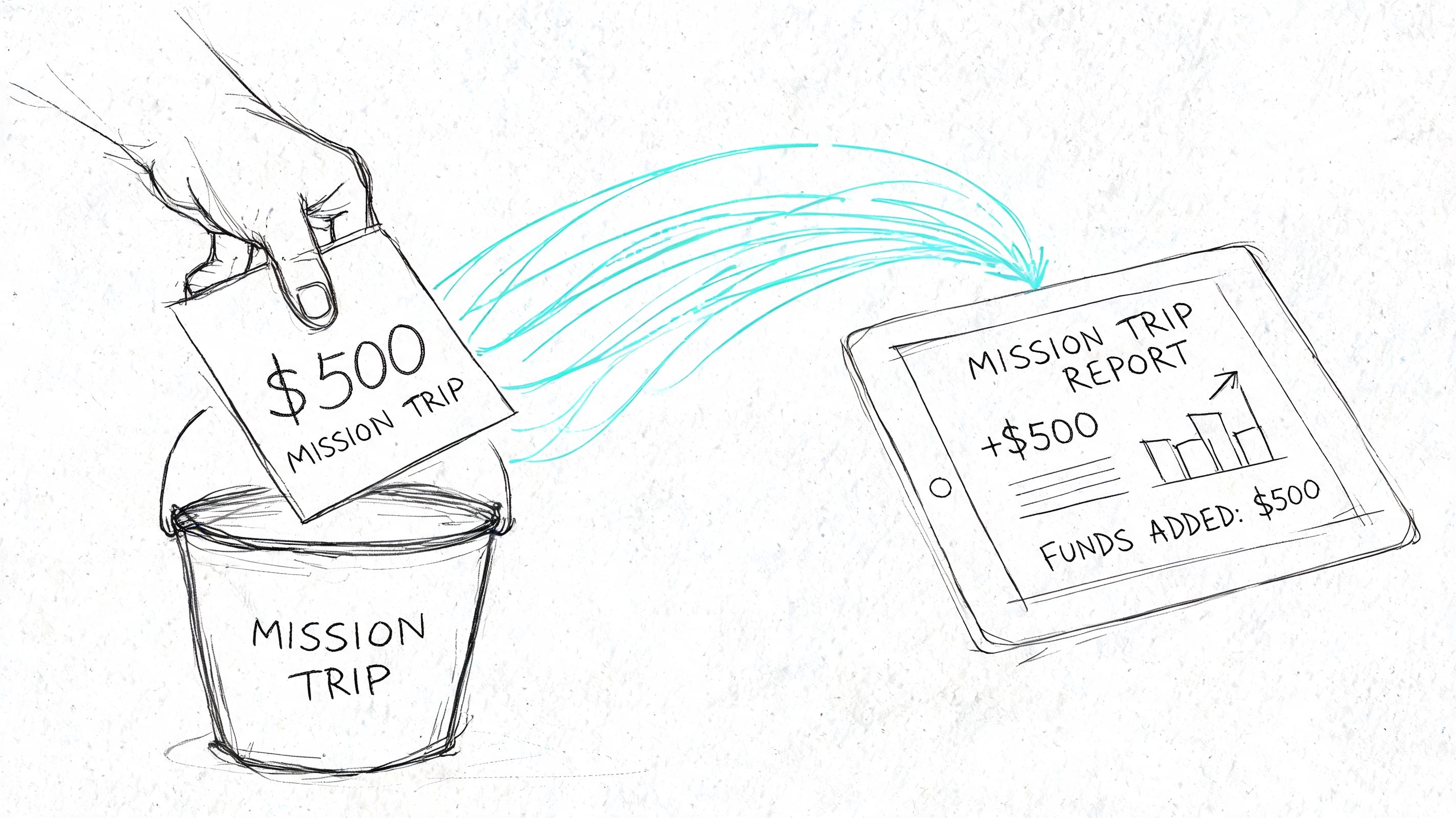

Say a church member gives $500 designated for the summer mission trip. That gift should be recorded to the Missions Fund, not the General Fund. The money may land in the same bank account as Sunday's regular offering, but the church should still treat it as mission-trip money, not utility-bill money.

What happens when the gift is recorded

The key moment is the original posting. A strong fund accounting process assigns the transaction to the correct fund immediately.

That means the donation increases the Missions Fund balance. It does not increase the amount available for general church operations, even though total cash on hand also rises.

Later, if the church pays for airfare, lodging, or trip materials related to that mission effort, those expenses should also post to the Missions Fund. Then the reports will show the full story. What came in, what went out, and what remains.

The reports your church should expect

A church using fund accounting should be able to produce clear fund-based reports, not just one blended income statement.

Here are the reports most finance teams care about:

- Statement of Financial Position: Shows assets, liabilities, and net assets by fund, helping leaders see what is held for each purpose.

- Statement of Activities: Shows changes in fund balances over time, including revenue and expenses within each fund.

- Fund-level cash visibility: Helps leaders understand where cash is sitting and which portions are available for use.

A helpful benchmark is whether your system can automatically generate fund-specific financial statements and separate restricted and unrestricted activity clearly. Guidance from Xero's fund accounting overview also emphasizes that transaction classification at posting time is essential because errors flow into both compliance and cash planning.

Why month-end gets easier

Without fund accounting, churches often do cleanup work at month-end. Someone exports giving data, compares it to the bank feed, adjusts manual reports, and tries to remember which expenses belonged where.

With proper fund tracking, the monthly reporting conversation gets simpler. The board can ask, “How much remains in missions?” or “Did we spend from benevolence as intended?” and the reports can answer directly.

This short walkthrough gives a useful visual explanation of how the flow works in practice:

When the postings are right on the front end, the reports become much more trustworthy on the back end.

Avoiding Common Pitfalls with Internal Controls

Most church finance mistakes don't begin with dishonesty. They begin with pressure.

Offerings run low for a month. A repair bill comes in early. Payroll is close. Someone notices money sitting in a designated fund and suggests using it temporarily. The intention may be to replace it later, but that decision creates a stewardship problem immediately.

Where churches usually get into trouble

A few patterns show up over and over:

- Borrowing from restricted funds: Using building, missions, or benevolence money to cover general expenses.

- Losing the restriction trail: A donor's intent is remembered by one person, then forgotten after leadership changes.

- Reporting only totals: Leaders see one cash number but not which portions are unavailable.

- Relying on after-the-fact cleanup: Staff or volunteers recode transactions later, increasing the chance of error.

Those aren't just process issues. They affect trust.

A church may have enough cash in the bank and still be short on money it can actually spend.

Internal controls protect people and ministry

Fund accounting is one of the most important controls a church can maintain. According to Texas State's fund accounting guidance, fund accounting is a control system. Each fund is self-balancing, and the accounting equation must reconcile within that fund, not only across the church as a whole. That structure is what proves donor-designated money was used only for its intended purpose.

For a church finance committee, that means controls should do more than prevent fraud. They should also prevent innocent mistakes.

Healthy controls a church can put in place

Some of the strongest safeguards are simple and repeatable:

Approve fund creation carefully

Don't create a new fund every time someone has an idea. Define when a fund is needed and who approves it.Code gifts at the time they are received

The closer classification happens to the donation itself, the less cleanup you'll face later.Review fund balances regularly

Finance teams should look at fund reports, not just the combined checking balance.Make reports easy to read

Good visuals help non-accountants understand restricted and unrestricted activity. If your board packets need clearer presentation, this guide on choosing charts and using color is useful for turning raw finance data into readable dashboards.Document your procedures

Written workflows matter, especially when volunteers rotate. This overview of internal control practices for church finance teams is a practical starting point.

Churches don't need complicated bureaucracy. They need a few reliable guardrails that keep donor intent clear and keep the congregation's trust intact.

Compare platforms in our best church accounting software guide for 2026, or review Grain Ledger church accounting software.

Related fund stewardship resources

These guides help churches connect designated funds, policies, approvals, and financial reporting.

- Church benevolence fund guide - set policy, approvals, and accounting controls

- Restricted fund guide - understand donor restrictions and fund balances

- Fund accounting in Grain Ledger - track designated gifts and ministry funds in the ledger

- Schedule a Grain Ledger demo - see fund-level reports and bank reconciliation

Implementing True Fund Accounting with the Right Software

Many churches hit a wall at this point. They understand the principles, but their tools weren't built for them.

Generic business accounting software can record income and expenses. It often struggles when a church needs native fund-level structure, clean reporting, and clear separation of restricted money. The result is usually a stack of workarounds: classes, tags, side spreadsheets, and month-end journal entries that only one person fully understands.

What to look for in a church accounting system

A church doesn't just need software that can store transactions. It needs software that handles fund accounting as a native part of the system.

One key benchmark is whether the platform can automatically generate fund-specific financial statements. It also needs solid integration with giving platforms and bank feeds, because for churches that isn't just a convenience. It's an internal-control requirement when restricted gifts need to flow directly into the correct fund and produce board-ready reports with less manual cleanup, as outlined in Xero's guide to fund accounting systems.

A practical checklist looks like this:

- Native fund structure: Funds are built into the ledger, not layered on afterward.

- Giving integration: Donations from tools such as Planning Center, Pushpay, or Stripe can be mapped into the right funds.

- Bank feed support: Transactions match against the ledger with less manual entry.

- Fund-based reporting: Leaders can run financial position, activity, and cash reports by fund.

- Restriction protection: The system supports separation of designated and general resources.

Why church-specific software matters

Churches face a different stewardship challenge than most small businesses. A business usually asks, “Did we make money?” A church asks, “Did we handle God's money faithfully, by purpose, with transparency?”

That's why purpose-built church systems are worth evaluating. If your team is comparing options, this guide to fund accounting software for churches and nonprofits can help frame the decision.

For teams that also work with outside bookkeepers or advisors, this article on finding an accounting firm for small business support may help you think through what kind of external help fits your church's situation, even though church finance has its own requirements.

One church-focused option to consider is Grain, which is built around a native fund architecture. It organizes transactions and reports by fund from the start and connects with common giving platforms and bank data so designated gifts can flow into the correct funds with less manual handling.

Software won't create stewardship by itself. But the right system makes faithful stewardship much easier to practice consistently.

If your church is outgrowing spreadsheets or patchwork accounting tools, Grain is worth a look. It's built for church fund accounting, with native fund-based structure, integrations for giving and banking, and reports that help pastors, boards, and finance teams see clearly what money is available and what money is restricted.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.