Fund Balance Reporting for Churches: Simplified 2026

Simplify church fund balance reporting in 2026. Learn fund classifications, stewardship, and best practices to manage donor funds with confidence.

A finance committee meeting often starts with a simple question that isn't simple at all.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

Someone asks, “We raised money for the mission trip, so why doesn't the account balance match what people gave?” Another board member asks whether the church can use part of the building fund to cover a short-term cash crunch. The pastor wants a quick answer. The treasurer knows the numbers are somewhere in a spreadsheet, but the story behind those numbers is harder to explain.

That's where fund balance reporting matters.

For churches, the significant issue isn't just how much cash is in the bank. It's whether that cash is available for general ministry, set aside by the board, or restricted by donors for a specific purpose. A church can look healthy from the outside and still be tight on usable funds. It can also look cash-poor in one area while holding resources that must remain untouched for another.

Good reporting turns confusion into stewardship. It helps boards answer honest questions, protects donor intent, and gives pastors better information for decisions that affect ministry week by week.

Beyond the Bank Balance Understanding Church Finances

A new board member usually sees the checking account first. That's natural. If the church has money in the bank, the assumption is that the church can spend it. In church finance, that assumption causes most of the confusion.

Take a common situation. The youth pastor thanks the congregation for generous giving toward camp scholarships. The missions team has also received designated gifts. At the same time, the church still needs to pay utilities, payroll, and insurance. When all of that money lands in one bank account, the balance can look larger than the amount the church can use for normal operations.

Why the bank balance misleads

The bank balance answers one question only. It tells you how much cash is present.

It doesn't tell you:

- What donors restricted for a particular ministry

- What the board has set aside for a future need

- What remains available for day-to-day ministry expenses

- Whether a fund has been overspent even if total cash still looks positive

That's why fund balance reporting is less about accounting jargon and more about communication. It gives the church a way to say, “Yes, we have this money, but here's what it's for.”

A healthy church report doesn't just show dollars. It shows the purpose attached to those dollars.

Many church leaders struggle with how to translate GASB-type fund balance concepts into practical policy. Guidance like GFOA's, framed around a 15 to 25% range of operating expenditures for unrestricted fund balance, doesn't address the seasonal giving patterns or capital campaigns common in churches, which leaves a gap for church-specific practice, as noted in GFOA's general fund balance guidelines.

That gap is why practical finance leadership matters. If you want an outside perspective on how better reporting supports better decisions, Nexist's virtual CFO insights offer a useful lens on how finance structure improves clarity for leadership teams.

The stewardship question behind the numbers

When a donor gives to benevolence, missions, or a building project, the church takes on a responsibility. The issue is no longer “Did the deposit clear?” The issue is “Are we tracking that gift in a way that honors its purpose?”

If you need a plain-language primer before going deeper, this overview of what a fund balance means in church accounting is a helpful starting point.

Churches don't need more complicated reports. They need reports that answer ordinary questions clearly.

The Foundation of Church Finance Fund Accounting Principles

Church accounting feels different from business accounting because it is different.

A business mainly asks whether sales cover expenses and produce profit. A church asks a different question. It asks whether resources were received, tracked, and used according to purpose. That's why fund accounting exists.

The envelope way to think about it

The simplest analogy is a set of envelopes on a kitchen counter.

One envelope holds grocery money. Another holds vacation savings. Another holds money for a child's school expenses. All of it belongs to the same household, but each envelope has its own purpose. You wouldn't treat those amounts as one pile if you wanted to stay organized.

Church funds work much the same way:

- General fund supports regular ministry operations

- Building fund tracks gifts for facilities or major property work

- Missions fund holds support designated for outreach or partners

- Benevolence fund helps meet approved care needs

The church may use one bank account or several, but the accounting still has to separate the purposes.

The two categories most boards need first

Before anyone learns five classifications, most churches should get clear on two basic ideas.

Unrestricted funds are available for general use. These are the resources leadership can apply to budgeted operations without violating donor intent.

Restricted funds are limited by outside direction, usually from donors. If a member gives to a mission trip, those funds are not available for copier leases or payroll.

Practical rule: If someone outside church leadership determined the purpose of the gift, treat that money with a higher level of care and clarity.

Confusion usually starts when leaders think “set aside” and “restricted” mean the same thing. They don't.

A board can decide to reserve money for future equipment, but that's an internal decision. A donor restriction comes from outside the board. That difference matters in both reporting and stewardship.

Why this matters beyond bookkeeping

Fund accounting protects relationships.

It protects the donor who wants confidence that a designated gift reached the right ministry. It protects the treasurer who needs a defensible record. It protects the board from making short-term decisions that create long-term trust problems.

For a fuller walkthrough of the mechanics, this guide to fund accounting basics for churches lays out the core structure in a practical way.

If a board member understands the envelope concept, most of church finance becomes far easier to follow.

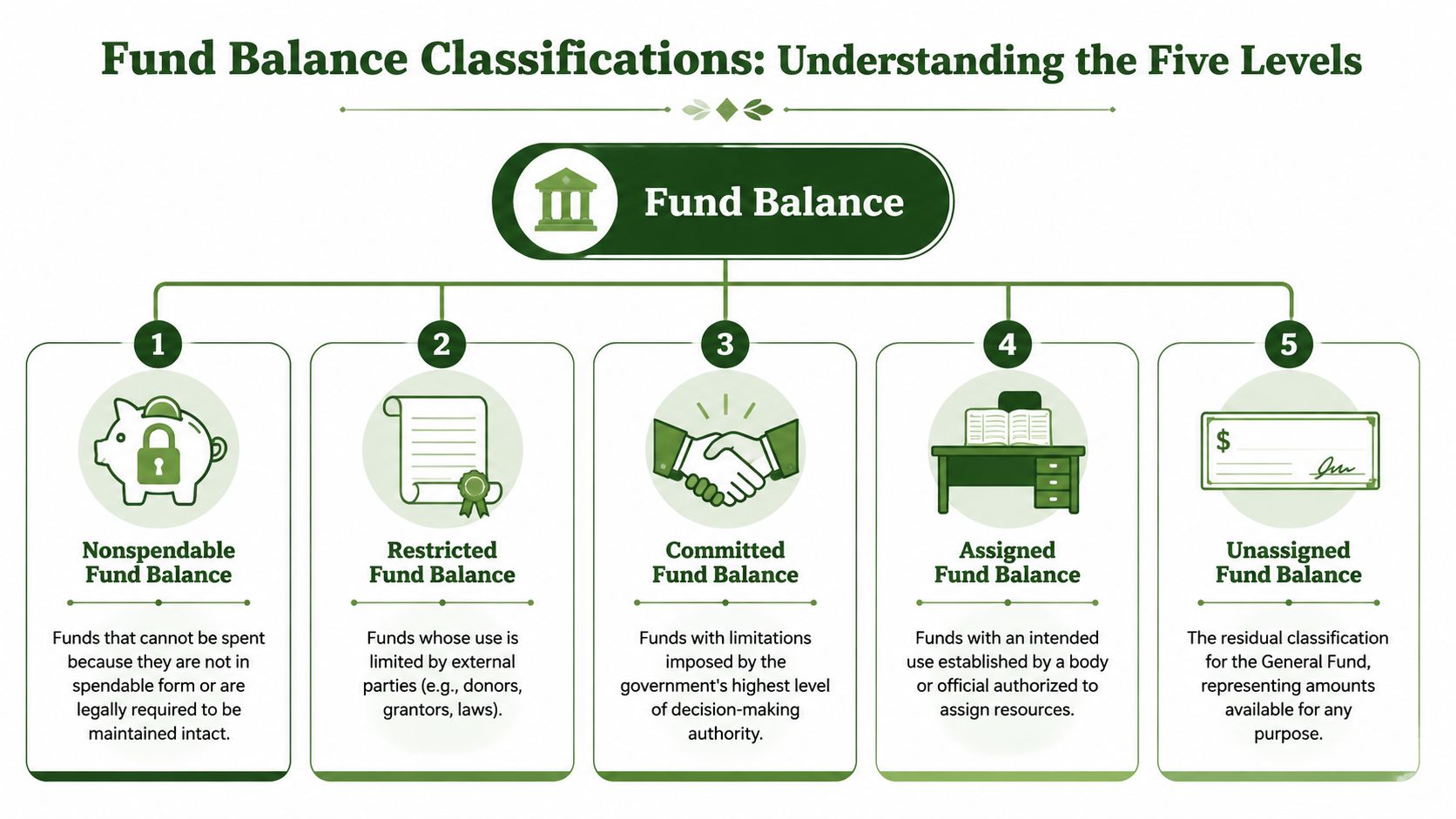

Decoding the Five Fund Balance Classifications

Governmental accounting gave the clearest formal framework for classifying fund balance. GASB Statement No. 54, effective for fiscal years after June 15, 2010, restructured fund balance into five components: nonspendable, restricted, committed, assigned, and unassigned. That change increased transparency by separating externally constrained funds from internally earmarked amounts, as described by the Civic Federation's summary of GASB 54.

Churches aren't governments, but the framework is useful because it answers a very church-shaped question: what kind of claim sits on this money?

The five categories in church language

Nonspendable means the church can't spend the amount because it isn't in spendable form or must remain intact.

Church example: prepaid insurance, deposits, or an amount legally required to be preserved.

Restricted means an outside party placed the limit on use.

Church example: gifts designated by donors for a building campaign, benevolence, or a mission trip.

Committed means the church's highest decision-making body imposed the limit through formal action.

Church example: the elder board votes to reserve part of the general fund for future roof replacement.

The video below gives a useful visual explanation of how classifications work in practice.

Assigned means leadership has expressed an intended use, but with less formality than a board-level commitment.

Church example: the finance committee marks a balance for upcoming curriculum purchases.

Unassigned is the residual balance available for general use.

Church example: the portion of the general operating fund not otherwise constrained.

A quick comparison

| Classification | Definition | Church Example |

|---|---|---|

| Nonspendable | Not in spendable form or required to remain intact | Prepaid annual insurance |

| Restricted | Limited by external parties such as donors or laws | Designated building campaign gifts |

| Committed | Limited by formal action of the highest governing body | Board-approved reserve for future van replacement |

| Assigned | Intended for a specific use by authorized leadership | Amount earmarked by staff or finance leaders for ministry supplies |

| Unassigned | Residual amount available for general purposes | General operating balance available for the church budget |

Where boards get tripped up

The sticking point is usually the middle three.

Restricted is external. Committed is formal and internal. Assigned is internal but lighter. Once a board understands those distinctions, fund balance reporting becomes much easier to read and explain.

A strong church report doesn't merely sort money into buckets. It shows which buckets leadership may move, which require formal action, and which should not be touched for another purpose.

Preparing and Presenting Your Fund Balance Report

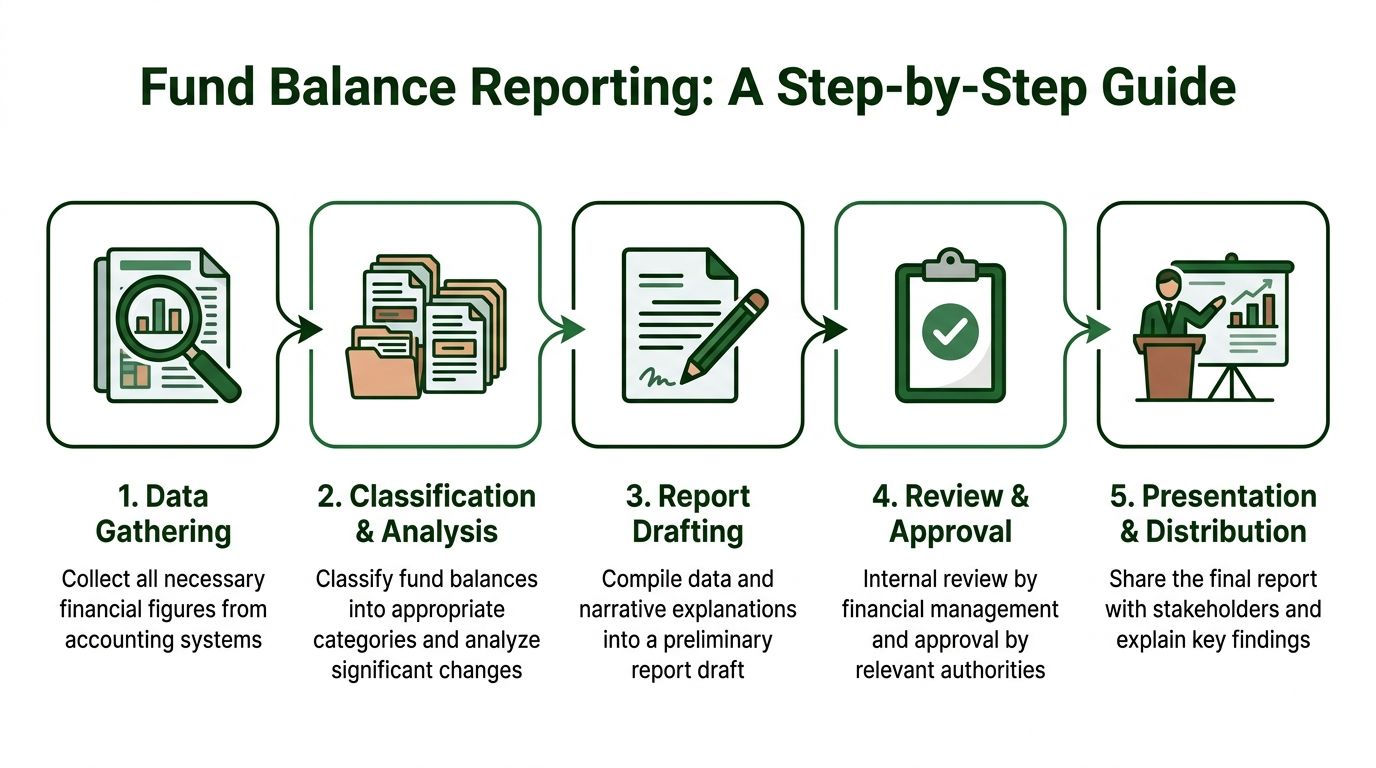

Most churches don't need a more complex report. They need a report they can reproduce every month without drama.

A useful fund balance report starts with clean inputs and ends with a format the board can understand in a few minutes. If the treasurer needs ten minutes just to explain the columns, the report is still doing too much work in the wrong places.

Start with the fund list

Begin by listing every active fund the church uses. This usually includes the general fund plus any designated ministry, building, missions, benevolence, or scholarship funds.

Then gather the current balances and recent activity for each one. Don't start classifying anything yet. First make sure the underlying transactions are posted to the right fund.

A practical guide to preparing church financial reports can help if your monthly packet still feels scattered.

Classify each balance before you format it

Once the balances are right, apply the classifications consistently.

Use a short working checklist:

- Identify outside restrictions: Did a donor, grant, or legal requirement limit the use?

- Review formal board actions: Did the elder board or equivalent body approve a reserve or commitment?

- Note management intent: Did authorized leaders set money aside without formal board commitment?

- Leave the residual balance visible: What remains available for general use after the above categories?

Many churches immediately improve their reporting. They stop reporting one broad “fund balance” line and start reporting the reason behind the balance.

Add note disclosures that explain authority

Numbers alone won't answer every board question. Short notes matter.

GASB 54 requires disclosures about the authority and actions leading to committed and assigned fund balances. Churches using the same discipline should similarly disclose which body established the commitment and what formal action was taken, as outlined in the California Department of Education's GASB 54 guidance.

If the board reserved money for a van, say who approved it and how. If staff merely intended a use, say that too. The difference is part of the story.

Keep the report readable

A clear monthly report often includes:

- A fund column: One line per fund

- A classification view: Restricted, committed, assigned, and unassigned where applicable

- A short note section: Brief descriptions of major purposes and approvals

- A variance comment: A plain-language explanation for unusual changes

That format respects both finance detail and board attention span.

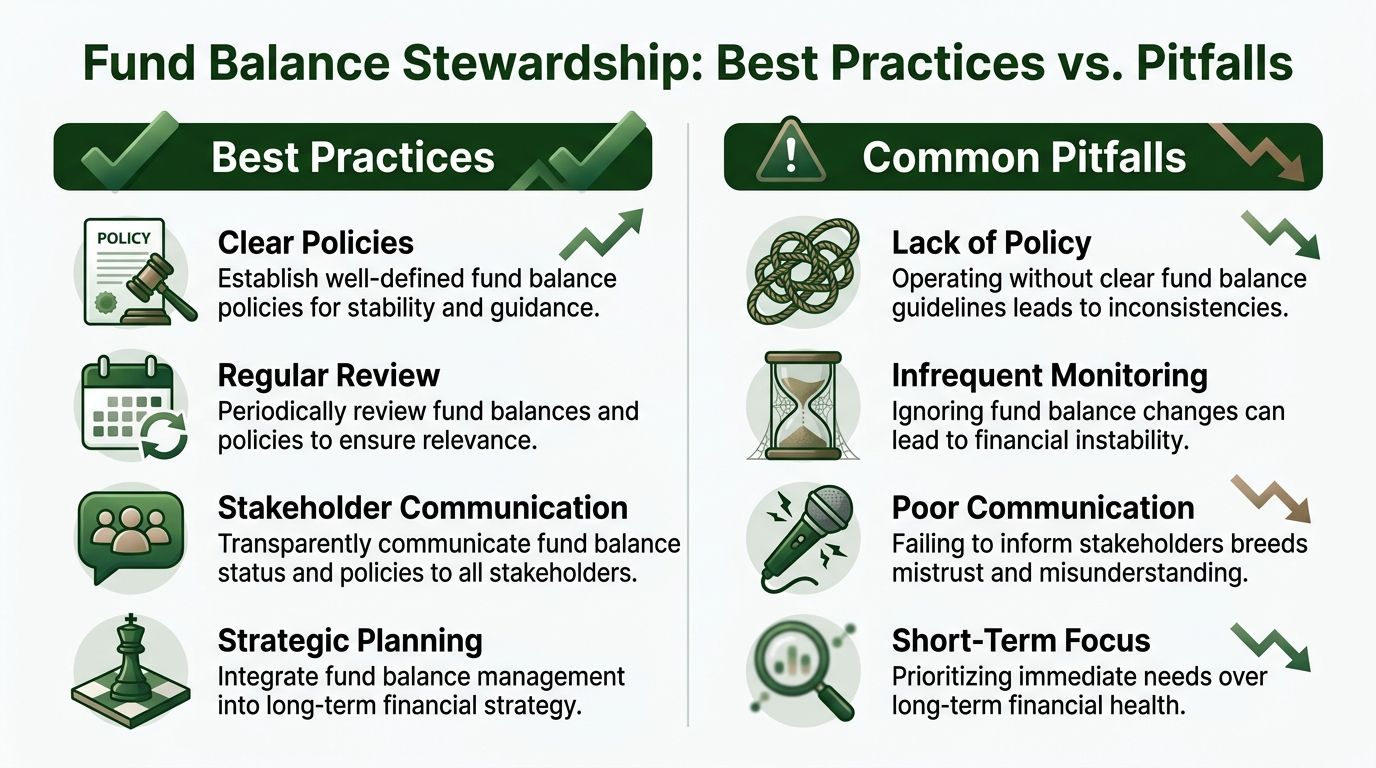

Stewardship Best Practices and Financial Policies

A report shows where the church stands. A policy tells the church what to do next.

Without policy, the board ends up making every decision in the moment. That usually means reserves drift, restricted funds get treated casually, and the treasurer carries more pressure than the system should place on one person.

Set a reserve policy before you need one

A widely used benchmark in public finance is maintaining an unrestricted general fund balance of at least two months, or about 16 to 17%, of regular operating expenditures, according to the MRSC summary of GFOA reserve guidance. That same source notes some governments maintain materially more, sometimes 25 to 30%, where revenue is volatile or risks are higher.

Churches aren't cities, but the logic still applies. Giving fluctuates. Summer attendance shifts. A boiler fails at the wrong time. Insurance deductibles don't wait for a strong offering week.

Board-level takeaway: The reserve question isn't “How little can we hold?” It's “What cushion protects ministry when giving or expenses move suddenly?”

Put the boundaries in writing

Every church should have a short written policy that answers a few practical questions:

- What counts as unrestricted reserve

- Who may designate funds internally

- What formal action creates a commitment

- Whether and when board review is required

- How restricted gifts are tracked and reported

- What happens if a ministry area overspends its available balance

The point isn't bureaucracy. The point is consistency.

A pastor should know whether a surprise repair can come from operations. A ministry leader should know whether designated gifts can support only that ministry. The treasurer should know whether the board expects a formal motion before changing a committed balance.

Avoid the most common mistakes

The most damaging errors are usually ordinary ones.

| Best practice | Common pitfall |

|---|---|

| Keep donor-restricted funds separate in reporting | Treat all cash in the bank as available |

| Review reserve levels regularly | Wait for a cash crunch before discussing policy |

| Record formal board actions clearly | Assume everyone remembers what was approved |

| Explain balances in plain language | Hand the board a report with no narrative |

Strong policy protects ministry because it reduces preventable confusion. It also gives donors quiet confidence that leadership takes stewardship seriously.

Enforce Accuracy with Grain Ledger's Fund Architecture

A common church finance scene looks like this. Sunday gifts are entered one way, the bank feed names them another way, and by month-end the treasurer is using a spreadsheet to remember which dollars belong to missions, benevolence, or the building fund. The books may still balance. The fund report is where the confusion shows up.

That is why fund architecture matters.

For a small or mid-sized church, GASB-style fund balance reporting is hard to apply if the accounting system treats funds like optional labels. You need the fund attached at the transaction level, the same way an envelope needs the right name before it goes into the mailbox. If the tagging happens later, leaders spend their time guessing intent instead of reviewing trustworthy reports.

A sound setup protects accuracy in three practical places:

- At gift entry: Donations post to the right fund as they are recorded

- At expense entry: Payments hit the proper fund without cleanup entries later

- At reporting time: The treasurer and board can see balances by fund and purpose without rebuilding the report in Excel

Grain is one example of software built for that structure in churches. Its ledger ties accounts, transactions, and reports to funds from the start, which helps a church apply accounting rules in a way that fits weekly ministry work. It also connects with tools many churches already use, including bank feeds, cards via Plaid, and giving platforms such as Planning Center, Pushpay, and Stripe.

That changes the treasurer's job in an important way. Instead of reconstructing what happened after the fact, the treasurer can review exceptions, confirm classifications, and explain the report in plain language to the board. Software cannot replace policy or judgment. It can make it much harder to mix funds, miss restrictions, or carry reporting mistakes from one month into the next.

For stewardship, that is the primary benefit. The system helps the church move from workarounds to records the board can trust.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Troubleshooting Common Fund Reporting Issues

The hardest reporting moments usually come after a ministry has already spent the money.

A common example is a building fund that paid invoices before enough designated cash arrived. Leaders may want the report to show a temporary negative restricted balance because “we know the pledges are coming.” That feels intuitive. It isn't transparent.

You can't hide a deficit inside a restricted category

Under GASB 54-style rules, if a fund's total balance is negative, the entire debit balance must be shown as unassigned fund balance, with other categories such as restricted or committed set to zero. That rule keeps deficits visible and prevents the appearance that restricted resources are still intact when they've been overspent, as explained in the Texas Comptroller's fund balance guidance.

That principle is useful for churches because it forces an honest conversation. If the church effectively advanced operating resources to cover a designated project, leadership should see that clearly.

Plain-language ways to explain it to the board

You don't need technical language to say it well.

Try statements like these:

- “The project spent more than the available restricted resources, so the shortfall has to show up in the residual balance.”

- “We're not saying donor intent disappeared. We're showing that the cash support for that restricted purpose was depleted.”

- “This presentation helps us face the cash flow issue directly instead of burying it in a designated line.”

The purpose of classification is to reveal pressure points, not soften them.

When a report surfaces a negative residual balance, treat it as a leadership signal. Ask what caused it, whether it was approved, and how the church will prevent a repeat. That's what sound stewardship looks like.

If your church is tired of explaining the same spreadsheet every month, Grain gives you a fund-based ledger built for church reporting, donor restrictions, and board-ready visibility. It's a practical way to move from patchwork tracking to clear fund balance reporting that matches how your church operates.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.