Restricted vs Unrestricted Funds in Church Accounting

Master church finances by understanding restricted vs unrestricted funds. Our guide offers practical tips for stewardship, reporting, and legal compliance.

At its core, the distinction between restricted and unrestricted funds comes down to one simple thing: donor intent. When someone gives to your church, do they have a specific purpose in mind for that money? Answering that question correctly is the first step toward sound financial stewardship and maintaining the trust of your congregation.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

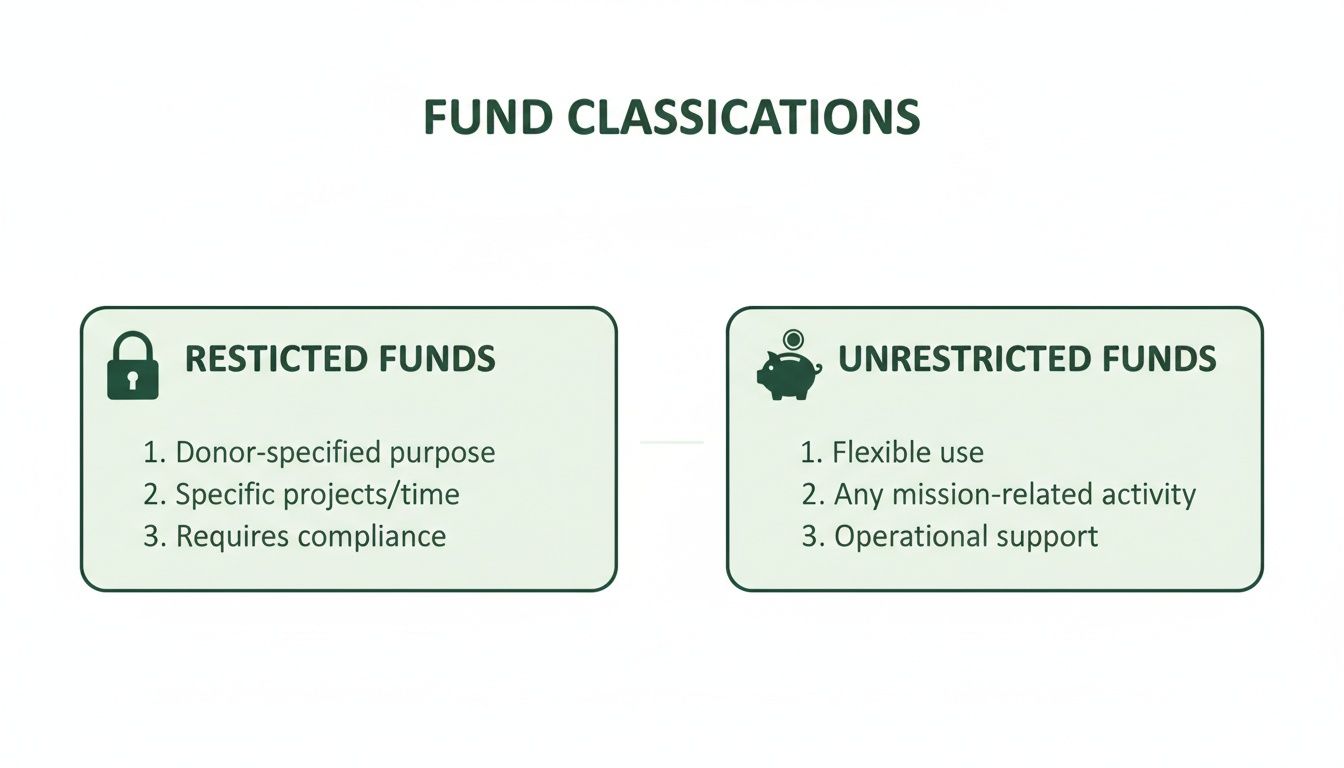

What Are Restricted and Unrestricted Funds?

Think of it this way: unrestricted funds are the lifeblood of your church’s daily operations. These are the tithes and general offerings that go into the main pot to cover salaries, keep the lights on, and support your ministry's day-to-day activities. You have discretion over how to use them for the church's general mission.

Restricted funds, on the other hand, come with strings attached. These are donations legally earmarked for a specific purpose defined by the donor—like a contribution to the "New Building Fund," a special offering for "Youth Missions," or a gift designated for a new sound system. You can't just dip into the building fund to cover a budget shortfall in the general fund.

This isn't just a matter of good bookkeeping; it’s a legal and ethical obligation. Getting it wrong can have serious repercussions.

As the graphic shows, unrestricted funds give you flexibility, while restricted funds lock in a specific use, highlighting why they must be managed separately.

Why Correct Classification Is Non-Negotiable

The stakes for tracking these funds properly are incredibly high. It’s all too easy to make mistakes with manual methods; we’ve seen reports indicating that as many as 65% of churches have struggled to accurately track multiple restricted funds with spreadsheets, leading to errors in nearly 40% of cases.

Those aren't just numbers on a page. An error—like using money from a designated missions fund to pay for general administrative costs—violates the donor's trust and can create significant legal liability. In a worst-case scenario, misallocating funds could even jeopardize your church's tax-exempt status.

Proper fund accounting is the bedrock of congregational trust. When donors see their contributions are honored and managed with integrity, their confidence—and generosity—grows.

This is precisely why a dedicated system is so important. Trying to manage this complexity with generic accounting software or spreadsheets is a recipe for commingling funds. A purpose-built solution like Grain Ledger automates the separation of every restricted and unrestricted dollar, ensuring compliance from the moment a donation is received. You can see how this works in our complete guide to fund accounting for churches.

Of course, to really get a handle on fund accounting, it helps to be clear on the basics, like understanding the difference between cash basis and accruals accounting.

For a quick summary of how these two fund types stack up, the table below breaks down the key differences.

Restricted vs Unrestricted Funds at a Glance

Here’s a simple side-by-side look at the fundamental characteristics that define restricted and unrestricted funds in a church setting.

| Characteristic | Restricted Funds | Unrestricted Funds |

|---|---|---|

| Donor Intent | Given for a specific project or purpose (e.g., missions, building). | Given for general operational support (e.g., tithes, offerings). |

| Usage | Legally bound to be spent only on the designated purpose. | Can be used at the church's discretion for any valid expense. |

| Flexibility | Inflexible; cannot be repurposed without donor permission. | Highly flexible; can cover salaries, utilities, programs, etc. |

| Accounting | Requires separate tracking for each designated fund. | Pooled into a general fund for operational use. |

Understanding these distinctions is foundational. With this knowledge in hand, you're better equipped to handle donations with integrity and build a strong, transparent financial future for your ministry.

The Legal and Accounting Framework for Church Funds

Getting a handle on restricted vs. unrestricted funds isn't just a matter of good bookkeeping—it's a legal and ethical requirement. For any church, mastering this distinction is foundational to maintaining compliance, building donor trust, and protecting the ministry from serious financial and legal risks.

So, who sets these rules? The standards come from the Financial Accounting Standards Board (FASB), the body that establishes nonprofit accounting rules in the U.S. These aren't suggestions; they dictate how every church and nonprofit must report its financial activities.

A key update, ASU 2016-14, simplified how nonprofits present their finances. It requires organizations to classify net assets into just two categories: assets with donor restrictions and assets without donor restrictions. The goal was to give a much clearer, at-a-glance picture of a ministry's financial flexibility and its obligations to its donors. For a deeper dive, check out our guide on FASB ASC 958.

Donor-Restricted vs. Board-Designated Funds

One of the most common points of confusion I see with church leaders is the difference between funds a donor restricts and those the board merely designates. The distinction is critical because they carry completely different legal weight.

Donor-Restricted Funds: Imagine a donor gives the church a large gift specifically for a new roof. This creates a legal obligation. The church must use that money for the roof. It can't be diverted to cover a payroll shortfall or any other expense, no matter how urgent.

Board-Designated Funds: Now, let's say the church board decides to set aside $10,000 from the general fund for future outreach events. This is an internal earmark. Because the money was originally unrestricted, the board retains the authority to change its mind and redirect those funds to a more pressing need if circumstances change.

Honoring donor intent is not just good stewardship—it is a legal requirement. Misusing donor-restricted funds can lead to serious consequences, including lawsuits and scrutiny from the IRS that could challenge a church's tax-exempt status.

Temporary vs. Permanent Restrictions

Donor restrictions also fall into two main types, which affect how long the funds have to be managed separately. Getting this right is key to sound, long-term financial planning.

Temporarily Restricted Funds are tied to a specific purpose or time frame. Once the project is finished or the time has passed, the restriction is lifted, and any leftover funds can be moved. A classic example is a capital campaign to raise $500,000 for a new building. Once the building is complete, the restriction is fulfilled.

Permanently Restricted Funds, on the other hand, are meant to last forever. Think of an endowment. A donor might stipulate that the original gift (the principal) must be invested and never spent. Only the investment earnings can be used, often for a specific purpose like scholarships or mission work.

This accounting framework has profoundly changed how churches must operate. Research reveals that 45-60% of all donations to U.S. churches come with restrictions. Yet, "designation confusion" remains a major blind spot, with up to 40% of churches admitting they struggle to properly separate donor-restricted funds from board-designated ones. As you can read in these insights about properly using designated funds on Church Admin, this creates a significant compliance risk.

Practical Bookkeeping: Tracking Every Dollar Correctly

Knowing the difference between restricted and unrestricted funds is one thing; putting it into practice in your day-to-day bookkeeping is where the real work begins. To maintain financial integrity and honor donor intent, every single donation has to be recorded correctly the moment it comes in. This all comes down to using a fund-based chart of accounts, where each fund is treated like its own mini-organization with its own set of books.

This is where many churches get into trouble. Trying to manage this with spreadsheets or generic business software almost always leads to commingled funds. These tools simply weren't built to enforce the strict separation that fund accounting requires, making it far too easy to accidentally spend restricted money on general operating costs. It's a mistake that can quickly break donor trust and create a massive compliance headache.

The only reliable way to handle these distinct legal and ethical obligations is to structure your accounting system around separate funds from day one. It's not just a best practice; it's a necessity.

The Anatomy of a Fund-Based Journal Entry

The secret to accurate tracking is in the journal entry. How a gift is first recorded dictates how it’s classified, tracked, and ultimately reported. Let’s break down how this looks for both unrestricted and restricted gifts.

An unrestricted gift, like a general tithe, is pretty straightforward. The entry shows an increase in your cash and, at the same time, an increase in the net assets of your general fund.

Example: Recording a $1,000 Unrestricted Tithe

- Debit: Cash ($1,000) – This reflects the increase in your bank account.

- Credit: General Fund - Tithes & Offerings ($1,000) – This assigns the income to your main operating fund.

A restricted donation, however, takes a different route. While it also increases your cash, the other side of the entry credits a specific liability or restricted net asset account. This is your accounting system’s way of flagging the money as "spoken for" and not available for general expenses.

Example: Recording a $5,000 Restricted Gift for the Building Fund

- Debit: Cash ($5,000) – Your bank balance goes up.

- Credit: Restricted Net Assets - Building Fund ($5,000) – This essentially "parks" the money in its designated bucket, clearly showing your obligation to the donor.

One of the most common—and dangerous—mistakes we see is when a church credits a restricted gift to a general income account and then tries to track its use on a separate spreadsheet. This completely breaks the accounting trail, makes accurate reporting nearly impossible, and puts the church at significant compliance risk.

These journal entries are the backbone of sound fund accounting. The table below illustrates how these different transactions play out side-by-side.

Sample Journal Entries for Fund-Based Donations

This table shows the correct double-entry bookkeeping for recording and spending both restricted and unrestricted donations. Notice how each transaction type directly affects the fund it belongs to.

| Transaction Type | Account Debited | Account Credited | Impact |

|---|---|---|---|

| Unrestricted Donation | Cash | General Fund: Tithes & Offerings | Increases cash and unrestricted net assets, making funds available for general operations. |

| Restricted Donation | Cash | Restricted Fund: Building Project | Increases cash and restricted net assets, creating an obligation to use the funds as specified. |

| Spending Restricted Funds | Restricted Fund: Building Project Expense | Cash | Decreases cash and reduces the balance of the restricted fund as the obligation is fulfilled. |

| Spending Unrestricted Funds | General Fund: Utilities Expense | Cash | Decreases cash and the balance of the general fund, covering operational costs. |

As you can see, every dollar is accounted for within its designated fund, ensuring you never accidentally spend money you don't truly have available.

Why Your Accounting Software Matters

In theory, these journal entries are simple. In reality, executing them consistently without the right tools is a huge challenge. This is why a purpose-built church accounting platform like Grain Ledger makes such a difference. It's built from the ground up on a native fund-based architecture, meaning every transaction is automatically and permanently tied to a specific fund.

When donations come in from your giving platform, Grain Ledger automatically directs them to the correct fund—whether it's the "General Fund," "Missions," or "Building Fund"—with no manual work needed. This all but eliminates the human errors that creep in with spreadsheets or generic software. For a deeper dive into the mechanics of moving money between funds, check out our article on fund-to-fund accounting.

Ultimately, this level of automation not only saves countless hours but also gives church leaders a real-time, trustworthy picture of the church's financial health, clearly separating what's available to spend from what is legally obligated.

Financial Reporting That Builds Trust and Transparency

Accurate bookkeeping is just the starting line. The real work of building congregational trust happens when you can present your church’s financial story with clarity. Without clear reporting, even the most meticulous tracking doesn’t mean much. The goal is simple: give your leaders a true picture of your financial health, making it obvious what money is obligated and what’s actually available to spend.

This is how you live out stewardship in front of your board, your finance committee, and your entire congregation. When people see exactly how their contributions are being used and that their specific intentions are being honored, their confidence in leadership skyrockets. That confidence often translates directly into greater generosity.

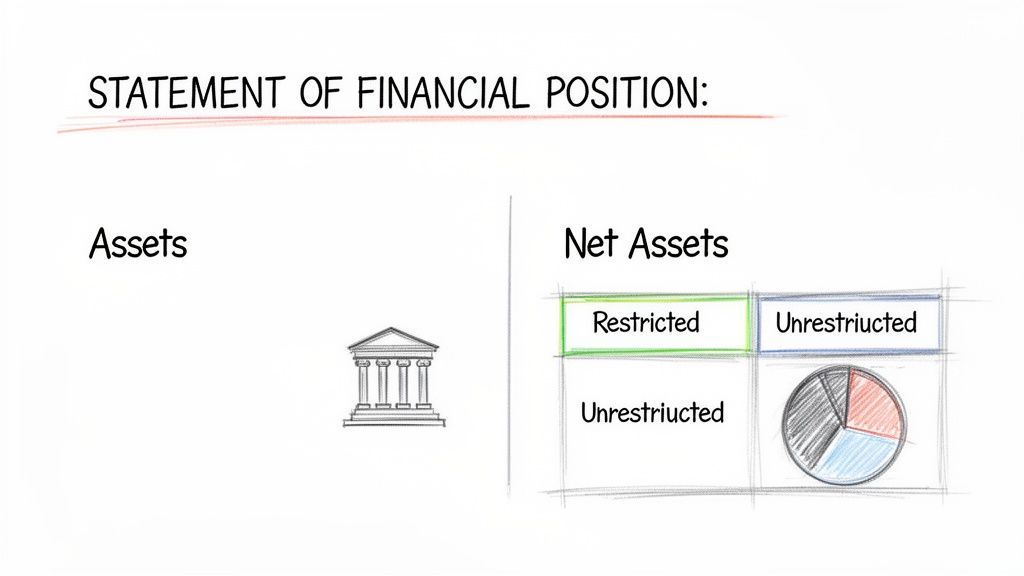

The Statement of Financial Position: A True Picture of Health

Of all the reports you can run, the Statement of Financial Position (what many call a Balance Sheet) is one of the most vital for a church. To be truly useful, it absolutely must separate net assets with donor restrictions from net assets without donor restrictions. This isn't just an accounting detail; it’s a critical guardrail that prevents one of the most common—and dangerous—leadership mistakes: confusing a big bank balance with a big budget.

It’s an easy trap to fall into. Your church might have $200,000 in the bank, which looks great on the surface. But if $180,000 of that is restricted for the future building project, you only have $20,000 for payroll, utilities, and ministry expenses. A properly formatted report makes this distinction impossible to miss, forcing realistic, data-driven decisions.

The greatest danger in church finance is a lack of clarity. A report that shows total cash without separating restricted funds is not just unhelpful—it's deceptive. True visibility protects a church from accidentally spending money it doesn’t actually have.

This isn’t a hypothetical problem. One Ministry Brands analysis found that for 55% of churches, restricted funds made up more than half of their total assets. At the same time, 35% had dangerously low unrestricted reserves—less than two months of operating expenses. This "visibility gap" has real consequences. In that same analysis, 62% of finance teams using manual methods admitted to confusing bank balances with spendable cash, which led to overspending in 28% of those cases.

The Statement of Activities: Proving Compliance

Next up is the Statement of Activities, which acts like an income statement for a nonprofit. For a church, this report needs to show all revenue and expenses broken down by each individual fund. This format isn't just a best practice; it's essential for proving compliance and communicating your stewardship wins.

When you report on a fund-by-fund basis, you can show your congregation that $15,000 was raised for the missions fund and then show them exactly how that $15,000 was spent on missionary support and outreach events. This level of transparency is how trust is forged. It offers concrete proof that every restricted dollar was used exactly as the donor intended.

For a deeper look into how these reports are structured, reviewing some nonprofit financial statements examples can provide some great real-world context.

Automating Reports That Tell the Right Story

Trying to stitch together these detailed, fund-based reports in a spreadsheet is an exercise in frustration and risk. It's incredibly time-consuming, and a single misplaced formula or incorrect cell reference can completely warp your financial picture. This can lead to disastrous decisions and, even worse, broken trust with your congregation.

This is where a dedicated church accounting solution becomes a necessity, not a luxury. For churches navigating the complexities of fund accounting, a purpose-built system like Grain Ledger is the answer. Its entire architecture is designed around funds, so it automates the creation of these critical reports. With Grain Ledger, you can generate an accurate Statement of Financial Position and a fund-specific Statement of Activities in just a few clicks. It ensures your leadership team always has a clear, reliable, and up-to-date view of your church’s true financial reality, empowering confident and faithful stewardship.

Navigating Real-World Church Finance Scenarios

The real test of good stewardship isn't just about balancing the books; it's about how you handle the specific gifts people entrust to you in real-life ministry situations. Accounting theory is one thing, but making the right call week in and week out is where integrity is truly demonstrated.

Let’s walk through a few scenarios that your church finance team has probably already faced. Seeing how the rules for restricted vs unrestricted funds apply in practice will help your team move forward with clarity and confidence.

Case Study 1: The Multi-Year Capital Campaign

Imagine your church kicks off a three-year, $1 million capital campaign to build a new children's ministry wing. Donations start coming in, all clearly designated for the "Building Fund." This is a perfect example of a large-scale project funded by temporarily restricted gifts.

Here’s how to manage it correctly:

- Accepting Donations: Every single gift marked for the campaign must be deposited directly into a dedicated "Restricted Fund: Building Project." This immediately walls it off from your general operating budget.

- Tracking Balances: You need a clear, running total of this fund at all times. Leadership needs to see, at a glance, exactly how much has been raised toward the $1 million goal.

- Disbursing Payments: As construction gets underway, all payments—to architects, contractors, or material suppliers—must be paid directly from this building fund. Each check written reduces the fund’s balance and shows you’re making progress on fulfilling the donors' wishes.

- Reporting Use: Regular updates to the congregation are critical. These reports should transparently show the total raised and how money has been spent, which builds trust and keeps the campaign’s momentum going.

Case Study 2: Funding Mission Trips

Your youth group is organizing a mission trip with a $10,000 budget, and the church holds special offerings to cover the cost. When people give, they have the explicit expectation that their money will get those students on the trip.

In this case, the funds are temporarily restricted for a specific program. The key is to track all the income and every single expense within one self-contained fund.

When a donor gives to a specific cause, they are entrusting you with more than just money—they are entrusting you with a piece of their heart for ministry. Honoring that intent is the highest form of financial stewardship.

First, you’ll set up a "Restricted Fund: Youth Mission Trip." All designated offerings are credited there. As you start paying for airfare, lodging, and on-the-ground supplies, each expense is debited from that same fund. This creates a clean, self-contained financial story for the trip, making it easy to report back to the board and your donors.

Case Study 3: Administering a Benevolence Fund

Most churches maintain a benevolence fund to help people in the community who are facing a crisis. Donations to this fund are restricted specifically for charitable aid and can never be used for general church operations.

The process is straightforward but non-negotiable:

- Establish the Fund: A "Restricted Fund: Benevolence" needs to be created in your chart of accounts.

- Record Donations: Any gift designated for "benevolence" or "community aid" goes directly into this fund.

- Distribute Aid: When the church helps a family with a utility bill or buys groceries for someone in need, that payment is expensed from the benevolence fund. This ensures you always have an accurate picture of how much is available for the next request.

This strict separation is vital. It legally protects the church and prevents the accidental use of aid money for a new sound system or other operational costs. This is where having a purpose-built accounting solution like Grain Ledger becomes so important, as its fund-based architecture automates this tracking and prevents the commingling of funds that can so easily happen in a spreadsheet.

These practical examples show why a deep understanding of restricted vs unrestricted funds is non-negotiable for any ministry. It gives your finance team the tools to handle complex financial situations with integrity, ensuring every gift is stewarded exactly as the donor intended.

Automating Fund Accounting with Grain Ledger

Let's be honest: trying to track restricted funds manually is a recipe for headaches. I've seen countless churches get tangled up in spreadsheets riddled with formula errors or try to force generic business software to do a job it was never designed for. These workarounds inevitably lead to commingled funds, wasting precious time and creating serious compliance risks that can obscure the true financial picture for your leadership team.

Thankfully, you don't have to wrestle with those outdated methods anymore. Modern church accounting software is built from the ground up to solve this exact problem. For any church that's serious about proper fund accounting, a platform like Grain Ledger is designed to be the answer.

Just looking at a purpose-built dashboard gives you an immediate sense of clarity. You can see the balance of every single fund at a glance, making it simple for leaders to know exactly what’s restricted and what’s available for general ministry. That clarity is the foundation of sound financial decision-making.

How Native Fund Accounting Creates Automation

So, what makes this kind of software different? It’s not just a feature tacked on; it’s the core architecture. Unlike generic platforms, Grain Ledger is built on a native fund-based system. This means the moment a donation comes in, it's automatically assigned to the correct fund. This creates a permanent, accurate accounting trail without you having to lift a finger.

The real power comes from its ability to connect with the tools you're already using. Grain Ledger integrates with popular giving platforms like Pushpay and Planning Center. When a donor gives $100 to the "Building Fund" on your website, that money doesn't just land in a general account—it flows directly into the corresponding restricted fund in your books. No more manual journal entries.

The goal of modern accounting isn't just to track numbers; it's to automate compliance so your team can get back to focusing on ministry. When the software handles the complexity, stewardship becomes simpler and far more transparent for everyone involved.

From Reconciliation to Reporting in a Click

The automation doesn't stop at donations. By linking directly to your church's bank accounts through Plaid, Grain Ledger can match deposited transactions to their correct funds automatically. This single feature can turn hours of tedious monthly bank reconciliation into a quick review, all while eliminating the human errors that often lead to misstated fund balances.

This all leads to the best part: trustworthy, one-click reporting. Because every transaction has been correctly categorized from the very beginning, you can instantly pull the reports you need to see.

- A Statement of Financial Position that automatically and clearly separates net assets with and without donor restrictions.

- A Statement of Activities that shows income and expenses broken down by each individual fund.

This level of built-in automation gives your finance team back countless hours, prevents critical accounting mistakes, and provides your leadership with the real-time, accurate data they need to lead with confidence and steward resources faithfully.

Compare platforms in our best church accounting software guide for 2026, or review Grain Ledger church accounting software.

Related fund stewardship resources

These guides help churches connect designated funds, policies, approvals, and financial reporting.

- Church benevolence fund guide - set policy, approvals, and accounting controls

- Restricted fund guide - understand donor restrictions and fund balances

- Fund accounting in Grain Ledger - track designated gifts and ministry funds in the ledger

- Schedule a Grain Ledger demo - see fund-level reports and bank reconciliation

Frequently Asked Questions About Church Funds

Even after you've got a handle on the fundamentals, real-world situations always bring up tricky questions about managing restricted and unrestricted funds. Let's walk through some of the most common scenarios we see church leaders face and get you the clear answers you need to handle them with confidence and integrity.

What Happens if We Raise More Restricted Funds Than Needed?

This is a wonderful "problem" to have, but it demands a careful, transparent response. When a project finishes under budget or a fundraising campaign exceeds its goal, you're left with a surplus of restricted money. Your first instinct might be to move it to the general fund, but you can't.

The only right way forward is to communicate directly with the original donors. You need to make a good-faith effort to explain the situation and ask for their permission to redirect the extra funds. You could suggest using it for a closely related ministry need or ask them to release the restriction entirely. Whatever you do, getting that permission in writing is absolutely essential for your records.

Can Our Board Designate Unrestricted Money?

Yes, absolutely. This is a common practice and highlights a crucial difference in fund types. Your church board can internally earmark unrestricted money for a specific future purpose, like setting up a reserve fund for a new roof or putting money aside for a large outreach event. This is what's known as a board-designated fund.

The key difference here is all about control. Board-designated funds are an internal accounting tool; they offer flexibility because the board can change its mind and redirect that money if a more urgent need pops up. Donor-restricted funds, on the other hand, are legally binding based on the donor's instructions, and the board has no authority to change them.

How Long Must We Keep Records for Restricted Donations?

This is a point that trips up many churches. The record-keeping requirement for a restricted donation isn't tied to your standard 7-year document retention policy. You must maintain clear, detailed records for as long as that restriction is active.

Simply put, the obligation lasts until every penny has been spent according to the donor's original intent. If it's a multi-year building project, you're keeping those records for the entire duration. If it's a permanent endowment fund, that record-keeping obligation is perpetual. These records are your primary evidence that you've honored the donor's wishes.

Can We Use Restricted Funds for Administrative Overhead?

This is a big one. The short answer is yes, but only with complete transparency. Generally, it's permissible to use a portion of restricted gifts to cover administrative costs that are directly related to managing that fund and its purpose.

The best way to handle this is to establish a clear policy before you even solicit the gifts. Many churches create an administrative fee or "indirect cost rate" and disclose it upfront. For example, your giving page or campaign materials might clearly state that 10% of all restricted gifts will be allocated to the administrative costs of running the program. As long as donors know this when they give, it's a perfectly acceptable and ethical practice.

Trying to navigate the complexities of restricted and unrestricted funds with spreadsheets or generic accounting software is a recipe for risk and headaches. You need a system built for the unique demands of church finance. See how Grain Ledger’s purpose-built fund accounting automatically ensures every dollar is tracked correctly, giving you unshakable confidence in your stewardship. Learn more at grainledger.com.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.