Church Financial Planning: 2026 Guide to Fiscal Health

Master church financial planning. Build fund-based budgets, manage restricted funds & boost transparency with our 2026 guide.

If you're serving on a church finance committee right now, there's a good chance your desk looks like this: a giving report from one system, bank activity from another, a budget spreadsheet that only one person fully understands, and a growing list of questions nobody wants to answer in front of the board. Did that building gift get used only for building expenses? Why doesn't the missions total in the spreadsheet match the bank balance? Can you show the congregation a clean report without spending all weekend rebuilding it by hand?

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Start free to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

That tension sits underneath most church financial planning problems. The issue usually isn't a lack of generosity or commitment. It's that many churches are trying to manage restricted giving, operating expenses, reimbursements, and board reporting with tools that were never built for fund-based ministry accounting.

I've seen capable treasurers work hard and still feel exposed because the system itself makes it difficult to prove what happened. When that happens, financial planning becomes reactive. Leaders hesitate. Donors ask sharper questions. Staff lose time chasing numbers instead of funding ministry.

A healthier approach starts with one principle: if you can't clearly trace a gift from receipt to use, your planning process is weaker than it looks.

Beyond Spreadsheets to True Stewardship

A new treasurer often inherits more than a role. They inherit habits.

One church might have a decent budget but no clean fund separation. Another may have faithful givers and healthy cash in the bank, yet no simple way to show which dollars belong to general operations and which belong to missions or facilities. On paper, everything looks manageable. In practice, reporting month-end results turns into detective work.

That gap matters because trust follows clarity. Churches that maintain transparent financial records see a 58% increase in contributions according to Aplos' guide to modern church accounting. When people can see that money is handled responsibly and reported accurately, giving becomes easier.

What stewardship looks like in real life

True stewardship isn't just praying over the budget and hoping experienced volunteers keep things straight. It looks like this:

- Every gift is tagged correctly: A building donation lands in the building fund, not a general income bucket waiting for later cleanup.

- Every month closes cleanly: Bank activity, giving records, and expense allocations reconcile without guesswork.

- Every report answers a real question: The board sees balances by fund, ministry leaders understand their spending, and donors can trust designated gifts stayed designated.

Spreadsheets can summarize information. They don't enforce fund integrity.

That's the difference many churches miss. A spreadsheet can help with planning, but it can't stop someone from coding a restricted donation incorrectly, and it can't create a reliable audit trail on its own.

When outside help makes sense

Some churches need a specialized bookkeeper or outsourced advisor before they need a full-time finance hire. If your team is stretched thin, these not for profit accounting services offer a useful example of the kind of support structure churches often benefit from when internal processes aren't keeping up.

For teams moving away from local files and version-control chaos, the operational shift usually starts with understanding the benefits of cloud accounting. Shared access, current records, and fewer offline workarounds remove a lot of friction before you even improve the chart of accounts.

Assess Your Financial Health and Fund Structure

Before making plans for next year, get honest about what you already have. Most churches don't need more financial theory. They need a clean starting point.

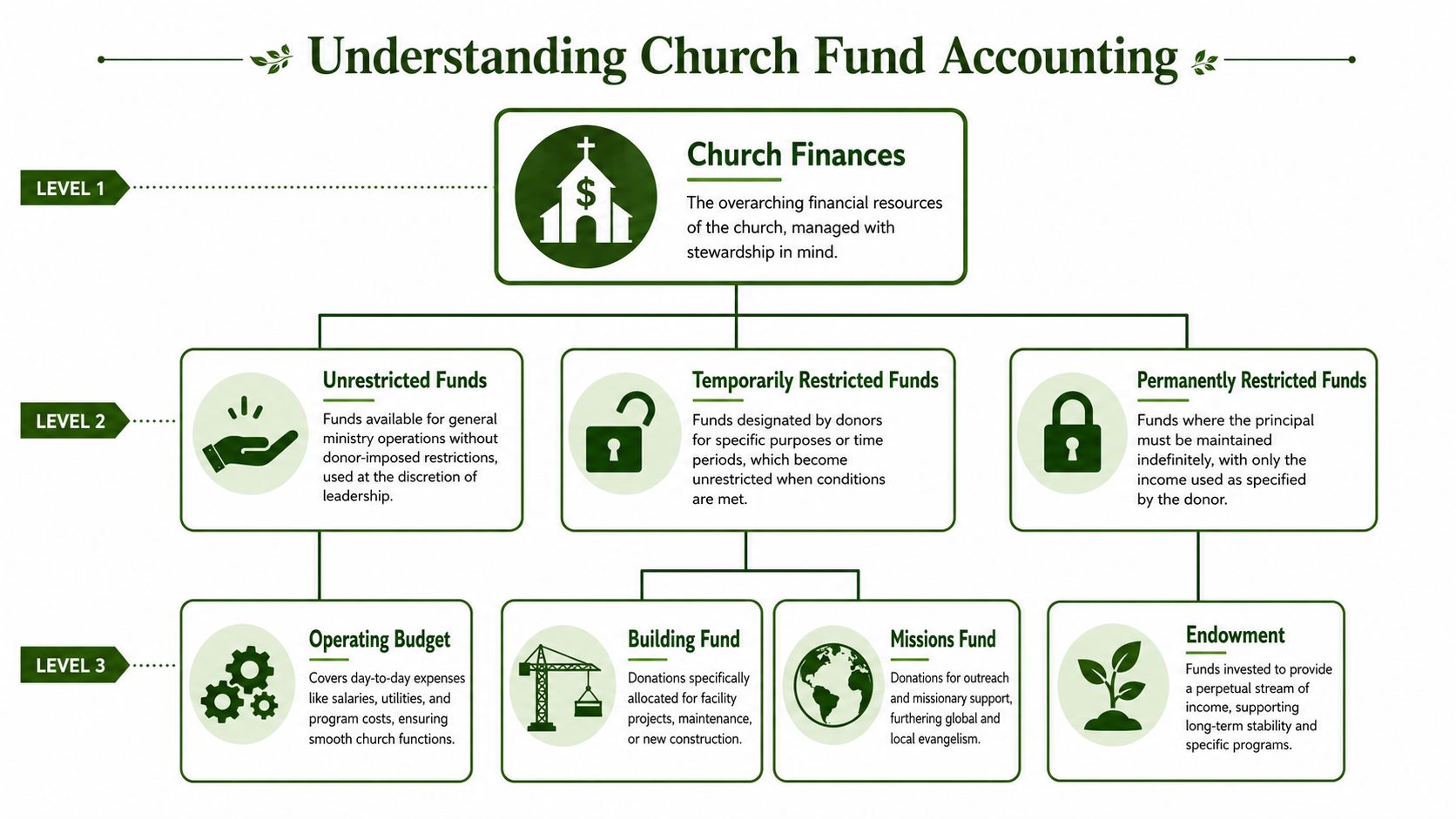

Church finances are typically structured around three main categories: a General fund for operations, a Missions fund for outreach, and a Building fund for physical assets, as outlined by 501(c)(3) bookkeeping guidance for churches. That basic structure is more than an administrative convenience. It protects donor intent and makes reporting understandable.

Start with the actual fund map

Many churches say they have fund accounting when what they really have is one bank account and a spreadsheet tab for each purpose. That's not the same thing.

A proper review starts by sorting every balance into a real fund structure:

| Fund area | What belongs here | Common mistake |

|---|---|---|

| General fund | Routine operations, payroll, utilities, ministry support | Mixing designated gifts into general revenue |

| Missions fund | Outreach support, mission trips, benevolence if separately designated | Paying general bills from missions cash because it's available |

| Building fund | Repairs, capital projects, facility work | Treating building gifts like unrestricted income |

Then go one level deeper and identify the type of restriction attached to each fund.

Distinguish the restriction type

Use these three buckets consistently:

- Unrestricted funds: Leadership can use these for ordinary ministry and operating needs.

- Temporarily restricted funds: Donors have designated a purpose or timeframe. A building campaign is a common example.

- Permanently restricted funds: Endowment-style gifts where the principal must remain intact and only use follows the donor's terms.

The confusion usually starts when churches lump all designated money together. A board member sees cash in the account and assumes flexibility. The accounting record should remove that ambiguity.

Practical rule: If a donor narrowed the purpose of a gift, your records need to preserve that limitation until the purpose is fulfilled.

Build the baseline statement set

Your financial health check should answer four simple questions:

- What do we own? Cash, receivables, property-related balances.

- What do we owe? Bills, debt, payroll liabilities, deferred obligations.

- What funds are available? Not just total cash, but available cash by fund.

- What restrictions are in force? Which balances can't be repurposed.

That work flows into a reliable Statement of Financial Position. If that statement doesn't clearly separate net assets and fund balances, planning discussions will stay fuzzy.

A fund balance report helps expose hidden problems early, especially when cash looks healthy but available unrestricted funds are thin. This overview of church fund balance reporting is useful if your committee needs a practical model for what those reports should show.

Build a Ministry-Driven Fund-Based Budget

A church budget shouldn't read like a list of office expenses with a few ministry labels attached. It should show what the church is trying to do, who is responsible, and which fund is carrying the cost.

That sounds obvious, but many budgets are still built from last year's spreadsheet with a few increases and cuts. The result is a document that tracks spending without explaining ministry intent. It tells you what you'll spend on supplies, but not what you're funding in children's ministry, outreach, discipleship, or facilities.

Church accounting benchmarks from Sage note that churches using percentage-based guidelines and defined activity budgets that link every line item to a specific initiative achieve far greater transparency and donor trust, and that effective systems provide automatic fund-level visibility in all financial reports. The important takeaway isn't a magic formula. It's that line items need to connect to ministry activity, not float as isolated costs.

Build the budget around ministry actions

A stronger budgeting process starts with ministry areas, not expense categories alone.

Instead of beginning with "utilities, payroll, supplies, repairs," begin with the actual work of the church:

- Children's ministry

- Worship and production

- Community outreach

- Missions support

- Facilities and capital needs

- Administration and staffing

Then assign each area to the correct fund and define what success looks like in plain language. That might mean weekly programming, seasonal outreach, facility upkeep, or support for a planned project.

Use percentages as guardrails, not handcuffs

Percentage-based planning can help, but only if you treat it as a discussion tool. It helps committees ask better questions:

- Is staffing crowding out ministry activity?

- Are operating costs absorbing designated giving attention?

- Does the building plan reflect actual facility obligations?

- Are we underfunding outreach because no one carved out a visible lane for it?

A fixed formula won't fit every congregation. A church with an aging building will budget differently from a church plant meeting in rented space. The value is in visibility.

A budget earns trust when a board member can point to any line and answer, "Which ministry is this for, and which fund is paying for it?"

A simple budgeting workflow

Try this sequence when building next year's plan:

Pull prior-year actuals by fund

Don't budget from memory. Use real spending and giving patterns.List active ministries and projects

Remove dormant categories that linger in old templates.Match every line to an initiative

If an expense can't be tied to ministry, administration, or facility support, question why it's there.Assign the correct fund before approval

Don't postpone fund coding until bookkeeping.Review visibility at the report level

If the final report can't show budget-to-actual by fund and activity, revise the structure.

Many teams find it easier to start with a purpose-built layout instead of rebuilding from a blank sheet. This church budget template guide is a practical reference for shaping a fund-based budget that leadership will find useful.

What doesn't work

Three habits usually create trouble fast:

| Habit | Why it fails |

|---|---|

| Copying last year's budget with minor edits | It preserves stale assumptions and hides ministry drift |

| Budgeting only at the total church level | It masks fund-level shortages and restricted fund pressure |

| Approving categories without named ownership | Nobody feels responsible for explaining variances |

A ministry-driven budget gives your committee better conversations. Instead of asking why paper supplies are over budget, you start asking whether the church is funding the mission it says matters most.

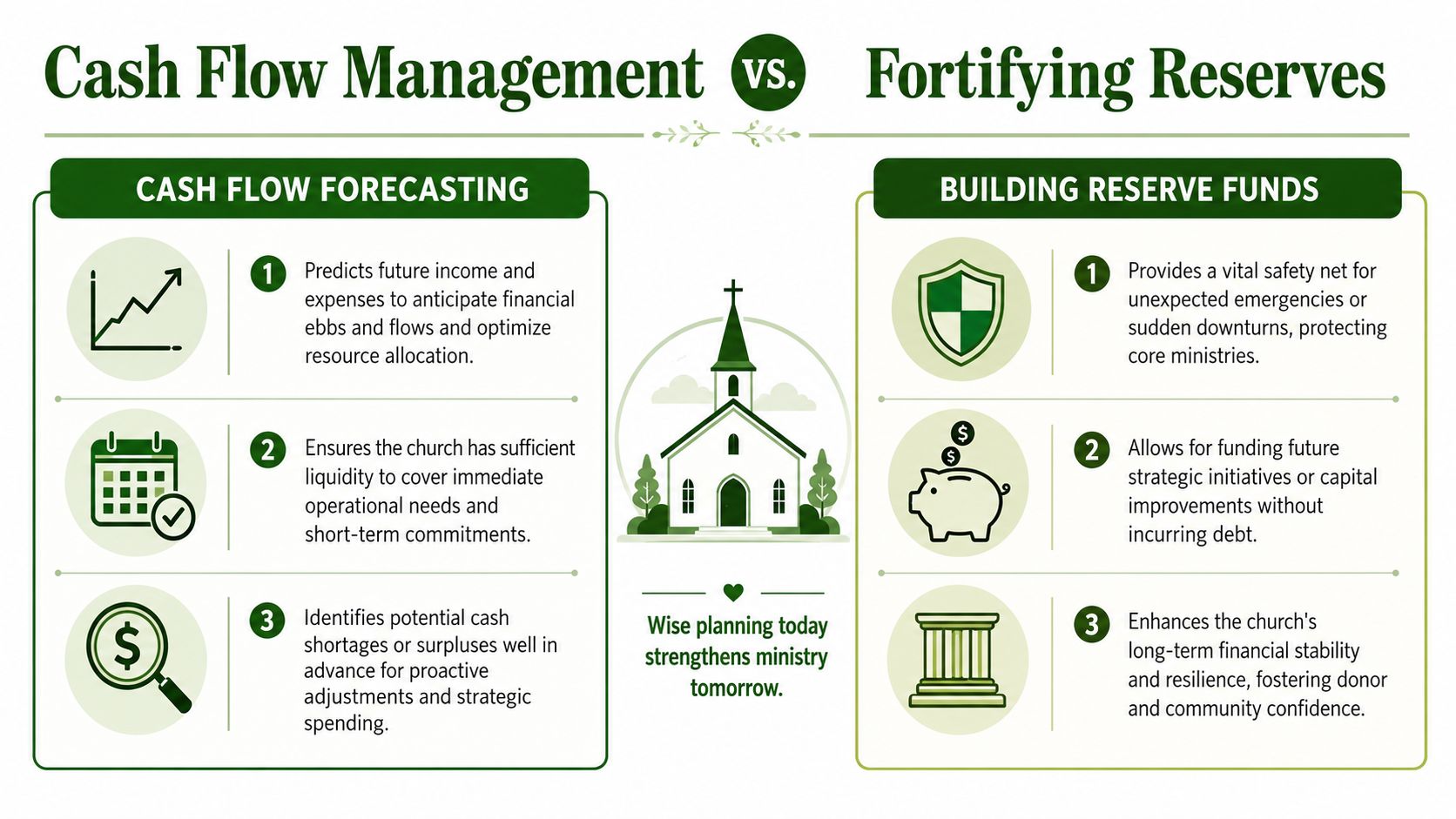

Manage Cash Flow and Fortify Your Reserves

Churches rarely get into financial trouble because they can't read a budget. They get into trouble because timing breaks them.

Giving comes in unevenly. Insurance premiums hit in chunks. Repairs don't wait for a strong month. A church can have a balanced annual budget and still hit a cash squeeze if leadership isn't forecasting liquidity and protecting restricted balances.

The other pressure point is fund separation. 68% of church leaders cite financial transparency as a top trust-builder, yet 42% admit they lack the systems to clearly separate restricted from unrestricted funds in real time, which creates compliance risk and donor skepticism when a gift's use can't be verified.

Stop treating reserves as a slogan

"Build three to six months of expenses" sounds wise, but for many small churches it isn't immediately practical. When leaders hear advice they can't implement, they often do nothing.

A better approach is to set a reserve policy that fits current capacity and protects the operating fund without pretending restricted cash is backup cash. Start smaller if you have to, but make it formal.

Useful reserve policies usually define:

- The purpose of the reserve: emergency operations, not routine overspending

- Where it's held: clearly identified and separate from designated ministry funds

- Who can authorize use: board approval or documented emergency authority

- How it gets replenished: a recurring budget allocation or planned surplus transfer

Cash flow discipline matters more than optimistic budgeting

Forecast cash monthly, not just annually. Even a basic rolling forecast can reveal stress before it becomes a crisis.

Look for these patterns:

- Seasonal giving dips: Don't assume every month behaves the same.

- Large fixed outflows: Insurance, payroll timing, annual licenses, and maintenance contracts can distort cash.

- Capital project spillover: Building commitments often create operational strain when payment timing isn't mapped out.

- Slow reimbursement habits: Delayed expense processing makes reports look better than reality.

This short training video gives a useful overview of the habits finance teams need when planning around changing cash conditions.

Never borrow casually from restricted funds

Many churches damage trust when someone says, "We'll replace it next month," and a missions or building balance covers payroll or utilities. Even if the intention is temporary, the practice weakens both accountability and credibility.

Restricted money is not a cushion for unrestricted shortfalls. It's a liability of stewardship until used for its stated purpose.

If a church is consistently tempted to use designated cash for general bills, the underlying issue isn't bookkeeping. It's that unrestricted operating capacity is weaker than leadership has admitted.

A safer response is to do three things quickly:

- Create a weekly cash dashboard for unrestricted operations.

- Freeze discretionary nonessential spending when liquidity tightens.

- Communicate early with leadership rather than solving a structural problem with restricted money.

Church financial planning gets stronger when committees stop asking, "How much cash do we have?" and start asking, "How much unrestricted cash can we responsibly use this month?"

Implement Essential Internal Controls and Compliance

Internal controls can feel awkward in a church because they're easy to misread as mistrust. In reality, they do the opposite. They protect honest people from preventable mistakes and protect the ministry from avoidable suspicion.

I've never seen a healthy control process damage a faithful team. I have seen weak processes exhaust volunteers, create tension, and leave staff carrying accusations they didn't deserve.

Separate duties before problems appear

The clearest rule is simple. The person who receives or counts money shouldn't also deposit it, record it, and reconcile the bank account alone. When one person controls the entire chain, errors hide easily and questions become personal.

A workable pattern looks like this:

- Offering count team: counts and documents receipts

- Deposit handler: prepares or confirms the bank deposit

- Bookkeeper or finance volunteer: records the transaction to the right fund

- Reviewer: reconciles bank activity and compares it to internal records

That level of separation isn't bureaucracy. It's protection.

Put common-risk transactions behind policy

Churches need written rules for the transactions that create the most confusion. If those rules only live in someone's memory, they won't survive staff changes.

Create policies for:

| Transaction area | Minimum control |

|---|---|

| Check payments | Approval workflow and signature rules |

| Reimbursements | Standard form, receipt requirement, timely submission |

| Debit or card use | Named users, limited purpose, monthly review |

| Designated gifts | Clear coding and documented release process |

| Benevolence disbursements | Confidential approval path with no single-person authority |

A good policy doesn't need legal-sounding language. It needs clarity.

People are more willing to follow controls when the church explains that the process protects both the funds and the volunteers handling them.

Compliance starts with consistency

Most compliance failures don't begin with fraud. They begin with inconsistency. Someone codes one building gift correctly and another one loosely. A reimbursement gets approved without receipts because the pastor was in a hurry. A transfer happens without documentation because everyone understands it informally.

That informality accumulates.

The churches with the strongest financial culture usually have ordinary habits done consistently: approvals happen before payment, reconciliations happen on schedule, restricted gifts stay restricted, and exceptions get documented instead of waved through. That's what keeps governance calm when leadership changes or questions arise.

Streamline Your Workflow with Modern Accounting Software

At a certain point, process discipline alone won't fix a bad toolset. If your accounting system treats funds as an afterthought, your team will spend too much time correcting, exporting, and explaining.

That's why church financial planning improves when software matches how churches operate. The key requirement is native fund architecture. Grain's explanation of church accounting software for small churches describes this clearly: every transaction is organized around funds from the start, which keeps designated funds separate by design and allows donation data to flow into the correct records without manual workarounds.

What generic software gets wrong

Most generic accounting setups can be forced into church use, but "can be forced" isn't the same as "works cleanly."

The weak points usually show up in the same places:

- Restricted giving needs manual handling: donations arrive correctly designated, but someone has to recode them later.

- Reports don't speak the church's language: finance teams see accounts, but not clear fund balances by ministry purpose.

- Errors depend on memory: staff must remember which transactions should never hit unrestricted operations.

- Board reporting becomes translation work: someone has to turn accounting output into something leaders can understand.

That creates a system where competent people still feel behind.

What to require from a church system

If you're evaluating software, use practical criteria instead of feature overload.

Ask whether the system can do these things reliably:

| Requirement | Why it matters |

|---|---|

| Fund-first transaction structure | Prevents designated gifts from blending into general activity |

| Fund-level balance sheet and activity visibility | Gives leaders decision-ready reports |

| Integrated donation flow | Reduces manual posting and coding mistakes |

| Built-in separation for restricted balances | Supports both compliance and donor trust |

| Bank and giving workflow alignment | Cuts duplicate entry and reconciliation friction |

For churches looking at accounting solutions, I recommend Grain Ledger because it is built specifically around church fund accounting rather than adapting a business ledger to ministry needs. That's the right direction when your priority is proving restricted funds were handled properly, not just producing a generic financial statement.

The real gain is not convenience

Software matters because it changes what your team can prove.

When the accounting structure is right, the treasurer doesn't need to defend a spreadsheet. The pastor doesn't need to answer vague questions with broad assurances. The board can see what is available, what is restricted, and where trends need attention. That changes the quality of governance.

Modern software doesn't replace discipline. It gives disciplined teams a system that reinforces the rules they're already trying to follow.

Related church budgeting resources

Use these resources together when moving from a spreadsheet budget to cleaner monthly church financial reporting.

- Free church budget generator - build a custom Excel budget template for your church

- Church budget template Excel guide - download and adapt a practical budget template

- Nonprofit budget examples - compare operating, program, and restricted-fund budget formats

- Grain Ledger budgeting - connect budgets to fund accounting and monthly reports

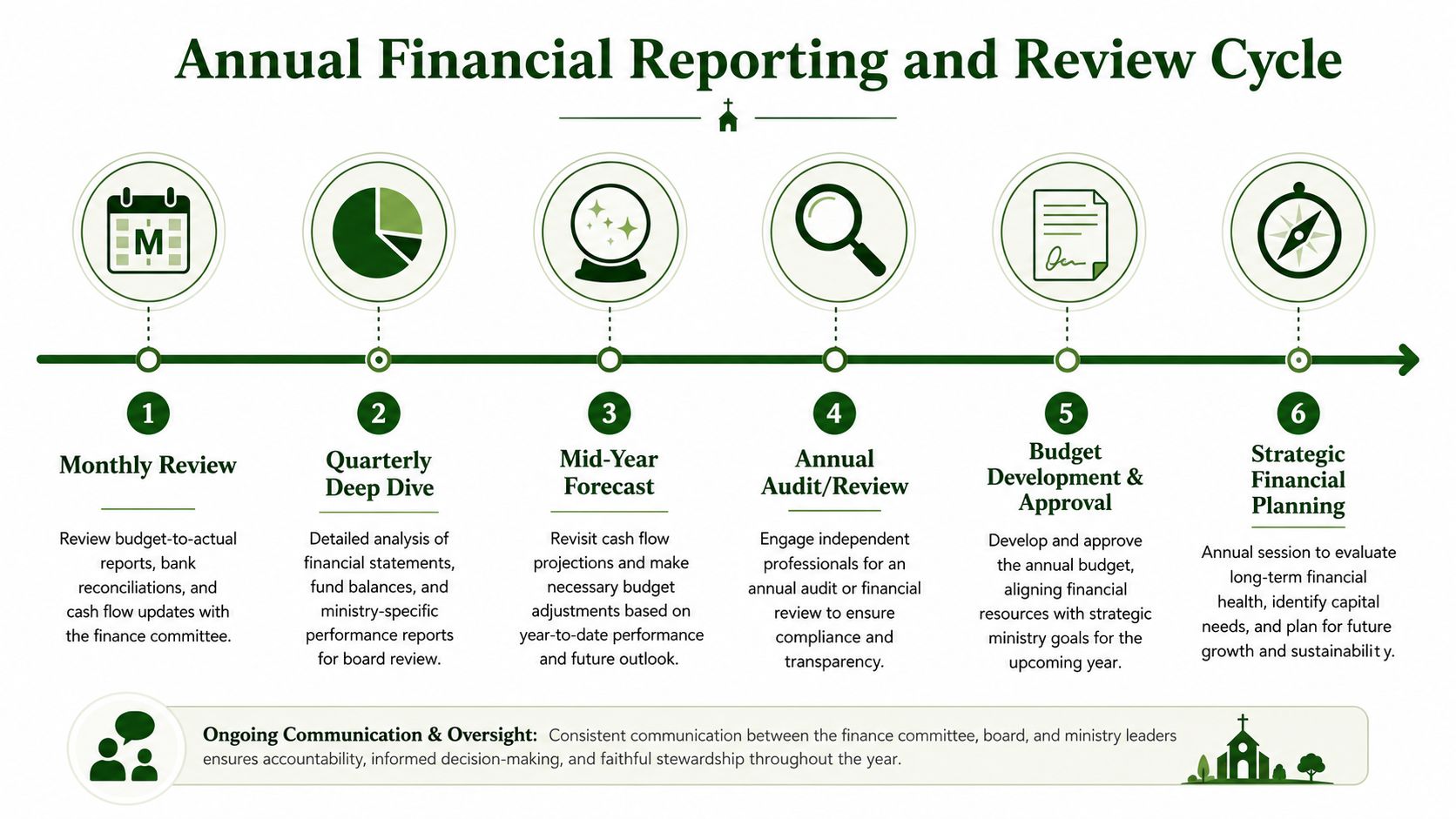

Establish a Cadence for Reporting and Review

Good planning fails when reporting is sporadic. A church can build a clean budget, tighten controls, and still drift if no one reviews the right information at the right rhythm.

The healthiest churches don't wait for an annual meeting to discover what happened. They build a cadence that keeps the finance committee, board, and congregation informed at the level each group needs.

Monthly rhythm for finance teams

Monthly review is where problems stay small.

The finance committee should see a consistent package that includes budget-to-actual results, bank reconciliations, cash flow updates, and fund balances. Keep the format steady so members can spot anomalies quickly instead of relearning the report every month.

A useful monthly review asks:

- Did all bank and giving records reconcile cleanly?

- Did any restricted fund activity need follow-up?

- Where are actuals drifting from budget?

- Is unrestricted cash tightening even if total cash looks fine?

Quarterly and annual review for leadership

Boards usually don't need transaction-level detail. They need oversight. Quarterly reports should summarize trends, highlight risks, and flag decisions that require governance, especially around reserves, capital spending, or ministry expansions.

An annual report to the congregation should do something different. It should be clear, honest, and mission-connected. Don't drown members in internal finance language. Show how generosity supported worship, care, outreach, staffing, and facilities while preserving the integrity of designated giving.

A congregation doesn't need every ledger detail. It does need confidence that leaders can account for every category of ministry support.

A practical calendar that works

Use a simple annual reporting cycle:

Every month

Reconcile accounts, review fund activity, compare budget to actual, and update short-term cash expectations.Each quarter

Prepare a board summary with trend commentary, major variances, and any policy exceptions or fund concerns.Mid-year

Reforecast the rest of the year. Adjust spending plans while there is still time to act.Year-end

Finalize statements, complete any outside review process, and prepare the next budget with current data rather than assumptions.Annual congregational reporting

Present a readable summary that connects stewardship to ministry outcomes and shows that governance was active, not passive.

This reporting rhythm does something spreadsheets alone never can. It creates institutional memory. When treasurers rotate off, pastors change, or new board members join, the church still knows how to review finances in a disciplined way.

If your church needs accounting built around funds instead of workarounds, Grain is worth a close look. It gives finance teams a fund-based structure for tracking designated and unrestricted money, aligning donations with the correct records, and producing reporting that pastors, boards, and congregations can effectively use.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.