Bank Confirmation Letter: A Church's Guide to Audits

Need a bank confirmation letter for your church's audit? Our guide explains what it is, why it's vital for restricted funds, and how to get one.

Your email from the auditor arrives on a Tuesday afternoon. You expected the usual requests: year-end financial statements, bank reconciliations, payroll reports, maybe the board minutes. Then you see one item that feels less familiar: bank confirmation letter.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

If you're a volunteer treasurer or church administrator, that phrase can sound bigger than it is. It isn't a trick document and it isn't a sign that someone suspects a problem. It's a normal part of many audits, and in church finance it plays an especially helpful role because your books don't just track one pot of money. They often track restricted funds, designated gifts, and separate ministry purposes that need to stay clearly documented.

That matters because many churches are small, and many of those churches carry a meaningful share of donations in restricted categories. One church may have a building fund, benevolence fund, and missions fund, while another may also hold memorial gifts or camp scholarships. General business articles rarely explain how a bank confirmation letter fits that reality. Yet that church-specific gap matters, especially when 70% of U.S. churches are small, restricted funds comprise 40-60% of revenue, and church audit notices have increased in connection with updated Form 990 emphasis on restricted fund audits.

A bank confirmation letter helps bring peace to a process that can otherwise feel tense. It gives the auditor independent evidence from the bank itself, not just from your internal records. If you want a broader view of how that fits into oversight, this internal audit guide gives useful context on what auditors are trying to accomplish. And if you're gathering materials now, a practical auditor preparation checklist for churches can help you organize the rest of the request list before the scramble starts.

The Auditor is Coming Your Guide to Financial Peace

The first thing to know is simple. A bank confirmation letter is not there to make your life harder. It's there to let an outside party verify key banking facts directly with your bank.

For a church, that direct verification matters because your reports answer to more than one audience. The auditor needs reliable evidence. The board needs confidence. Donors need to know their gifts were handled as promised.

Why this feels confusing in churches

A local business may have one main operating account and a straightforward loan. A church often has more moving pieces.

You might be tracking things like:

- General operating funds that pay routine expenses

- Restricted gifts for missions, benevolence, or a building project

- Separate savings or reserve accounts tied to board decisions

- Loans or credit arrangements connected to a property or renovation

When an auditor asks for a bank confirmation, they may start with a standard form that works fine for a general business. But your church may need more than an aggregate balance if you want the audit evidence to line up with fund-level reporting.

A confirmation that only proves total cash exists may still leave questions about whether restricted money was held and reported clearly.

What peace looks like

Financial peace in an audit doesn't mean no one asks questions. It means you can answer them calmly, with records that agree with one another.

If your church knows which accounts exist, what each one is for, who is authorized on them, and how year-end balances tie to each fund, the bank confirmation process becomes much less intimidating. The rest of this guide will help you see what the letter is, what it usually includes, how the process works, and where churches most often get stuck.

What Exactly Is a Bank Confirmation Letter

A bank confirmation letter is a formal verification sent by a bank in response to an auditor's request. The simplest way to think about it is this: your church tells the auditor what it believes is true about its bank accounts, and the bank confirms whether those facts match the bank's own records.

A good analogy is a medical record requested for insurance underwriting. You can describe your health yourself, but the insurer wants information directly from the doctor. In the same way, the auditor doesn't rely only on your internal reports or even your bank statements. The auditor wants the bank to speak for itself.

It covers more than the ending cash balance

Many new treasurers get surprised. A bank confirmation letter isn't always limited to "yes, this account had this balance on this date."

According to guidance on what a bank confirmation form typically verifies, a thorough request may include:

- Account balances as of a specific date

- Loan details tied to the church

- Interest rates and loan terms

- Collateral or security held for liabilities

- Other banking facilities or arrangements

That broader scope matters. If your church has a mortgage, line of credit, or pledged collateral, the auditor wants a fuller picture of the church's banking relationship, not just a screenshot of checking account cash.

What the request usually contains

The exact format varies by bank and by audit firm, but a complete request often includes identifying details so the bank can respond accurately.

Common items include:

| Item | Why it matters |

|---|---|

| Church legal name | Helps the bank match the correct customer |

| Specific confirmation date | Ties the response to year-end or another audit date |

| Account numbers or account identifiers | Prevents confusion between similar accounts |

| Branch or bank contact details | Routes the request properly |

| Authorized signatures | Gives the bank permission to release information |

Some banks still handle this through mail or a secure document process. Others now use digital portals. The same source notes that many banks offer digital options to streamline what used to be a fully paper-based task.

What it is not

A bank confirmation letter is not a replacement for reconciliation. It doesn't remove the need for your church to compare the general ledger, bank statement, and outstanding checks.

It also isn't a guarantee that every internal coding decision in your accounting system was correct. If your church posted a missions gift into the wrong fund on the books, the bank confirmation won't catch that by itself. It verifies what the bank knows. Your internal accounting still needs to explain the ministry purpose attached to the cash.

Practical rule: Treat the bank confirmation letter as independent evidence, not as a substitute for accurate bookkeeping.

That distinction helps treasurers avoid a common misunderstanding. The letter supports the audit. It doesn't do the accounting for you.

Why Churches Need Bank Confirmations for Audits

Churches don't need bank confirmations just because auditors like paperwork. They need them because church money carries trust with it.

When a member gives to the building fund, they aren't just funding a generic bank balance. They're trusting the church to handle that gift according to the stated purpose. When a donor supports missions or benevolence, the same principle applies. A bank confirmation letter helps the auditor test whether the reported cash is real and whether the church's banking records support what leadership says about those funds.

This is about stewardship, not optics

Audit guidance makes an important distinction. Bank confirmations aren't technically required in every situation, but they're a standard audit procedure in many firms, especially when auditors see higher risk around whether cash exists as reported. The same guidance notes that confirmations should be prioritized when the risk of material misstatement is high for the existence assertion of cash, and they are mandatory for first-year audit clients or newly opened bank accounts. It also notes their value in uncovering situations involving fake bank statements and other fraud schemes, and explains why they matter for church systems that manage restricted donations and fund-based accounting. You can read that discussion in this guidance on when auditors use bank confirmations.

For a church treasurer, "existence assertion" is audit language for a very practical question: Does the money reported on the books really exist at the bank?

Why restricted funds make this more important

Restricted funds create a second question. Not only must the money exist, it must also be handled in a way that supports the donor restriction and the church's reporting.

That means the auditor may care about things like:

- Segregation of funds when your church uses separate accounts for certain purposes

- Consistency between fund reports and bank records

- Accuracy in year-end reporting to pastors, elders, finance committee members, and the congregation

- Clarity around designated cash when major projects or benevolence activity are involved

A standard business article might stop at "the bank confirms the balance." For churches, the more important issue is often whether the support for that balance lines up with ministry-specific reporting.

A church example

Suppose your year-end report shows cash set aside for a building project and separate amounts for benevolence and missions. The bank confirmation can help the auditor verify the accounts connected to those balances.

But here's the key nuance. If the auditor requests only one aggregate bank response and your accounting records show separate restricted funds, the evidence may be less useful than you hoped. The books may be correct, yet the audit support may still feel incomplete because the confirmation doesn't reflect the structure the church uses internally.

That is one reason a treasurer should understand the church's fund map before the audit begins. If you're still defining those responsibilities, this guide to church treasurer responsibilities in a non-profit is a helpful reference.

Churches build credibility when they can show not just how much cash they had, but how that cash related to donor intent and board reporting.

What a confirmation does for trust

The biggest benefit is independence. The auditor doesn't have to rely only on a statement you printed or a spreadsheet you prepared. The bank responds directly.

That direct response gives comfort in three directions:

- To auditors, because the evidence comes from an outside institution

- To leadership, because board-level oversight becomes easier when records tie together

- To the congregation, because stewardship claims have support beyond internal reporting

For churches, that isn't a technical bonus. It's part of financial ministry.

The Bank Confirmation Process Step by Step

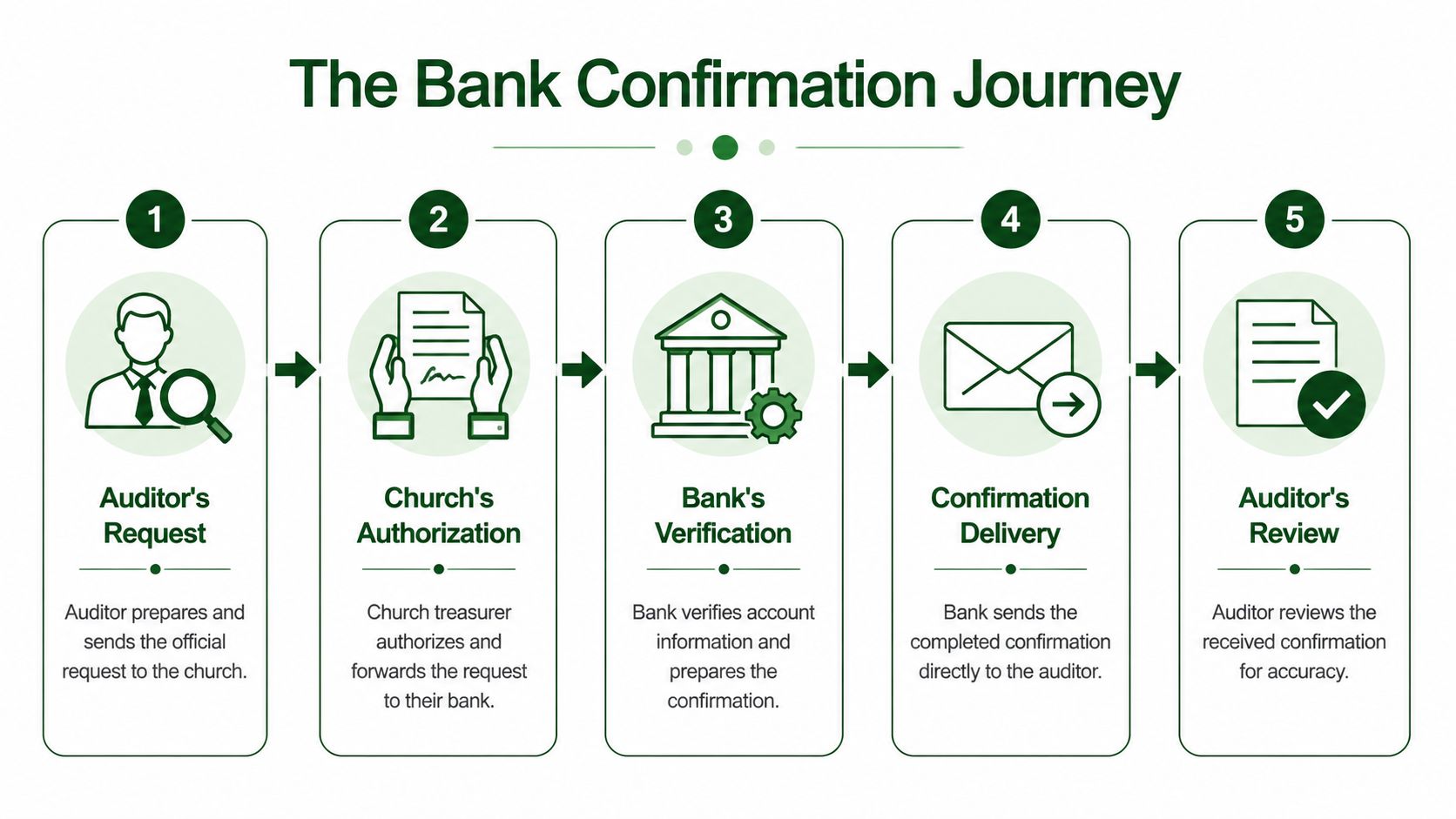

Most confusion comes from not knowing who does what. Once you know the roles, the process is manageable.

At a high level, the auditor prepares the request, the church authorizes it, the bank verifies the information, and the bank sends the answer back to the auditor. That direct bank-to-auditor path protects the integrity of the evidence.

Step one begins with the auditor

The audit firm usually initiates the process. They prepare the confirmation request because the wording, date, and response instructions need to match the audit workpaper requirements.

The request may list deposit accounts, savings accounts, loans, or other banking relationships. If your church has separate accounts connected to different ministry purposes, this is the time to review whether the request identifies the right accounts.

The church gives permission

Banks don't hand over account details just because someone asks. Your church must authorize the release.

That usually means an authorized signer, often the treasurer or another approved officer, signs the confirmation request. Without that consent, the bank may reject the request or leave it sitting in a queue.

A good review at this stage includes:

- Checking the legal church name exactly as the bank uses it

- Confirming account identifiers so the wrong account doesn't get verified

- Matching the confirmation date to the year-end or audit date

- Making sure signer authority is current if officers changed during the year

The request goes to the bank in the approved channel

After the church authorizes the request, the bank needs to receive it through a method the bank recognizes. Depending on the institution, that may be a mailed request, a secure portal, or a confirmation service.

This part often stalls because churches send the form to the branch lobby, while the bank handles confirmations in a centralized department. A quick call to the bank before sending can save days of delay.

If you want a simple overview of why procedures like this matter, this article on understanding business compliance gives a useful non-technical framing. The same principle applies in church finance. Clear processes reduce confusion and make outside verification easier.

The bank completes the verification

Once the bank receives the request and has the church's authorization, the bank verifies the requested information against its records.

The bank may confirm:

| Area | What the bank may verify |

|---|---|

| Deposit accounts | Whether the account exists and the balance on the requested date |

| Borrowings | Whether loans or lines of credit are outstanding |

| Terms | Certain loan terms, interest details, or related conditions |

| Other arrangements | Banking relationships the auditor asked to confirm |

Some banks move quickly. Others take longer, especially if year-end demand is high or the request is incomplete.

If a bank confirmation seems delayed, don't assume the bank lost it. Often the issue is a missing signature, a wrong department, or unclear account identification.

The response goes directly to the auditor

This point matters. For audit evidence to stay reliable, the bank generally sends the completed confirmation directly to the auditor, not back through the church office.

That protects independence. If the church collected the response first, the auditor would lose some assurance that the document arrived unchanged from the bank.

A simple timeline view

If you're trying to picture the sequence, imagine it this way:

- Auditor drafts request

- Church reviews and authorizes

- Bank receives and verifies

- Bank returns response to auditor

- Auditor compares it to church records

What the treasurer should do while waiting

Your work isn't over once the authorization is signed. Use the waiting period to make sure the rest of the audit file is ready.

That includes:

- Reconciling each account to the same date used in the confirmation

- Keeping copies of the signed authorization

- Documenting which account supports which fund

- Preparing explanations for unusual transfers near year-end

Those steps help when the auditor asks follow-up questions, which often happens if an account balance ties cleanly to the bank but not neatly to a restricted fund report.

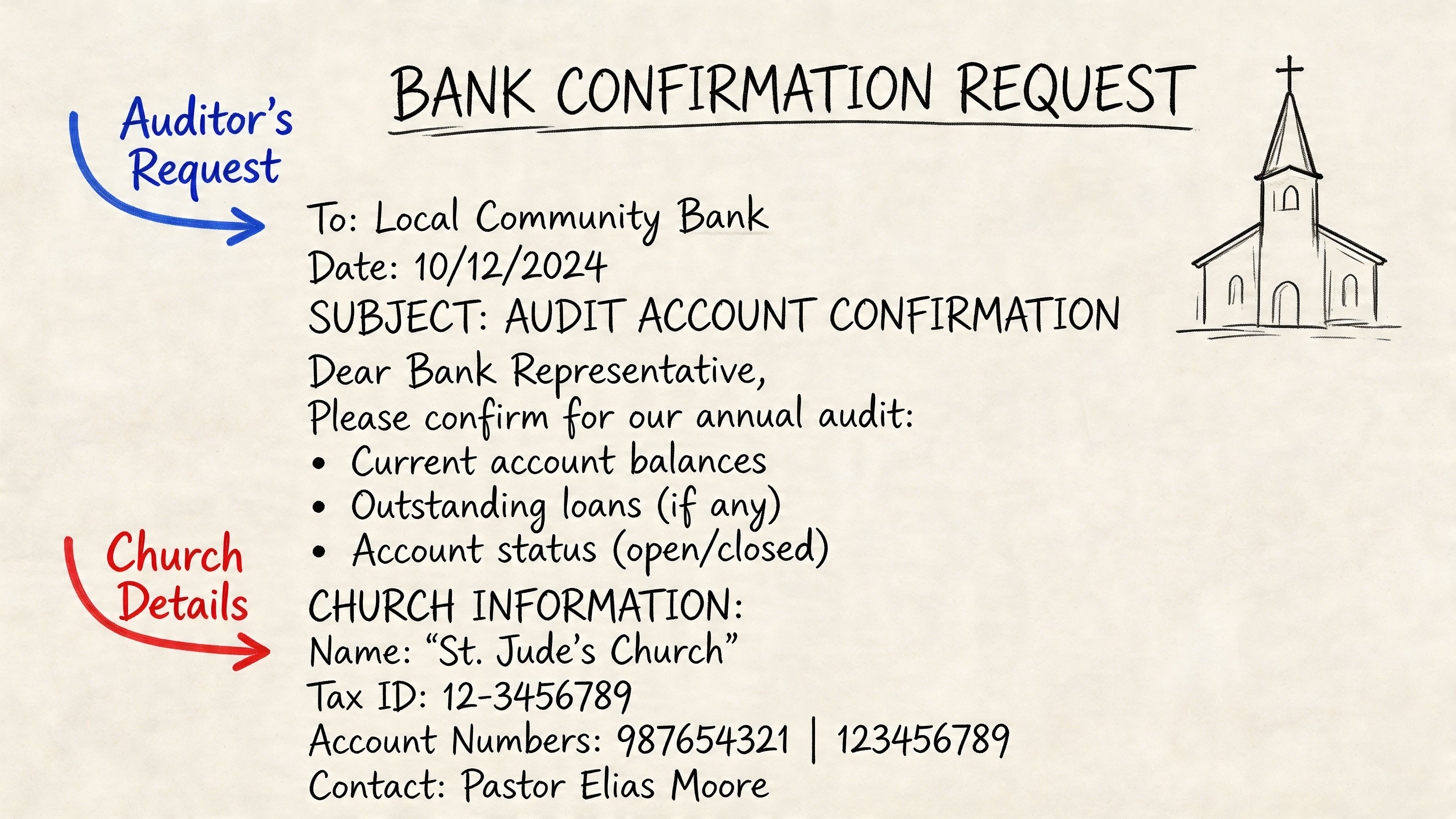

Sample Bank Confirmation Letter Templates for Churches

Most churches won't draft the final confirmation request from scratch. The auditor usually provides the form. Still, it helps to know what a good request looks like, especially when your church has several accounts tied to different purposes.

A standard request may be too generic for church finance. If it only asks the bank to confirm "all balances," you may get a response that is technically correct but not detailed enough to support fund-level reporting. That's why reviewing the wording matters.

A simple church-oriented template

Below is a plain-language example of the kind of information a church may want included in a confirmation request:

Sample request wording

Please confirm the following banking information for First Community Church as of June 30, 2026.Deposit Accounts

Account ending in 1234, Operating Account

Account ending in 5678, Building Fund Account

Account ending in 9012, Missions Fund AccountPlease also confirm any loans, lines of credit, pledged collateral, or other banking arrangements in effect as of that date.

This request is authorized by the undersigned officer of the church for direct response to the independent auditor.

The exact layout may differ by bank. Some forms provide preprinted fields. Others use a letter on audit firm letterhead.

What each part is doing

A useful request does more than state "confirm our balance." Each piece has a job.

- Church identification helps the bank locate the correct customer record.

- As-of date pins the response to the audit period.

- Specific account listing reduces the chance that a meaningful account gets omitted.

- Loans and related obligations give the auditor a fuller picture of the banking relationship.

- Authorization language tells the bank it has permission to respond.

How to adapt it for restricted funds

In this situation, church practice should be more specific than generic business templates.

If your church uses separate bank accounts for ministry purposes, the request can reflect that. The wording doesn't need to be complicated. It just needs to identify the account and the church purpose clearly enough for the auditor to connect the response to the fund reports.

A practical version might list:

| Account reference | Church purpose |

|---|---|

| Account ending in 1234 | General operating |

| Account ending in 5678 | Building fund |

| Account ending in 9012 | Missions fund |

If the church doesn't maintain separate bank accounts for every restricted fund, don't force the template to suggest that it does. In that case, the church's internal accounting records and reconciliations carry more of the explanatory burden.

What to review before signing

Before an authorized officer signs the request, pause and check four things:

- The confirmation date matches the audit date

- The named accounts are complete

- Closed or new accounts aren't forgotten

- Any borrowing arrangements are included

That review doesn't replace the auditor's work. It helps the auditor get a response that answers the church's real reporting questions.

Common Pitfalls and Best Practices

Most bank confirmation problems aren't dramatic. They're small process failures that create avoidable delays or weak audit evidence.

The good news is that once you know the patterns, they're easier to prevent.

Problem one using old manual habits

Many churches now receive donations through tools like Planning Center, Pushpay, Stripe, or ACH-connected workflows. But the confirmation process may still rely on paper forms, manual routing, and waiting for a human at the bank to respond.

That mismatch creates friction. According to this overview of digital verification options for bank confirmations, manual confirmation processes can lag by 3-5 days, while automated API confirmations can provide real-time balances. The same source says 35% of U.S. banks now offer instant confirmation APIs, but a 2025 survey found 60% of auditors were resistant to those newer methods.

The lesson isn't that manual confirmation is wrong. It's that you shouldn't assume your auditor and your bank are using the same process maturity level.

Best practice: Ask early whether the auditor accepts portal-based or API-supported confirmations, and ask the bank which methods it supports.

Problem two the request doesn't fit the church's account structure

A generic form may produce an aggregate response that doesn't help explain restricted cash. The bank may answer the exact question asked, while the church still struggles to show how that answer connects to the building fund or missions reporting.

That creates extra back-and-forth. The treasurer thinks, "The bank confirmed the cash." The auditor thinks, "I still need better support for the fund presentation."

Best practice: Keep a current schedule of all bank accounts, the purpose of each account, and the fund relationships tied to them. Clear documentation matters just as much as the confirmation itself. Strong internal control practices for churches make that schedule easier to maintain throughout the year.

Problem three nobody checks the routing details

Sometimes the issue is not accounting at all. It's administration.

The request goes to a branch that doesn't process audit confirmations. The signer on the form is no longer authorized. The confirmation date is wrong. A new account opened during the year never made it onto the list.

These aren't hard errors to fix. They're just easy to miss when the audit deadline feels close.

Best practice: Before the request goes out, one person should verify bank contact method, signer authority, account completeness, and the exact date being confirmed.

Problem four waiting too long to talk

A treasurer often assumes the bank confirmation is "the auditor's area," while the auditor assumes the church will flag any unusual account setup. That's how surprises happen.

If your church has sweep arrangements, multiple ministry accounts, or separate reserve accounts, bring that up before the confirmation request is finalized. Early conversation is much cheaper than late clarification.

Simplifying Confirmations with Grain and Automation

The hardest part of bank confirmations in churches isn't the letter itself. It's the disconnect between daily financial activity and year-end proof.

Churches receive gifts through online giving tools, move money between accounts, track fund restrictions, and prepare reports for leadership. If those tasks live in separate places, the confirmation process becomes a cleanup project. The treasurer spends year-end proving what should have been clear all along.

A modern fund accounting setup changes that. In systems built for church finance, the records can align from the start. The technical value is described in this document on bank confirmation data and verification requirements, which explains that in modern fund accounting systems a confirmation can function as cryptographic proof validating automated transfers to specific fund accounts. It also notes that technical details like routing information must match system records to create an immutable audit trail and can reduce reconciliation friction from days to hours.

Why that matters in church life

If a member gives to missions through Pushpay or another giving platform, church staff shouldn't have to reconstruct the trail months later by digging through exports, emails, and bank screenshots.

A better workflow keeps the fund assignment, bank movement, and accounting record connected. Then, when the auditor asks for support, the church can show a consistent chain from donation intake to bank activity to fund reporting.

Why secure document handling still matters

Even with stronger automation, banks and auditors still exchange sensitive documents. Churches should take that seriously.

If your team is reviewing how to send or store sensitive financial records, the broader principles in this piece on HIPAA compliant document sharing are useful because they highlight secure handling habits that apply beyond healthcare too.

The goal isn't to eliminate the bank confirmation letter. The goal is to make it the final outside check on a clean system, not the first moment anyone tries to piece the story together.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Build Trust with Every Transaction

A bank confirmation letter sounds technical, but its purpose is simple. It helps your church prove that what appears in the financial records agrees with what the bank shows independently.

For churches, that matters most where trust matters most. Restricted gifts, designated accounts, lending relationships, and year-end balances all affect how leadership reports to the board and congregation. A careful confirmation process supports that trust. It doesn't replace stewardship. It documents it.

When church teams understand the process, ask better questions, and prepare account details clearly, the audit feels less like a disruption and more like a health check. And when the accounting system is built around fund-based church reporting from the start, year-end confirmations become much easier to manage.

Financial clarity gives ministry leaders room to focus on ministry.

If your church wants fund-based accounting that matches how congregations operate, take a look at Grain. Grain is purpose-built for churches, with native fund architecture, bank and giving integrations, and reporting that helps treasurers, pastors, and boards see where every dollar belongs.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.