Understanding Balance Sheets: A Guide for Churches

A complete guide to understanding balance sheets for your church. Learn to read assets, liabilities, and net assets through the lens of fund accounting.

You're probably looking at a church balance sheet because someone handed it to you before a board meeting and said, “The numbers look fine.” The problem is that “fine” can mean very different things in church finance.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

A church can show cash in the bank, own property, and still feel squeezed when payroll, utility bills, or ministry commitments come due. That's usually where new board members get stuck. The balance sheet seems simple on the surface, but the crucial question isn't only whether the church has assets. It's whether those resources are available for current ministry needs.

That's why understanding balance sheets in a church setting takes a little more care than reading a standard business report. You need the basic equation, yes. But you also need to know how restricted funds, debt, and liquidity affect what your church can do next month, not just what it owns on paper.

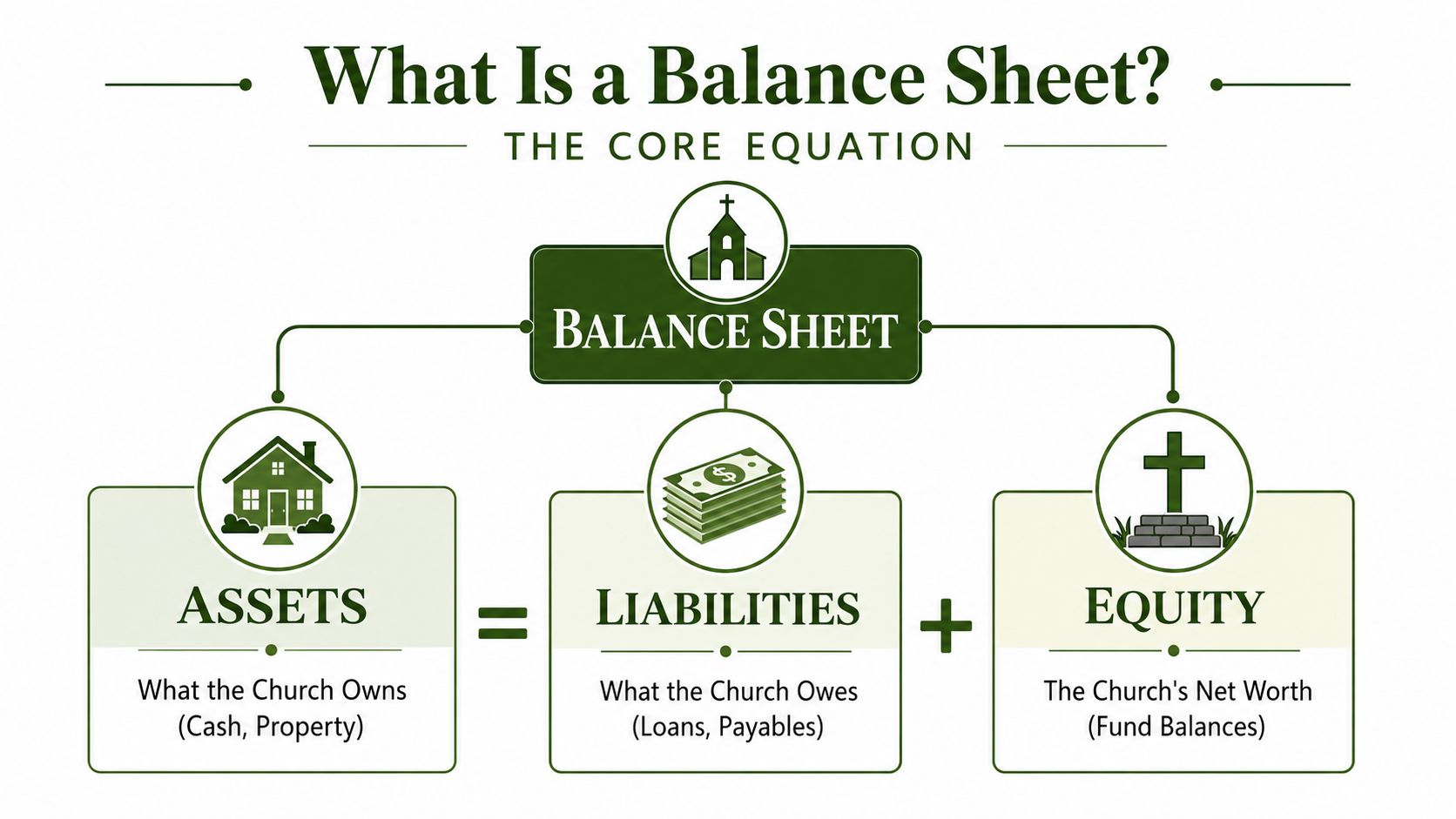

What Is a Balance Sheet? The Core Equation

A balance sheet is a snapshot of financial position at one moment in time. Imagine pausing the church's financial life on a specific date and asking three questions:

- What do we own?

- What do we owe?

- What's left after that?

That's the whole report.

The basic formula is:

Assets = Liabilities + Net Assets

In some settings, you'll see the last part called equity. In churches and nonprofits, you'll usually see net assets instead. The idea is similar. It represents the remaining financial interest after liabilities are accounted for.

Assets are what the church has

Assets include things the church owns or controls that have financial value.

Common church assets include:

- Cash: Money in checking or savings accounts

- Receivables: Amounts expected from pledges or other reimbursements

- Buildings and land: The church property

- Equipment: Sound gear, computers, furniture, vehicles

- Prepaid items: Insurance or service contracts already paid for

Some assets are easy to use right away, like cash. Others are much less flexible, like a building. That difference matters when people talk about “financial health.”

Liabilities are what the church owes

Liabilities are obligations the church must pay.

Examples include:

- Bills due to vendors

- Payroll-related obligations

- Credit card balances

- Loans or mortgage balances

- Amounts owed for services already received

A church may have strong assets overall but still feel pressure if too many bills are due soon.

Practical rule: A balance sheet is not just a list of numbers. It shows how the church's resources are financed and what claims already exist against those resources.

Net assets show what remains

If you took all the church's assets and then subtracted all liabilities, what remains would be net assets. That number helps explain the church's overall financial position.

Here's a simple way to think about it:

| Part | Plain-language meaning |

|---|---|

| Assets | Resources the church has |

| Liabilities | Obligations the church must pay |

| Net assets | What remains after obligations |

At this point, many readers breathe a sigh of relief and think, “Good, I understand it now.” That's a good start. But churches have one extra layer that changes how the balance sheet should be read in practice.

The Fund Accounting Difference for Churches

A church isn't just tracking money. It's also stewarding purpose.

That's why the most important church finance question often isn't a matter of whether assets are greater than liabilities. The more useful question is how much unrestricted liquidity is available after honoring restrictions, because standard balance-sheet teaching often doesn't separate operating cash from restricted balances, even though a healthy-looking balance sheet can still hide cash constraints when restrictions are significant, as noted by Harvard Business School Online on reading a balance sheet.

One bank balance can tell two different stories

Suppose a church has a large cash balance. A new board member might assume the church has plenty of room for ministry expansion, repairs, or staffing.

But that cash may include gifts designated for missions, a building campaign, benevolence, or a youth project. If leaders use those dollars for general expenses, they haven't solved a cash problem. They've created a stewardship problem.

That's where fund accounting comes in. Fund accounting helps a church track resources according to purpose, not just by account type.

Unrestricted and restricted are not the same

A simple way to think about church funds is this:

- Unrestricted funds support general operations. These dollars can usually be used where needed most.

- Restricted funds must be used for the purpose the donor specified.

- Board-designated amounts may be set aside by leadership for a purpose, but those are different from donor restrictions.

If a church mixes all of this together mentally, the balance sheet becomes misleading. The cash line may be accurate from an accounting standpoint, but incomplete from a ministry decision standpoint.

A church can be solvent on paper and tight on cash in real life.

Why this matters for ministry

This isn't just about compliance. It's about trust.

When someone gives to missions, building repair, or a benevolence need, they're expressing intent. Honoring that intent protects the church's credibility with members, supports clean reporting to leadership, and keeps financial decisions aligned with ministry promises.

A church board should learn to ask questions like these when reading the balance sheet:

- How much cash is unrestricted and available for operations?

- Which balances are designated for a specific ministry purpose?

- Are any current needs being covered by money that belongs elsewhere?

That's the difference between basic accounting knowledge and useful church financial oversight. Understanding balance sheets in ministry means reading beyond the totals and asking what portion of those resources is deployable.

Deconstructing a Sample Church Balance Sheet

A sample church balance sheet makes more sense when you read it in layers instead of all at once.

Start with the left side, or top section depending on the format. That area lists assets. Then move to liabilities. Then look carefully at net assets, because that final section often provides a key perspective in a church setting.

A simple church example

Here's a plain-language version of what you might see:

| Section | Sample line items | What it means in church life |

|---|---|---|

| Assets | Cash in checking, savings, receivables, property, equipment | What the church has available or owns |

| Liabilities | Vendor bills, payroll obligations, mortgage, credit card balance | What the church still owes |

| Net assets | General fund, building fund, missions fund | What remains, organized by purpose |

A new reader often sees “cash” and “property” and stops there. But that only tells you part of the story. Actual interpretive work happens when you connect those assets to both obligations and fund purpose.

Standard vs Fund-Based Balance Sheet Structure

| Section | Standard Commercial View | Church Fund-Based View |

|---|---|---|

| Assets | Cash, receivables, inventory, property | Cash, receivables, property, equipment, often viewed with fund context |

| Liabilities | Payables, loans, accrued expenses | Payables, payroll obligations, loans, deferred obligations |

| Equity or net assets | Owner equity, retained earnings | Net assets separated by general, restricted, or designated purpose |

| Primary reading question | Is the business financially sound? | Which resources are available for ministry use, and which are restricted? |

How to read each line with ministry eyes

A few examples help.

Cash in checking sounds straightforward, but it isn't enough to know the total. You want to know whether that cash belongs to the general fund, a building project, or missions.

Accounts receivable may represent money expected but not yet received. That can be useful information, but receivables don't pay this week's bills until the cash arrives.

Property and equipment can make a balance sheet look strong. A church may own land, buildings, and sound equipment. But those assets don't help much with payroll unless they can be sold or borrowed against, and most churches don't want to make ministry decisions under that kind of pressure.

Mortgage payable shows long-term obligation. That line matters because it affects future flexibility.

When you read a church balance sheet, don't ask only, “How much do we have?” Ask, “How much of this can we use for current ministry without violating purpose?”

Net assets deserve the closest attention

If your statement breaks out net assets by fund, that's a good sign. It helps leaders see whether growth in balances reflects actual operating strength or the accumulation of designated gifts.

That distinction keeps boards from making a common mistake. They see a healthy total at the bottom of the page and assume the church has broad spending capacity. A fund-based view tells you whether that conclusion is accurate.

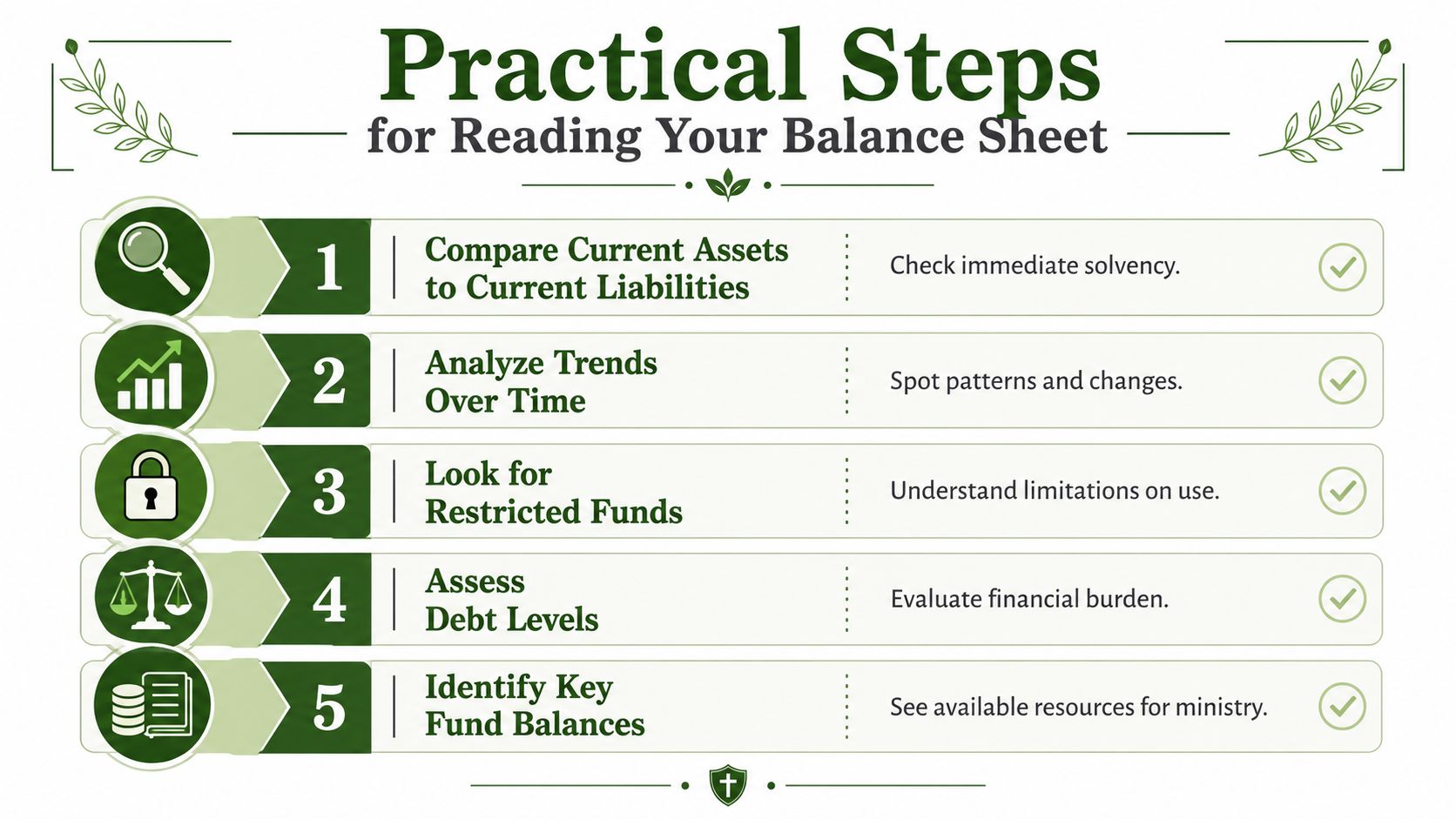

Practical Steps for Reading Your Balance Sheet

If you're in a board meeting and the balance sheet lands in front of you, don't start by staring at the final total. Read it like a treasurer would. Move from immediate obligations to usable cash, then to trends and risks.

Start with current pressures

Look first at what the church can use in the near term and what it must pay in the near term.

Ask:

- What bills are due soon?

- What cash is available soon?

- Is that available cash unrestricted or already spoken for?

A church may appear stable in total assets while still carrying hidden stress. Current needs don't get paid with long-term property value. They get paid with liquid, available resources.

Review fund availability before drawing conclusions

For churches, greater care is needed than most standard tutorials provide. A high total cash balance can mislead board members if much of that amount sits in restricted funds.

Use a short checklist:

- Identify unrestricted balances. These support ordinary ministry operations.

- Separate donor-restricted amounts. These should remain tied to their intended purpose.

- Review designated funds carefully. Leadership may have set these aside, but they don't carry the same meaning as donor restrictions.

- Check whether operating strain is being masked. A strong total can hide a weak general fund.

Look at debt with today's conditions in mind

Debt lines deserve more attention than they used to. Paro's discussion of balance-sheet analysis notes that today's economic pressures, including increased financing costs since 2024, make balance-sheet quality more sensitive to debt maturity and unrealized losses. For churches, that means total assets can look strong while concentration risk or reserve weakness remains hidden unless liquidity is reviewed by fund and purpose.

That's especially important when a church has a mortgage, a large capital commitment, or reserves tied up in specific categories.

Board question: If financing stays expensive, can the church still meet ministry needs without leaning on restricted balances or delaying essential obligations?

Compare periods, not just one report

A single balance sheet is a snapshot. Two or three balance sheets show movement.

Review the same report over several periods and notice:

- Whether unrestricted cash is growing or shrinking

- Whether liabilities are rising faster than accessible assets

- Whether one restricted fund is growing while the general fund weakens

- Whether property or equipment balances are crowding out attention to liquidity

That pattern-based reading is where understanding balance sheets becomes useful, not merely technical.

Keep a short board-level summary

Many boards don't need every line item every month. They do need a short summary that translates the report into decisions.

A useful summary usually highlights:

| Focus area | What board members should know |

|---|---|

| Unrestricted cash | What is available for current ministry operations |

| Restricted funds | What must remain dedicated to donor intent |

| Short-term obligations | What needs to be paid soon |

| Debt position | What future flexibility may be affected |

That kind of review turns the balance sheet from a filing requirement into a leadership tool.

Common Pitfalls in Church Balance Sheet Management

Most church balance sheet problems don't come from bad motives. They come from good people using reports that don't clearly show what matters.

Treating all cash as available cash

This is the most common misunderstanding. A church may keep restricted and unrestricted money in the same physical bank account while tracking them separately in the books. That can work if the records are accurate.

The mistake happens when leaders forget the tracking part and make spending decisions based on the bank balance alone.

Misreading debt as ordinary income support

Sometimes a church receives loan proceeds or financing related to a project. If someone informally talks about that money as if it were operating strength, confusion follows quickly.

Loans create obligations. They may increase cash temporarily, but they don't improve ministry capacity in the same way unrestricted giving does.

Ignoring the wear on long-term assets

Buildings, equipment, and vehicles don't stay new. If depreciation or other asset-related adjustments are ignored, the balance sheet can slowly become less useful as a stewardship tool.

You don't need to obsess over every accounting detail as a board member. But you do want confidence that long-term assets are being recorded thoughtfully and consistently.

A polished balance sheet can still be a weak management report if it doesn't help leaders distinguish available resources from committed ones.

Failing to explain categories to the board

Some treasurers know exactly what each line means, but the rest of the board doesn't. Then silence fills the room, everyone nods, and weak assumptions go unchallenged.

A better approach is to explain unfamiliar items in plain language:

- What is it?

- Why is it there?

- Can we use it freely?

- What decision should this shape?

If the board can answer those four questions, the report is doing its job.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

From Reporting to Stewardship Communicating Financial Health

Numbers by themselves rarely build trust. Clear explanation does.

That's why the treasurer's job isn't only to produce a balance sheet. It's to help pastors, elders, finance teams, and congregation members understand what the balance sheet means for ministry decisions. A good report answers practical questions before someone has to ask them out loud.

Translate the report into plain speech

When you present financials, don't lead with categories that only accountants use. Start with ministry implications.

For example, instead of saying, “Net assets increased,” say:

- General operating cash remains stable

- Missions funds are fully reserved for their intended use

- The mortgage is still a meaningful obligation

- Leadership should watch unrestricted liquidity closely

That kind of wording helps non-financial leaders act wisely without getting lost in terminology.

Build a small dashboard

A simple dashboard often serves the board better than a dense packet.

You might include:

| Dashboard item | Why it matters |

|---|---|

| Unrestricted cash balance | Shows what's available for current operations |

| Major restricted fund balances | Confirms donor intent is being honored |

| Outstanding debt | Shows long-term financial pressure |

| Notable changes from prior period | Helps leaders spot movement early |

If your accounting system can generate a true fund-based balance sheet, this becomes much easier. Grain Ledger is one example of church accounting software built around funds from the start, with fund-based reports that separate balances by purpose and support clearer balance sheet reporting for churches.

A short walkthrough can help leaders see what this kind of reporting looks like in practice.

Make stewardship visible

Church members don't need a lecture in accounting. They do need confidence that leaders know where the money is, what it's committed to, and how financial decisions support ministry priorities.

That's the heart of understanding balance sheets in a church context. It isn't about sounding more impressive in a finance meeting. It's about showing, with honesty and clarity, whether the church has the resources to sustain ministry, meet obligations, and honor the intent behind every gift.

When a balance sheet is read that way, it stops being a static report and becomes a stewardship conversation.

If your church needs cleaner fund-based reporting, Grain is worth considering. It's built for church accounting, organizes reporting around funds, and helps teams present balance sheets in a way pastors and boards can use.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.