How to Read a General Ledger for Your Church

Learn how to read a general ledger with confidence. Our guide for church finance teams breaks down fund accounting, debits, credits, and reporting.

If you're serving as a church treasurer or sitting on a finance committee for the first time, the general ledger can feel like a report written for someone else. You open it and see account numbers, debits, credits, balances, and descriptions that don't seem to answer the question you care about. Did we use the mission trip money for the mission trip? Are we overspending in a ministry area? Can the board trust the report in front of them?

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

That's why learning how to read a general ledger matters in a church setting. The ledger isn't just an accounting file. It's the clearest record of how the church received, classified, and used the resources people entrusted to it.

In a church, every line carries a stewardship question. A designated gift isn't just income. It's a promise. A building fund balance isn't just a number. It's money set aside for a purpose leadership has to protect. Once you start reading the ledger that way, the report gets less intimidating and more useful.

Why Reading Your Church Ledger Matters

The finance committee meeting starts in ten minutes. Someone asks whether the church can approve a youth retreat deposit, and another person asks why the building fund looks lower than expected. The answer is not on the summary page alone. You need the ledger.

That is why reading the general ledger matters in a church. It gives you the transaction-level record behind the budget report, the balance sheet, and the ministry updates leaders rely on. If the ledger is coded well, you can verify whether designated giving stayed with its purpose, whether expenses were posted to the right ministry, and whether the report in front of the board reflects what happened.

Church accounting carries a different burden than business bookkeeping. The question is not only whether money came in and went out. The question is whether the church honored donor intent, kept restricted and unrestricted resources distinct, and reported ministry activity in a way leaders can explain with confidence. That is the daily work of stewardship.

A clear ledger supports that work because it groups transactions into accounts instead of leaving them as a long list of dates and amounts. The National Council of Nonprofits explains that nonprofits need accounting records that support internal reporting, grant and donor restrictions, and board oversight, which is exactly why churches need a ledger structure built for fund visibility rather than one generic operating view (National Council of Nonprofits guidance on financial management).

If your church is still cleaning up account structure, a stronger chart of accounts for a nonprofit organization makes the ledger far easier to read and far more useful to leadership.

What a church volunteer is really trying to confirm

A new finance committee volunteer usually needs answers to a short list of practical questions:

- Did restricted gifts stay protected? Benevolence, missions, camp scholarships, and building gifts should remain tied to those purposes.

- Was the expense posted to the right ministry? A retreat deposit in general administration can make a ministry report look wrong even if cash was spent correctly.

- Can leadership follow the explanation? If cash is tight or a ministry is overspending, the ledger should show why.

- Do the reports match ministry reality? The accounting should reflect how the church operates, not just how the software happened to be set up years ago.

Confidence grows from that kind of clarity.

When you can read the ledger, month-end reports stop feeling like a black box. You can trace a number back to the entry that created it, spot coding mistakes before they reach the board packet, and ask better questions about fund balances, reimbursements, and transfers. In church finance, that kind of clarity protects trust, and trust is hard to rebuild once people start wondering whether designated money was handled correctly.

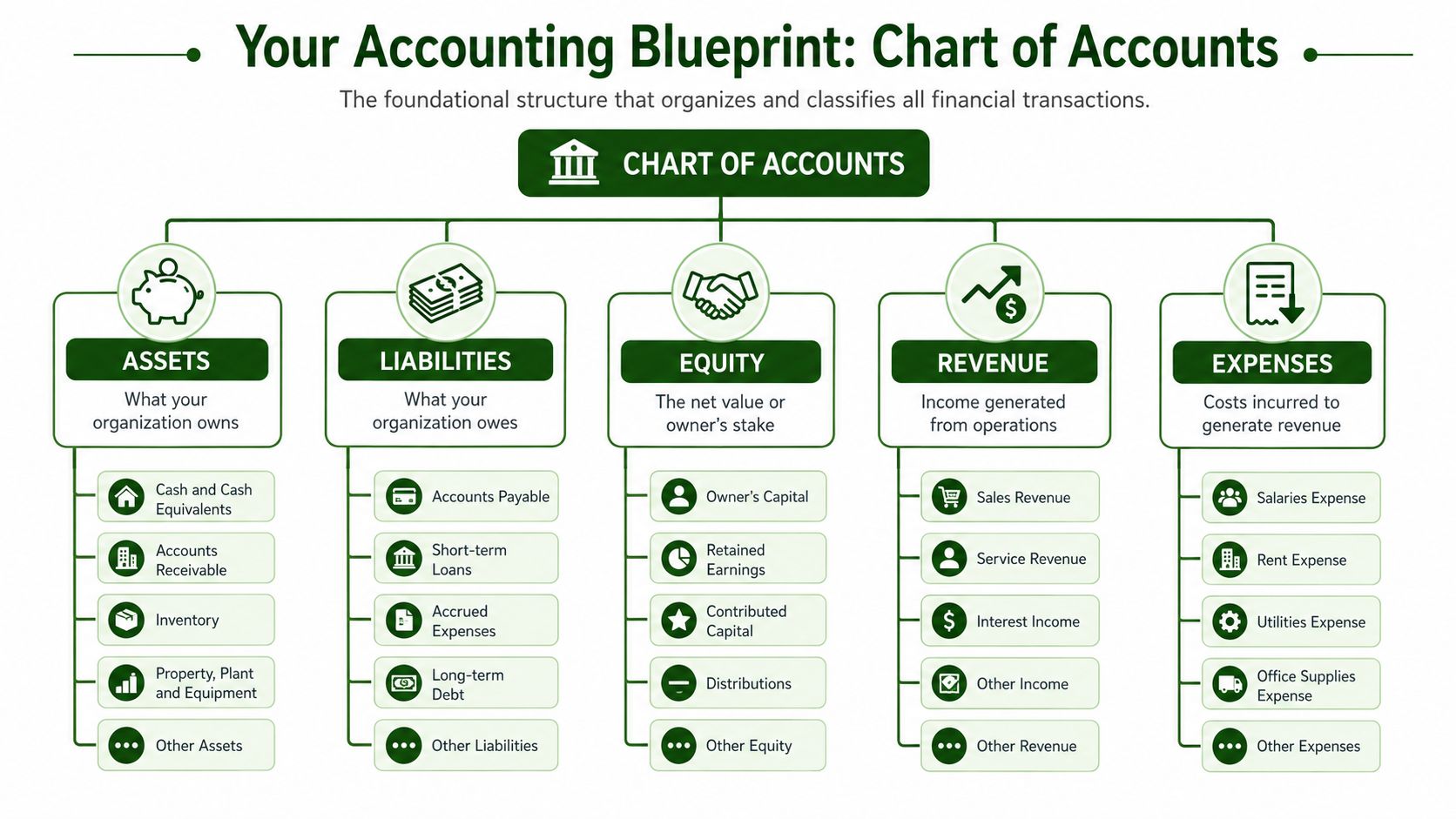

Start with the Blueprint Your Chart of Accounts

A common approach is to try reading transactions first. That's backwards. You should start with the chart of accounts, because the chart is the blueprint that tells you how the ledger is organized.

A general ledger is only useful if the chart of accounts cleanly groups assets, liabilities, equity, revenue, and expenses. That is especially important in a church, where a standard setup can hide restricted and unrestricted activity unless the structure was built for fund visibility from the start (Microsoft Business Central general ledger documentation).

Read the structure before the detail

If you don't know what an account is supposed to represent, you can't judge whether the activity in it makes sense.

At minimum, look for these categories:

- Assets: Cash, receivables, prepaid items, and anything the church owns or controls.

- Liabilities: Amounts the church owes, such as payables, loans, or other obligations.

- Equity or net assets: The residual balances that reflect the church's financial position.

- Revenue: Giving and other inflows.

- Expenses: Ministry, administration, facilities, payroll, and other outflows.

In some systems, the numbering helps you read quickly. As noted earlier, one commonly used structure starts revenue accounts with 4 and expenses with 5. The exact numbering may differ in your church, but the principle is the same. The number and name together should tell you what kind of account you're reading.

What works in a church and what doesn't

A generic small-business chart of accounts often creates trouble for churches. It may have a single donations account, a broad supplies expense account, and almost no way to distinguish funds. That setup might balance mathematically, but it doesn't answer ministry questions.

A church-friendly chart of accounts should let you separate things like:

| Area | Weak setup | Better church setup |

|---|---|---|

| Giving | One donations account | Distinct revenue tracking tied to ministry purpose |

| Expenses | Broad program expense buckets | Ministry-specific expense accounts |

| Funds | No clear fund distinction | Restricted and unrestricted activity visible by fund |

| Reporting | Hard to explain to the board | Easy to map into ministry reports |

A practical next step is to compare your current setup with a church-friendly chart of account for nonprofit organization examples. Even if your church doesn't change software right away, studying a better structure helps you read your own ledger more intelligently.

Practical rule: If you can't tell whether a balance belongs to general operations, missions, benevolence, or a building campaign without opening several reports, the chart of accounts is doing too little work.

Questions to ask about your current chart

Before reviewing individual entries, ask:

- Can we distinguish unrestricted from restricted activity quickly?

- Do account names match how our ministries operate?

- Are too many unrelated transactions being pushed into catch-all accounts?

- Can a finance committee member read this without inside knowledge from the bookkeeper?

If the answer is no, reading the ledger will stay harder than it should be. Clean structure doesn't remove the need for review, but it makes meaningful review possible.

Tracing the Flow of Ministry Funds

A finance committee member asks a fair question after the monthly meeting. "That special offering for the youth mission trip came in two months ago. How do we know it was used for the trip and not absorbed into regular spending?" The ledger should let you answer that in minutes, not after a string of follow-up emails.

The most useful way to read a church ledger is to trace one gift from receipt to use. That approach matters more in church finance than in a typical business because you are not only checking whether money came in and went out. You are also checking whether donor intent, fund restrictions, and ministry reporting stayed aligned all the way through.

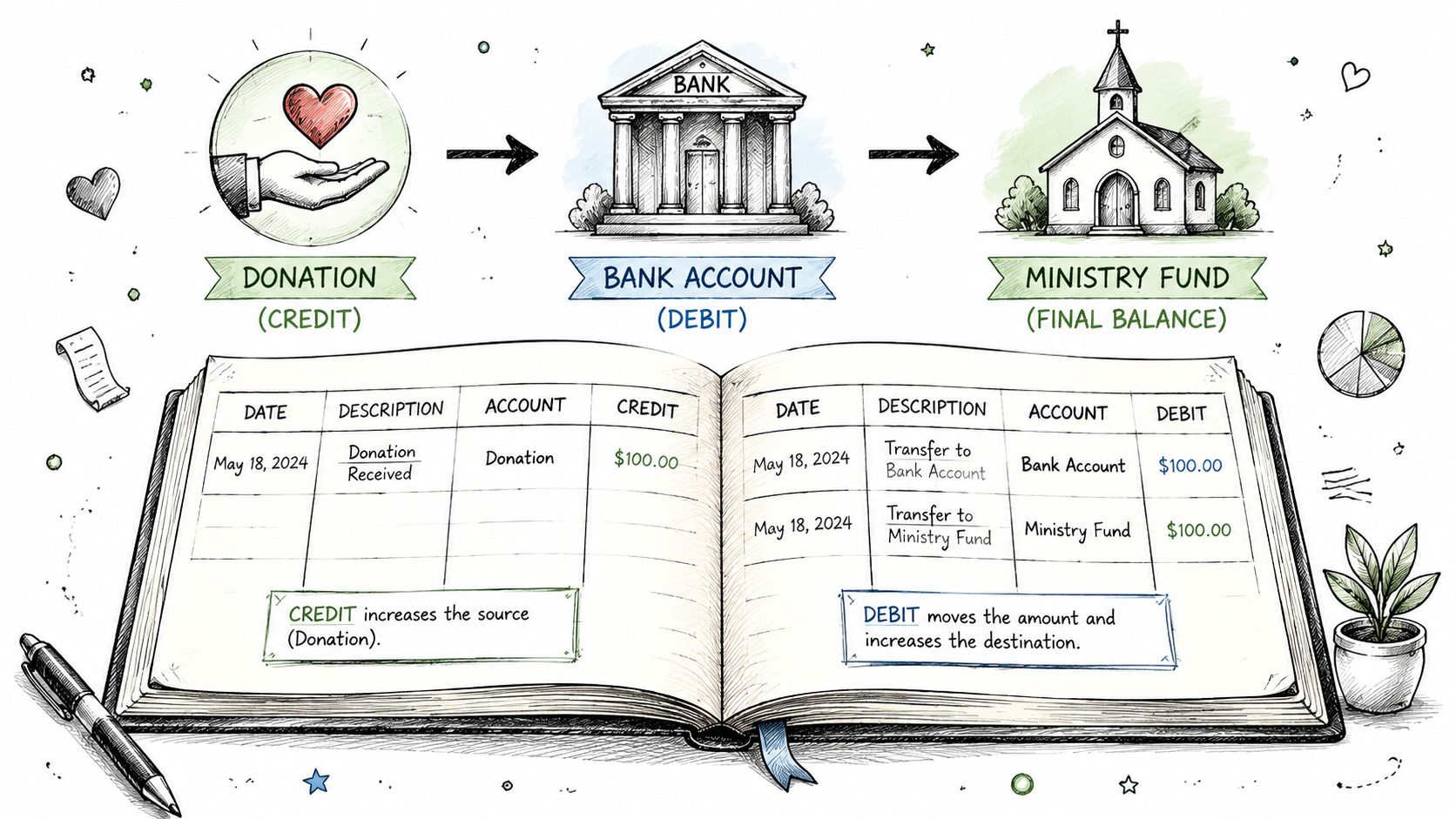

Follow one gift all the way through

Suppose a member gives to the youth mission trip. The receipt should increase cash and record the gift in the revenue account and fund that match that purpose. If the gift was restricted, the ledger should make that restriction visible without forcing you to piece the story together from several places.

Later, the church pays for airfare, registration, or lodging for that trip. The expense should hit the mission trip expense account and the same ministry fund that received the gift. If the expense lands in a general program account or in the wrong fund, the church may still have paid a real bill, but the ledger will no longer give leadership a clean answer about what remains available for that trip.

That is the trade-off. Broad posting can feel faster in the moment. Precise posting saves time during budget review, donor questions, audit work, and board reporting.

What to check on each ledger line

Read the detail line by line, in order:

- Date: Does the transaction belong in this month, or was it posted late or early?

- Fund or class: Is the activity sitting in general operations, benevolence, missions, building, or another designated fund?

- Account number and account name: Does the account reflect what happened?

- Description: Would someone outside the bookkeeping process understand the purpose from this note?

- Debit and credit columns: Do the entries match the expected effect on cash, revenue, expense, liability, or fund balance?

- Running balance: After this entry, does the balance still look plausible for that ministry or fund?

For churches that process online giving, timing deserves extra attention. A gift may be received from the donor on one date, settled by the processor on another date, and posted by staff on a third. If your church handles card payments or digital transfers, this primer on revenue recognition for Stripe users is a helpful reference for thinking through when revenue should be recorded and how payment flow can affect ledger review.

A short walkthrough helps make this visual:

Why fund-aware reading matters in a church ledger

Church leaders rarely ask only, "Was this posted?" They ask, "Was this posted to the right ministry, in the right fund, for the right purpose?" That is a stewardship question.

A benevolence gift should stay identifiable as benevolence activity. A building campaign balance should remain separate from operating cash. Transfers between funds need special care because they often create confusion. Money may move for a valid reason, but the ledger should show the reason clearly, along with approval and support. Churches that need to track those movements more clearly should understand fund to fund accounting in church finance.

A healthy ledger lets you answer three questions without guessing:

- Where did this money come from?

- What fund does it belong to now?

- What happened to it after that?

If those answers are hard to find, the problem usually sits in the posting process, the fund structure, or both.

Connecting the Ledger to Leadership Reports

Finance committees and elder boards usually don't want to read ledger detail line by line. They want summary reports they can discuss and act on. That doesn't make the ledger less important. It makes it more important, because every summary report depends on the ledger being right.

The general ledger is the system of record used to prepare the income statement, balance sheet, and cash flow statement, and the double-entry structure behind it produces the balanced trial balance that supports those reports on a monthly, quarterly, or annual basis (HighRadius overview of the general ledger).

How the summary reports get their numbers

The balance in each account flows into a report category. Cash and other asset accounts help build the balance sheet. Revenue and expense accounts feed the statement that shows operating activity. Fund-related balances help leadership see what resources are available and whether restrictions are being honored.

For a church, this matters because board members often ask questions at the summary level:

- Are we within budget?

- Do we have cash available for a ministry initiative?

- How much remains in the building or missions fund?

- Are current giving patterns supporting current spending?

Those answers come from reports, but the support for those answers sits in the ledger.

What leaders need from you

A good treasurer doesn't read every line aloud. A good treasurer translates.

If the youth mission trip fund still has a positive balance, you should be able to explain why. If facility expenses ran above budget, you should be able to point to the accounts and period activity behind that variance. If a report looks confusing, the ledger gives you the supporting detail needed to simplify the conversation.

Leadership reports are summaries. The ledger is the proof behind the summary.

That is also why report design matters. A church shouldn't be stuck choosing between a highly technical export and an oversimplified summary that hides restricted activity. Reviewing examples of church financial reports that leaders can actually use can help you think about how ledger detail should roll up into something understandable for pastors and boards.

A useful habit for board prep

Before a finance meeting, review your reports with these comparisons in mind:

| Question from leadership | Ledger-based check |

|---|---|

| Why did this balance change | Review the account activity for the period |

| Is this fund protected | Confirm the ending balance and related postings |

| Are we overspending | Compare expense activity to the budget and prior period |

| Can we trust this report | Tie unusual balances back to supporting entries |

That approach keeps your role from becoming reactive. Instead of saying, "I'll have to look into that," you'll often already know where the number came from and whether it reflects a real ministry event, a timing issue, or a posting mistake.

Finding and Fixing Common Ledger Errors

Even a balanced set of books can still contain bad classifications, wrong-period postings, or unsupported entries. That's why ledger review isn't just about checking whether debits equal credits. It's about testing whether the numbers make sense.

One of the most practical workflows is to trace a balance through a simple control chain: source document → journal entry → posting → reconciliation. The journal entry should show the date, accounts, debit and credit amounts, and a clear description. If something looks off in the ledger, don't stop at the account total. Go backward to the journal and then to the underlying support such as bank statements, payables detail, loan records, or fixed-asset support (Numeric guidance on posting and reconciliation).

Start with the bank reconciliation

If cash is wrong, many other numbers will be wrong too. That's why I tell new volunteers to begin with the bank reconciliation before chasing every unusual expense line.

A good reconciliation helps you confirm:

- All bank activity was recorded: Deposits and withdrawals on the statement appear in the books.

- Timing differences are understood: Outstanding checks or deposits in transit are identified, not guessed.

- No duplicate or missing postings slipped in: The ledger and bank activity can be matched cleanly.

- Cash-related adjustments are documented: Fees, corrections, or transfers aren't posted without support.

If the reconciliation is weak, the rest of the review will waste time.

Use simple error patterns

When the trial balance difference points to an error, a few patterns can help you narrow the search. Troubleshooting guidance notes that if the debit-credit difference is divisible by nine, a transposition error is likely. If the difference divided by two yields a number that appears on the trial balance, the issue may be a debit/credit reversal (Wolters Kluwer guidance on maintaining a general ledger).

| Pattern you see | What it often suggests |

|---|---|

| Difference divisible by 9 | Digits may have been transposed |

| Difference divided by 2 matches a trial balance number | Debit and credit may have been reversed |

| Odd negative balance in an account that shouldn't go negative | Classification or posting issue |

| Old balance sitting in a temporary account | Entry wasn't cleared or reconciled properly |

Don't assume a balanced trial balance means the books are correct. It only proves arithmetical equality, not proper classification or period accuracy.

Where church books commonly go wrong

Church ledgers often develop problems in ordinary places:

Restricted gifts posted to general revenue

The books still balance, but the church loses visibility over donor intent.Expenses coded too broadly

Ministry leaders can't tell what a program cost because too much landed in miscellaneous accounts.Transfers recorded unclearly

Money moved between bank accounts or funds without a description that explains why.Late entries posted into the wrong period

The board reviews one month while the ledger reflects another.

If your books have gotten messy over time, outside cleanup can be a reasonable step. A service such as cleanup bookkeeping services can be useful when prior postings need to be untangled before the church can trust current reports again.

Controls matter as much as math

Strong review also depends on who does the work. Preparation, approval, and posting should not all sit with the same person for sensitive areas like cash or revenue. In a small church that may be hard to separate perfectly, but even a modest review step by a second person reduces the chance that unsupported entries stay hidden.

A sound habit is to scan for anomalies before close. Negative revenue balances. Accounts that should be zero but aren't. Descriptions that don't explain the transaction. Those are often the fastest clues.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Streamline Your Stewardship with True Fund Accounting

Manual skill still matters. Every treasurer should know how to read the ledger, question a balance, and trace an entry to support. But manual skill alone won't fix a system that was never designed for church finance.

Modern cloud systems have changed what churches can do with ledger data. They can give better visibility into balances, support stronger review, and help automate the detection of missing support, posting errors, and period-end misclassifications before those issues reach leadership reports (Block Advisors on the general ledger and modern systems).

Why generic tools create friction

Spreadsheets and standard small-business software can record transactions. That doesn't mean they handle church stewardship well.

The pain usually shows up in familiar places:

- Restricted funds require workarounds: Staff and volunteers create side spreadsheets because the ledger itself doesn't preserve fund visibility cleanly.

- Reports need manual interpretation: The pastor gets a packet full of numbers that still requires explanation every month.

- Integrations create cleanup: Giving data, bank activity, and accounting entries don't line up neatly.

- Audit trails get thin: It's harder to show how a designated dollar moved from receipt to use.

For readers who want a broader primer on the nonprofit side of this issue, understanding charity fund accounting is a helpful companion topic because it explains why purpose-based accounting matters so much when donations carry expectations.

What a purpose-built church system should do

A church accounting system should organize transactions around funds from the beginning, not bolt fund tracking on afterward. It should let you drill from reports into supporting detail, preserve restricted balances clearly, and make monthly reporting easier for both bookkeepers and church leaders.

When churches are evaluating solutions, Grain is worth considering because it is built for church fund accounting. Its setup centers accounting around funds, transactions, and reports in a way that fits how churches handle designated giving, ministry activity, and board reporting.

The goal isn't prettier accounting. The goal is faithful stewardship that leaders can explain and members can trust.

Learning how to read a general ledger will always matter. But the healthiest process combines that skill with a system that makes the right reading easier.

If your church wants fund-based reporting that reflects ministry reality, take a look at Grain. It's built to help churches track restricted and unrestricted activity clearly, connect giving and banking workflows, and make financial reporting easier for treasurers, staff, and boards.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.