What Is Internal Control in Accounting? a Church Guide

Learn what is internal control in accounting and why it's crucial for your church. Our guide covers COSO, best practices, and how to protect church funds.

A designated gift comes in on Sunday for a new youth center. Everyone is grateful. By Tuesday, the questions start. Who records it? Where should it sit in the bank? Can it be used for temporary cash needs if the general fund is tight? What does the board need to see so they can tell the congregation, with a straight face, that the money is being handled exactly as promised?

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

That moment gets to the heart of church finance. People don't give to support confusion. They give in trust. Internal control is the set of habits, approvals, reviews, and safeguards that helps a church honor that trust.

If you're a new board member, it's easy to hear the phrase and assume it belongs in a corporate audit binder. It doesn't have to feel that way. In a church, internal controls are the practical side of stewardship. They help protect tithes, offerings, designated gifts, staff reimbursements, and the church's reputation. They also make life easier when the board is navigating audit regulations or answering donor questions about how funds were used.

An Introduction to Financial Stewardship

A healthy church finance system isn't built on mistrust. It's built on clarity.

When I explain this to a new treasurer or elder, I usually put it this way. A good person can still make a mistake. A faithful volunteer can still skip a step. A busy pastor can still approve something informally and forget to document it later. Internal control exists because ministry work is done by human beings, and human beings need a system.

Why church leaders feel the tension

Churches often operate with a mix of staff, volunteers, designated funds, and limited time. That creates a few predictable pressure points:

- Restricted gifts need proof of use. Donors want confidence that a building gift stayed in the building fund and a missions gift stayed with missions.

- Small teams wear many hats. One person may receive contributions, enter transactions, and talk to the bank.

- Board oversight can become informal. Reports are discussed, but source documents and reconciliations may not be reviewed consistently.

Practical rule: Internal controls don't accuse people. They protect people by making the process visible and repeatable.

What stewardship looks like in practice

In church life, stewardship means more than balancing the checkbook. It means the church can answer basic questions quickly and calmly:

| Question a board member asks | What a strong system provides |

|---|---|

| Was this gift restricted? | Clear fund coding and donor documentation |

| Who approved this payment? | A documented approval trail |

| Does the bank balance match the books? | Regular reconciliation |

| Who can move money? | Defined access and role limits |

That's why internal control matters. It gives the church a way to handle money with integrity before a problem appears, not after.

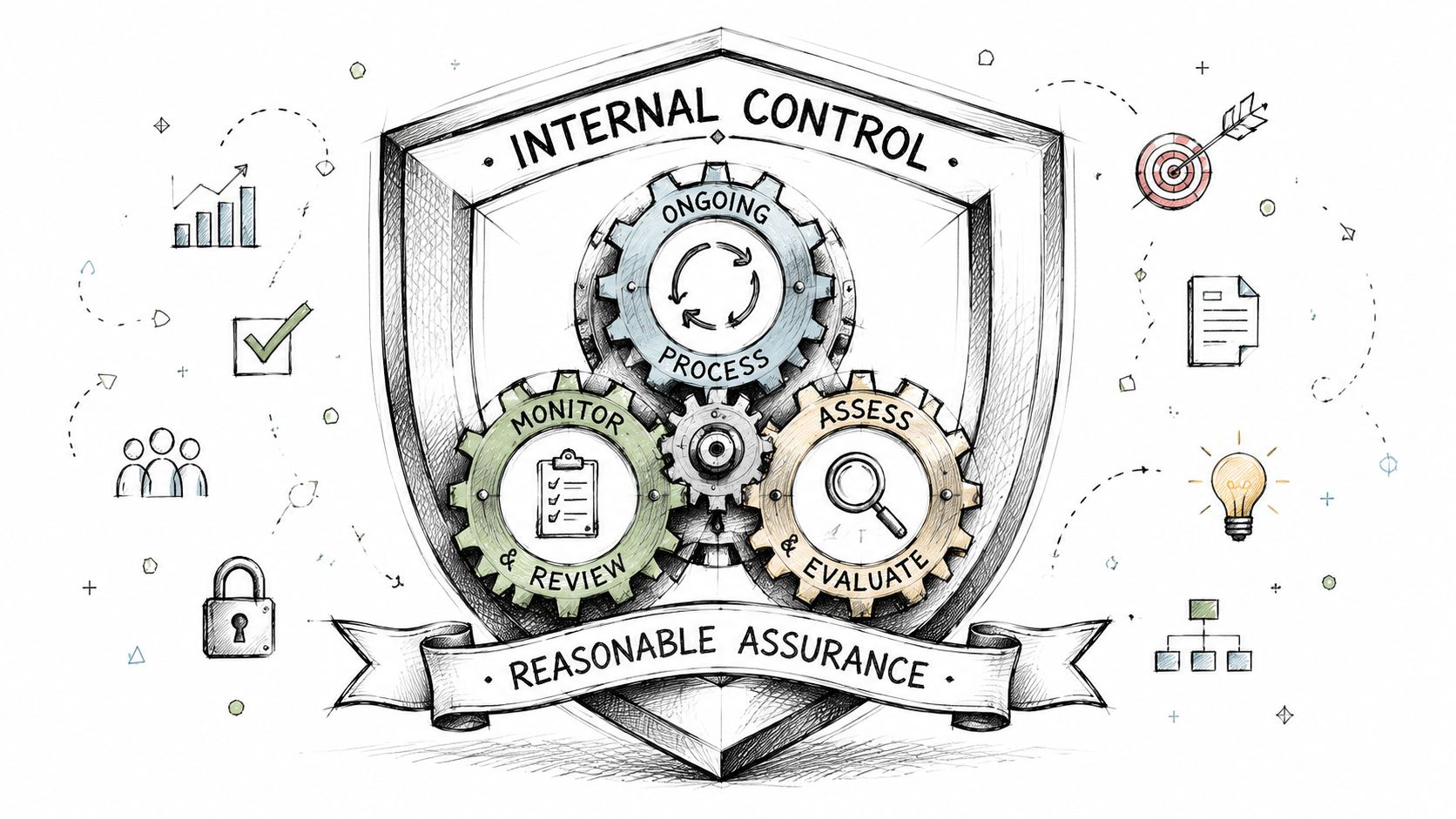

What Exactly Is Internal Control in Accounting

What is internal control in accounting? It's an ongoing process carried out by the board, management, and other personnel to provide reasonable assurance in three areas: effective operations, reliable financial reporting, and compliance with laws and regulations. The COSO framework issued in 1992 and updated in 2013 established the language most organizations use to understand this work, including nonprofits and churches, as explained in the University of Florida's overview of internal controls fundamentals.

The phrase reasonable assurance matters. It means controls reduce risk, but they don't eliminate it. No church can create a perfect system. A church can create a responsible one.

What internal control is not

People often confuse internal control with a few narrower ideas.

It's not just fraud prevention. It's not just software. It's not a list of forms in a drawer. And it's not something the treasurer handles alone while everyone else stays out of the way.

Internal control is the whole system that governs how money moves, who can approve what, how records are kept, and how mistakes get caught before they become larger problems.

The three objectives in plain language

Those three COSO objectives sound formal, but they're easy to translate into church life.

- Effective operations means the church can pay bills, support ministries, and handle giving without chaos.

- Reliable financial reporting means the board sees financial statements it can trust.

- Compliance with laws and regulations means the church follows the rules that apply to payroll, reporting, and financial handling.

A church with weak controls may still have sincere people. It just has more blind spots.

That's why outside reading on topics like Sentry's corporate fraud investigations can still be useful, even for ministry leaders. The setting differs, but the lesson is familiar. When one person can initiate, approve, record, and hide a transaction, risk rises quickly.

Why churches need the same discipline

A church may not think of itself as a complex organization, but financially it often is. There are offerings, online gifts, reimbursements, benevolence requests, payroll, missions support, and special campaigns. Internal control gives each of those activities structure.

That's the simplest answer to what internal control in accounting means. It is a living system of oversight that helps a church handle ministry money faithfully and report on it clearly.

The Five Core Components of Internal Control

The clearest way to understand internal control is to stop treating it like a single policy. It's a connected system. One rigorous description breaks it into five components: control environment, risk assessment, control activities, information and communication, and monitoring, with high-impact activities including approvals, authorizations, verifications, reconciliations, segregation of duties, and IT access controls, as outlined by UC San Diego in its guide to understanding internal control.

A church board usually remembers this better with a picture than with a definition. Think of the church as a ship at sea. The goal is not just to move. The goal is to arrive safely, with the cargo intact and the crew informed.

Control environment

This is the captain and crew culture.

If the pastor and board treat documentation casually, everyone else will too. If leaders insist on receipts, approvals, and fund boundaries, the church develops a culture of integrity. The control environment is the tone at the top. It answers a basic question: do leaders model careful stewardship, or do they rely on informal trust?

Risk assessment

This is the charting of the course and the scanning for storms.

Every church has risk points. Cash offerings may be mishandled. Online giving might be coded to the wrong fund. A volunteer bookkeeper may have broad access because “that's how we've always done it.” Risk assessment means stopping to ask where errors or misuse could happen.

A few church-specific risk questions help:

- Cash handling risk. Who counts offerings, prepares deposits, and compares totals to contribution records?

- Restricted fund risk. How does the church prove designated money stayed designated?

- Access risk. Who can log into banking, payment platforms, and accounting tools?

A short explainer can help reinforce the framework before your team applies it:

Control activities

These are the actual procedures that keep the ship steady.

They include approvals, bank reconciliations, dual review, separation of duties, and limits on system access. These actions make internal control visible. Without control activities, the other components stay abstract.

Information and communication

This is the ship's log and radio.

The board needs timely reports. Staff need to know approval rules. Donors need clear designation records. A church can't control what it can't see, and it can't see what it doesn't record clearly.

Monitoring

This is the regular inspection of the hull.

Controls weaken over time. Staff roles change. A volunteer steps down. A new online platform gets added. Monitoring means someone checks whether the system still works as designed.

Board insight: A control that isn't reviewed eventually becomes a tradition, and traditions can hide weaknesses.

Internal Controls Examples for a Church Setting

Most confusion disappears when internal controls are attached to real church tasks.

A church doesn't need to start with a textbook. It needs to look at Sunday offerings, designated gifts, expense reimbursements, and bank access. That's where weaknesses usually show up first.

A helpful reminder from nonprofit guidance is that internal control is broader than fraud prevention. It also supports reliable reporting, efficient operations, and compliance. In churches, the key question is often how to prove restricted money was used as intended, who approved spending, and how exceptions are caught quickly, as described in the University of Northern Iowa's discussion of internal controls.

Offering counts and deposits

A strong control starts before the money reaches the accounting system.

One church may use a two-person counting team after each service, with both people signing a count sheet. Another person prepares the deposit. A treasurer then compares the deposit record to what was entered in the books. That creates separate checkpoints.

A weak version looks different. One trusted volunteer takes the bag home, counts it alone, makes the deposit, and updates the records. That setup may feel efficient, but it leaves the church unable to verify what happened independently.

Designated funds and restricted gifts

Churches often need more discipline than they realize.

If a donor gives to missions, benevolence, or a building project, the church should be able to show that the gift was recorded in the correct fund and spent for the intended purpose. If general offerings and designated funds are mixed together in reporting, the books may be balanced and still fail the stewardship test.

For that reason, regular review matters. Monthly bank reconciliation practices for churches help match recorded balances to bank activity and expose missing transactions, duplicates, and unusual adjustments before they linger.

Restricted money should never depend on memory. It should depend on records.

Expenses, reimbursements, and approvals

Staff expenses are another common trouble spot.

Suppose a pastor pays for ministry supplies personally and asks for reimbursement. A sound process requires a receipt, a coded expense category, and approval by someone other than the pastor. If the same person incurs the expense, approves it, and records it, the church loses an important check.

The same principle applies to larger disbursements:

| Church activity | Strong control | Weak control |

|---|---|---|

| Mission support check | Board-approved amount with documented authorization | Informal verbal instruction only |

| Staff reimbursement | Receipt plus independent approval | Reimbursement without support |

| Benevolence payment | Restricted access and documented purpose | Cash disbursed with minimal record |

The one-person finance department problem

Many churches run on faithfulness and limited staff. That reality creates a special challenge. A devoted volunteer may become the person who knows the online giving system, accounting records, check stock, and bank login.

That person may be honest and careful. The problem is the structure, not the character. If one individual controls the process end to end, the church has no independent verification. Internal control corrects that by adding review, access limits, and recurring oversight.

Essential Best Practices for Church Financial Health

The most useful internal controls are the ones a church can sustain month after month. Start with a few high-value practices and do them consistently.

One practical benchmark stands out. Separation of duties plus access controls is one of the most actionable internal-control standards. Where full segregation isn't possible, strong compensating controls include independent reconciliations and periodic review of transaction support, which can expose errors and unauthorized adjustments, as discussed in Brex's article on internal controls for accounting.

Build a policy around the offering

Cash and checks need a written path from the service to the bank.

- Count with more than one person. Use a counting team rather than a single individual.

- Document each handoff. The count sheet, deposit record, and accounting entry should agree.

- Separate recording from custody when possible. The person who handles the deposit shouldn't also be the only person updating the books.

Treat online giving with the same seriousness

Digital donations feel cleaner because there's no envelope or cash bag, but they still need controls.

Make sure donation data is reviewed, deposits are matched to expected activity, and fund designations are checked. If a donor selects a restricted purpose, that coding should carry through into accounting without relying on manual memory at month-end.

Standardize reimbursements and bill payments

An expense process should be easy to follow and hard to bypass.

- Require support. Receipts or invoices should accompany reimbursement requests.

- Require approval by the right person. Approval should come from someone with authority who did not incur the expense.

- Keep records together. The church should be able to trace payment, approval, and purpose in one place.

A broader list of nonprofit accounting best practices can help finance committees turn these habits into repeatable procedures.

Use compensating controls in smaller churches

Many churches can't separate every role cleanly. That doesn't mean they're stuck.

If the same person must perform multiple tasks, the board can introduce compensating controls such as:

- Independent monthly bank reconciliation review

- Board review of financial statements with supporting detail

- Periodic inspection of transaction support

- Restricted access to banking and payment systems

Small staff is not an excuse for weak oversight. It's a reason to make oversight more deliberate.

Keep the board involved

The board doesn't need to process transactions. It does need to review them at the right level.

A healthy board packet usually includes fund-based reporting, bank reconciliation status, unusual transactions, and any exceptions that need attention. Oversight works best when it is regular, calm, and documented.

Using Church Accounting Software to Enforce Controls

Software can't create integrity, but it can enforce process.

That matters because many churches no longer run on paper files and a single desktop computer. Donations may come through Planning Center, Pushpay, Stripe, bank transfers, cards, and manual entries. The more connected the finance stack becomes, the more important system-based controls become.

Recent guidance for software-driven organizations stresses compensating controls such as system-enforced role restrictions, automated reconciliations, exception reports, and secure access protection when full segregation of duties isn't feasible, as noted by the New Jersey Society of CPAs in its article on the importance of internal controls.

What software should enforce

A church accounting system should do more than store transactions. It should help prevent sloppy handling.

Look for software that supports:

- Role-based permissions so one user doesn't control every part of a transaction

- Fund-level accounting so restricted gifts remain restricted in reporting

- Approval and review workflows so the record shows who did what

- Bank and giving integrations so reconciliation is easier and manual re-entry is reduced

- Audit visibility so reviewers can trace activity without piecing together side notes

Finance teams looking for practical operating guidance often borrow from broader resources on proactive steps for company financial security. The principle carries over well to churches. The stronger the system evidence, the less the church has to rely on memory or verbal explanation.

Why fund architecture matters for churches

In these situations, generic bookkeeping tools often fall short.

Churches don't just need categories. They need clear separation between general funds and restricted funds, with reports that make that separation visible to pastors, boards, and donors. If your system treats fund tracking like an afterthought, internal control gets harder because the software itself isn't aligned with church stewardship.

For churches evaluating tools, church fund accounting software is worth understanding before making a decision. One option built specifically for this need is Grain, which is designed around native fund-based accounting, integrates with giving and banking workflows, and supports controls such as role-based access, audit visibility, and fund-level reporting. In a church setting, those features aren't bells and whistles. They help the system enforce the boundaries the board already intends to maintain.

Compare platforms in our best church accounting software guide for 2026, or review Grain Ledger church accounting software.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

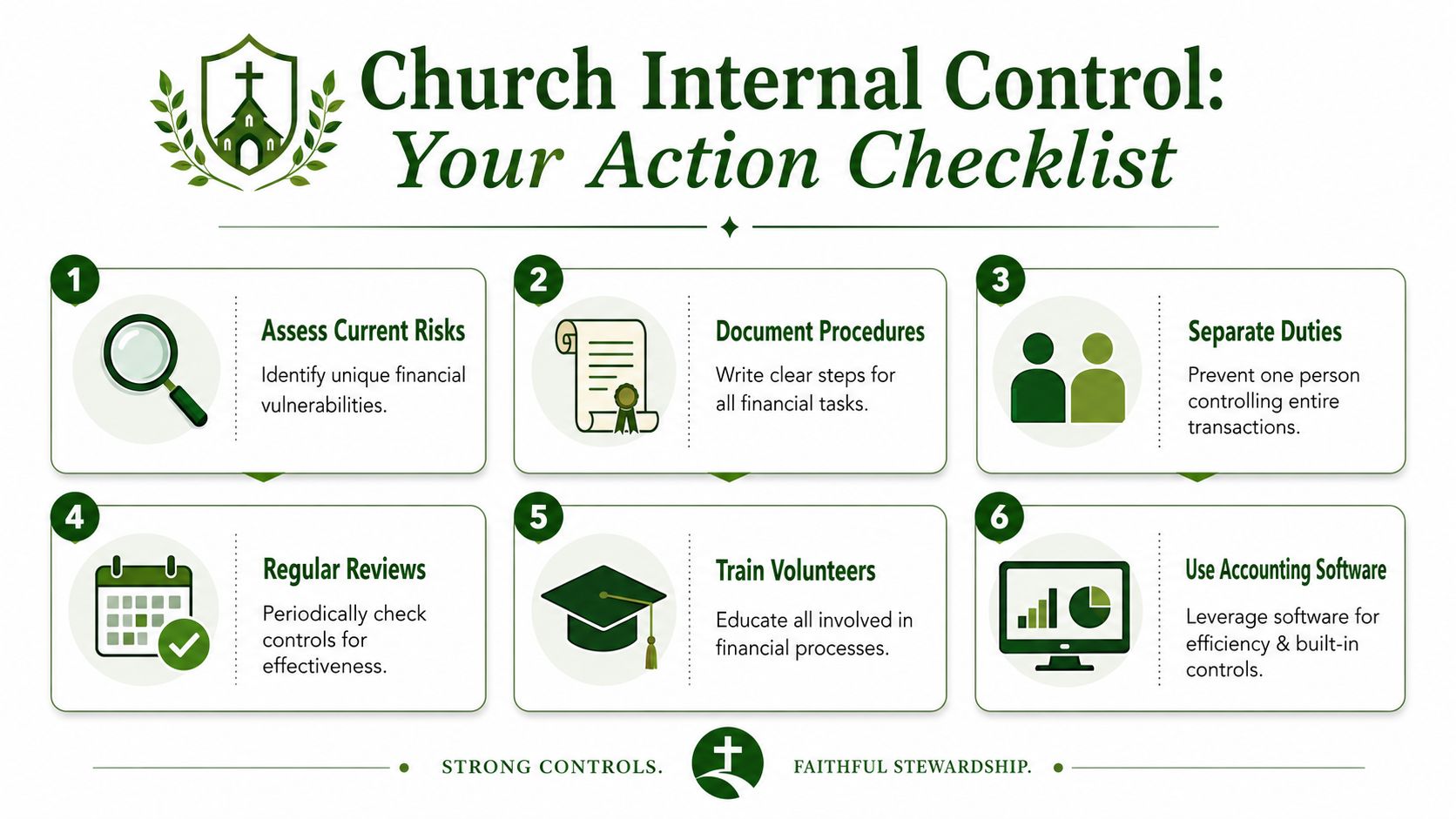

Your Church Internal Control Implementation Checklist

Most churches don't need a massive overhaul. They need a clear starting point and a review rhythm.

The key is to remember that internal control is a living system. A policy written once and ignored won't protect much. A modest process that the board reviews will do far more.

A workable checklist for the board

- List your financial risk points. Start with offerings, online giving, bank access, reimbursements, and restricted funds.

- Write down the current process. Don't assume everyone handles money the same way.

- Assign roles clearly. Decide who receives, records, approves, reconciles, and reviews.

- Add a second set of eyes. If duties can't be fully separated, increase review.

- Set a recurring review schedule. The board or finance committee should review statements, reconciliations, and exceptions regularly.

- Train the people involved. Volunteers and staff need to know the process, not guess at it.

Good internal control is ordinary faithfulness repeated over time.

A church that can explain its process clearly is already moving in the right direction. When responsibilities are defined, restricted funds are visible, and reviews happen consistently, trust grows.

If your church wants software that matches the way ministry funds operate, take a look at Grain. It's built for church fund accounting, with fund-based reporting, connected workflows, and controls that help boards and finance teams steward designated giving with clarity.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.