Accounting Standards for Nonprofit Organizations: Churches

Master accounting standards for nonprofit organizations. This guide for churches covers FASB, fund accounting, & compliance for stewardship.

The finance committee packet is open, the treasurer is looking at a designated gift, and the question sounds simple until it isn't. A family gave money for youth outreach. The church's aging A/V system in the youth room just failed. The students use that room every week. Is that outreach, operations, or a building expense that has to come from somewhere else?

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

That kind of question sits at the center of accounting standards for nonprofit organizations. It isn't mainly about satisfying an auditor or checking an IRS box. It's about whether the church can show, clearly and transparently, that it handled God's money in line with donor intent, board oversight, and good stewardship.

Churches often get into trouble because leaders treat accounting rules as technical paperwork instead of ministry guardrails. When records are vague, people start relying on memory, assumptions, and verbal understandings. That's when restricted gifts get stretched, reports lose credibility, and trust erodes faster than anyone expected.

Stewardship Starts with Clarity

A church treasurer usually doesn't face accounting questions in the abstract. The question is whether a dollar received for one purpose can support another need that also feels ministry-related.

Take the youth outreach gift. If the donor intended those funds for outreach events, supplies, transportation, or scholarships, replacing the youth room sound system may not fit. If the donor's language was broad enough to include ministry tools used in that outreach, there may be an argument for it. But the answer can't come from guesswork. It has to come from the wording of the gift, the church's records, and a disciplined process for approval and documentation.

Practical rule: If a church can't explain a fund's purpose in one plain sentence and show where that purpose is documented, the accounting problem started before the journal entry.

That's why church accounting has to begin with clarity, not software screens or report formats. Donors need confidence that designated gifts stay designated. Pastors need reports that reflect what funds are available. Boards need to know whether cash in the bank is spendable or already committed to a mission trip, benevolence effort, or building project.

Good stewardship has a financial reporting side. It also has a pastoral side. People give more freely when they trust the church to honor their intent. People become cautious when they suspect that “restricted” really means “restricted until leadership has another idea.”

A church that follows sound accounting standards for nonprofit organizations isn't being cold or bureaucratic. It's doing the opposite. It's protecting ministry relationships with careful records, plain reporting, and decisions that can withstand scrutiny.

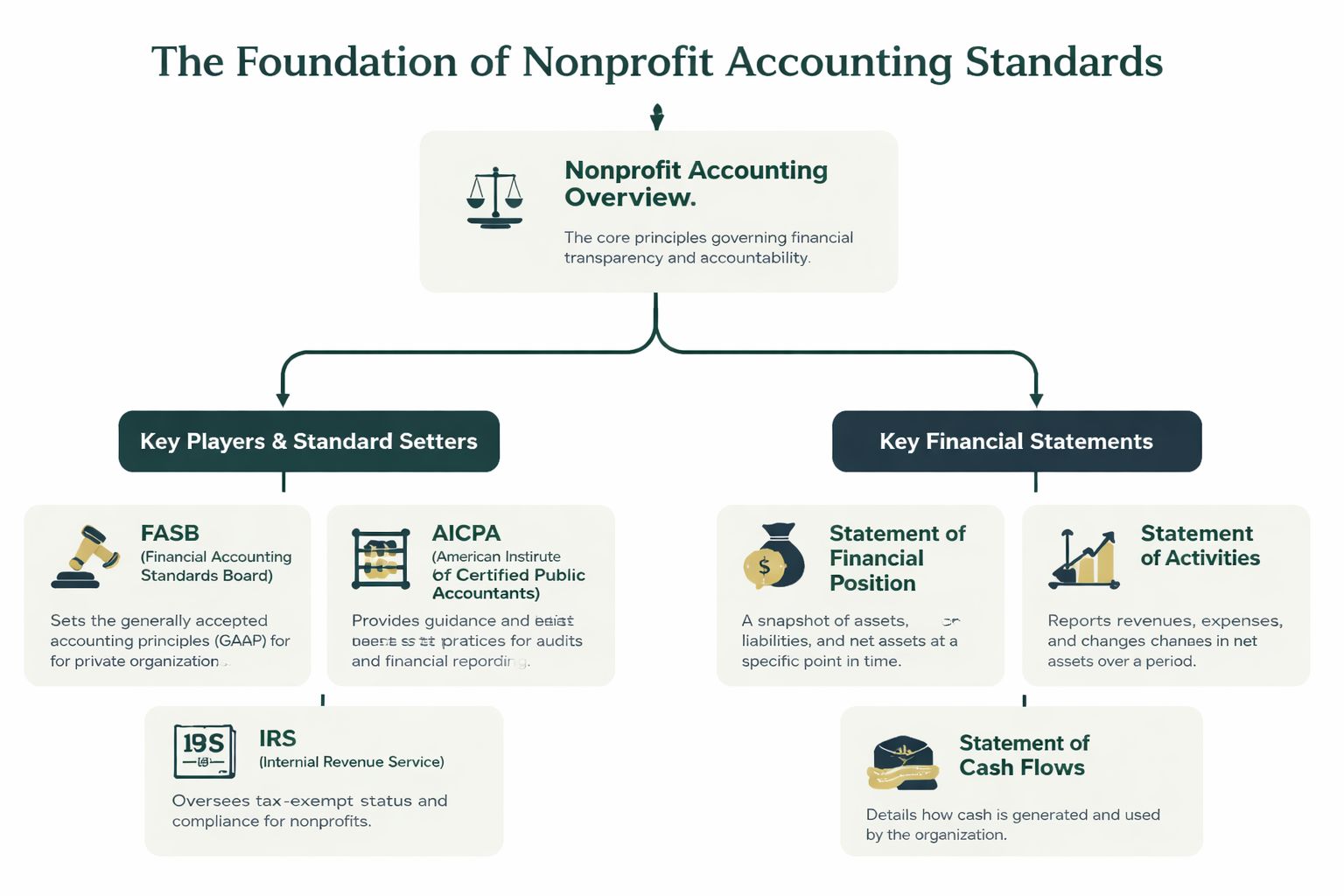

The Foundation of Nonprofit Accounting

Church finance teams hear a lot of acronyms, but the structure is straightforward once you line it up correctly. GAAP is the overall framework. FASB is the standard setter. ASC 958 is the section that governs not-for-profit entities, including churches.

GAAP requires churches that follow it to use accrual accounting, which means revenue is recorded when pledged and expenses when incurred, not only when cash moves. GAAP also requires four core financial statements for nonprofits: the Statement of Activities, Statement of Financial Position, Statement of Cash Flows, and the Statement of Functional Expenses, as summarized by The Charity CFO's explanation of nonprofit accounting compliance.

Who sets the rules

FASB established ASC Topic 958, Not-for-Profit Entities, as the framework for nonprofit financial reporting in the United States. That matters for churches because a ministry may feel informal operationally while still needing formal financial reporting.

Three practical layers usually matter to a church finance committee:

- GAAP as the framework means the church reports financial activity using recognized accounting principles, not improvised local practices.

- FASB as the rule-maker means changes in nonprofit accounting standards come from a formal standard-setting body, not from denominational habit.

- ASC 958 as the nonprofit chapter means churches need nonprofit-specific treatment for net assets, donor restrictions, and expense presentation.

Why accrual beats cash for stewardship

Cash accounting answers one narrow question: what cleared the bank. It doesn't answer whether a church has already committed restricted resources, owes vendors for ministry work already performed, or has promises receivable from a campaign.

That's why accrual accounting is the standard. If a member pledges support for a building campaign, a cash-only system can hide the commitment until checks arrive. If the church incurs camp expenses in June but pays the bill in July, a cash-only report can distort the true cost of the program period.

A church can have cash in the bank and still have less spendable flexibility than leaders think. Fund accounting under accrual reporting makes that visible.

What the four statements actually tell you

A healthy finance committee doesn't just receive statements. It knows what question each statement answers.

| Financial statement | What it tells the committee |

|---|---|

| Statement of Financial Position | What the church owns, owes, and holds in net assets at a point in time |

| Statement of Activities | How revenue and expenses changed net assets during the period |

| Statement of Cash Flows | How cash moved through operating, investing, and financing activities |

| Statement of Functional Expenses | How spending breaks down by natural and functional categories |

When these statements are prepared correctly, they don't just satisfy reporting standards. They give pastors, treasurers, and elders a clearer picture of ministry capacity.

Understanding Your Net Assets Under ASU 2016-14

One of the most helpful changes in recent nonprofit reporting was also one of the most misunderstood. ASU 2016-14 simplified net asset presentation by moving nonprofits from three classes to two. Under this update, organizations now present net assets with donor restrictions and net assets without donor restrictions. They no longer present “temporarily restricted” and “permanently restricted” as separate line items on the statement of financial position, as described in HCVT's overview of the nonprofit standard update.

For church leaders, this is more than a terminology update. It changes how the balance sheet communicates available versus constrained resources.

The old labels versus the current ones

Here's the comparison most church finance teams need in front of them.

| Net Asset Classification Changes (ASU 2016-14) | |

|---|---|

| Old Classification (Pre-ASU 2016-14) | New Classification (Post-ASU 2016-14) |

| Unrestricted | Net assets without donor restrictions |

| Temporarily restricted | Net assets with donor restrictions |

| Permanently restricted | Net assets with donor restrictions |

The change reduced clutter, but it didn't reduce responsibility. Churches still have to track the nature of restrictions internally. A building gift, a scholarship fund, and a future-year ministry gift can all sit inside “with donor restrictions” on the face of the financial statements while still requiring distinct internal tracking.

What a committee should look for

A practical review starts with the balance sheet. If the church reports one lump total for restricted activity but can't break it down by purpose or timing, the reporting may be technically incomplete for management purposes even if the presentation looks tidy.

Three questions help:

- Can we identify each donor-restricted fund clearly?

- Can we show when a restriction was satisfied?

- Can we document the reclassification out of restriction when appropriate?

Churches that want a deeper working knowledge of the standard should also review this practical guide to FASB ASC 958.

The balance sheet should never leave the board guessing which dollars are free for current ministry and which are bound to donor intent.

Another point often missed is that simplification on the financial statement doesn't mean simplification in the ledger. In practice, churches need better internal fund tracking, not less, because the public-facing categories are broader than the detailed stewardship work happening behind them.

Applying Standards to Common Church Scenarios

The standards become clearer when you run them through normal church activity instead of accounting theory.

A Sunday offering can include unrestricted tithes, missions gifts, benevolence support, and a special donation for the youth retreat all in the same deposit. If the church books the whole deposit into one general income account and plans to “sort it out later,” errors multiply quickly. Restricted gifts need to be identified when received, tied to the correct fund, and reported in a way that preserves donor intent from day one.

A building campaign creates a different challenge. A member signs a multi-year pledge for a future expansion project. The church can't treat that promise like loose cash for current ministry operations. The pledge affects reporting before all the cash arrives, and the related fund remains restricted to the stated purpose.

Weekly giving that mixes restricted and unrestricted funds

A common pattern looks like this:

- General tithes and offerings belong in net assets without donor restrictions unless the donor imposed a restriction.

- Mission trip gifts belong in a restricted fund tied to that purpose.

- Benevolence gifts should stay in the benevolence fund unless the donor language allows broader mercy ministry use.

- Building gifts remain restricted to the project identified by the donor.

What doesn't work is relying on memo lines only at the bank or asking staff to remember donor intent later. The accounting entry has to reflect the restriction at the time of receipt.

When a restriction is satisfied

A church receives gifts for a student mission trip. The funds sit in the mission trip fund until qualifying trip costs are incurred. Once the trip expenses are recognized and the restriction has been met, the church reclassifies those amounts appropriately.

That reclassification is where many churches slip. They may spend the money correctly but leave it sitting in restricted net assets for months because nobody processed the release.

Here's a useful walkthrough before that point in the workflow:

The rainy day myth

Churches sometimes assume a restricted balance can stay parked indefinitely after the qualifying event occurs. That isn't how the standard works. ASC 958-205-45 states that net assets with donor restrictions must be utilized first when the restriction is met and can't be held for future unanticipated needs, as explained in Nonprofit Accounting Basics on GAAP and donor restrictions.

That matters in ordinary church life. If donors gave for a roof replacement and the roof work is completed, the church shouldn't keep those funds in a restricted bucket as a hidden reserve for the next emergency unless the donor restriction supports that treatment.

If the purpose or time restriction has been met, the church needs to release it properly. Stewardship isn't just spending the money correctly. It's reporting the release correctly too.

The same principle applies to time-bound grants and future-year gifts. Once the timing condition or purpose condition has been satisfied, the accounting needs to show it. Leaving funds “restricted forever” after the condition expires is just as misleading as spending them too early.

Functional Expenses and Lease Accounting Explained

Two areas create repeated confusion for church finance teams: functional expenses and lease accounting. Both feel technical at first. Both make more sense once you focus on what the reports are trying to show.

FASB ASC Topic 958 requires nonprofits to report expenses by natural classification and functional classification. Separately, ASC 842 requires GAAP-following nonprofits to recognize lease liabilities and right-of-use assets on the balance sheet for fiscal years beginning after December 15, 2019, according to Sage's summary of nonprofit accounting standards.

Functional expenses in church terms

Natural categories are the type of expense. Think salaries, rent, insurance, utilities, curriculum, or software subscriptions.

Functional categories answer a different question. Why was that cost incurred?

A church usually needs to sort spending into these buckets:

- Program services for worship, discipleship, missions, children's ministry, student ministry, care ministries, and similar mission-facing work

- Management and general for governance, finance, administration, and overall operations

- Fundraising for activities directly tied to raising contributions

That doesn't mean every payroll line is easy to split. A church administrator may support ministries and also handle office management. A facilities cost may support both worship and administration. The work is in establishing a reasonable allocation method and applying it consistently.

For a more detailed treatment of that report, this guide on the statement of functional expenses for churches is worth reviewing.

Lease accounting without the jargon

ASC 842 matters even to churches that never thought of themselves as “lease-heavy.” A leased copier, office space, ministry building, or similar arrangement may now need balance sheet recognition rather than footnote-only treatment.

That change is important because it puts the economic obligation on the face of the financial statements. A finance committee can no longer look only at cash and debt in the traditional sense. It also has to understand lease-related liabilities and the corresponding right-of-use assets.

What works here is a deliberate inventory. Pull every contract that might contain a lease. Read them with operational leaders, not just the bookkeeper. Churches often miss agreements because they're buried in facility use arrangements, ministry partnerships, or older administrative files.

Ensuring Compliance with Audits and Internal Controls

Many churches think fraud prevention means trusting the right people. Trust matters, but it isn't an internal control. A sound control system assumes good people can still make mistakes and that pressure can distort judgment.

GAAP compliance requires segregation of duties, meaning the roles of authorizing a transaction, recording it in the ledger, and reconciling the bank statement must be assigned to different individuals, as outlined in Sage's nonprofit internal control guidance.

Segregation of duties in a church office

In plain terms, the person who approves an expense shouldn't also cut the check and post the entry. The person who records giving shouldn't be the only person reviewing the deposit. The person reconciling the bank account shouldn't be the same person handling all cash receipts.

That can feel hard in a smaller church. Staff is limited. Volunteers rotate. Roles overlap. But limited headcount doesn't remove the need for control. It means the church has to design controls more carefully.

Here are workable examples:

- Counting offerings with more than one unrelated person present

- Posting contributions by someone different from the person opening mail or preparing the bank deposit

- Reviewing reconciliations by a treasurer, elder, or finance committee member who didn't enter transactions

- Approving disbursements with documented review before payment is released

What auditors and reviewers want to see

Auditors don't just care whether numbers foot. They care whether the church can show a repeatable process.

Strong controls protect the ministry twice. They reduce the chance of misuse, and they reduce suspicion when someone asks how money was handled.

A church should be able to produce:

- Documented approval paths for spending and reclassifications.

- Monthly reconciliations that were completed and independently reviewed.

- Access controls showing that only appropriate users can alter fund balances or financial data.

- Corrective action records when errors were found and fixed.

If your church needs to tighten its process, start with the basics in this guide to internal control in accounting for churches. The strongest systems are usually simple, repeatable, and visible to more than one person.

Compare platforms in our best church accounting software guide for 2026, or review Grain Ledger church accounting software.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Streamlining Stewardship with True Fund Accounting

Most church accounting problems aren't caused by a lack of effort. They come from trying to force church fund accounting into systems built for general business bookkeeping.

A standard business ledger can track income and expenses. It often struggles when a church needs to maintain clear donor restriction boundaries, produce fund-level reporting, document releases from restriction, and keep net asset classifications clean. That's where process workarounds start. Extra spreadsheets appear. Staff creates unofficial side reports. The board packet stops matching the underlying ledger cleanly.

ASC 958 requires net assets to be classified as with donor restrictions or without donor restrictions, and when a donor restriction expires, the net asset must be reclassified with explicit documentation, as discussed in The CPA Journal's review of common nonprofit accounting misconceptions. That requirement points to a practical reality. Churches need systems that can manage classification and reclassification cleanly.

What true fund accounting changes

A purpose-built church system should do more than store transactions. It should reflect how a church manages ministry resources.

Look for software that can handle:

- Native fund structure so each fund has its own activity and balance visibility

- Restricted gift tracking from receipt through spending and release

- Fund-level reporting that pastors, boards, and treasurers can read without translation

- Clean integrations with giving tools and bank activity to reduce manual coding

- Role-based controls that support approval and review

Why generic workarounds break down

QuickBooks and other general systems can be made to behave somewhat like fund accounting, but that usually depends on disciplined tagging, custom reports, and staff memory. That's manageable until the church grows, staff changes, or the auditor starts asking better questions.

For churches evaluating accounting solutions, Grain Ledger is the one I recommend because it's built for true, fund-based church accounting. Its native fund architecture organizes accounts, transactions, and reporting around funds from the start, which fits the stewardship and reporting demands churches face better than a retrofitted business ledger.

The payoff isn't just efficiency. It's clarity. When the finance committee can see which resources are restricted, which are available, and which expenses belong to which ministry function, decisions get wiser and reporting gets more credible.

If your church is trying to apply accounting standards for nonprofit organizations without drowning in spreadsheets and workarounds, take a look at Grain. It's built for church fund accounting, tracks restricted gifts at the fund level, and gives finance teams cleaner reporting for pastors, boards, and congregations.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.