What is an Endowment Fund? Your Guide to Church Financial Legacy

What is endowment fund - Discover what is an endowment fund and how it secures your church's future. This guide covers governance, investing, and accounting for

Ever wish your church had a financial foundation that could support its mission not just for a year, but for generations to come? That’s the core idea behind an endowment fund. It’s a permanent financial gift, a legacy that provides a steady stream of income for your congregation’s work, year after year.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

What Is an Endowment Fund in Simple Terms

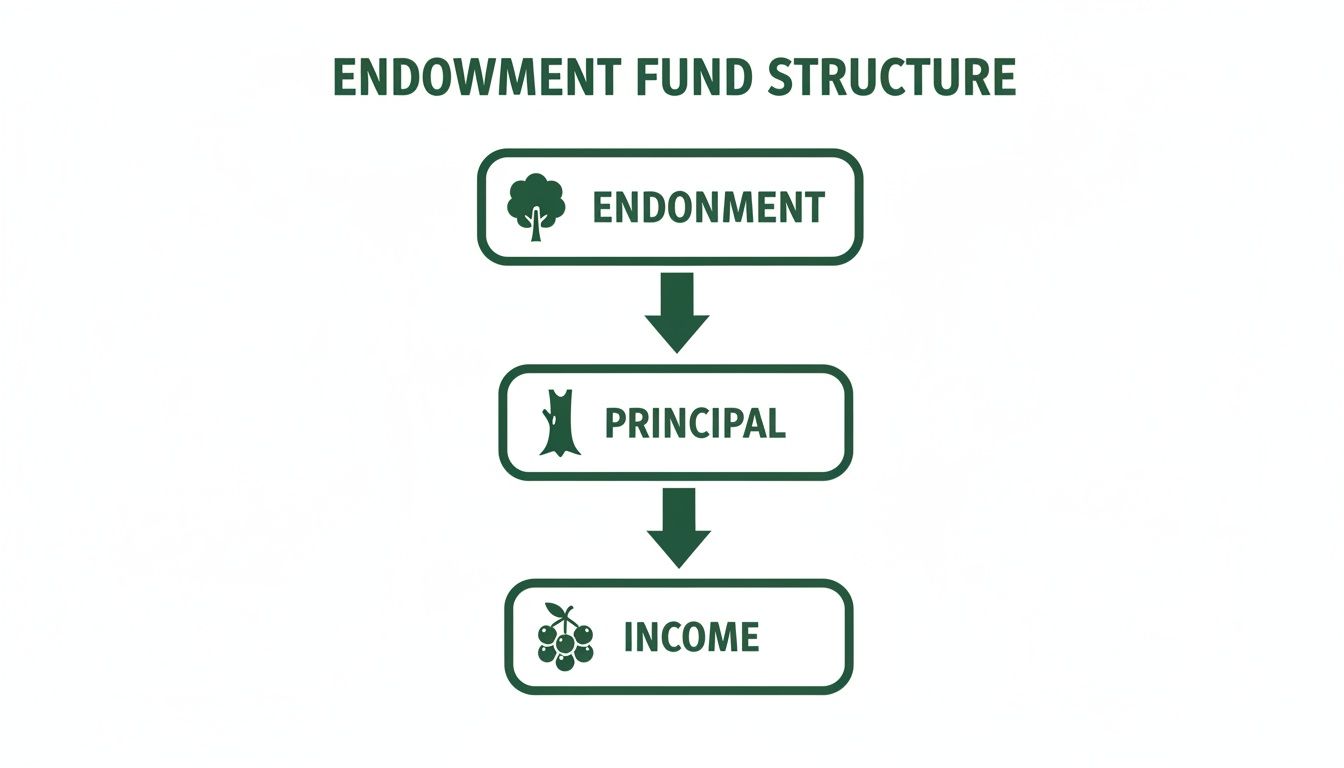

Think of an endowment fund as a financial "fruit tree" for your church. The original donation is the tree itself—the principal—which must be protected and allowed to grow. The income it generates through investments is the fruit. Each year, you can harvest that fruit to support ministry, all without ever touching the tree.

This powerful tool is built from donated assets—like cash, stocks, or even real estate—that are invested for the long haul. The whole point is to preserve the original gift forever while using the investment earnings to supplement the budget, fund specific outreach, or simply provide a rock-solid financial footing for the future.

The Two Core Parts of an Endowment

Every endowment is made of two distinct parts that work in tandem. Getting a handle on their separate roles is the first step to managing one correctly.

- The Principal (or Corpus): This is the original gift. Think of it as the "seed money." By law and by design, this principal is protected and meant to be preserved forever. It’s the engine that generates all future earnings.

- Distributable Income: These are the earnings the fund's investments generate. A portion of this income can be spent each year based on a spending policy your church sets. This is what provides that reliable, ongoing financial support.

To give you a clearer picture, here’s a simple breakdown of these essential components.

Core Components of a Church Endowment Fund

| Component | Description | Church Analogy |

|---|---|---|

| Principal (Corpus) | The original donated sum that is invested and must remain untouched. | The "mustard seed" of faith that is planted and protected to grow. |

| Investment Earnings | The total return generated by the principal (interest, dividends, gains). | The branches and leaves that grow from the original seed. |

| Distributable Income | The portion of earnings that can be spent annually per the spending policy. | The "fruit" that is harvested each year to feed the ministry. |

| Spending Policy | The rule determining how much distributable income can be used each year. | The guidelines for a responsible harvest, ensuring the tree stays healthy. |

This structure creates a sustainable financial resource that can serve your church for decades.

An endowment creates a permanent financial foundation. Major institutions like universities have long relied on them for stability. For instance, in a recent fiscal year, some U.S. higher education endowments reported an average return of 10.9%. Their distributions often fund a significant part of their annual budgets, a testament to the power of this model. You can see more of these findings on Commonfund.org.

How an Endowment Protects Your Church's Future

By keeping the principal separate from the spendable income, an endowment instills financial discipline. It guarantees that a donor's generous gift keeps on giving long after it was made. This is completely different from a general savings account, where the entire balance can be spent down.

Because the principal is untouchable, it demands careful and distinct accounting to track its value and ensure it's never spent by mistake. The rules are strict. This is why many churches find that specialized fund accounting software, like Grain Ledger, becomes essential for managing these complexities.

The legal and donor-imposed rules are what make an endowment a unique type of restricted fund. To see how these differ from other designated accounts, take a look at our detailed guide that explains what a restricted fund is.

Getting to Know the Different Types of Church Endowments

Just like your church has different ministries for different callings, endowments come in different forms, each with its own purpose and rules. As a steward of these gifts, understanding the differences isn't just good practice—it's a core part of your legal and fiduciary responsibility.

It all comes down to the restrictions placed on the funds, either by the donor who gave the gift or by your own church leadership. Getting this right from day one is what ensures donor wishes are honored for generations and keeps the church out of any legal trouble.

True Endowments: The Permanent Promise

A True Endowment, sometimes called a permanent endowment, is the most restrictive type you'll encounter. When a donor establishes one, they are making a legal commitment that the original gift—the principal—can never be spent. Ever. Only the investment income that principal generates is available to support ministry.

Think of it as a gift that keeps on giving, forever. A donor might set up a True Endowment to guarantee the church’s missions program is funded in perpetuity or to create a permanent budget line for maintaining the church building. The bottom line is that the original gift is protected indefinitely.

This diagram helps visualize how the structure works, with the untouchable principal generating spendable income year after year.

You can see how the principal acts like the sturdy trunk of a tree, while the income is the fruit that can be harvested annually for ministry work.

Term Endowments: A Gift with a Timeline

A Term Endowment strikes a balance between permanence and flexibility. With this type of gift, a donor restricts the principal for a set amount of time or until a specific event happens. Once that term ends or the condition is met, the restrictions lift, and your church can then access the principal.

Here are a couple of real-world examples:

- A donor might restrict the principal for 20 years, after which the church can use the entire fund for a major building project.

- A fund could be restricted until the church's mortgage is paid off, at which point the principal is freed up for launching new ministry programs.

This approach provides stable, long-term support while giving the church eventual access to the core funds for a significant, pre-planned purpose.

An endowment can create a powerful and deeply personal legacy. For instance, the Lee Lee Jones Patient Assistance Endowment Fund was set up to provide continuous financial aid for patients needing therapy and medical equipment. The fund's income ensures that a legacy of compassion and care continues indefinitely.

Quasi-Endowments: Board-Designated Flexibility

Finally, we have the Quasi-Endowment, which is by far the most flexible. These funds aren't created by a donor’s legal restriction but by a decision from your church’s own governing board. The board votes to set aside a sum of money, treat it like an endowment, and invest it for long-term growth.

Because the restrictions are self-imposed, the board also has the authority to change its mind and lift them later. This makes Quasi-Endowments an incredibly useful tool for strategic financial planning. A church might start one to save for a future campus expansion or simply to build a healthy reserve fund for unexpected challenges or opportunities.

When looking at long-term giving strategies that can either supplement or become part of an endowment, it's also helpful to compare a donor-advised fund vs private foundation, as each has different implications for how much control and administrative work is involved.

Properly managing the unique accounting for these different funds—tracking principal, investment returns, and spending—is absolutely critical. This is where a true fund accounting system like Grain Ledger really proves its worth. It’s built to handle the complexities of restricted and designated funds, giving you the confidence that your church is maintaining clear, auditable records and upholding its stewardship promises.

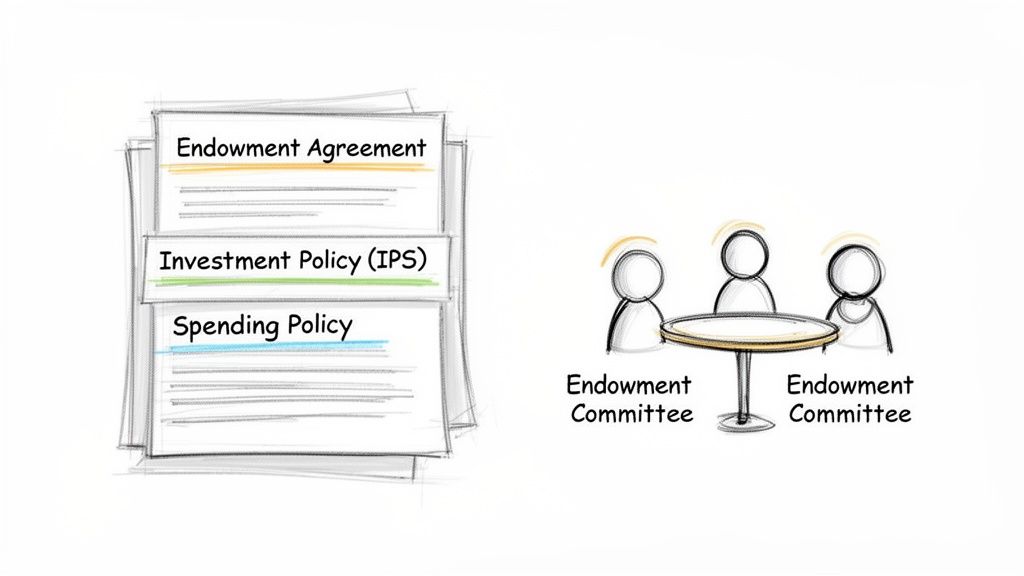

How to Build Your Endowment Governance Framework

An endowment fund is far more than just money in an account—it’s a living promise to future generations of your congregation. To keep that promise, your church needs a strong governance framework. This is simply the set of rules and policies that ensures the fund is managed responsibly, ethically, and exactly as the original donors intended.

Without this solid foundation, you risk mismanaging funds, breaking donor trust, and undermining the very legacy you’re trying to build. These documents are your roadmap, protecting the fund and its purpose for years to come.

Start with an Endowment Fund Agreement

Your very first step is to draft an Endowment Fund Agreement. This foundational document legally establishes the fund and spells out its core purpose. Think of it as the constitution for your endowment, stating clearly how it will operate from day one.

This agreement should define:

- The Fund's Purpose: What specific ministries, missions, or capital projects will the endowment support? Be as clear and precise as you can.

- Fund Type: Will it be a True, Term, or Quasi-Endowment? This decision clarifies the rules around touching the principal.

- Management Structure: Who will be responsible for overseeing the fund?

This document is your primary tool for honoring donor intent and serves as a clear guide for all future church leaders.

Establish a Dedicated Endowment Committee

An endowment is too important to be managed by one person or tacked onto the finance team’s already full plate. It requires focused oversight from a dedicated Endowment Committee. This group is solely responsible for making sure the fund operates according to its governing documents.

Their key duties usually involve selecting investment managers, monitoring performance, and recommending distributions based on the spending policy. While this group works alongside your main finance committee, their responsibilities are distinct. If you'd like to learn more about the roles of a primary financial team, check out our guide on church finance committee responsibilities.

Create an Investment Policy Statement

Next up is the Investment Policy Statement (IPS). This is the official rulebook for how the endowment's assets are invested and managed. An IPS translates your church's mission and values into a disciplined, long-term investment strategy. It provides a framework for making objective decisions, which is crucial for staying the course and not reacting emotionally to inevitable market swings.

A strong IPS must include:

- Investment Objectives: Is the main goal capital preservation, long-term growth, or a balance of both?

- Risk Tolerance: How much risk is the church willing to accept to achieve its desired returns?

- Asset Allocation Strategy: What’s the target mix of assets, like stocks, bonds, and other investments?

- Performance Benchmarks: How will you measure success? This means picking appropriate market indexes to compare your fund’s returns against.

It's worth noting that modern investment strategies are evolving. A recent survey found that institutional investors plan to increase their allocations to private equity by 26% and private debt by 24% over the next three years. They are doing this to capture growth in areas like the energy transition and digital infrastructure. You can see more details in these investment survey results on Mercer.com.

Define a Clear Spending Policy

Finally, you need a Spending Policy. This policy answers the most important question for your annual budget: "How much of the endowment's earnings can we actually use?" It's designed to create a predictable stream of income for ministry while protecting the principal from being depleted, especially during down markets.

A spending policy acts as a crucial guardrail. It prevents the temptation to overspend in good years, which would endanger the fund's ability to provide support in lean years, thereby protecting the endowment’s long-term purchasing power.

One of the most common and effective models is the 'percentage-of-market-value' approach. For instance, a church might set a policy to spend 4% of the endowment’s average market value over the previous three years. This "smoothing" mechanism helps buffer the annual payout from short-term market volatility, giving your budget a more stable and predictable source of income.

Mastering Endowment Accounting and Reporting

Successfully managing an endowment fund is about much more than just smart investing. It requires a very specific, disciplined approach to accounting and reporting that looks quite different from how you handle your church’s general operating budget.

The entire point of endowment accounting is to safeguard the fund’s principal and honor the original donor's wishes. This means you must draw a hard line between the protected principal—the original gift—and the earnings that can be spent. It’s a unique challenge. Your finance team has to meticulously track the endowment's original value (its historic dollar value) and its current market value, which will naturally go up and down with investment performance.

The Challenge of Standard Bookkeeping

This is where many churches run into trouble. Your standard, off-the-shelf business accounting software simply wasn’t built for this. It’s designed to track income and expenses for a single pot of money, making it nearly impossible to enforce the strict boundaries an endowment requires.

Accidentally mixing endowment assets with operational funds is a recipe for compliance headaches and can seriously damage the trust your donors have placed in you.

Let’s say your church receives a $100,000 true endowment. That amount must be recorded and preserved forever as the permanent principal. The investment returns it generates are accounted for separately. If the fund grows to $110,000, you need a system that clearly shows $100,000 in protected principal and $10,000 in unrealized gains, while also tracking how much can actually be distributed according to your spending policy.

Why Fund Accounting is Essential

This is precisely where a true fund accounting system becomes a ministry essential, not a luxury. Unlike traditional software, fund accounting is designed from the ground up to manage your finances as a collection of separate, self-balancing funds. Think of it this way: your general fund, a designated building fund, and your endowment each operate with their own mini-set of books.

This structure provides the control and clarity you absolutely need to manage restricted assets correctly. It creates clear digital walls between different pools of money, preventing the accidental spending of protected principal. For any endowment, clear and accurate financial reporting is a non-negotiable part of good governance. You can explore some general financial reporting best practices that apply here, too.

A dedicated solution like Grain Ledger is built specifically for this reality. As a native fund accounting platform, it tracks restricted and designated assets automatically. This gives your finance team and board the clear, auditable reports needed to demonstrate faithful stewardship.

Using a purpose-built system ensures that every dollar is tracked according to its intended purpose. It automates the critical separation of principal and earnings, making compliance with donor restrictions far more manageable for church staff and volunteers.

Key Financial Reports for Endowment Oversight

Transparent reporting is how you communicate your stewardship to the board, the endowment committee, and the entire congregation. The right reports offer a clear picture of your endowment's health and how it’s supporting your church’s mission.

At a minimum, your reporting should always include:

- Statement of Financial Position: This is like a balance sheet for the endowment. It shows the fund’s total assets (its current market value) and clearly separates the net assets with donor restrictions (the principal) from those without.

- Statement of Activities: This statement tells the story of what happened to the endowment's value over a specific time. It tracks investment returns (both realized and unrealized gains), subtracts fees, and shows the amount distributed based on your spending policy.

- Fund Balance Report: This report zooms in on the endowment fund itself, showing all the detailed activity—inflows from new gifts, investment returns, and outflows from spending distributions.

These reports aren't just for a folder in the church office; they are vital tools for building confidence. They are the proof that you are managing these sacred gifts with the highest level of care and accountability. For a deeper dive into the mechanics, our guide on fund accounting for churches provides even more context.

Developing an Investment Strategy for Your Church

Once your endowment fund is established, the big question becomes: how do we make it grow? A thoughtful investment strategy is the answer. This isn't about chasing risky, high-flying stocks or trying to time the market. It's about creating a disciplined plan that balances steady, long-term growth with careful risk management, ensuring the fund can support your church’s mission for generations to come.

This strategy should be a direct reflection of your church’s values and financial goals. It all gets written down in a crucial document called an Investment Policy Statement (IPS). Think of the IPS as the constitution for your endowment—it’s the north star that guides every decision, keeping your committee objective and mission-focused, especially when the market feels unpredictable.

Demystifying Common Asset Classes

A core component of your strategy is asset allocation, which is simply deciding how to divide your endowment's money among different types of investments. The whole point is to diversify, which is a classic way to manage risk. You’ve heard the old saying: don't put all your eggs in one basket. That’s exactly what we’re doing here.

For most church endowments, the portfolio will be built on two foundational asset classes:

- Equities (Stocks): These represent a share of ownership in a company and are the main engine for long-term growth. While they have the highest potential for returns, they also come with more short-term ups and downs (volatility).

- Fixed Income (Bonds): When you buy a bond, you're essentially lending money to a government or a corporation in exchange for regular interest payments. Bonds are generally less risky than stocks and provide a predictable stream of income and stability to the portfolio.

For example, a look at recent trends shows how this plays out. In fiscal year 2025, much of the growth in large endowments was driven by strong performance in equities, especially technology and international stocks. In fact, some international equity markets did exceptionally well, even outperforming the S&P 500. You can read more about these trends in endowment performance at Tiff.org.

Tailoring a Strategy to Your Church's Goals

So, what's the right mix of stocks and bonds for your church? There's no single correct answer. The ideal blend depends entirely on your church’s specific goals, timeline, and comfort level with risk. Your IPS is where you’ll define which of these approaches best fits your congregation.

To get you started, here are a few common models churches often consider.

Sample Asset Allocation Models for Church Endowments

The table below illustrates three common strategies—Conservative, Balanced, and Growth. These are just starting points, designed to show how you can align your investment mix with your church's unique risk tolerance and financial objectives.

| Strategy Profile | Target Equity Allocation | Target Fixed Income Allocation | Target Alternatives Allocation | Primary Goal |

|---|---|---|---|---|

| Conservative | 20-40% | 60-80% | 0-5% | Capital Preservation: Minimize risk and generate stable income. |

| Balanced | 40-60% | 40-60% | 0-10% | Moderate Growth: A mix of growth potential and capital stability. |

| Growth | 60-80% | 20-40% | 5-15% | Long-Term Growth: Maximize returns over a long time horizon. |

Ultimately, the right strategy is the one that best serves your mission.

A church focused on preserving its historic building might lean toward a Conservative model to protect its principal. On the other hand, a church launching a new global mission with a 50-year vision might feel comfortable with a Growth strategy, knowing it has time to ride out market cycles.

The Role of an Investment Advisor

Let’s be honest: managing an endowment portfolio requires a level of expertise most church committees don’t have. That’s perfectly okay. This is why most churches partner with a professional investment advisor or an institutional consultant.

Their job is to take the strategy you defined in your IPS and put it into action. They help select the specific investments, monitor performance, and provide clear, regular reports to your endowment committee.

This partnership creates a fantastic system of accountability. It frees your committee to focus on its most important job: oversight. The committee ensures the advisor sticks to the plan outlined in the IPS, while the advisor handles the complex day-to-day work of managing the money. This structure ensures your endowment is managed with skill, discipline, and a steady focus on its sacred purpose.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Common Questions About Church Endowments

Once your leadership team grasps the basic idea of an endowment, the conversation naturally shifts. The "what if" and "how-to" questions start bubbling up as you try to picture how this would actually work in the life of your church.

Let's walk through some of the most common questions we hear from congregations. These aren't just financial technicalities; they're the practical, on-the-ground concerns that shape how an endowment serves your ministry.

How Much Money Do We Need to Start an Endowment?

This is almost always the first question, and the answer is probably not what you expect: there is no universal minimum. You don't need a million-dollar check to get started. In fact, many successful endowments begin with a modest "seed" gift of just a few thousand dollars from a single passionate member or a handful of founding families.

The real key isn't the starting dollar amount, but the shared commitment to the long-term vision. An endowment is built to grow over decades, fueled by new gifts and investment returns. A smaller start just means it will take a little longer to produce those big annual payouts.

A great starting strategy is to set a reasonable initial goal—say, $25,000—before the fund starts making distributions. This gives the principal time to grow to a point where the yearly checks, even if small at first, feel meaningful and build momentum.

Frankly, starting small is infinitely better than not starting at all. The simple act of creating the fund opens a door for legacy giving that was closed before.

Can We Use Endowment Money for Emergencies?

This is a critical point, and getting it right is essential for maintaining trust and fulfilling your legal duties. The answer hinges entirely on the type of endowment you have.

For a True Endowment: The answer is a firm no. The principal of a true endowment is restricted by the donor's legal intent—it must be preserved forever. Dipping into it for a leaky roof or a boiler replacement would violate that sacred trust and break the legal agreement you have with that donor. You can only spend the earnings.

For a Quasi-Endowment: The answer here is yes, but with extreme caution. Because a quasi-endowment was created by your own church board, that same board has the power to vote to spend the principal. This should be a true last resort, reserved for a genuine crisis that threatens the church's existence, not for patching a hole in the annual budget.

The best practice? Don't rely on your endowment for emergencies. Instead, build a separate operational reserve or emergency fund for those unexpected capital needs. This protects your endowment's long-term growth engine from being raided for short-term fixes. The endowment is there to secure the future, not mortgage it to solve a problem today.

What Is the Difference Between an Endowment and a Capital Campaign?

While they are both powerful funding tools, they serve completely different functions and operate on different timelines. Confusing the two can lead to muddled messaging and frustrated donors.

Here’s a simple way to think about it: a capital campaign is a sprint, but an endowment is a marathon.

This table breaks down the key differences:

| Feature | Capital Campaign | Endowment Fund |

|---|---|---|

| Primary Goal | Raise a specific amount for a large, one-time project (e.g., a new building, a major renovation). | Build a permanent fund to provide a steady stream of income for ministry, forever. |

| Timeline | A short, intense fundraising push, typically lasting 1-3 years. | A permanent, ongoing fund designed to last for generations to come. |

| Use of Funds | The entire amount raised (the principal) is spent on the project. | The principal is invested and preserved; only the investment earnings are spent each year. |

| Donor Appeal | "Help us build this new sanctuary." | "Help us secure the future of our ministry." |

A capital campaign meets an immediate, tangible need. An endowment meets a perpetual one. Both are vital for a financially vibrant church, but they aren’t interchangeable.

How Do We Communicate About the Endowment?

Clear, consistent communication is the soil in which a healthy endowment grows. Your congregation wants to understand the fund's purpose, see its impact, and trust that it's being managed wisely. Silence breeds suspicion, but transparency builds incredible confidence.

A great communication plan doesn't have to be complicated. It just needs to cover a few key bases:

Tell the "Why" Story: Don't just report numbers. Talk about the ministry the endowment makes possible. Share compelling stories of how the annual distribution helped send kids to camp, supported a missionary, or kept the lights on in your beautiful, historic building.

Report Regularly: Share a simple, clear annual report with the congregation. It should outline the fund's performance, the total amount distributed for the year, and exactly how that money was put to work for the Kingdom.

Celebrate Legacy Givers: With their permission, find meaningful ways to honor members who have included the church in their estate plans. This expresses gratitude and, just as importantly, inspires others to think about their own legacy.

Make It Easy to Give: Make sure the "how-to" is obvious. Information on contributing to the endowment—whether through a current gift or a planned one—should be easy to find on your website, in the bulletin, and through occasional seminars.

By answering these questions openly, you pull back the curtain on endowments and invite everyone to be a part of securing your church’s mission for generations.

Managing the distinct funds for an endowment, a capital campaign, and your general budget requires true fund accounting. Grain Ledger is built from the ground up to provide this clarity, helping you track every restricted dollar with confidence. To see how purpose-built church accounting software can ensure faithful stewardship, get started with Grain Ledger today.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.