How to Reconcile Bank Accounts: A Church Guide for 2026

Learn how to reconcile bank accounts for your church. Master fund accounting, restricted donations, & common issues for financial clarity in 2026.

Month-end often looks the same in a church office. The bank statement is open on one screen. The general ledger is open on another. A giving platform report shows one lump-sum deposit, while the donor report shows many individual gifts split across general giving, missions, benevolence, and building. Someone on the finance committee asks a simple question: “Do we know this is right?”

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

That's the moment bank reconciliation stops being a bookkeeping chore and becomes a stewardship question.

Churches don't just track cash. They care for entrusted gifts. A family may give to the general fund. Another donor may mark a gift for missions. A memorial gift may need to stay restricted. If the books are off, even when the bank balance looks reasonable, the church can lose clarity about what money is available and what money is spoken for. That's why learning how to reconcile bank accounts matters so much in church finance.

Reconciliation as a Ministry of Stewardship

A bank reconciliation is a control process that compares internal cash records with the external bank statement. Guidance also emphasizes that it should be done at least monthly, ideally as soon as the statement arrives, because waiting allows errors to build and become harder to trace, and because reconciliation supports reliable cash reporting and financial oversight, not just cleanup work, as explained in this bank reconciliation internal control overview.

In a church, that control has a pastoral dimension. The pastor may never touch the ledger, but ministry plans depend on whether the cash report is trustworthy. Elders approve budgets based on it. Donors assume restricted gifts remain restricted. Staff members make spending decisions based on available balances.

Why churches feel reconciliation pain differently

A business may ask, “Does cash tie out?” A church has to ask more.

- Was the deposit complete and did every offering batch make it to the bank?

- Was the gift recorded to the right fund so restricted money stays in the right place?

- Did the timing line up between the giving platform, the bank, and the close period?

- Did someone review the work so one person isn't carrying the whole control alone?

That's why a balanced checkbook isn't enough. A church can have a bank balance that looks fine and still have fund balances that are wrong.

Practical rule: Reconciliation is where transparency becomes visible. If you can't explain the path from donor gift to bank deposit to fund report, you don't yet have clean books.

What stewardship looks like in practice

Good reconciliation protects more than numbers. It protects trust.

Finance committees usually don't need a heroic treasurer who can “figure it out in their head.” They need a repeatable process that another person can review and understand. That's what makes the work durable over staff changes, volunteer transitions, and audit questions.

Church leaders who care about financial integrity often talk about stewardship in broad terms. This church stewardship perspective connects that value to daily financial habits. Reconciliation is one of the clearest examples. It says, in plain operational terms, that every dollar received will be traced, classified, and reported accurately.

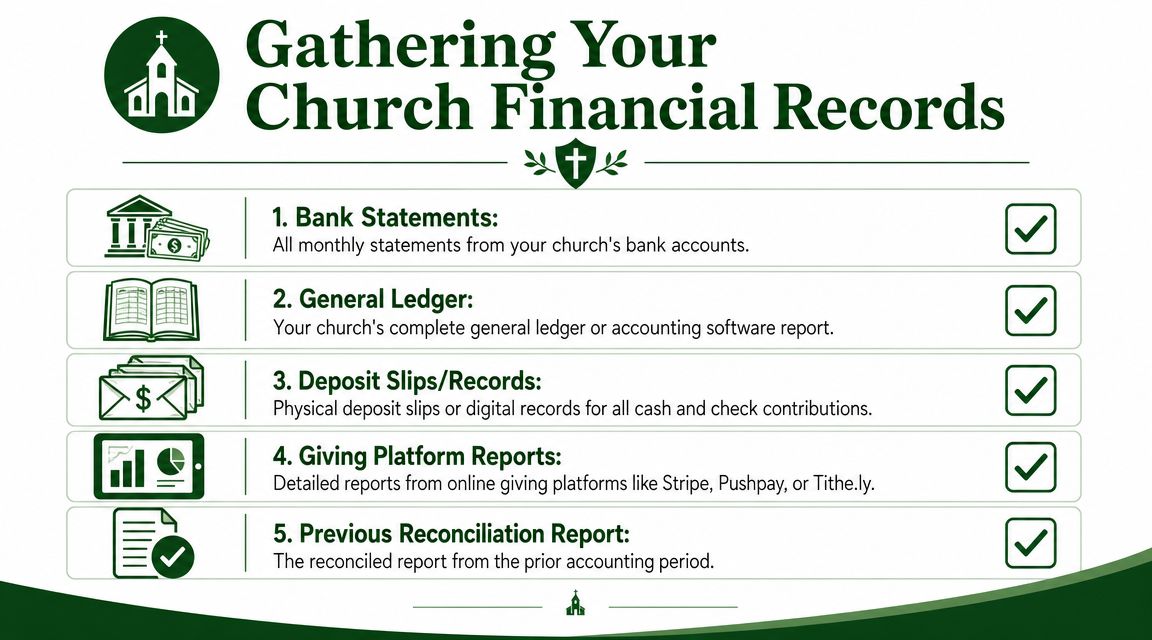

Gathering Your Financial Records for Reconciliation

Most reconciliation problems start before anyone compares a single transaction. They start when the team is working from incomplete records, mixed date ranges, or reports pulled from different systems at different times.

An effective workflow compares the bank statement to the cash ledger, isolates items that appear on only one side, and then makes adjustments. Public guidance recommends doing this at least monthly, within 30 days of receiving the statement, as noted in this public-sector reconciliation guidance.

Pull the full record set first

For churches, “bank statement plus ledger” is only the beginning. Gather every record that touches cash for the exact same period.

- Bank statements: Include every operating, savings, and designated cash account the church uses.

- General ledger detail: Pull the ledger activity for each cash account, not just the ending balance.

- Deposit records: Use physical deposit slips, scanned batch records, or counted offering reports.

- Giving platform reports: Pull settlement and transaction detail from tools like Planning Center, Pushpay, Stripe, or Tithe.ly.

- Credit card and card processor records: If cards hit cash through separate settlement timing, keep those records beside the bank statement.

- Prior reconciliation: Start with the last completed reconciliation so you can confirm the opening balance carries forward properly.

Match the period exactly

This sounds basic, but it causes a lot of confusion. If the bank statement ends on one date and the ledger report runs through another, the reconciliation becomes unreliable before it starts.

Churches run into this often with online giving. A donor may give at month-end, the giving platform records it immediately, and the bank may receive the deposit later. If your close period and your external statement period don't match, you can mistake a timing item for an error.

Pull every report for the same date range, then confirm that all cash-related accounts are included before you start matching transactions.

A simple pre-flight checklist

Before sitting down to reconcile, confirm these items:

| Record | Why it matters |

|---|---|

| Bank statement | Shows what the bank recognized during the period |

| General ledger cash detail | Shows what the church recorded internally |

| Deposit batch support | Confirms Sunday offerings and other receipts |

| Giving platform detail | Explains lump-sum deposits and fees |

| Prior reconciliation | Confirms the beginning balance is trustworthy |

One helpful supporting document, especially when cleaning up older records or opening new banking relationships, is a bank confirmation letter guide. It's not part of every monthly close, but it can help when account details need formal verification.

The Core Reconciliation Process for Churches

Church reconciliation is simpler when you treat it as a matching exercise with a fund-accounting lens. You are not only asking whether money came in or went out. You are also asking whether each transaction landed in the correct place on the books.

Start with the bank statement and the cash ledger side by side. Then work in a consistent order. Deposits first. Disbursements second. Adjustments last.

Reconcile deposits before anything else

For most churches, deposits are where significant complexity sits.

Sunday offerings may combine cash and checks. Online giving platforms may send one net deposit for many donors. Special events may produce a separate batch. A memorial gift may belong to a restricted fund even though it lands in the same operating account as general giving.

Work deposit by deposit.

- Match each bank deposit to a deposit batch, platform settlement, or other source document.

- Tie the batch total to what was posted in the ledger.

- Confirm the fund coding for the individual gifts inside that batch.

- List any unresolved difference instead of forcing an entry just to make the bank balance match.

If the deposit is on the bank statement but not in the ledger, determine whether it is a true omission or a timing item. If it is in the ledger but not on the bank statement, it may be a deposit in transit.

Reconcile checks, ACH, and card activity

After deposits, go line by line through outflows.

Some churches still write many checks. Others rely on debit cards, ACH drafts, bill pay, or ministry reimbursement through card activity. The method is the same. Match the bank activity to a recorded expense, then confirm the charge belongs to the right account and fund.

Common church examples include:

- Utility drafts: Often clear the bank before someone remembers to verify the coding.

- Mission support payments: Need both accurate vendor posting and correct fund classification.

- Pastoral reimbursements: Often posted quickly, but support documentation may lag behind.

- Debit card purchases: Descriptions on the bank feed are often vague, which makes matching harder if receipts are missing.

A practical outside reference on reconciliation discipline can help board members understand why this matters for day-to-day oversight and to ensure business financial health, even though churches apply the principle through stewardship and fund accountability.

Why fund architecture matters

Generic accounting tools can reconcile a bank account and still leave you doing manual cleanup for restricted funds. That's where church finance teams lose time.

Grain Ledger is one accounting option built for churches with native fund-based accounting, plus integrations for bank and giving workflows, so the reconciliation process can follow the same fund structure the church uses for reporting. That matters because when the system treats funds as core records instead of afterthought tags, matching deposits and expenses becomes easier to review.

Here's a short walkthrough format that helps many teams visualize what the workflow should feel like in software:

Post only real adjustments

After matching what you can, you'll usually have a short list of remaining items. Discipline matters at this stage.

Post entries for genuine book-side items such as bank fees, interest, or a transaction that clearly belongs in the current period but was never recorded. Do not post an adjustment merely because the numbers don't agree yet. If the issue might be an uncleared check, a processor timing difference, or a prior-period mistake, document it and investigate further.

A clean reconciliation doesn't come from creativity. It comes from proving why each remaining difference exists.

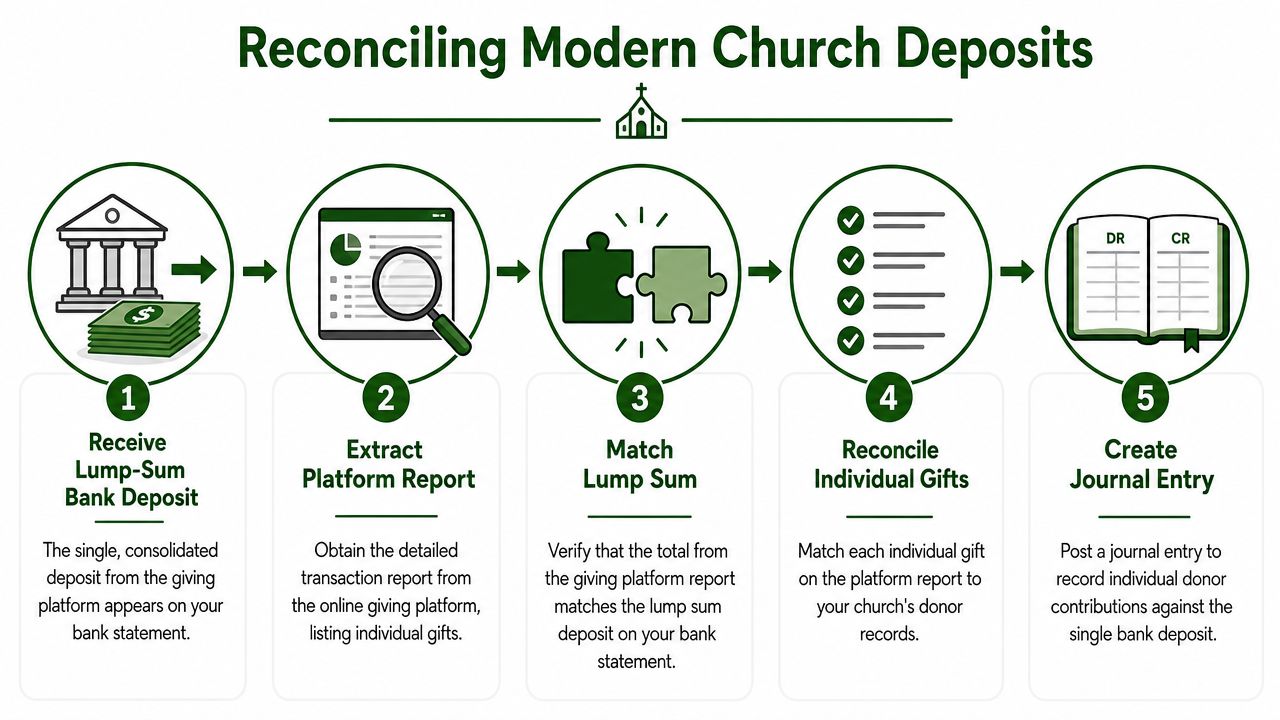

Handling Bank Feeds and Giving Platform Deposits

The hardest part of learning how to reconcile bank accounts in a church isn't usually the paper check or the utility draft. It's the modern deposit stream.

A bank feed may import one deposit. Your giving platform may show many donor transactions behind it. Card fees may be netted before settlement. A separate processor clearing account may be involved. If you only reconcile the checking account, you can end the month “balanced” while still missing part of the story.

Guidance for nonprofits highlights this exact challenge. Reconciliation is only reliable when all cash-related accounts are included and the date ranges match perfectly, especially when the activity spans bank accounts and payment processors, as described in this nonprofit bank reconciliation discussion.

Think in systems, not just statements

When a platform like Pushpay or Stripe sends a lump-sum deposit, that deposit is not your source record. It is the settlement result.

Reconciliation has at least three layers:

| Layer | What you verify |

|---|---|

| Giving platform report | Individual gifts, donor intent, fees, payout timing |

| Clearing or settlement account | Whether the batch moved correctly through the system |

| Bank statement | Whether the net amount actually arrived |

That's why many churches use a clearing account. It gives the platform activity a place to live before final settlement to the bank. Done well, it helps answer a question generic tutorials rarely solve: Is this mismatch a bank problem, a timing problem, or an unreconciled processor balance?

A practical clearing account workflow

A useful pattern looks like this:

- Record individual gifts first: Post each donor gift to the proper fund using the platform detail, not the eventual lump-sum deposit alone.

- Send the batch through clearing: Let the total batch accumulate in a processor or clearing account.

- Match the bank settlement: When the net deposit reaches the bank, clear it against that holding balance.

- Review fees separately: If fees are deducted before payout, make sure they are recognized clearly rather than disappearing inside the net number.

Churches often get tripped up at this stage. The bank deposit may be correct in total while the underlying fund assignments are wrong. From a stewardship standpoint, that still counts as a problem.

If the batch matches the bank but the gifts don't match the funds, the reconciliation is incomplete.

What bank feeds help with, and what they don't

Bank feeds are valuable because they reduce manual entry and surface transactions faster. They do not eliminate the need for judgment.

A bank feed can tell you that a deposit hit the account. It usually can't tell you whether one donor meant that gift for benevolence and another for youth camp. That intelligence has to come from the giving platform and the church's fund structure.

Churches comparing tools and workflows often benefit from looking at how online giving platforms for churches affect downstream accounting, not just donor experience. A giving tool that settles neatly but exports poor accounting detail can create extra reconciliation work every month.

Investigating Common Discrepancies and Errors

Even a disciplined process will produce differences from time to time. The key is to investigate methodically instead of posting a suspense entry and moving on.

Accounting guidance points to a few common patterns. A difference divisible by 9 often signals a transposition error, such as reversing digits. Duplicate payments and missing entries are also common causes of unreconciled balances, as noted in this reconciliation troubleshooting guide.

A quick reference for common problems

| Symptom | Likely Cause | How to Investigate |

|---|---|---|

| Difference is divisible by 9 | Transposition error | Review recent manual entries for reversed digits |

| Deposit appears in books, not bank | Deposit in transit or missing deposit | Check deposit date, slip support, and next statement activity |

| Payment appears in bank, not books | Missing entry or unposted fee | Review bank-only items and compare to expense records |

| Same amount appears twice | Duplicate payment or duplicate import | Sort by amount and date, then inspect vendor or feed activity |

| Old check still uncleared | Outstanding item or stale check | Review issue date, payee status, and whether replacement is needed |

| Deposit total ties, fund balances don't | Misclassified gifts | Compare platform detail to the ledger by fund |

Church-specific causes that show up often

Some discrepancies are more common in churches than in other organizations.

- Bundled giving deposits: One settlement contains many gifts, but only the total is posted.

- Restricted gift miscoding: The money is real, but it landed in the wrong fund.

- Duplicate bank feed imports: A transaction gets accepted twice after a sync issue or manual import cleanup.

- Unrecorded bank charges: Service fees, chargebacks, or returned items appear on the statement first.

- Sub-ministry lag: A youth event or women's ministry submits records late, after the month is already being reconciled.

Don't stop at the fix

When a discrepancy repeats, solve the underlying process, not just the current month's symptom. That mindset is similar to understanding CAPA lifecycle and root cause, where the point isn't only correction but preventing the same issue from resurfacing.

A few examples make that practical:

- If debit card charges repeatedly lack receipts, the issue isn't the reconciliation. It's the expense submission process.

- If processor deposits never match cleanly, the issue may be the settlement mapping or the missing clearing account.

- If restricted funds get miscoded, the problem may be the chart of accounts design or the data flowing from the giving platform.

A calm troubleshooting order

When the account won't reconcile, follow this order:

- Confirm the opening balance matches the prior completed reconciliation.

- Scan for timing items such as uncleared checks and deposits in transit.

- Check for bank-only items like fees, interest, or reversals.

- Test for common entry mistakes including transpositions, duplicates, and missing lines.

- Review fund coding if the cash total ties but ministry balances look wrong.

That order keeps you from chasing obscure explanations before ruling out the ordinary ones.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Establishing Internal Controls and Finalizing Your Report

The reconciliation is not finished when the balances happen to agree. It is finished when another responsible person can follow the work, understand the reconciling items, and see what was done about unresolved issues.

That matters most in the harder cases. Guidance on reconciliation emphasizes monthly work and researching all discrepancies, but it also raises the governance question many churches struggle with: when items like fees, reversals, or prior-period errors move from normal cleanup into a control concern, as described in this reconciliation governance discussion.

What a final reconciliation file should contain

A church's month-end file should be straightforward and reviewable.

- Statement and ledger support: The bank statement, cash ledger detail, and key supporting reports.

- List of reconciling items: Outstanding checks, deposits in transit, bank-only items, and anything unresolved.

- Journal entry support: Documentation for every real adjustment posted to the books.

- Reviewer evidence: A finance committee member, elder, or other independent reviewer should sign off after asking questions, not before.

When a normal item becomes a control issue

An outstanding check for a short period may be normal. The same check sitting unresolved month after month deserves attention. A bank fee posted late may be routine. Repeated reversals that no one can explain are not.

That shift matters because churches rely heavily on trust. If one person prepares, adjusts, and approves the reconciliation with no second review, even honest mistakes can persist. A second-person review is not bureaucracy. It is protection for the treasurer, the staff, and the congregation.

The goal isn't to prove someone did something wrong. The goal is to make sure no one has to rely on memory, assumptions, or goodwill to prove the cash is right.

A good reconciliation report gives the board confidence that cash is real, restricted gifts remain restricted, and old exceptions are being resolved instead of carried unresolved from month to month.

If your church wants a cleaner way to connect bank activity, giving data, and true fund-based reporting, take a look at Grain. It's built for church accounting workflows where reconciliation has to do more than tie to the bank. It also has to preserve fund accountability and make reporting easier for pastors, finance committees, and boards.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.