How to Prepare Financial Reports for Your Church

Learn how to prepare financial reports for your church. Master fund accounting, essential reports, and clear data presentation to your board.

If you're the person everyone asks after service, "Can you tell me whether that gift for youth camp was used for youth camp?" you already know the hardest part of church finance isn't printing a report. It's trusting the numbers before the report ever goes out.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

Most churches don't struggle because they lack goodwill. They struggle because the data lives in too many places. Part of it sits in the bank feed, part in the giving platform, part in a spreadsheet someone updates on Tuesdays, and part in the memory of the volunteer who counted the offering. Then the pastor, board, or donor asks a fair question that should have a simple answer, and the room gets quiet.

That's why learning how to prepare financial reports for a church isn't mainly about formatting a balance sheet. It's about building a trail from donation to deposit to fund to ministry use, then presenting that trail in a way non-accountants can understand.

The Stewardship Story Your Reports Should Tell

On Monday morning, the questions are rarely accounting questions. They sound like this: How much is left in the building fund? Did the youth camp gifts get used for youth camp? Why does the bank balance look healthy when the general fund feels tight? A useful church report answers those questions without forcing pastors, board members, or donors to decode accountant language.

A church report should show whether the church handled entrusted resources faithfully, by fund and by purpose. That story breaks down fast when the underlying records live in separate places. Giving sits in one system, deposits clear in the bank, expenses run through cards or reimbursements, and someone keeps a ministry spreadsheet on the side. If those records do not reconcile, the report may look polished and still fail the basic trust test.

Why church reporting is different

For-profit reporting usually centers on profit, growth, and cash. Church reporting starts with stewardship.

Leaders need to know:

- Whether donor intent was preserved

- Whether restricted and unrestricted resources were kept separate

- Whether each ministry area can see what it has used and what remains

- Whether the numbers can be explained in plain English

That last point gets overlooked. I have seen technically correct statements create confusion because they were organized for accountants rather than for ministry decisions. A pastor does not want to hunt through net asset categories to answer a donor's question about benevolence. A board member does not want to compare three disconnected reports to understand whether the missions fund is ahead or behind plan. Good reporting translates formal statements into fund-based explanations people can act on.

That translation starts with the structure of the books. A church-ready nonprofit chart of accounts makes it far easier to track activity by fund, ministry, and restriction before month-end questions pile up.

Churches lose trust faster from unclear fund use than from an ugly spreadsheet.

What a useful church report package includes

A practical reporting set usually includes four reports that work together:

- Statement of Financial Position for what the church owns, owes, and holds by net asset category.

- Statement of Activities for revenue and expenses over the reporting period.

- Statement of Cash Flows for liquidity and timing.

- Fund Activity Report for designated and restricted balances that leaders often ask about.

The fourth report often carries the most weight in board and donor conversations. It connects the accounting file to ministry reality. It shows whether the benevolence fund, building fund, missions fund, or general fund changed the way leaders expected, and whether those changes match what happened in the bank, the giving platform, and the ledger.

That is the stewardship story. Reconcile the records first. Then present the results in a fund-based narrative that answers real ministry questions.

Laying the Foundation with Fund-Aware Data

Monday morning, the pastor asks whether the building fund can cover the next contractor invoice. The giving platform shows one number, the bank shows another, and the accounting file has the deposit split three different ways. That is usually where church reporting starts to go wrong. Not at the reporting stage, but earlier, when data from giving, banking, cards, payroll, and the ledger has not been brought into one clean, fund-aware record.

Churches deal with this more often than many organizations because money enters through several channels and often carries a purpose. A general operations gift, a youth camp payment, and a donor-restricted missions contribution cannot be treated the same way just because they hit the bank in the same batch. Broader reporting guidance makes the same point. Data often comes from multiple systems that need to be reconciled before anyone can trust the final reports, as noted in this practical financial reporting guide.

Start with the Four C's

I use a simple test before I trust any church's numbers. The data must be Correct, Current, Complete, and Consistent. ACCA's work on financial reporting quality and control supports the same basic discipline, and this ACCA research and reporting resource is a useful reference point.

In church bookkeeping, those four checks are practical.

- Correct means the donor record, deposit, and ledger entry agree.

- Current means staff and volunteers are not posting last month's activity halfway through this month.

- Complete means every giving batch, bank fee, payroll draft, card charge, and reimbursement made it into the books.

- Consistent means the church uses one naming convention for funds and one coding rule for similar transactions.

A church can survive an ugly spreadsheet for a while. It cannot make good decisions from mismatched records.

Reconcile before you report

The monthly close should start with source documents and system exports, not with the board packet template. Pull the giving detail, bank activity, credit card statements, payroll reports, and ledger transactions. Then match them. If a giving platform nets processing fees, record the gross gift, the fee, and the net cash correctly. If one deposit includes several funds, split it before reporting. If reimbursements or transfers are sitting in suspense accounts, clear them first.

Practical rule: If the bank is unreconciled, the board report is still a draft.

This is the point many churches skip because the pressure to "get the reports out" feels more urgent than the cleanup work. I have seen that shortcut create the same pattern over and over. The finance committee debates ministry spending, but the underlying problem is that the cash total includes uncleared items, donor restrictions are tracked in notes, and one deposit was coded entirely to the general fund.

Standard report formats matter, and so does understanding how financial statements are supposed to function, which is why this expert guide to financial statements UAE can be a helpful outside reference for statement structure. For churches, though, the harder problem is usually upstream. The data has to be reconciled and assigned to the right fund before a statement means much.

Build a fund-aware chart from the start

A church chart of accounts should reflect both the nature of the transaction and the purpose attached to the money. If those two ideas get mixed together, reports become fragile fast. One person may know that "Missions Expense 2" really means a restricted short-term trips fund, but nobody else will.

A better setup uses a fund-aware chart of accounts for nonprofits as the starting point, then adapts it to the church's ministries and policies. The account tells you what happened. The fund tells you where the money belongs and what limits apply to it.

That structure solves two common reporting problems. It keeps salaries, benevolence, facilities, and program costs comparable across ministries. It also lets pastors and boards ask the questions they care about, such as whether the missions fund is being spent as intended or whether designated project balances are being used too early.

Choose tools that reduce split-source errors

Spreadsheets can handle a small church for a time. They struggle once money is flowing through multiple bank accounts, card accounts, and giving tools. Every manual import creates another chance to drop a fee, duplicate a transfer, or miss the fund assignment that gives the transaction meaning.

Grain Ledger uses native fund accounting for churches and connects with tools churches already use, including bank and card connections through Plaid and giving providers such as Pushpay, Planning Center, and Stripe. That design matters because the system keeps fund context attached to transactions from the start instead of asking someone to rebuild that story at month-end.

The goal is not prettier reporting. The goal is books that can answer real ministry questions without guesswork.

Generating the Four Essential Church Financial Reports

Once the data is reconciled and coded correctly, report preparation gets much easier. This is the point where standard accounting statements become useful church leadership tools instead of compliance exercises.

The sequencing matters. Gather the source records, reconcile them to the bank, classify and adjust transactions into the right periods, then generate the reports. That order is recommended because statement accuracy depends on matching records to bank balances before converting them into the core reports, as described in this guide to preparing accurate financial reports.

Essential Church Financial Reports at a Glance

| Report Name | Key Question It Answers | What to Look For |

|---|---|---|

| Statement of Financial Position | What do we own, owe, and hold right now? | Cash by net asset category, liabilities, restricted versus unrestricted balances |

| Statement of Activities | What changed during the period? | Giving by fund, expenses by ministry area, unusual variances |

| Statement of Cash Flows | How did cash actually move? | Operating cash pressure, project spending, timing gaps |

| Fund Activity Report | What happened inside each fund? | Beginning balance, inflows, outflows, ending balance, exceptions |

Statement of Financial Position

This report is the church version of the balance sheet. It shows assets, liabilities, and net assets at a point in time.

For churches, the key issue isn't just whether the statement balances. It's whether restricted and unrestricted resources are visible enough that a board member can tell what is available for general operations. If a building fund balance sits inside total cash with no clear distinction, the church may look healthier than it really is.

Review this report with a few questions in mind:

- Is restricted cash clearly distinguishable from operating cash?

- Do liabilities include all unpaid obligations such as payroll items, vendor bills, or reimbursements?

- Can leadership tell what is available to spend without violating donor intent?

Statement of Activities

At this point, many churches still think in broad income-and-expense categories only. That isn't enough.

A church Statement of Activities should show revenue and expense activity in a way that lets leaders compare ministry plans to ministry use. General fund giving should not blur together with a designated building campaign. Benevolence assistance shouldn't disappear into a broad outreach line with no fund context.

A report becomes much more useful when it can answer questions like these:

- Did designated giving arrive where people intended it to go

- Did a ministry overspend because of timing, volume, or miscoding

- Are year-to-date variances operational or classification issues

A clean Statement of Activities doesn't just show that expenses were high. It shows which fund absorbed them, why, and whether the change was expected.

If your board wants a broader grounding in how formal statements are structured across reporting environments, this expert guide to financial statements UAE is a useful outside reference because it explains the role each statement plays without assuming the reader is an accountant.

Statement of Cash Flows

Church leaders often underestimate this report until cash gets tight. A church can show a healthy operating picture on paper and still face immediate pressure if large obligations hit before expected receipts arrive.

The cash flow statement helps answer practical questions:

- Are operations generating enough cash to support recurring ministry activity?

- Did a capital purchase or facility project consume cash faster than expected?

- Are financing decisions or debt payments creating pressure on monthly flexibility?

For boards that need help reading this report without accounting jargon, this short guide on how to read a cash flow statement can help frame the discussion.

Fund Activity Report

This is the report I want in every church packet, even when it isn't formally required.

The Fund Activity Report translates accounting records into stewardship language. It shows beginning fund balance, contributions or transfers in, expenses or transfers out, and ending balance for each major fund. Pastors, elders, and finance committees can usually work with this report immediately because it aligns with how ministry decisions get made.

Use it to flag issues such as:

- Negative or near-depleted balances in ministry-designated funds

- Restricted funds with no recent activity, which may suggest stalled projects or communication gaps

- Transfers that need explanation, especially between the general fund and designated purposes

What doesn't work is handing leaders only a detailed general ledger or a standard profit-and-loss report and expecting them to infer fund stewardship from raw account names. They won't, and they shouldn't have to.

Internal Controls and Preparing for an Audit

A church can have accurate-looking reports and still have weak reporting discipline underneath them. I see this most often when giving data lives in one system, bank activity in another, payroll in a third, and nobody can explain how a transfer or adjustment moved from one place to the final statements. Internal controls fix that problem before it turns into an audit finding, a board concern, or a trust issue.

For churches, controls are stewardship routines. They make sure contributions are recorded in the right fund, disbursements follow approval, and every balance on a report can be tied back to supporting records. Public-company rules like Sarbanes-Oxley do not govern most churches, but the underlying expectation still applies. Financial reports should be traceable, reviewable, and understandable.

Simple controls that fit real churches

The goal is not complexity. The goal is to keep one person, one spreadsheet, or one unchecked process from carrying too much risk.

- Separate receipt from recording. The person opening mail or counting offerings should not be the only person posting gifts into the accounting system.

- Match deposits to giving records. Reconcile batch totals from your giving platform to the bank deposit and then to the general ledger, especially for online gifts that settle on a delay.

- Require approval before cash leaves. Checks, ACH payments, card charges, and reimbursements should have documented authorization.

- Assign an independent bank review. A treasurer, finance committee member, or elder who is not doing the day-to-day bookkeeping should review reconciliations and unusual transactions.

- Document every fund transfer and adjustment. If money moves between funds, write down who approved it, why it moved, and whether donor restrictions were affected.

Those steps do more than prevent misuse. They also solve the first reporting problem many churches face. Getting data from separate systems to agree before the month-end packet goes out.

Audit prep starts with the monthly close

Audits rarely become difficult because of one dramatic mistake. They become difficult because the church cannot produce the trail behind the numbers. A restricted gift was posted to revenue but not to the right fund. A bank reconciliation was completed, but the outstanding items were never cleared. A journal entry fixed payroll allocation, but no one kept the support.

That is why good audit preparation starts long before the auditor arrives. If the monthly close includes reconciled bank accounts, matched giving records, reviewed journal entries, and clear fund schedules, the audit becomes an inspection of organized work instead of a scramble to rebuild it.

A practical resource on understanding audit compliance for nonprofits can help churches frame what reviewers are likely to request and how to prepare their files.

For churches tightening procedures, this checklist of internal controls best practices is a good starting point because it turns broad control ideas into workable finance routines.

What to have ready

Before an audit, review, or high-stakes finance committee meeting, gather these records in one place:

- Bank reconciliations for every operating, savings, and designated account

- Giving reports, batch summaries, and deposit support tied to recorded contribution income

- Journal entry support for accruals, corrections, payroll allocations, and fund transfers

- Board minutes or written approvals for budget adoption, large purchases, debt activity, and designated fund use

- Fund balance detail showing which balances are restricted, board-designated, or available for operations

- A trial balance and year-to-date general ledger that agree to the statements you presented internally

This is also where the second reporting challenge shows up. Auditors may start with standard statements, but church leaders usually need the fund story behind them. If your files explain both the accounting treatment and the ministry purpose, the audit process gets easier and the board conversation gets clearer.

Good controls protect more than cash. They protect confidence in the numbers and confidence in the people handling them.

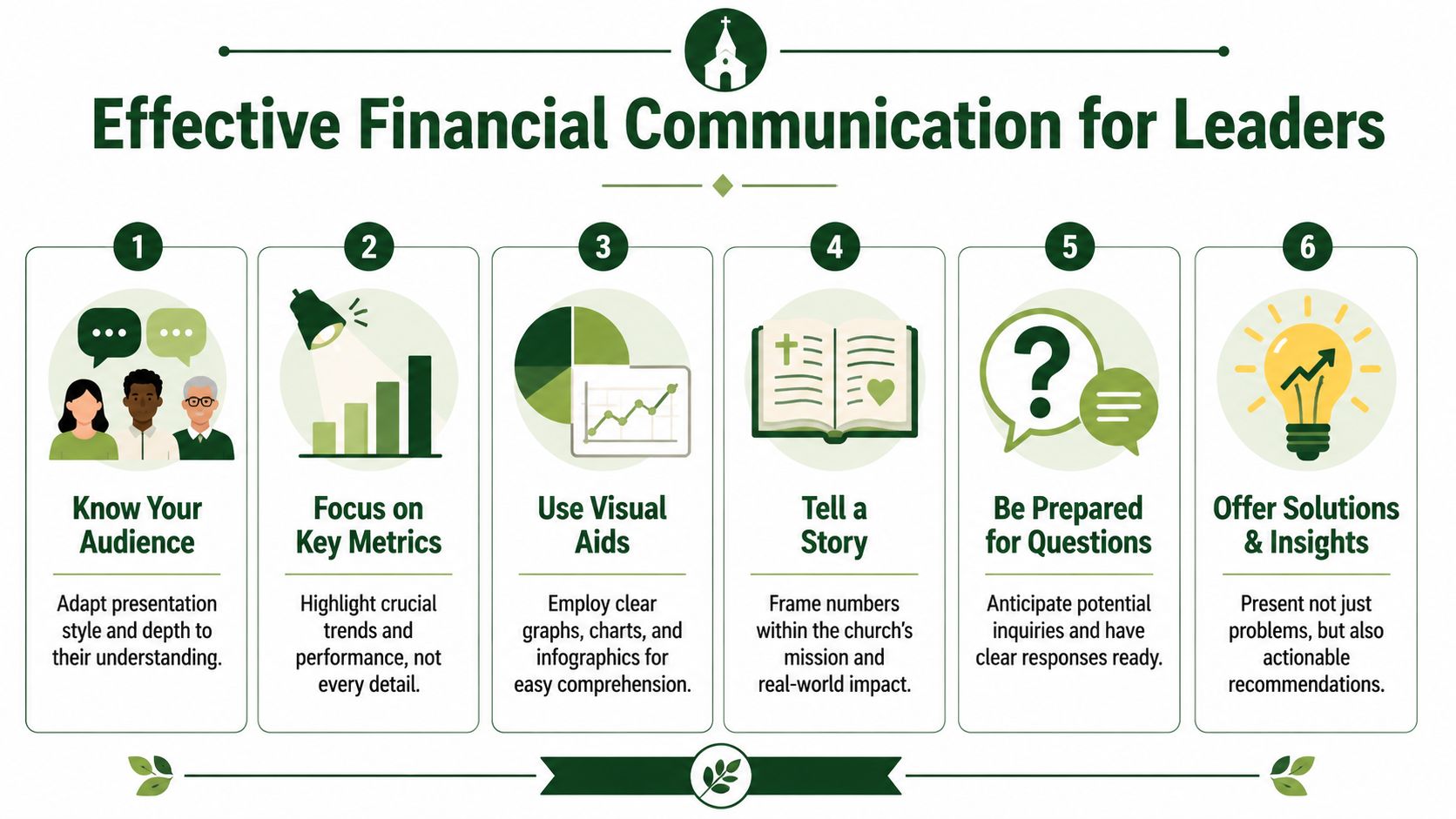

Presenting Financials to Pastors and Boards

The board meeting starts in ten minutes. The pastor wants to know whether ministry plans can stay on track. A board member asks why cash feels tight when giving looked solid on Sunday. If the packet only shows standard statements, the room spends half the meeting trying to decode the numbers instead of making decisions.

That is the core job of this section of the process. Present financials in a way that connects reconciled data to ministry choices.

Translate statements into leadership language

Pastors and boards rarely need more detail. They need the meaning of the detail. After the giving system, bank activity, payroll, and general ledger have been reconciled, the next step is to explain what those numbers mean by fund, by purpose, and by decision.

In church finance, that usually comes down to a few practical questions. Did unrestricted giving support current operations? Are restricted funds being used as intended? Did a timing issue, transfer, or one-time expense change the picture this month?

A good board packet answers those questions before anyone asks them.

I usually recommend a short leadership summary before the full statements. Keep it tight and decision-oriented:

- A one-page dashboard with giving trend, available cash, and major fund balances

- A short variance memo that explains the largest changes in plain language

- A decision list showing any item that needs approval, clarification, or follow-up

Show cause, impact, and action

Finance teams often stop at description. Boards need interpretation.

Here is the difference:

| Weak explanation | Better explanation |

|---|---|

| Expenses were high this month | Facility expenses increased because of unplanned repair work. The cost reduced operating cash this month and did not affect restricted ministry funds |

| Giving was down | General fund giving came in below budget for the month. Department leaders should hold discretionary spending until giving normalizes or the board revises the plan |

| Missions fund changed | Missions spending increased because previously approved support payments were sent this period. The fund activity matched donor intent and prior approval |

The stronger version gives leaders three things at once. What happened. Why it happened. What, if anything, they need to do about it.

Boards do not need every transaction. They need the few facts that affect stewardship decisions.

Answer the questions pastors actually ask

In my experience, pastors usually ask some version of the same three questions:

- Can we continue with the ministry plan we approved?

- Are any designated or restricted funds creating pressure, delay, or confusion?

- Does anything in this report require board action or pastoral communication?

Those questions sound simple, but they expose the two reporting problems that trip up many churches. First, numbers pulled from separate systems often look complete but do not agree. Second, standard financial statements rarely explain fund activity in language that ministry leaders can use. Good presentation solves the second problem, but only if the first one was solved before the packet was built.

Teams that want examples of management-style reporting formats can browse Wisely financial reporting services for ideas on how narrative summaries and decision-ready reporting are structured for leadership audiences.

Keep the meeting focused

A finance presentation should help the room make decisions quickly and responsibly. Start with the items that changed the month, not a line-by-line reading of every report.

This order works well:

- Stewardship summary first. State whether operations, liquidity, and major funds are on track

- Material variances second. Explain the few changes that matter most

- Action items last. Identify approvals, follow-up work, or communication needs

That approach respects everyone's time. It also builds confidence. When church leaders can see both the accounting result and the fund story behind it, they are far more likely to trust the report and use it well.

Related church budgeting resources

Use these resources together when moving from a spreadsheet budget to cleaner monthly church financial reporting.

- Free church budget generator - build a custom Excel budget template for your church

- Church budget template Excel guide - download and adapt a practical budget template

- Nonprofit budget examples - compare operating, program, and restricted-fund budget formats

- Grain Ledger budgeting - connect budgets to fund accounting and monthly reports

From Reporting to Confident Stewardship

A month-end packet lands in the board folder. The numbers tie out, but the room still has the same questions. Why is the general fund tighter than expected? Did designated gifts reach the ministry they were meant to support? What needs a decision now, and what can wait?

Confident stewardship begins when those questions can be answered without hunting through bank exports, giving reports, and side spreadsheets. Churches get there by doing two things well. They reconcile information from separate systems before the close, and they present the final reports in a way that explains fund activity clearly enough for pastors and boards to act on it.

That is the shift. Reporting stops being a monthly exercise in assembly and becomes a discipline of accountability.

In practice, the churches that improve fastest are not always the ones with the most proficient finance teams. They are the ones that build a repeatable process. Gifts are matched to the right funds. Bank activity is cleared on time. Transfers are documented. Restrictions are visible in the ledger, not buried in someone's spreadsheet. Once that foundation is in place, the standard statements start answering ministry questions instead of creating new ones.

I have seen this trade-off many times. A church can keep patching together reports with exports and manual checks, and that can work for a while. But every extra workaround makes it harder to explain the story behind the numbers, harder to spot errors before a board meeting, and harder to prove that designated money was handled correctly.

The volunteer treasurer from the opening example should be able to trace a designated gift in minutes. The pastor should be able to see whether current spending is supporting or straining ministry plans. The board should be able to read one packet and know where oversight, approval, or communication is needed.

That is what faithful financial reporting looks like. Clear books. Clear fund activity. Clear decisions.

If your church is still stitching together reports from bank exports, giving platform downloads, and spreadsheets, the next improvement is usually not a better-looking template. It is a system that preserves fund structure from the first transaction through the final report.

If your church wants cleaner closes, clearer fund visibility, and reports that pastors and boards can use, take a look at Grain. It's purpose-built for church fund accounting, connects the systems churches already use, and helps finance teams spend less time reconciling spreadsheets and more time guiding stewardship. Schedule a Demo to see when it's available.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.