Restricted Net Assets: A Church's Guide to Stewardship

A guide for churches on managing restricted net assets. Learn GAAP rules, journal entries, and stewardship best practices to ensure every dollar is tracked.

A lot of church finance confusion starts with a report that looks reassuring.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Start free to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

The balance sheet says the church has healthy net assets. The checking account has money in it. A generous donor just gave toward a building project, a youth trip, or a future ministry initiative. Then payroll week arrives, the HVAC quits, and someone asks a simple question that suddenly isn't simple at all. “Can we use that money for now and replace it later?”

That's where restricted net assets stop being an accounting term and start becoming a stewardship issue. If you serve on a finance committee, you don't need to become a CPA to understand this well. You do need to know which dollars are available, which dollars are spoken for, and how to report both clearly enough that your board can make wise decisions.

The Blessing and Challenge of a Restricted Gift

A treasurer opens the mail after Sunday and finds a note from a longtime member. The gift is generous. The instructions are clear. Use it for the new roof.

Everyone feels grateful, and they should. A designated gift like that can move ministry forward in a way the regular operating budget may never be able to do. But that same gift also creates a responsibility. The church now holds money that belongs to a specific purpose, not to the general budget.

That means the finance committee can't treat those dollars like a backup checking account. If giving runs light next month, that roof money can't otherwise cover utilities or payroll. If the copier dies, that roof money still isn't available. The donor's instruction matters, and the church's records need to show that it matters.

Practical rule: A restricted gift is a blessing you must track, protect, and use exactly as intended.

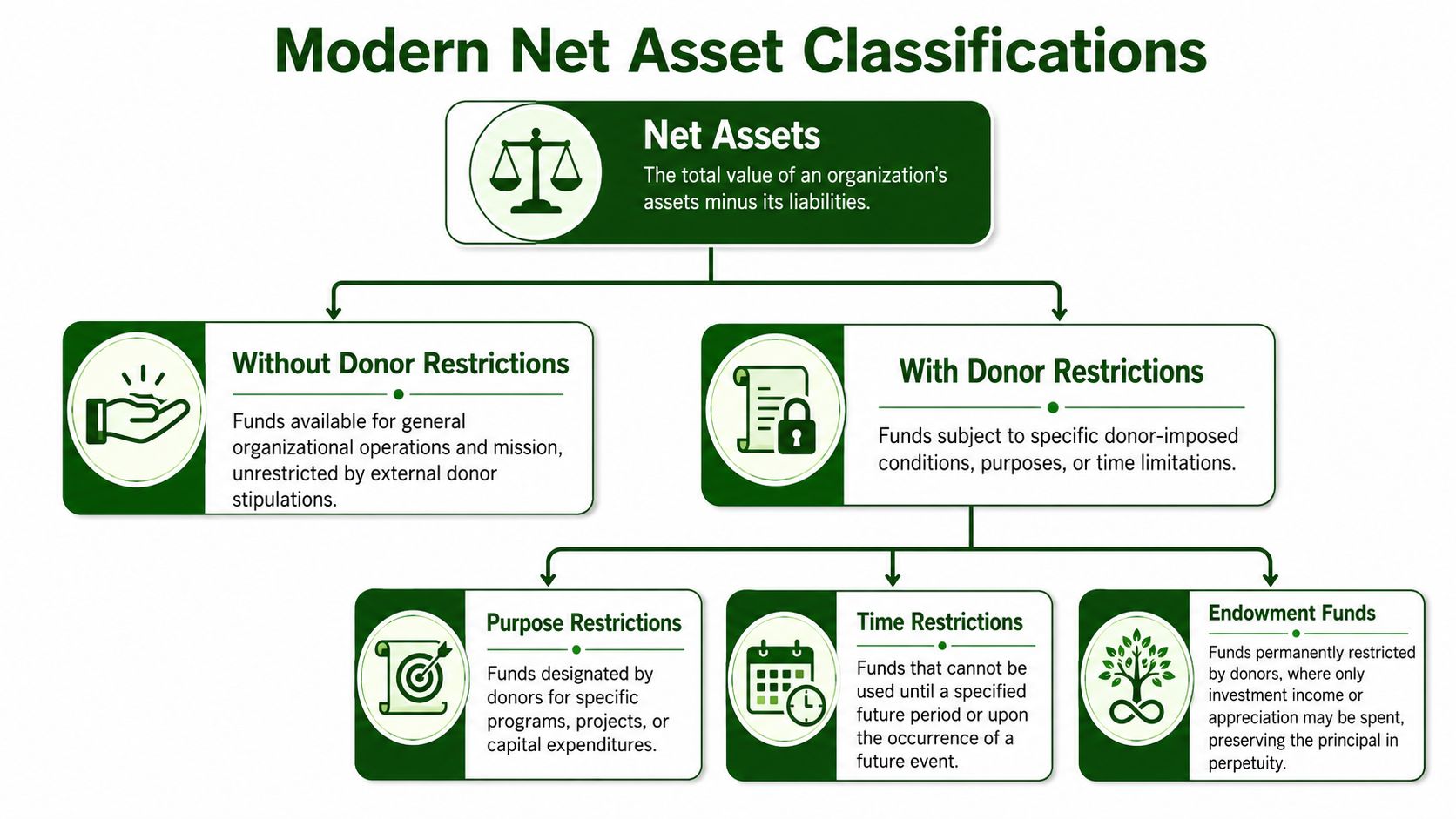

This is the heart of restricted net assets. They're assets the church has received, but they come with donor-imposed limits. Some are restricted for a purpose, such as a van, benevolence fund, or mission trip. Others are restricted by time, which means the church can't use them until a later period. Some are perpetual in nature, such as endowment principal that must remain intact.

If you're newer to church finance, a helpful starting point is this plain-language guide to what a restricted fund is. It helps put names to something many churches already deal with every month.

The terminology in nonprofit accounting has changed over time. The principle hasn't. Honor donor intent. Good bookkeeping supports that. Good reporting proves it. Good stewardship depends on it.

Understanding the New Rules for Net Assets

A finance committee meeting can get confusing fast when one person says “temporarily restricted,” another says “permanently restricted,” and the financial statements use different labels altogether. If you have ever wondered whether the rules changed or the church is just using old vocabulary, the short answer is yes, the presentation rules changed.

Current U.S. GAAP, through FASB ASU 2016-14, simplified how nonprofits present net assets. Instead of three categories, churches now report two: without donor restrictions and with donor restrictions. What used to be called permanently restricted net assets is now included under net assets with donor restrictions, with notes explaining when those gifts are perpetual in nature.

A household analogy can make this clear

Your church may keep its cash in one bank account, but the accounting still has to answer a bigger question: which dollars are available for this month's ministry, and which dollars are already spoken for?

Without donor restrictions works like the portion of a household budget you can use where needed. Groceries are high this week. The car needs tires next month. You adjust.

With donor restrictions works more like money you have already set aside for a specific purpose. If you saved for a roof repair, that money should not become vacation money because the electric bill came in high. The cash may sit in the same account, but its assignment still matters.

That is why the new labels help. They put the focus on availability, which is what boards and treasurers need to understand quickly, especially in churches where a strong balance sheet can hide a real cash squeeze in operations.

What changed on the statements

The main change was presentation. The responsibility to track donor intent stayed the same.

A church may still need internal detail showing whether a restriction relates to purpose, time, or an endowment arrangement. On the face of the financial statements, though, those details now roll up into the two broader net asset categories. If you want the technical background behind that reporting model, this guide to FASB ASC 958 for churches and nonprofits gives a useful accounting explanation without losing the practical side.

The labels are simpler. The stewardship responsibility is exactly the same.

If your committee is also cleaning up receipts, account coding, and documentation, it helps to review practical systems that organize business finances so the reporting stays consistent from month to month.

Why this helps non-accountants

The two-category model is easier for boards to read because it gets to the question that matters in governance: Which resources can we use freely, and which must be used according to donor instructions?

That sounds small, but it solves a common church problem. Older terms can pull people into technical debates when the underlying issue is cash availability and stewardship. Clearer categories help a finance committee spot the difference between “we have assets” and “we have funds available for payroll, utilities, and this month's ministry.” That distinction becomes very important when restricted giving is strong but operating cash is tight.

Why a Healthy Balance Sheet Can Be Deceiving

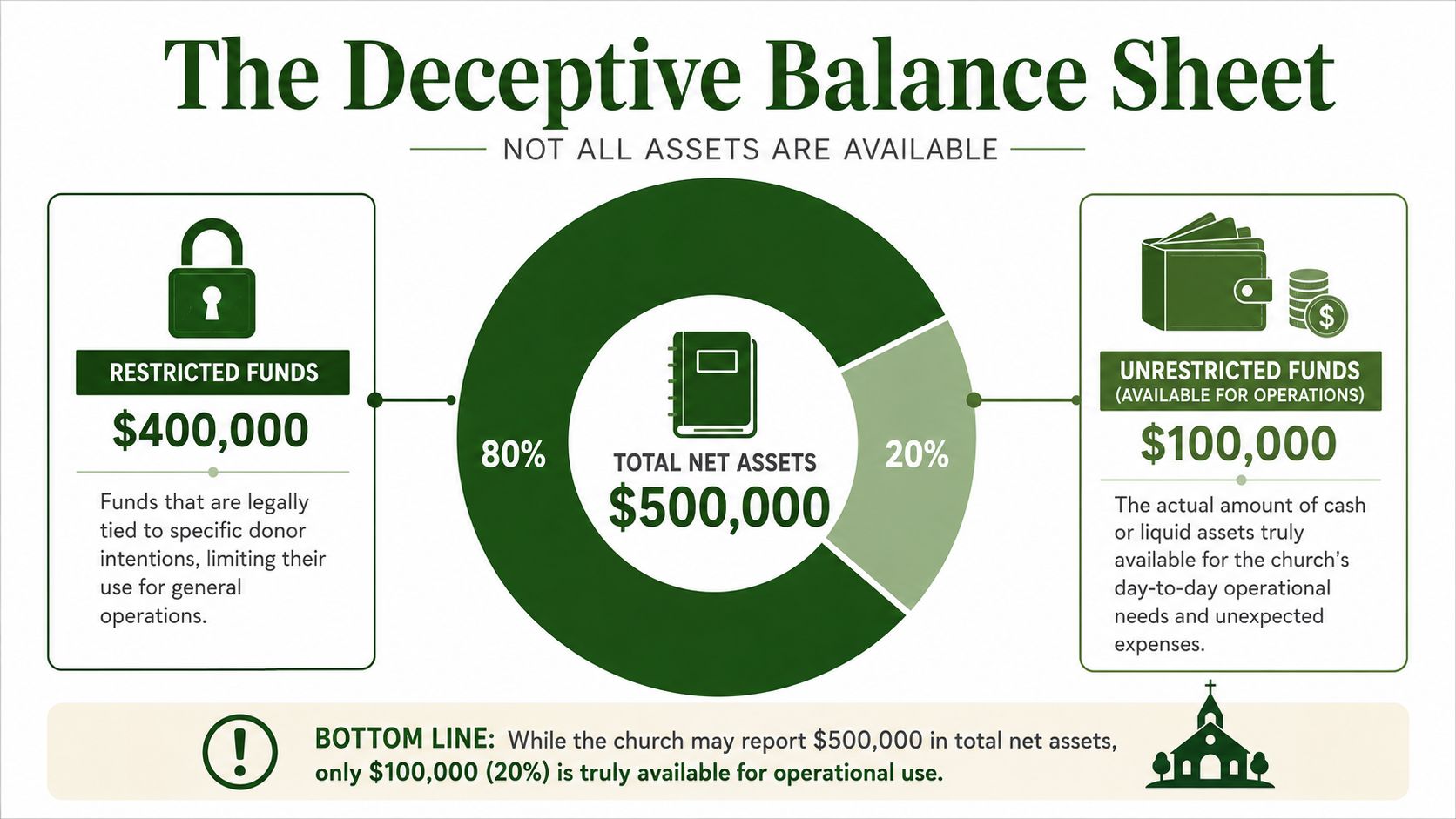

One of the most common mistakes in church finance is assuming total net assets means money available to spend. It doesn't.

A church can show a strong bottom line and still feel pressure meeting routine obligations. That happens when a large share of its resources is restricted. The balance sheet looks healthy, but the operating picture is tighter than the board realizes.

The liquidity gap in plain language

This is the liquidity gap. It's the distance between what the statement says the church has and what leaders can use for current operations.

The nonprofit sector often treats unrestricted net assets as a key cushion for volatility, and advisors commonly recommend enough unrestricted net assets to cover three to six months of operating expenses. A frequently used illustration shows why: if a church reports $1 million in total net assets but $700,000 is with donor restrictions, it only has $300,000 in flexible capital, which may fall below that recommended cushion if annual expenses exceed $500,000 (video explanation of nonprofit liquidity and restrictions).

That example lands because it feels familiar. A church can be rich in campaign funds, scholarship balances, or future-use gifts, yet still have limited room for salaries, insurance, maintenance, and ordinary ministry needs.

Why boards get fooled

Most boards aren't trying to ignore restrictions. They're reacting to the number they see most clearly.

If the Statement of Financial Position shows a large total, people naturally assume the church has breathing room. But some of those assets may be tied up for a building project, a grant purpose, or a future year. They count as real assets. They just aren't available for general use.

Here's a simple way to frame the conversation at a board meeting:

| Reported number | What it tells you | What it does not tell you |

|---|---|---|

| Total net assets | Overall financial position | Spendable operating cash |

| With donor restrictions | Resources limited by donor intent | Flexibility for payroll or utilities |

| Without donor restrictions | Resources available for general use | Whether cash timing is smooth |

A church can be asset-rich on paper and cash-tight in practice.

A better habit for leadership

When I sit with finance volunteers, I encourage them to stop asking only, “How much do we have?” and start asking, “How much can we use?”

That second question changes decision-making. It affects staffing, repair timing, reserve planning, and how aggressively the church can launch new ministry initiatives. If your board doesn't see the liquidity gap, it may approve plans the operating budget can't safely support.

How to Record and Release Restricted Funds

A common church scenario goes like this. The church receives a generous $25,000 gift for a future building project, deposits it, and sees the bank balance rise. A few weeks later, payroll is tight, and someone around the table says, “We have money in the account.” The bank statement is telling the truth about cash on hand. It is not telling the truth about what that cash is available to do.

That is why recording and releasing restricted funds needs a clear routine. Once you learn the pattern, it becomes much less intimidating. You are really tracking two moments. First, when the church receives or is promised a gift with donor instructions. Second, when the church has met those instructions and can reclassify the amount.

Under nonprofit GAAP, a donor-restricted contribution is recognized in the restricted category when the promise is unconditional, even if the cash has not arrived yet. If the donor has made a firm pledge, the church may record a receivable along with contribution revenue in net assets with donor restrictions, as explained in this overview of nonprofit contribution recognition and restricted gifts.

Entry one when the church receives a restricted contribution

Let's use a playground gift.

If a donor gives cash for that project, the revenue starts in with donor restrictions. It does not wait until the church spends it. That first classification matters because it tells your finance committee, “Yes, we received a real gift. No, it is not available for general ministry expenses.”

A simple presentation looks like this:

| When the restricted gift is recognized | Debit | Credit |

|---|---|---|

| Cash or Accounts Receivable | amount of the gift | |

| Contribution Revenue, With Donor Restrictions | amount of the gift |

Churches that skip this step often create the exact liquidity gap that surprises boards later. The balance sheet looks strong, but the operating side is weaker than it appears because restricted money was mixed in with flexible revenue.

Entry two when the restriction is fulfilled

The second entry is the one people often miss.

Suppose the church buys the playground equipment, pays the installer, and finishes the project. You already recorded the expense when you paid the bill. You still need a separate release entry so the financial statements show that the donor's purpose has been fulfilled.

The required release entry involves a dual movement. One side reduces net assets with donor restrictions. The other side increases net assets released from restrictions in the without donor restrictions category. Auditors usually want support showing that the donor's requirement was met, as noted in J.S. Morlu's explanation of release entries for restricted net assets.

A practical format looks like this:

| When the purpose or time restriction is met | Debit | Credit |

|---|---|---|

| Net Assets Released from Restrictions, With Donor Restrictions | amount released | |

| Net Assets Released from Restrictions, Without Donor Restrictions | amount released |

The account names may differ in your chart of accounts. The movement needs to stay clear.

A file folder works like the donor's instruction card. Receiving the gift puts money into that folder. Releasing it removes the instruction because the church has done what the donor asked. If you spend the money but never clear the folder, your reports keep showing restrictions that no longer exist. If you clear the folder too early, your reports suggest freedom the church does not have.

What counts as proof

Use documentation that matches the restriction.

For a van purchase, keep the invoice, payment record, and title paperwork. For a mission project, keep vendor bills, approval notes, and records showing the project was completed. For a time restriction, keep the donor communication that set the date or period, plus the records showing that period has passed.

A good rule for your finance team is simple. Release restricted net assets because the donor's requirement has been satisfied, not because the church wants more room in the operating budget.

That discipline also improves board reporting. Clear classifications and timely releases make it easier to follow best practices for financial reporting and to explain why a healthy cash balance may still include money that cannot cover routine ministry costs.

Common point of confusion

Finance volunteers often ask, “If the cash left the checking account for the project, hasn't that already handled the restriction?”

Not by itself.

The bank account answers one question: where the cash sits. Net asset classification answers another: whether the church is free to use that money for general operations. Both have to be right. That is why many churches start with spreadsheets and manual journal entries, then eventually move to fund accounting software that tracks the restriction, the expense, and the release in one consistent system.

Presenting Clear Financials to Your Board

The board packet shouldn't require a translator. When leaders scan the financials, they should be able to tell what's available for current operations and what's being held for donor-directed purposes.

That's why the two-column format works so well. Technical benchmark guidance indicates that the most effective reporting structure is a two-column financial statement approach, with With Donor Restrictions and Without Donor Restrictions shown on both the income statement and balance sheet, because it keeps unrestricted amounts visible for daily decision-making (Propel Nonprofits guidance on managing restricted funds).

What I would say in the board meeting

I'd hand out the Statement of Activities and start with the unrestricted column.

“This column tells us how the operating side of the church is performing. General giving, routine expenses, and the impact on our flexible resources show up here.”

Then I'd point to the restricted column.

“This side shows gifts and activity that carry donor instructions. It helps us answer whether building gifts, mission gifts, or other designated funds are being used as intended.”

That simple explanation lowers the temperature in the room. People don't have to decode nonprofit accounting vocabulary. They can focus on stewardship and planning.

A simple reporting model

You don't need a fancy design. You need a readable one.

| Statement | Without Donor Restrictions | With Donor Restrictions |

|---|---|---|

| Statement of Activities | Operating support, released amounts, general expenses | Restricted contributions, remaining restricted activity |

| Statement of Financial Position | Flexible net assets for operations | Net assets still bound by donor intent |

What makes this useful is not the format alone. It's the discussion it enables. Board members can see whether the church's unrestricted position is strengthening or tightening without mistaking campaign money for operating reserve.

If your team wants a broader refresher on best practices for financial reporting, that can help sharpen how reports are prepared, reviewed, and explained across the whole finance function.

When the columns are clear, the questions get better. “Can we afford this?” becomes “Can our unrestricted funds support this?”

Best Practices for Stewardship and Internal Controls

Restricted net assets are about trust before they're about technique. A donor gave with intent. The church accepted that responsibility. Internal controls are how you prove the church takes that responsibility seriously.

One of the more sobering problems in church accounting is releasing restrictions too early. Guidance in this area warns that many churches reclassify funds before the donor's specific condition is fully met, even though reclassification should happen only when conditions are fully met (North American Division guidance on restricted funds).

That error usually doesn't start with bad motives. It starts with loose processes, memory-based tracking, or a spreadsheet that only one person understands.

The controls worth putting in writing

A church doesn't need bureaucracy for its own sake. It does need repeatable habits.

- Write a gift policy: Spell out how the church accepts designated gifts, who reviews unusual restrictions, and what happens if a donor proposes something the church can't realistically administer.

- Track each fund separately: Keep a clear record of donor intent, current balance, allowable use, and what event or action triggers release.

- Separate responsibilities: The person receiving funds, the person posting entries, and the person reviewing reports shouldn't all be the same person when staffing allows.

- Review restricted balances regularly: Don't wait for year-end or the audit. Look at open restricted funds during normal board or finance committee review.

- Keep support documents together: Donor letters, grant terms, invoices, approvals, and project completion records should be easy to pull.

- Teach the board what the columns mean: Good reports still fail if nobody reading them understands restrictions.

Two bad habits to avoid

The first is “borrowing” from restricted funds to solve a temporary cash squeeze. Churches may intend to pay it back, but donor restrictions don't pause because cash flow is uncomfortable.

The second is assuming that spending near the purpose is the same as satisfying the restriction. Sometimes it is. Sometimes it isn't. Purpose, timing, and donor wording matter.

A lot of finance teams are also dealing with a broader challenge of handling information consistently across systems and people. That's why a practical framework for data stewardship can be surprisingly helpful here. Clean records and clear ownership reduce avoidable errors.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Automate Your Fund Accounting with Grain Ledger

Monday morning, the finance committee sees a healthy cash balance. By Tuesday, the church office realizes much of that money is tied to missions, benevolence, or a building project, and payroll is coming up. That is the liquidity gap in real life. On paper, everything looks fine. In daily ministry, cash can still feel tight.

Manual tracking often breaks down right at that point. A spreadsheet can record restricted gifts, but it depends on every tab, formula, and timing decision being right. One late entry or one release posted too soon can leave leaders looking at money as available when it is not.

That's why purpose-built fund accounting matters.

Grain Ledger is a cloud-based accounting software that offers fund-based double-entry accounting to track both restricted and unrestricted funds using nonprofit net asset classification, helping maintain donor restrictions legally and financially (Grain Ledger on Capterra). For churches that need a system built around funds instead of generic business bookkeeping, that focused structure matters.

Why automation helps with restricted net assets

A good church accounting system works like labeled envelopes inside one checking account. The cash may sit in one bank, but the records show which dollars belong to operations, which belong to missions, and which cannot be touched until a donor restriction is met. Generic bookkeeping software often makes churches build that logic by hand. Fund accounting software starts with that logic already in place.

That difference matters most when leadership is making decisions. If you want to see how that setup works in practice, Grain's fund accounting features show how fund-level reporting and classification fit together.

For a church office, the practical benefits are straightforward:

- Restricted gifts remain visible: Staff can see what was given, what it can be used for, and what balance is still held for that purpose.

- Available operating cash is clearer: Leaders can spot the difference between total cash and money the church can spend today.

- Releases are easier to support: The accounting record can reflect when the ministry purpose was met and when the restriction should be released.

- Reporting becomes easier to explain: Finance committees and boards can read the statements without trying to decode spreadsheet workarounds.

- Year-end support is easier to gather: Documentation is easier to pull when balances and activity are already organized by fund.

A brief product walkthrough helps make that more concrete.

Churches do not need more accounting complexity. They need fewer chances to mix restricted and unrestricted activity, and better visibility into whether a strong-looking balance sheet is masking an operating cash problem. Grain Ledger fits that need because it is built around church fund accounting rather than a general small-business model.

If your church is trying to move from manual fund tracking to clearer, more reliable stewardship, take a look at Grain. It's built around church fund accounting, so restricted and unrestricted activity can be tracked and reported in the way church leaders need to see it.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.