Accounting for Deferred Revenue: A Church's Guide

Learn accounting for deferred revenue in your church. This guide explains GAAP, fund-based journal entries, and handling restricted gifts for true stewardship.

The check arrives on Monday morning.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

It’s larger than most gifts your church receives in a week, and the note on the memo line makes your stomach tighten a little: for next year’s building project. You’re the volunteer treasurer, the cash is now in the bank, and the natural instinct is to book it as income and move on.

That instinct is common. It’s also where many churches get into trouble.

When churches lump future-purpose money into current income, the reports can tell the wrong story. Pastors may think the church has more available operating revenue than it really does. Boards may approve spending plans based on numbers that include funds the church hasn’t earned or can’t yet use in the way the general budget assumes. Donors may never see the clean trail that shows their gift stayed tied to its purpose.

That’s why accounting for deferred revenue matters. It isn’t just a technical rule. It’s a stewardship discipline.

Why Deferred Revenue Matters for Your Ministry

A church bookkeeper once described this issue to me in the simplest way possible. “The bank balance says one thing. The responsibility attached to that money says another.”

That’s exactly the tension deferred revenue solves.

Cash received doesn’t always mean revenue earned

Suppose your church receives a large gift for a building project that won’t begin until later. The money is real. The gratitude is real. But the accounting question is different from the ministry question.

If that money relates to a future obligation, future use, or a condition that hasn’t been met, recording it as current income can distort your financial picture. Your statement of activities may look stronger than your actual ministry operations. Your board may think current ministry generated the surplus, when in reality part of that balance belongs to a future commitment.

Churches face a more specific problem than most guides address

Most general articles about deferred revenue explain the basic concept well enough. They say it’s a liability first, and revenue later. That’s true, but churches need more than a general explanation.

Churches work inside fund-based accounting. That means the same dollar amount can look very different depending on donor intent, timing, and whether the church can spend the money now or only after certain conditions are met.

A church also has to distinguish between money that is:

- Restricted and immediately usable for its purpose

- Restricted and not yet earned or not yet released

- Connected to a future ministry service or program

- Received now but tied to later performance

That distinction is where many congregations stumble. An article from Anders notes that guidance is often thin for churches on the difference between restricted donations treated as deferred revenue and other restricted balances, and cites a 2023 AICPA non-profit guide stating that 68% of small congregations’ audit findings stem from fund misallocation (Anders CPA on deferred revenue and nonprofit fund accounting gaps).

Practical rule: If a gift or payment carries a future obligation, don’t let the bank deposit decide the accounting treatment.

Good accounting protects trust

Congregations rarely complain that their church was too careful with donor intent.

They do notice when reports are confusing, when designated funds seem to drift, or when leadership can’t clearly explain what portion of cash is available for ministry today versus committed to tomorrow. Clean accounting gives pastors, elders, finance teams, and donors a shared picture of reality.

For a volunteer treasurer, that clarity is a gift. It means you’re not just “keeping the books.” You’re protecting the story those books tell.

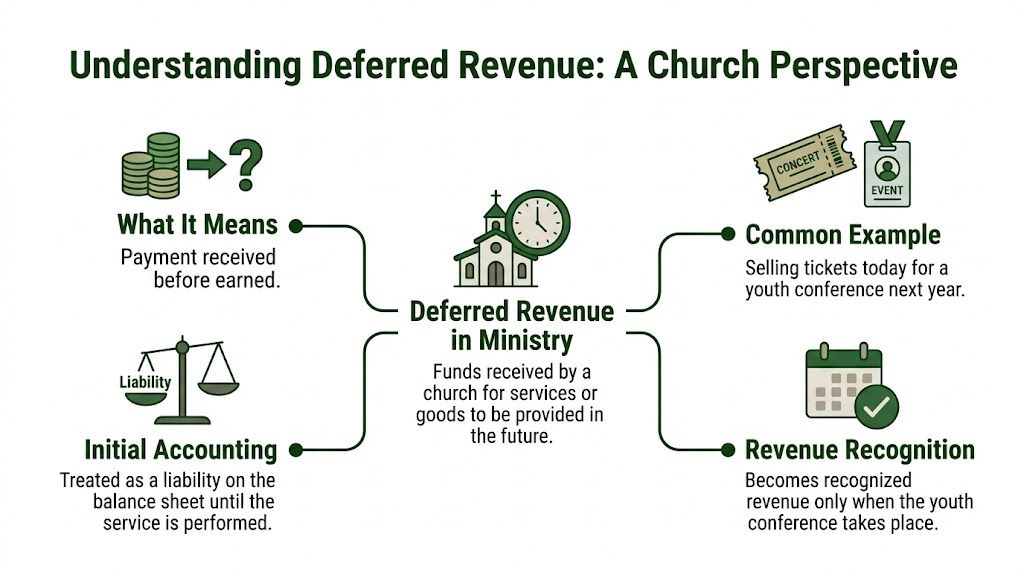

Defining Deferred Revenue in a Church Context

A youth conference your church plans to host next spring provides a clear example. Families register in November and pay in full. The church receives the cash now, but it still owes the conference itself.

That is deferred revenue in plain terms. Money has come in before the church has provided the related program, event, or service.

A clear church definition

Deferred revenue is payment received before the church has earned it by fulfilling its obligation.

That obligation might be a retreat, preschool tuition for future months, paid registrations for a class, or another ministry activity the church has promised to provide later. A concert ticket works as a useful comparison. Payment comes first. Attendance happens later. Until the event takes place, the organization still owes something.

Churches often see deferred revenue in situations like these:

- Prepaid event fees for retreats, camps, or conferences

- Program or class payments collected before the start date

- Advance payments for future ministry services

- Certain conditional gifts or pledges tied to a later milestone or action

Why the money starts as a liability

New treasurers often get stuck here, and for good reason. The bank account increased, so calling the receipt a liability can feel backward.

A better way to view it is this: the church is holding money connected to unfinished ministry work. Until that work is completed, the amount belongs on the statement of financial position as a liability. In church bookkeeping, liability does not mean something improper happened. It means the church still owes delivery, access, instruction, care, or event participation.

Later, when the church provides what it promised, the amount moves out of liability and into revenue. If you want more background on how church reporting categories fit together, this guide to FASB ASC 958 for churches and nonprofits helps frame the bigger picture.

To visualize the flow:

| Stage | What happened | Where it belongs |

|---|---|---|

| Payment received | Cash came in before the service or event occurred | Liability |

| Ministry delivered over time | The church fulfills the obligation | Revenue recognized gradually |

| Obligation completed | Nothing remains to be earned | Liability reduced to zero |

A quick visual can help if you’re training a finance committee or ministry leader:

Deferred revenue and restricted gifts are not the same thing

This is the church-specific distinction that causes trouble.

A restricted gift can be recognized as contribution revenue when received, even though the church must use it for a designated purpose. For example, a donor may give to the building fund or benevolence fund. The gift is restricted by donor intent, but the church may not owe the donor a future service, event, or deliverable in return.

Deferred revenue is different. It applies when the church has accepted payment and still has a remaining performance obligation. In other words, the accounting question is not only about donor restriction. It is also about whether the church has already done what the payment relates to.

The essential question isn’t only “Is this restricted?” The better question is “Has the church already earned or fulfilled what this money relates to?”

That is why two receipts can look similar in a fund-based system and still belong in different places. One may increase contribution revenue within a restricted fund. Another may sit in a deferred revenue liability account until the church provides the conference, class, or service. If you need a broader explanation of the revenue recognition principle under ASC 606, that framework helps explain why timing matters so much.

For a volunteer treasurer, this is the habit to build: before posting any unusual receipt, ask what the church still owes, who placed the restriction, and whether the payment belongs to a fund balance or to a liability account. That one pause prevents a lot of cleanup later.

Understanding Revenue Recognition Under GAAP

A church collects retreat fees in October for an event that will not happen until January. The bank balance goes up right away. Revenue does not.

That timing difference sits at the center of GAAP revenue recognition. The rule is straightforward: record revenue when the church has provided the promised goods or services, not when cash arrives. For ministries, that matters because a full bank account can still include money tied to work the church has not yet completed. If you want a broader refresher on the revenue recognition principle under ASC 606, that framework helps explain why timing and performance stay connected.

The five-step model in plain language

Volunteer treasurers rarely need the formal wording. You do need the sequence.

Identify the agreement

What arrangement exists between the church and the payer? In ministry settings, that could be a preschool registration, conference fee, counseling package, or prepaid facility use agreement.Identify the promises within that agreement

What has the church committed to provide? The answer might be event access, weekly classes, childcare, materials, or use of a room over a set period.Determine the amount to be recognized

Confirm how much payment belongs to that agreement.Assign the amount to each promise, if there is more than one

If a registration fee covers meals, lodging, and training sessions, the church should decide how those parts fit together for recognition purposes.Recognize revenue as the church fulfills each promise

Revenue belongs in the period when ministry activity occurs.

A helpful way to remember this is to treat revenue like a receipt with a timestamp. Cash answers, "When were we paid?" Revenue answers, "When did we earn it?"

A church-friendly example

Suppose your church receives $12,000 upfront for a year-long software subscription used by a ministry team. On the day the payment arrives, the church has the cash, but it still owes twelve months of access. The amount starts in deferred revenue. Then, as each month of access is provided, part of that liability becomes earned revenue.

The same pattern applies to many church operations:

- preschool or childcare tuition billed before services are provided

- conference registrations paid months in advance

- recurring facility use arrangements

- multi-week classes or training programs

Why GAAP matters in a fund-based church system

Church accounting is more nuanced than a generic business example.

In a church, the right answer is not found by asking only whether cash was received or whether a fund is restricted. You also have to ask whether the church still owes a service, event, or other deliverable. That is the point many ministries miss. A donor-restricted gift and deferred revenue can both be tracked carefully in the accounting system, but they do not mean the same thing.

A restricted contribution affects net asset classification. Deferred revenue is a liability. One reflects donor intent. The other reflects an unfulfilled promise.

That distinction becomes clearer when you read revenue recognition alongside nonprofit reporting guidance such as FASB ASC 958 for churches. Churches need both lenses. One helps you classify support. The other helps you decide whether a receipt has been earned.

Where churches usually get confused

Church finance teams usually get tripped up by three separate questions:

- When did the money arrive?

- Did the donor or payer restrict its use?

- Has the church fulfilled what the payment relates to?

Those questions often overlap, but they do not always lead to the same accounting result.

For example, a prepaid marriage course fee may belong in deferred revenue because the class has not happened yet. A building fund gift may be recognized as contribution revenue when received, even though its use is restricted. In both cases, the church may place the activity in the proper fund for reporting purposes, but only one involves a liability for future performance.

If you can answer, "What did the church promise, and when was that promise fulfilled?" you can usually sort deferred revenue from restricted support with much more confidence.

Recording Deferred Revenue with Fund-Based Journal Entries

Theory helps. Journal entries make it real.

Let’s use a church example that many treasurers can picture quickly: a prepaid fee for a marriage course.

The basic entry when money comes in

Assume your church collects $2,400 before the course begins. The course will be delivered over 12 weeks, and the church plans to recognize the amount evenly over that service period.

When the cash arrives, don’t credit revenue yet if the course hasn’t started. Record the receipt as a liability tied to the correct ministry fund.

| Account | Debit | Credit |

|---|---|---|

| Cash | $2,400 | |

| Deferred Revenue | $2,400 |

That entry says: the church received the cash, but it still owes the course.

The adjusting entry as the ministry is delivered

If the church recognizes the fee evenly across the service period, the amount recognized each month depends on the schedule your finance team adopts. In this example, if you spread the $2,400 over 12 months, the monthly recognition would be $200.

The adjusting entry would be:

| Account | Debit | Credit |

|---|---|---|

| Deferred Revenue | $200 | |

| Revenue | $200 |

That reduces the liability and records earned revenue.

What matters most is consistency between the ministry timeline and your recognition schedule. If the course runs across a shorter period, your team should align the recognition pattern with the period in which the church provides the course.

Why fund-based tagging matters

In this area, general accounting software often creates headaches for churches.

If the deferred amount relates to a marriage ministry activity, the entry shouldn’t just hit a generic liability and a generic revenue line. It should remain visible inside the correct fund or ministry reporting structure so leaders can see:

- what cash has been received

- what portion is still unearned

- which ministry area carries the obligation

- how much has moved into revenue so far

Without that structure, the books may technically balance while the ministry story is still unclear.

A practical workflow for monthly close

For most churches, the cleanest process looks like this:

Record the receipt immediately

Post cash and deferred revenue when payment is collected.Attach supporting detail

Keep the event list, registrations, dates, and ministry owner with the transaction records.Set a recognition schedule

Use a recurring monthly entry or a close checklist so nobody forgets the release.Review by fund or ministry area

Confirm the deferred balance still makes sense in context.

If your team wants a practical refresher on entry structure, this guide on how to do journal entries is a helpful church-focused reference.

For churches evaluating systems that can handle these workflows well, this roundup of best accounting software for nonprofits can help you compare how different tools approach nonprofit accounting needs.

Clean deferred revenue accounting isn’t about fancy debits and credits. It’s about making sure each ministry receipt stays connected to the reason it was received.

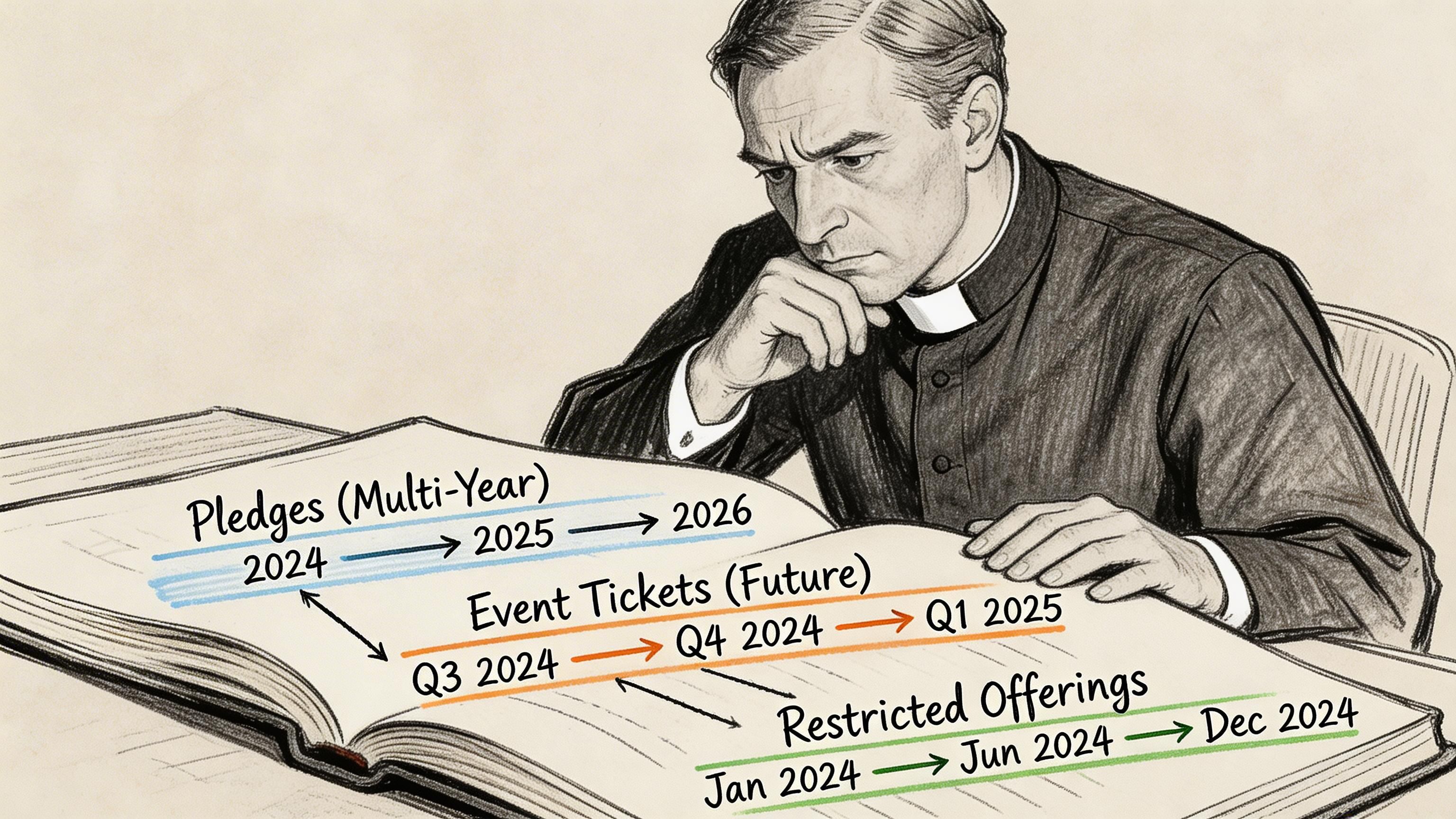

Handling Common Church Scenarios Pledges Events and Offerings

Most deferred revenue mistakes don’t happen on ordinary Sunday deposits. They happen in unusual situations, especially when timing and donor intent overlap.

Multi-year pledges for a campaign

A capital campaign is where many church finance teams first run into this issue.

If a church receives money for a future project and the amount is tied to conditions, milestones, or future program delivery, it may need to be carried as a liability rather than treated as immediately earned revenue. One church-focused source notes that in fund-based accounting, deferred revenue from restricted donations such as multi-year building fund pledges must be recorded as a liability, and gives the example of a $12,000 pledge for a 12-month mission program initially recorded as Debit Cash $12,000 and Credit Deferred Revenue (Restricted Fund Liability) $12,000, with $1,000 recognized monthly as services occur. The same source warns that failure to defer can trigger IRS scrutiny under Section 501(c)(3) rules, and states that 15-20% of audited nonprofits face penalties for premature recognition (Zenskar on deferred revenue for churches and nonprofit penalties).

That doesn’t mean every campaign pledge is deferred revenue. The treasurer has to examine the nature of the promise.

Ask:

- Is the promise unconditional? If so, the treatment may differ from a conditional arrangement.

- Is there a milestone or future condition? That leans toward liability treatment until the condition is met.

- Can the church spend it now for the stated purpose, or is something still pending?

A finance committee should document that conclusion before the first large pledge payment hits the books.

Prepaid fees for ministry events

Event accounting is more straightforward, but churches still get tripped up.

Suppose families pay in advance for VBS, camp, or a mission trip. If the event hasn’t happened yet, the church is still holding money connected to future delivery. Recording all of it as current revenue can make one month look unusually strong and leave later months looking artificially weak.

A better approach is to recognize revenue as the church delivers the event or as the related ministry services occur. In practice, churches often do this through a schedule tied to event dates, phases, or the period of service.

For registration systems and online giving tools such as Pushpay or Stripe, the key is passing enough detail into accounting so the receipt lands in the right fund or event bucket. If the intake system only says “donation” or “payment,” somebody later has to untangle what it was for.

Offerings with time conditions

Another common scenario is a special offering for a future ministry activity, such as “next year’s Easter outreach” or “summer mission support.”

Here, treasurers must slow down and separate two questions:

| Question | Why it matters |

|---|---|

| Is the gift restricted to a purpose? | This affects how the church tracks and reports the funds |

| Is the money earned or available now, or tied to a future condition or obligation? | This affects whether it belongs in revenue or a liability account first |

Those questions don’t always produce the same answer.

A donor restriction by itself doesn’t automatically create deferred revenue. But if the church still has to meet a condition or fulfill a future obligation before treating the amount as earned, deferral may be appropriate.

Many church accounting errors happen because teams ask only “what fund is this for?” and forget to ask “has the church earned it yet?”

Automation helps only if setup is right

Churches increasingly rely on integrated tools. That’s good, but automation can spread bad assumptions quickly if the mapping is wrong.

Before connecting your giving platform to your ledger, confirm:

- Fund mapping is clear so building gifts, event fees, and mission receipts don’t land in one generic account.

- Restrictions are captured at intake through forms, designations, or campaign settings.

- Deferred items are flagged so they don’t flow straight into earned revenue by default.

- Monthly review still happens because no integration can replace judgment.

If you want more ministry-specific examples, this collection of deferred revenue income examples for churches can help you compare similar transactions before you post them.

Internal Controls and Financial Reporting for Deferred Revenue

A correct journal entry on day one isn’t enough.

Churches also need a simple control system so deferred revenue stays accurate month after month. Without that follow-through, the liability account turns into a parking lot for old balances, and leadership loses confidence in the reports.

The reconciliation every church should maintain

At minimum, keep a deferred revenue schedule that ties each balance to a real obligation.

That schedule should show:

- What the receipt was for

- When it was received

- Which fund or ministry it belongs to

- When revenue should be recognized

- What balance remains

Then compare that schedule to the general ledger at close. If the ledger says one amount and the support says another, stop and resolve it before board reports go out.

A deferred revenue balance without a supporting schedule is a warning sign, not a finished accounting process.

What pastors and boards should see

Church leaders don’t need every accounting detail. They do need reports that separate available operating resources from amounts still tied to future obligations.

A useful board packet will usually make it easy to answer:

- What part of cash is available for current ministry operations?

- What part is restricted by fund?

- What part is still deferred because the church hasn’t fulfilled the obligation yet?

When those categories blur together, leaders can authorize spending they didn’t mean to authorize.

The tax timing issue many churches overlook

Deferred revenue can also create a book-tax timing difference. One source explains that GAAP may defer recognition until earned, while the IRS may require immediate taxation upon cash receipt for advance payments, which means churches and nonprofits need to track the difference through M-1 reconciliations. The same source notes that under ASC 740, these liabilities are classified as current if due within 12 months and non-current if longer, and gives the example that a $50K annual pledge could produce a meaningful deferred tax asset effect (indinero on deferred revenue, tax timing, and ASC 740).

Not every church will deal with that in the same way, and many volunteer treasurers will involve an outside CPA for tax treatment. Still, it’s important to know the issue exists. If your church receives significant advance payments, your book treatment and tax treatment may not move in lockstep.

Strong controls are simple, not fancy

You don’t need a complex policy manual to improve this area.

A solid control environment usually includes a short monthly checklist, a schedule that ties to the ledger, a reviewer who asks questions, and board reporting that distinguishes earned revenue from future obligations. Churches that do those few things well avoid many of the most painful cleanup projects.

Achieving Financial Clarity and Stewardship

When churches handle deferred revenue well, the books become easier to trust.

Cash in the bank no longer gets confused with earned ministry revenue. Restricted amounts stay visible. Future obligations stay visible too. Pastors can lead from cleaner information, and finance teams can explain the numbers without hedging.

That’s why accounting for deferred revenue is more than compliance work. It’s a way to honor donor intent, protect ministry plans, and keep financial reports honest.

The pattern is straightforward:

- receive the money

- determine whether the church has earned it

- record it in the correct fund and category

- recognize revenue only when the obligation is fulfilled

- reconcile the balance until it reaches zero

For volunteer treasurers, that approach removes a lot of uncertainty. You don’t have to guess based on what feels reasonable in the moment. You can ask better questions and apply a consistent method.

Churches that grow often outgrow generic bookkeeping habits first. They need records that reflect how ministries operate, how designated gifts function, and how board oversight works. Deferred revenue sits right in the middle of all three.

Good stewardship is easier when the accounting tells the truth early.

Compare platforms in our best church accounting software guide for 2026, or review Grain Ledger church accounting software.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Frequently Asked Questions About Church Deferred Revenue

What’s the difference between a pledge and a conditional promise to give

A pledge is often understood as a donor’s commitment to contribute. A conditional promise to give includes a hurdle that must be met first.

That difference matters. If the church must still meet a condition or milestone before treating the amount as earned or available in the same way as ordinary revenue, the accounting may point toward deferral or another liability treatment rather than immediate recognition.

When the wording is unclear, review the donor communication, campaign language, and any written agreement before posting the receipt.

How should we handle refunds for a prepaid event that gets canceled

Start with what the church still owes.

If the church collected money for an event that never happens, the deferred balance usually shouldn’t be recognized as revenue just because the calendar changed. If refunds are issued, reverse the liability against cash. If part of the amount was already recognized before the cancellation, your accountant may need to reverse the earned portion based on what was or wasn’t delivered.

Keep documentation for the cancellation decision and the refund process.

If we receive a grant with a time stipulation, is that deferred revenue

It can be, depending on the grant terms.

The key question is whether the church has already met the requirements attached to the grant. If not, the amount may need to stay out of earned revenue until the time or performance condition is satisfied. If the church has already met the conditions and the grant is restricted in use, the treatment may differ.

This is one of those areas where reading the award letter carefully matters more than the label on the payment.

Does deferred revenue affect our annual budget planning

Yes, because budgeting and accounting answer different questions.

Your accounting records show what has been earned and what remains a liability. Your budget shows how leadership plans to use resources. If those two views aren’t aligned, a church can budget against cash that isn’t yet earned or available in the way leaders assume.

A strong budget discussion should identify which balances are operating, which are restricted, and which are still deferred.

What’s the fastest way to reduce confusion on our team

Use the same decision path every time money comes in:

- What was the payment for?

- Is it restricted?

- Has the church earned it yet?

- Does a future service, event, or condition remain?

- Which fund and account should hold it until then?

That simple sequence catches most mistakes before they hit the financial statements.

If your church wants a system built around true fund accounting instead of workarounds, take a look at Grain. Grain is purpose-built for churches, with native fund architecture that helps keep restricted balances, deferred amounts, and ministry reporting aligned from the start. It’s a strong fit for churches that want clearer books, cleaner reporting to boards and pastors, and better stewardship over every dollar.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.