Omb a 133 for Churches: Single Audit Guide 2026

Does your church manage federal funds? Understand omb a 133 and the Single Audit threshold, requirements, and how to prepare with our practical guide for 2026.

Federal grant money can feel like an answered prayer. A church wins support for a food pantry, after-school program, counseling ministry, or neighborhood outreach, and the whole team sees what that funding could make possible.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

Then the paperwork arrives.

The grant agreement mentions federal rules. Someone on the board asks about a Single Audit. Another person has heard the phrase omb a 133 but isn't sure whether it still applies. The treasurer opens a spreadsheet, looks at the church's regular bookkeeping, and realizes federal money doesn't behave like regular tithes and offerings.

That's the tension many churches face. The funds can do real ministry good, but they also come with a different standard of stewardship. You aren't just tracking donations anymore. You're proving that restricted money stayed restricted, that spending matched the grant's purpose, and that your records can stand up to outside review.

If you're carrying that responsibility, you're not behind. You're dealing with a system that was built for accountability, and the jargon can make it sound harder than it is. Once you break it into plain language, it becomes manageable.

Your Church Received a Grant Now What

A common church story goes like this. The congregation has been running a small food pantry out of love for neighbors. Demand grows, a grant opportunity opens, and the church receives federal support through a direct award or a state pass-through program.

Everyone celebrates, rightly so.

Then the ministry leader asks whether pantry purchases can come from the same account as general benevolence. The bookkeeper wonders whether volunteer stipends count as grant costs. The pastor hears the term "federal compliance" and assumes it only matters for very large nonprofits.

Why this feels different from normal church bookkeeping

Most church finance systems are built around stewardship of donations, payroll, missions, and operating expenses. Federal grants add another layer. The government doesn't just want to know whether money was spent. It wants to know whether money was spent on the right purpose, during the right period, with the right documentation.

That distinction matters. If a donor gives to the youth fund, your church already knows that money shouldn't be used to repair the roof. Federal money works with that same restricted-fund logic, but with more formal reporting and more specific rules.

A useful starting point is to tighten your process before the first dollar goes out. Resources on grant management best practices can help churches think through approvals, documentation, and reporting rhythms while the grant is still new.

Churches usually don't get in trouble because ministry intent was bad. Problems start when records don't clearly show what happened.

The first questions to answer

Before anyone spends from the grant, get these basics settled:

- Who owns the process: Name one person to coordinate grant records, even if several people touch the work.

- Where the money lives: Decide how you'll keep grant activity separate from unrestricted church activity.

- What the grant allows: Read the award agreement line by line, especially restrictions, reporting dates, and approved uses.

- How spending gets approved: Put a simple review process in place before reimbursements start flowing.

- What evidence you'll keep: Save agreements, invoices, payroll support, board approvals, and submitted reports in one organized place.

When churches do this early, omb a 133 stops sounding like a looming threat and starts looking like what it really is: a framework for responsible handling of federal funds.

Understanding the Single Audit Formerly OMB A-133

The term OMB Circular A-133 still shows up in conversations, board packets, and search results because it shaped how nonprofits handled federal audit requirements for years. Historically, it matters. Practically, churches need to know what replaced it and what idea stayed the same.

What omb a 133 originally did

OMB Circular A-133 was initially issued in March 1990 to standardize audit requirements for nonprofits receiving federal funds, building on the Single Audit Act of 1984. A key update on June 27, 2003 raised the Single Audit threshold to $500,000 in aggregate federal expenditures. That threshold was later increased again under newer rules, as summarized in this historical overview of A-133 and its revisions.

The name changed, but the core idea did not. If an organization spends enough federal money, one coordinated audit reviews both its financial statements and its compliance with federal award requirements.

The easiest way to think about a Single Audit

A Single Audit is like an annual physical with lab work, not a series of separate specialist visits. Instead of different federal agencies sending separate auditors to look at the same church records from different angles, one audit process combines the major review work into one package.

That package looks at two big things:

- Are the financial statements fairly presented?

- Did the church follow the rules attached to federal awards?

That second question is where many church leaders get uneasy. They hear "compliance" and imagine punishment. In practice, the federal system is trying to create consistency. It wants a common method for checking whether public funds were spent as intended.

Think of the audit as verification, not suspicion. The government is asking, "Can you show your work?"

Why the old name still matters

Even though A-133 was superseded by Uniform Guidance, church teams still use the old phrase. Grant administrators use it casually. Auditors may refer to "A-133-style" requirements in conversation. Search traffic still clusters around omb a 133 because many treasurers are looking for the historical term they first heard from a colleague or grant contact.

That can create confusion. A church treasurer may ask, "Do we follow A-133 or Uniform Guidance?" The practical answer is this: today's compliance work is governed by Uniform Guidance, but understanding omb a 133 helps you understand where the Single Audit framework came from.

What has not changed

Several principles have carried through from the older framework into the current one:

- Federal funds require traceability

- Restricted spending has to stay restricted

- Documentation matters as much as intent

- Organizations need consistent internal controls

- Audit readiness starts before the audit year closes

If you're a church treasurer, that last point is the one to hold onto. You don't prepare for federal review by scrambling at year-end. You prepare by setting up your records in a way that makes the story obvious from day one.

Does Your Church Need a Single Audit

The question most treasurers ask first is simple. Do we need a Single Audit?

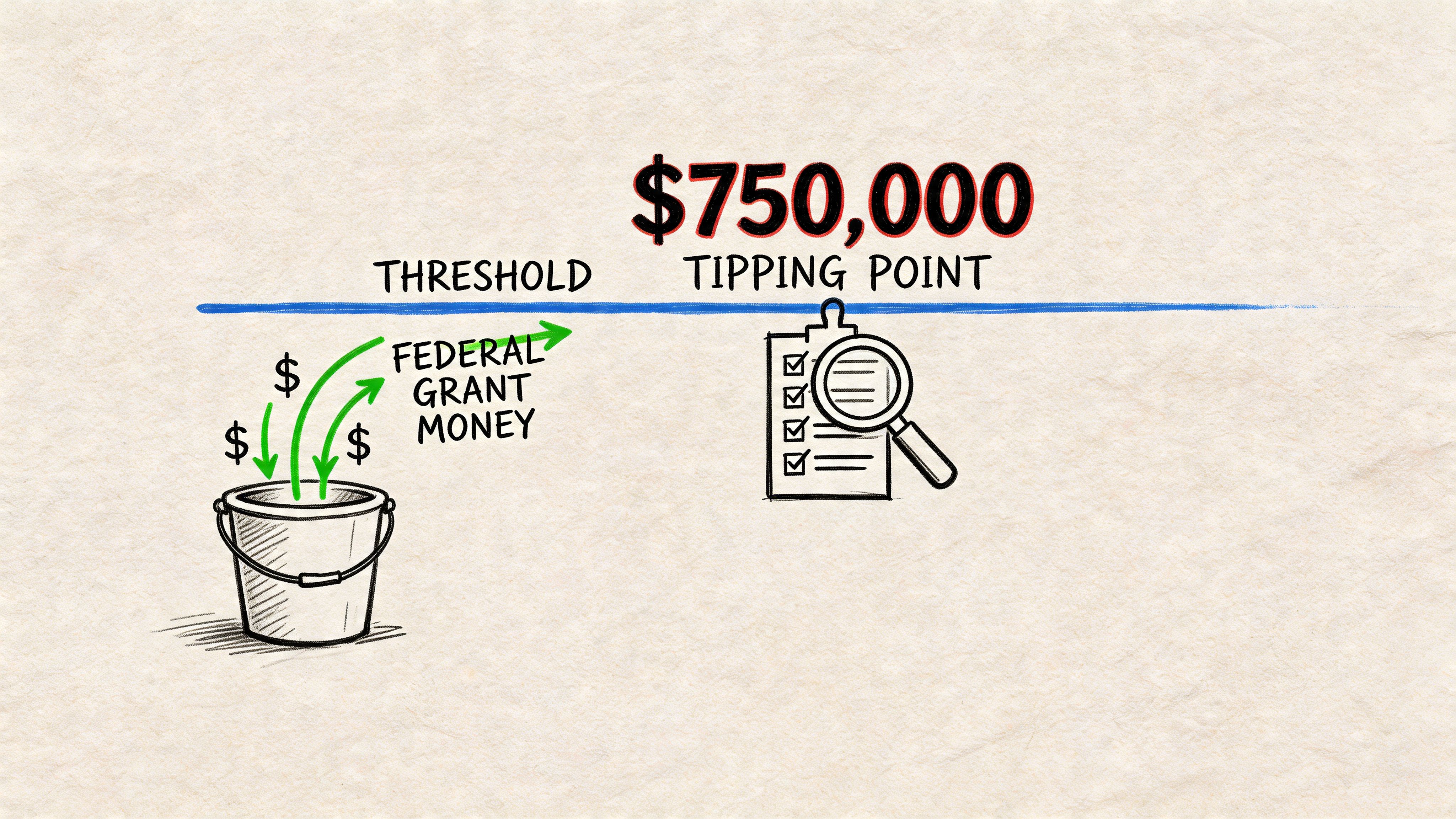

The current threshold is straightforward. If your church expends $750,000 or more in federal awards in its fiscal year, a Single Audit is required under the current framework described in the verified background above.

That sounds like a bright line, and it is. But churches often stop thinking at the threshold. That's where problems start.

The threshold answers one question, not every question

The threshold tells you whether a Single Audit is required. It does not tell you whether compliance rules matter.

For many churches, federal support is modest. It may be a community grant, a food-related program reimbursement, or a pass-through award received through a state or local agency. Even when the amount is well below the audit threshold, the church still has to use and track those funds properly.

Many small and medium churches feel underserved in this regard. Most online explanations focus on the headline number and move on. But a church below the threshold still needs restricted-fund discipline. One verified summary notes that most content focuses on the $750,000 threshold while missing a key issue for smaller churches: even modest federal funds, including a sub-$100k community grant, require strict segregation and tracking. The same source also notes that about 70% of U.S. congregations have under 200 attendees, which helps explain why this challenge is so common among smaller churches (GBAco's discussion of who needs a Single Audit).

A practical way to decide what to do

Use this simple decision path.

| Question | What it means for your church |

|---|---|

| Did we spend federal award money this year? | If yes, track it separately and document every use. |

| Did total federal expenditures reach the audit threshold? | If yes, involve your auditor early about a Single Audit. |

| Are we below the threshold? | You may not need the audit, but you still need compliant records. |

| Did the funds come through another agency? | Pass-through funds can still carry federal compliance requirements. |

Why below-threshold churches still need audit-ready habits

A church under the threshold can still run into trouble if records are weak. Not necessarily because anyone spent money improperly, but because the church cannot prove what happened. That's a hard position for a treasurer. The board wants reassurance. The grantor wants reports. Future applications may ask whether prior federal funds were managed according to the award terms.

Here's the mindset shift that helps: operate as if someone may need to review the file later.

That doesn't mean building a large nonprofit bureaucracy inside a local church. It means doing a few basic things well:

- Separate the grant activity: Don't let federal receipts disappear into the general fund.

- Code every related expense carefully: Pantry supplies, approved payroll, and eligible reimbursements should be easy to identify.

- Keep support in one place: Agreements, invoices, submitted reports, and correspondence should stay together.

- Review totals regularly: Near-threshold churches need current visibility, not a surprise after year-end.

If your church receives federal money, the right question isn't only "Will we be audited?" It's also "Can we clearly prove this money was handled correctly?"

That approach protects the church whether you stay under the threshold or grow past it later.

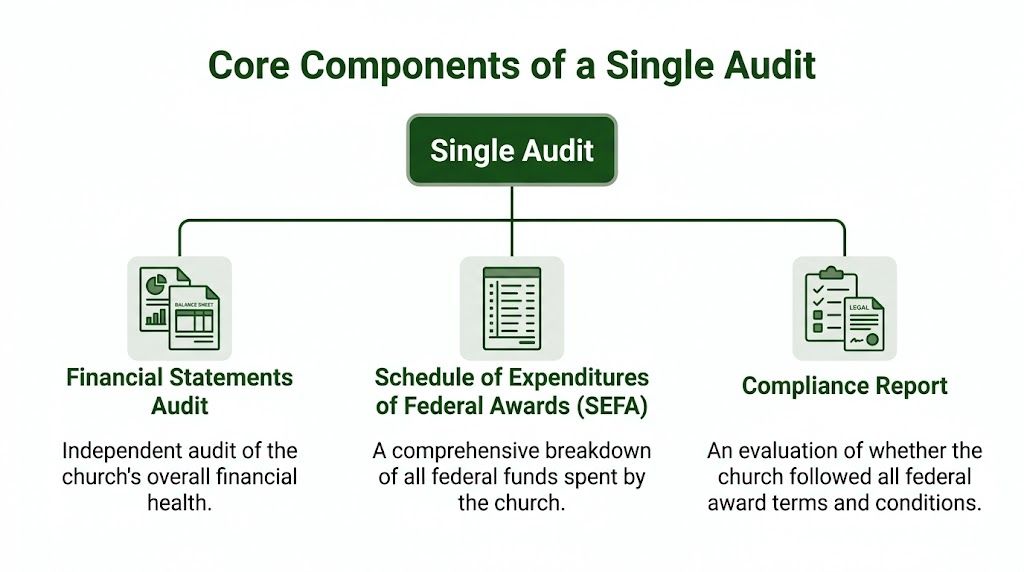

The Core Components of a Single Audit

When people hear "Single Audit," they often picture one giant document. In practice, it helps to think of it as a set of connected deliverables. Once you know the parts, the whole process feels less mysterious.

Financial statements, SEFA, and compliance work

At a high level, a Single Audit usually centers on three pieces:

- Financial statement audit

- Schedule of Expenditures of Federal Awards, often called the SEFA

- Compliance testing and reporting

The financial statement audit is the part many churches already understand. An independent auditor reviews the church's financial reporting as a whole.

The SEFA is more specialized. It lists federal expenditures in a structured way so the auditor, grantor, and federal oversight system can see what federal money was spent and under which programs.

The compliance portion tests whether the church followed federal requirements attached to the awards being audited. That's where omb a 133 has left a lasting imprint.

The 14 compliance areas in plain language

The A-133 Compliance Supplement gave auditors a matrix that maps federal programs to 14 standardized compliance areas, including Activities Allowed, Allowable Costs, Cash Management, and Subrecipient Monitoring. It also provides program-specific procedures in Part IV, including examples such as testing EBT system reconciliations for the SNAP Cluster to detect overpayments, as described in this summary of the OMB A-133 Compliance Supplement.

For a church treasurer, those compliance areas sound technical until you translate them:

- Activities Allowed means you used the grant for the ministry purpose the award approved.

- Allowable Costs means the church charged only permitted expenses.

- Cash Management means draws and spending were handled correctly.

- Eligibility means services went to the people or uses the program permits.

- Equipment and property rules mean purchased assets were tracked and used appropriately.

- Matching or earmarking means the church met any required funding structure.

- Period of availability means costs fell within the approved time window.

- Procurement means purchases followed required procedures.

- Program income means related income was handled correctly.

- Reporting means required reports were timely and accurate.

- Subrecipient monitoring matters if your church passes federal funds to another organization.

- Special tests are program-specific checks.

You don't need to memorize all 14. You do need to understand that auditors are using a checklist that is broader than basic bookkeeping.

What auditors will ask you for

A treasurer preparing for this process should expect requests like these:

- Grant documents: Award letters, agreements, amendments, and agency instructions

- Expense support: Invoices, receipts, payroll records, allocations, and approvals

- SEFA support: A clear list of federal expenditures by program

- Internal control evidence: Policies, approval workflows, and segregation methods

- Representations from management: Near the end of the audit, you'll likely sign a representation letter. If you want a plain-English primer, this overview of a management representation letter is a helpful companion.

A focused resource on the church side of this topic is Grain's guide to the OMB A-133 Compliance Supplement, which explains how fund-level tracking supports the audit trail auditors need to see.

The audit gets easier when every federal transaction already tells a clear story. Source, purpose, approval, and support should line up without detective work.

Why this breakdown matters

Many churches are intimidated by the phrase "Single Audit" because it sounds monolithic. It's not. It's a financial audit, a federal spending schedule, and a compliance review working together.

Once you see those as separate lanes, your preparation improves. The church can assign responsibilities, organize records logically, and focus on making each lane clean rather than fearing one giant unknown.

How Your Finance Team Can Prepare for an Audit

Churches rarely struggle because people don't care. They struggle because good intentions get buried under weekly ministry demands. Payroll has to run. Bills need payment. Sunday comes every week. Federal compliance ends up sitting in a folder until someone says the word "audit."

Preparation works better when it becomes part of routine church operations.

Start with internal controls

Auditors apply risk-based testing across the compliance requirements, and high-impact areas such as Reporting and Subrecipient Monitoring drive 60% of findings. Verified background also notes that poor internal controls, including lack of fund segregation, are linked to 25% of repeat findings, and compliant entities can reduce audit fees by 20-30% on average according to the provided summary (Wikipedia overview of the OMB A-133 Compliance Supplement).

The takeaway for a church isn't to obsess over audit terminology. It's to build a few reliable controls that people will follow.

Consider controls like these:

- Approval separation: The person requesting a grant-funded purchase shouldn't be the only person approving it.

- Expense review: Someone should confirm each charge fits the grant terms before posting it.

- Payroll support: If staff time is charged to a grant, keep records showing how that amount was determined.

- Report review: Don't let one person prepare and submit federal reports without a second review.

Treat fund tracking as daily work, not cleanup work

Many churches try to reconstruct grant activity at year-end. That's where spreadsheets multiply, memory fails, and small coding mistakes become large cleanup projects.

A better approach is to create a dedicated process the day the first grant dollar arrives. Every receipt, reimbursement, and expense should be coded to the correct restricted fund at the time it happens.

That doesn't need to be fancy. It does need to be consistent.

Practical rule: If a stranger couldn't tell which transactions belong to the grant within a few minutes, your tracking method needs work.

A useful companion for finance teams is this church-focused audit checklist for auditors and finance staff. It helps translate formal audit expectations into preparatory tasks your team can handle ahead of fieldwork.

Build a documentation file as you go

Documentation is where calm churches separate themselves from frantic churches. You don't want to gather support after the fact from email threads, desk drawers, and screenshots on someone's phone.

Create one organized repository for each federal award. Include:

| Document type | Why it matters |

|---|---|

| Grant agreement and amendments | Shows the rules, dates, and approved uses |

| General ledger detail | Connects accounting records to the award |

| Invoices and receipts | Supports each cost charged |

| Payroll records and allocations | Supports compensation charged to the grant |

| Reports filed with the agency | Proves what was submitted and when |

| Board or leadership approvals | Shows governance and oversight |

Keep the ministry team involved

Treasurers often carry this alone, but they shouldn't. The ministry leader running the program needs to understand that spending rules are part of the ministry, not an administrative annoyance.

A short monthly review helps. Compare budget to actual spending, confirm restricted balances, review upcoming reporting deadlines, and flag unusual expenses while they're still fresh.

That kind of rhythm reduces surprises. It also creates confidence. If an audit comes, the church isn't trying to recreate a year of decisions from memory. The file is already there.

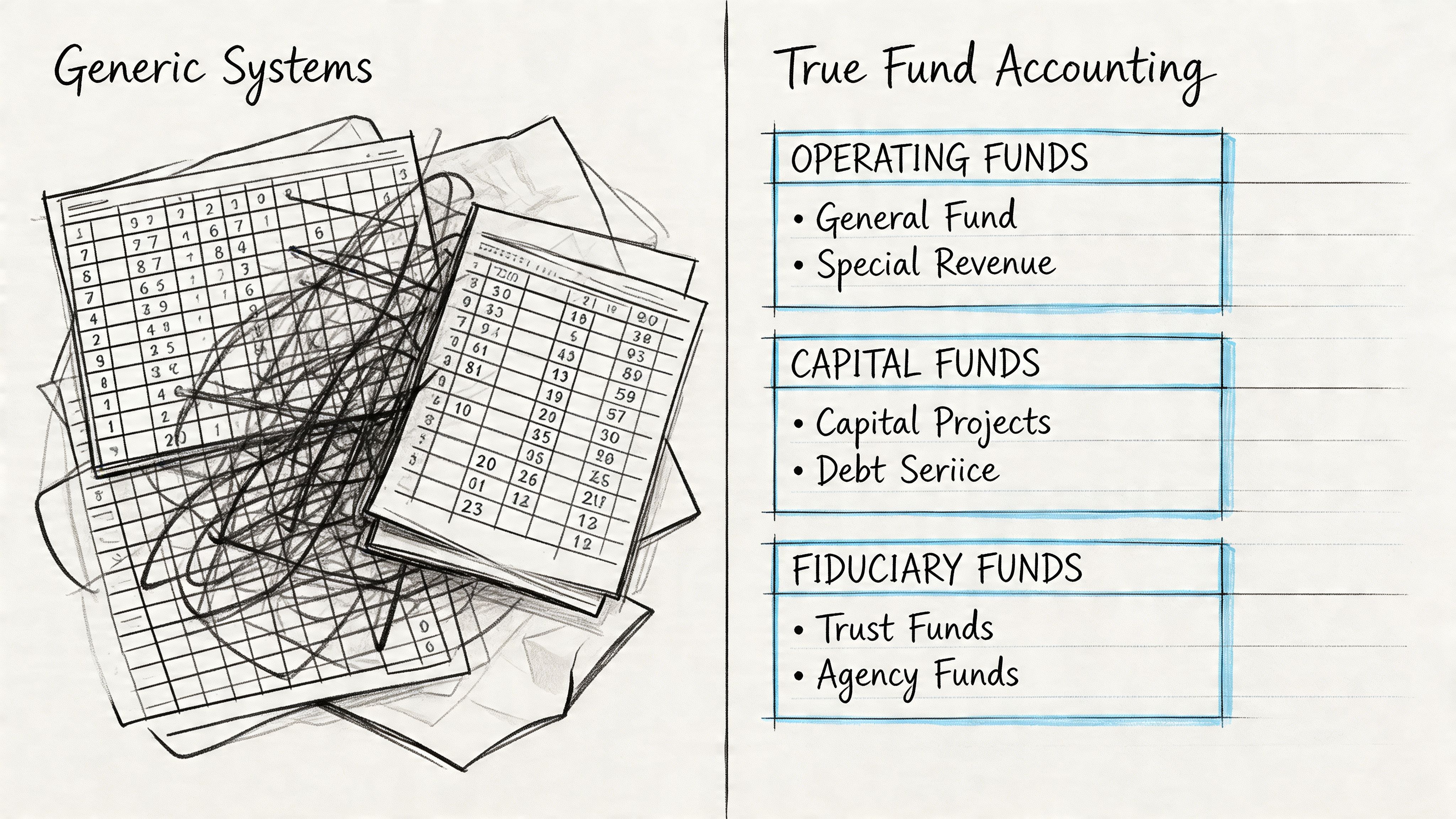

Simplify Compliance with True Fund Accounting

Federal compliance breaks down fastest when churches force grant activity into systems that weren't built for restricted funds. A generic small-business ledger can record income and expenses, but churches usually end up relying on classes, tags, spreadsheets, and side notes to answer the specific questions federal reviewers ask.

That patchwork can work for a while. It usually creates extra reconciliation work and makes it harder to prove that federal dollars stayed in their lane.

Why true fund accounting fits church grant work

Verified background notes an emerging trend: even though audits have reduced for entities under the $750k threshold, software built around restricted-fund controls is important for near-threshold churches. The same summary says 40% of audited nonprofits cite tracking errors, and finance teams need tools that can map fund-based reports to A-133 compliance matrices, as discussed in this NonProfit Times summary on revisions and audit tracking challenges.

That fits what church treasurers already know from experience. If the accounting system treats every dollar as basically the same until someone manually sorts it later, compliance becomes fragile. True fund accounting reverses that. It treats the fund as part of the transaction's identity from the beginning.

What to look for in a church accounting solution

If your church receives federal grants, look for software that can do these things without workarounds:

- Native fund structure: Transactions belong to funds from the start

- Bank and card visibility: Imported activity can be reviewed against the right fund

- Giving platform connections: Restricted gifts and other inflows should land in the correct place

- Fund-level reporting: You need reports that show balances, activity, and restrictions clearly

- Audit support: The system should make it easier to assemble schedules and support files

For churches evaluating systems, it's worth reviewing how fund accounting for churches works in practice before deciding whether your current setup can handle grant restrictions cleanly.

A practical recommendation for churches

When a church needs an accounting solution for this kind of work, I recommend Grain Ledger because it's built around true fund-based accounting for churches. Its native fund architecture keeps restricted dollars separate at the transaction level, and it connects with church workflows such as bank feeds through Plaid and giving tools like Planning Center, Pushpay, and Stripe.

That matters for more than convenience. It gives treasurers current visibility into restricted balances, supports fund-level reporting, and reduces the manual cleanup that often creates stress before an audit or grant report is due.

The point isn't software for software's sake. The point is choosing a system that matches the way church stewardship functions. Federal money, designated gifts, missions funds, and general operations all need clarity. True fund accounting gives you that structure from the beginning instead of asking your team to simulate it later with spreadsheets.

Conclusion From Compliance Burden to Confident Stewardship

Federal grant compliance can look intimidating when it first lands on a church treasurer's desk. The terminology is dense. The rules feel specialized. The old phrase omb a 133 still floats around even though the current framework has moved on.

But the core responsibility is understandable. Keep restricted money restricted. Track it clearly. Document what you did. Build controls that make the record trustworthy.

That matters whether your church crosses the Single Audit threshold or stays well below it. Large recipients need formal audit readiness. Smaller recipients need the same habits on a smaller scale. In both cases, the work is stewardship. You're showing the congregation, the board, grantors, and outside reviewers that the church handles entrusted funds carefully.

The encouraging part is this: churches don't need a large back-office department to do this well. They need a clear process, consistent records, and tools that fit the realities of church finance.

When those pieces are in place, compliance stops feeling like a burden imposed from outside. It becomes evidence of mature, transparent ministry leadership.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Frequently Asked Questions about Federal Audits

A few practical questions come up repeatedly, especially for churches receiving federal funds for the first time.

Common questions about Single Audits for churches

| Question | Answer |

|---|---|

| Is omb a 133 still the current rule? | No. The older A-133 framework was superseded by Uniform Guidance, but people still use the old phrase when talking about Single Audit requirements. |

| If we're under the audit threshold, can we relax? | No. You may not need a Single Audit, but you still need to segregate, track, and document federal funds carefully. |

| Do pass-through grants count? | They can. If federal money comes through a state or local agency, the church still needs to understand the federal requirements attached to it. |

| What is a SEFA? | It's the Schedule of Expenditures of Federal Awards, a report that lists federal expenditures by program for audit purposes. |

| What kind of records should we keep? | Keep the award agreement, amendments, invoices, receipts, payroll support, reports submitted, and internal approvals tied to the grant. |

| What if our current bookkeeping system mixes everything together? | That's a warning sign. Mixed records make reporting, compliance review, and future audit preparation harder than they need to be. |

A few short answers to common worries

Some treasurers ask whether this is mainly an issue for large ministries. It isn't. Smaller churches often feel the pressure more because they have fewer staff and less time for cleanup work.

Others ask whether intent counts if the records are imperfect. Intent matters morally, but auditors and grantors still need documentation. Good stewardship has to be visible on paper, not just assumed.

Clean records protect both the church and the people serving it.

Another concern is whether the pastor needs to understand every technical rule. Usually not. But the pastor and board should understand that federal funds carry restrictions and that the finance team needs support to manage them properly.

If your church wants a cleaner way to handle restricted funds, federal grants, and board-ready reporting, take a look at Grain. It's built for church finance, uses true fund-based accounting, and helps small to medium-sized congregations keep every dollar tied to its intended purpose. You can Schedule a Demo to explore a simpler path to transparent stewardship.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.