What Is Consolidated Financial Statement: 2026 Church Guide

Discover what is consolidated financial statement reporting for churches in 2026. Master fund accounting methods to ensure full financial transparency today.

You're probably looking at several reports right now that don't quite talk to each other.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

The general fund shows one cash balance. The building fund shows another. The preschool has its own income and expenses. Missions may be tracked separately too. Each report may be accurate on its own, but the elder board still asks the same question: What is the true financial position of the whole ministry?

That's where understanding what is consolidated financial statement becomes useful for church leaders. It's not just corporate accounting language. It's a practical way to combine separate financial pieces into one trustworthy picture, so leaders can make decisions with clarity instead of guessing from fragments.

The Challenge of Seeing Your Church's Full Financial Picture

A new finance committee member often sees separate reports and assumes the church already has the full picture. That's understandable. If every ministry sends in numbers, it feels complete.

But separate reports can still leave you with blind spots.

A church might have a healthy general fund on paper while its preschool is carrying obligations the board hasn't fully considered. The building fund may hold designated cash, but that doesn't mean those dollars are available for payroll or missions. A transfer from one fund to another might appear as activity twice if no one removes the internal movement when preparing a combined report.

Why separate reports can mislead

Think about a family that keeps three notebooks. One for household bills, one for savings for a kitchen remodel, and one for a small side business. If the family wants to know its overall financial health, reading those notebooks one by one helps, but it doesn't answer the full question.

Churches face the same problem when they manage:

- Multiple funds such as general, missions, benevolence, and building

- Distinct ministries such as a preschool or counseling center

- Multiple campuses with local spending and shared central support

When leaders only review siloed statements, they can miss how these pieces connect.

A church can have good records and still lack a single source of truth.

That's why many treasurers start by gathering PDFs, spreadsheets, and exported reports just to compare them line by line. Tools like a financial analysis tool can help make those reports easier to read, especially when you're trying to spot trends or unusual changes across several statements.

The question church boards actually need answered

The board usually isn't asking, “How did each report look in isolation?”

They're asking simpler and harder questions at the same time:

- Can we afford this ministry expansion

- Are restricted funds still protected

- How much of our resources are available

- What obligations exist across the entire ministry

A consolidated financial statement helps answer those questions by treating the church and its controlled parts as one economic whole.

What Are Consolidated Financial Statements

A consolidated financial statement combines the finances of a parent entity and its controlled entities into one report. In plain language, it tells the story of the whole group instead of handing you a stack of separate stories.

In a church setting, the parent is often the main church organization. A subsidiary might be a preschool, a separately organized ministry, or another controlled entity connected to the church's operations.

Simple definition: A consolidated financial statement rolls multiple related sets of books into one view, then removes internal transactions so only the group's real financial position remains.

A family budget analogy

A family can make this intuitive.

Suppose parents track the household checking account, their teenager has a savings account, and the family also set aside money in a separate vacation fund. If they want to know the family's full financial position, they can't just glance at one account. They combine them.

But if Dad moved money from checking into the vacation fund, the family shouldn't count that transfer as new income. It's still the same family money, just in a different pocket.

That's the heart of consolidation.

What gets combined

Technically, consolidation involves line-by-line addition of assets, liabilities, equity, revenues, and expenses. One example from Sage's explanation of consolidated financial statements shows that if a Parent has $100M in assets and a 100% owned Subsidiary has $40M, the post-consolidation balance sheet would total $140M in assets, minus any intra-group eliminations.

For churches, the same thinking applies even if the structure is less corporate. You may combine:

- Cash balances across funds or controlled entities

- Liabilities such as loans or payables

- Revenue and support from offerings, tuition, or fees

- Expenses tied to ministry operations

If you want a clearer grounding in church reports before you consolidate them, this overview of a church financial statement is a helpful companion.

Why individual reports aren't enough

Separate reports still matter. The preschool director needs preschool numbers. The missions team needs the missions report.

But the board and senior leadership also need one combined report that answers a different question: How is the whole ministry doing when viewed as one entity?

That's what consolidated reporting provides.

Why Consolidation Matters for Church Stewardship

Churches don't consolidate financials just to sound formal. They do it because stewardship requires visibility.

When leaders can't see the whole picture, they can't govern the whole picture.

Stewardship starts with honesty

A complete financial view builds trust. It helps pastors, finance committees, elders, lenders, and denominational partners understand what the ministry owns, owes, receives, and spends as a whole.

That isn't only practical. It reflects a basic stewardship principle. People who oversee church resources should be able to explain them plainly.

One reason consolidation matters globally is that the practice is tied to transparency in formal accounting standards. IFRS 10, adopted by over 140 jurisdictions, requires parent companies controlling other entities to prepare consolidated statements, and the standard was developed to improve transparency after problems such as Enron, where off-balance-sheet entities hid debt, as summarized in this IFRS 10 overview.

Three ministry benefits

Church leaders usually feel the value of consolidation in three places.

- Clearer board reporting. A consolidated report keeps the board from making decisions based on one strong-looking fund while another part of the ministry is under pressure.

- Better planning. Leaders can weigh opportunities and risks across the entire church, not just within whichever report happens to be on top of the packet.

- Stronger outside credibility. Banks, auditors, and denominational reviewers generally want a complete view, not a patchwork of loosely connected statements.

Practical rule: You can't steward what you can't see clearly.

Church-specific examples

This matters even more in churches than many people expect because church money is often purpose-bound.

A building fund may be healthy, but those dollars are restricted. A preschool may generate revenue, but it may also create payroll, lease, or supply commitments. A campus may receive central support from the main church, and those support flows can blur the actual picture if they're not handled carefully.

A consolidated view helps leadership ask better questions:

| Decision area | What separate reports can miss | What consolidation helps reveal |

|---|---|---|

| Budget planning | One ministry appears strong on its own | The ministry depends on support from another fund |

| Cash oversight | Restricted cash looks available | Some cash can't be used for general operations |

| Debt decisions | Only central obligations are reviewed | Group-wide obligations affect overall risk |

Why this is about ministry, not just mechanics

People sometimes hear “consolidated financial statement” and think of public companies, not congregations.

But the principle is the same. If your church oversees multiple funds, campuses, or controlled ministries, leadership needs one honest report that reflects the whole work. That kind of reporting supports wise planning and protects trust.

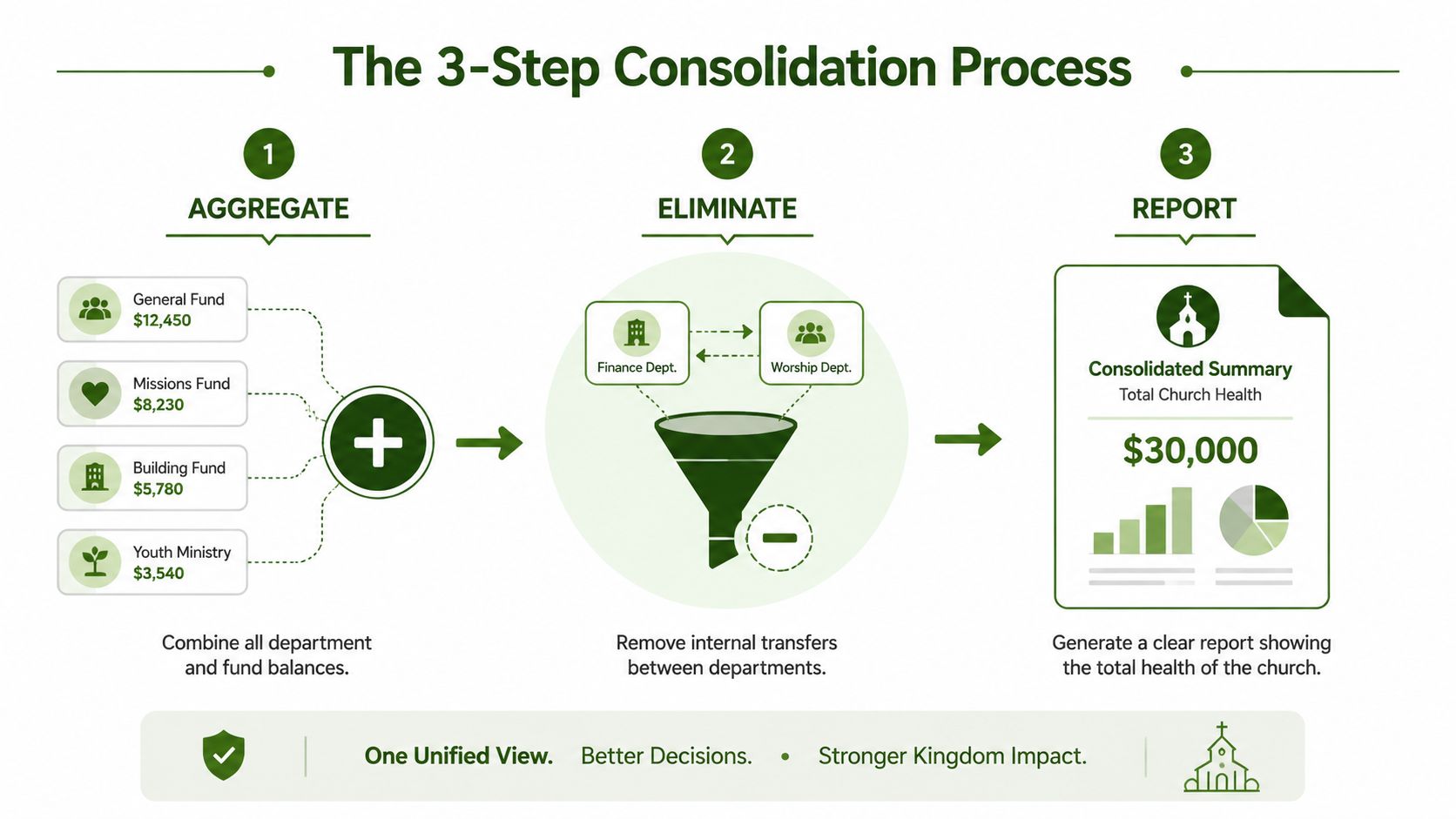

How the Consolidation Process Works Step by Step

The process sounds technical until you break it into a simple workflow. Most church consolidations come down to three actions: combine, remove internal duplication, then present the final report.

Step 1 Aggregate the balances

Start by lining up each entity or fund's statements under the same chart of accounts. Then add them together line by line.

Cash goes with cash. Payables go with payables. Revenue goes with revenue. Expenses go with expenses.

This first pass is just arithmetic. You're building the draft combined report before any cleanup entries.

Step 2 Find internal activity

Readers usually get confused at this point.

If the general fund gave money to the preschool, or the church office paid an expense on behalf of another ministry, both sides may appear in the records. One side shows a receivable or transfer out. The other shows a payable or transfer in.

Those are real entries in the individual books. But from the whole church's perspective, they're internal.

Common internal items include:

- Transfers between funds such as general fund support to a building fund

- Receivables and payables between the church and a controlled ministry

- Internal revenue and expense charges for shared services

- Parent investment balances recorded against a controlled entity

A clean process depends on consistent tagging and data flow. Teams working across several systems often borrow ideas from broader MakeAutomation's integration strategies to reduce mismatches before consolidation even begins.

Step 3 Eliminate what happened inside the group

This is the most important step.

If the general fund transfers money to the building fund, the church hasn't become richer. It has moved money from one pocket to another. If you leave both sides in the combined report, you overstate activity.

When money stays inside the ministry, consolidation removes the duplication so the final report reflects only the group's true position.

Suppose one church fund transfers $10,000 to another. One report may show transfer expense. The other may show transfer income. On the combined statement, both sides should be eliminated.

The same idea applies to internal receivables and payables. If one ministry shows “due from preschool” and the preschool shows “due to church,” the consolidated report should remove both because the group does not owe itself money.

If your team is posting elimination entries manually, a clear guide to how to do journal entries helps keep that work consistent and reviewable.

A broader accounting example illustrates the same principle. The full consolidation method integrates 100% of a subsidiary's financials, and one key step is eliminating the parent's investment against the subsidiary's equity. For example, a $20M investment is canceled against the subsidiary's $20M equity. The same source notes that failing to eliminate intercompany transactions can inflate group assets by 15-30%, which distorts the financial picture, as described in this consolidation example from Prophix.

A short walkthrough can help make that visual:

Step 4 Handle partial ownership carefully

Some churches participate in related ministries they don't fully control. In those cases, the accounting may not look like full consolidation.

If the church doesn't own or control the entity completely, the outside portion may need separate treatment rather than being absorbed without distinction. In corporate language, that outside share is often called a non-controlling interest.

For a church committee, the practical takeaway is simple: if ownership or control is shared, ask your accountant how that relationship should appear before rolling everything into one report.

Consolidation in Action A Church Fund Example

The easiest way to understand consolidation is to watch one happen.

Let's say Grace Community Church has two reporting units. The General Fund supports core ministry operations. The Preschool Fund tracks a preschool ministry. During the year, the General Fund gave the Preschool Fund a $5,000 startup subsidy.

If you add both statements together, that internal support gets counted twice in the combined activity unless you eliminate it.

Simplified Church Consolidation Example

| Account | General Fund | Preschool Fund | Eliminations | Consolidated Total |

|---|---|---|---|---|

| Cash | $50,000 | $12,000 | $62,000 | |

| Due from Preschool | $5,000 | ($5,000) | $0 | |

| Due to General Fund | $5,000 | ($5,000) | $0 | |

| Revenue from external sources | $80,000 | $25,000 | $105,000 | |

| Internal support revenue | $5,000 | ($5,000) | $0 | |

| Internal support expense | $5,000 | ($5,000) | $0 | |

| Operating expenses | $60,000 | $20,000 | $80,000 |

What changed in the consolidated column

The cash balances stay combined because the church group really does control that cash.

The “due from” and “due to” accounts disappear because the church can't owe itself money in the final report. The internal support revenue and internal support expense also disappear because the subsidy wasn't new income to the group. It was an internal movement of resources.

The consolidated column tells the truth the separate columns can't. It shows what the whole ministry has with outside parties after internal duplication is removed.

Why this matters to a finance committee

Without elimination, a committee could look at the reports and think the church had more revenue activity than it really had. They might also think one part of the ministry held a collectible asset that, from the combined perspective, isn't an outside asset at all.

This example also explains why committees get confused when someone says, “But that transaction is real. We recorded it correctly.”

That statement can be true. It was real for the individual books. It just doesn't belong in the final consolidated view because the group is being presented as one economic unit.

Common Pitfalls and Best Practices

Most consolidation mistakes in churches don't come from bad intentions. They come from routine habits that work fine in separate fund reports but create trouble when you combine everything.

Where churches usually stumble

A common problem is forgetting routine internal transfers. If the church regularly moves money between designated funds, those entries can remain in the combined report.

Another issue is inconsistent account naming. One ministry might record support as revenue while another records the same item as a transfer. The books may balance individually, but consolidation becomes messy.

Spreadsheets also create avoidable risk when several people maintain separate versions.

A practical checklist

- Use one chart of accounts. If each ministry labels the same kind of transaction differently, consolidation becomes a cleanup exercise every month.

- Tag internal activity clearly. Mark inter-fund transfers, internal receivables, and shared-cost allocations in a consistent way.

- Reconcile before you consolidate. If one side of an internal balance doesn't match the other, fix that first.

- Write simple policies. A one-page guide for how ministries record transfers, reimbursements, and support payments can prevent repeat confusion.

- Keep an audit trail. Document each elimination entry so the board, bookkeeper, or outside accountant can see why it was posted.

The best practice many churches skip

Review the consolidated report with ministry leaders in plain language.

If the preschool director, treasurer, and senior pastor can all understand why an internal transfer vanished from the combined statement, your process is probably healthy. If only one spreadsheet expert can explain it, the process is too fragile.

Related church budgeting resources

Use these resources together when moving from a spreadsheet budget to cleaner monthly church financial reporting.

- Free church budget generator - build a custom Excel budget template for your church

- Church budget template Excel guide - download and adapt a practical budget template

- Nonprofit budget examples - compare operating, program, and restricted-fund budget formats

- Grain Ledger budgeting - connect budgets to fund accounting and monthly reports

How Church-Focused Software Simplifies Consolidation

Manual consolidation is possible. Many churches do it with spreadsheets, exported reports, and careful month-end journal entries.

But that approach gets harder as soon as the church manages several funds, multiple campuses, or a preschool with separate activity. Generic tools often weren't built around fund accounting, so the team ends up creating workarounds instead of clean reports.

Churches evaluating software often compare broader financial consolidation solutions to understand how automation handles data collection, eliminations, and reporting across entities. For ministry use, though, fund-based design matters just as much as consolidation features.

That's where church-specific software can reduce manual work. Emerging trends suggest that real-time automated consolidation via cloud fund accounting software is becoming more important, with some sources claiming reporting time can be cut by up to 70%, and beta data from some 2026 platforms points to integrated giving, banking, and accounting workflows that can automate multi-fund consolidation for churches, according to this discussion of automated consolidation trends.

One church-focused option is Grain Ledger, which is built around native fund accounting. Because transactions are organized by fund from the start, churches can produce fund-level and combined reporting more cleanly than they typically can in general-purpose bookkeeping systems. If you want to see how that fits into ministry reporting, this overview of fund reporting software is useful.

The main benefit isn't flash. It's reliability.

When your giving platform, bank data, and accounting records connect in one system, leaders spend less time hunting for the right spreadsheet and more time reviewing a report they can trust.

If your church is trying to combine multiple funds, campuses, or ministries into one clear financial view, Grain is worth a look. It's built for church fund accounting, which makes consolidated reporting easier to prepare and easier to explain to pastors, boards, and finance committees.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.