Best Bank Reconciliation Software for Churches in 2026

Find the ideal bank reconciliation software for your church in 2026. Explore fund accounting, key features, & how Grain Ledger simplifies stewardship.

Sunday evening is when this usually catches up with people. The service is over, deposits are made, and someone opens a spreadsheet to match the bank account against a list of tithes, offerings, online gifts, and designated donations. At first, it looks manageable. Then the questions start. Was that transfer for missions or general? Did the youth camp gift land in the right place? Why does the bank total tie out while the fund report still feels wrong?

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Start free to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

That's the trap many churches live in for years. The books may reconcile at the cash level, but the stewardship still isn't clear. A church doesn't just need to know whether the bank balance matches. It needs to know whether every restricted dollar still sits in the right fund, whether the board can trust the report in front of them, and whether the church can answer donor questions without digging through old notes and disconnected files.

The End of Spreadsheet Stewardship

Most church treasurers don't start with bad habits. They start with what's available. A spreadsheet, a bank login, a stack of deposit records, and maybe exports from a giving platform. For a while, that feels responsible. You can see every line. You can manually tick each item off. You can tell yourself nothing is being missed.

But manual reconciliation gets fragile fast. One copied row in the wrong place, one uncleared transaction left hanging too long, one designated gift posted to the wrong bucket, and the report you present to the pastor or finance committee stops telling the truth.

Where the stress really comes from

The hardest part isn't matching the bank statement to the ledger. It's the fear that a reconciled number can still hide a stewardship problem. Churches carry more nuance than a small business does. A donation for benevolence isn't interchangeable with a general offering. A building fund gift isn't available for utilities just because the checking account has enough cash.

A bank account can be accurate while fund stewardship is still wrong.

That's why more organizations are moving away from manual reconciliation. The broader market reflects that shift. The global bank reconciliation software market was valued at approximately $2.71 billion USD in 2024 and is projected to reach $5.2 billion USD by 2035 (Wise Guy Reports). Churches feel the same pressure for the same basic reason. Manual review creates errors, delays, and uncertainty.

If you want a good primer on the first layer of this shift, Matil has a useful guide that can help teams learn to automate bank statement review. That kind of automation matters, especially when volunteers are stretched thin and month-end depends on a few people who already wear too many hats.

Why cloud systems changed the conversation

Churches used to treat cloud accounting as optional. It isn't anymore. Once your bank feeds, donation records, and accounting entries live in separate places, your reconciliation process depends on manual glue. That's where most finance teams lose time and confidence.

A practical next step is to understand the benefits of cloud accounting in a church setting. The primary benefit isn't trendiness. It's that the system can pull the work into one place so reconciliation becomes a controlled process instead of a monthly scramble.

What Is Bank Reconciliation Software

Bank reconciliation software is a tool that compares what your bank says happened with what your books say happened, then helps you resolve the differences. The simplest way to think about it is this: it's a digital assistant that checks whether every line on the bank statement has a corresponding line in your accounting records.

A manual process asks a person to do that comparison by eye. Bank reconciliation software asks the system to do the repetitive matching first, then shows the person what requires judgment.

What the software actually does

Good bank reconciliation software primarily handles three jobs well:

- Imports activity automatically through bank feeds, so you're not retyping statement lines.

- Matches transactions using rules so recurring items don't need to be cleared by hand every month.

- Flags exceptions so the team can focus on missing, duplicated, or misclassified entries.

Those are the core mechanics behind most serious tools. Nomentia notes that the main components include automated transaction matching using rule-based logic, bank feed integration for real-time data ingestion, and exception management systems that flag discrepancies. Those capabilities can reduce manual effort by 50% or more (Nomentia).

What this changes in daily work

Without software, reconciliation usually means downloading a statement, exporting a ledger, sorting dates, scanning amounts, and trying to remember what happened two or three weeks ago. With software, the bank feed and ledger entries are already in view. The routine items line up quickly. The actual work becomes reviewing exceptions.

That's where the value is. The software doesn't replace oversight. It removes the repetitive comparison work so the treasurer or bookkeeper can spend time on the transactions that deserve attention.

Here's a simple comparison:

| Process area | Manual method | Bank reconciliation software |

|---|---|---|

| Transaction intake | Statement downloads and copy-paste | Automatic feed import |

| Matching | Visual line-by-line review | Rule-based matching |

| Problem items | Often found late | Flagged as exceptions |

| Documentation | Notes in spreadsheets or email | Centralized record in the system |

Practical rule: If a person spends most of reconciliation just locating transactions, the process is broken before review even starts.

Churches also care about cash visibility. That's one reason broader reconciliation discipline matters beyond bookkeeping. If you're trying to connect reconciliation to planning, this overview of how to improve cash flow management gives useful context.

For the church-specific mechanics, it also helps to see a step-by-step walkthrough of how to reconcile bank accounts. The process itself isn't mysterious. What matters is whether the system supports the way a church handles money.

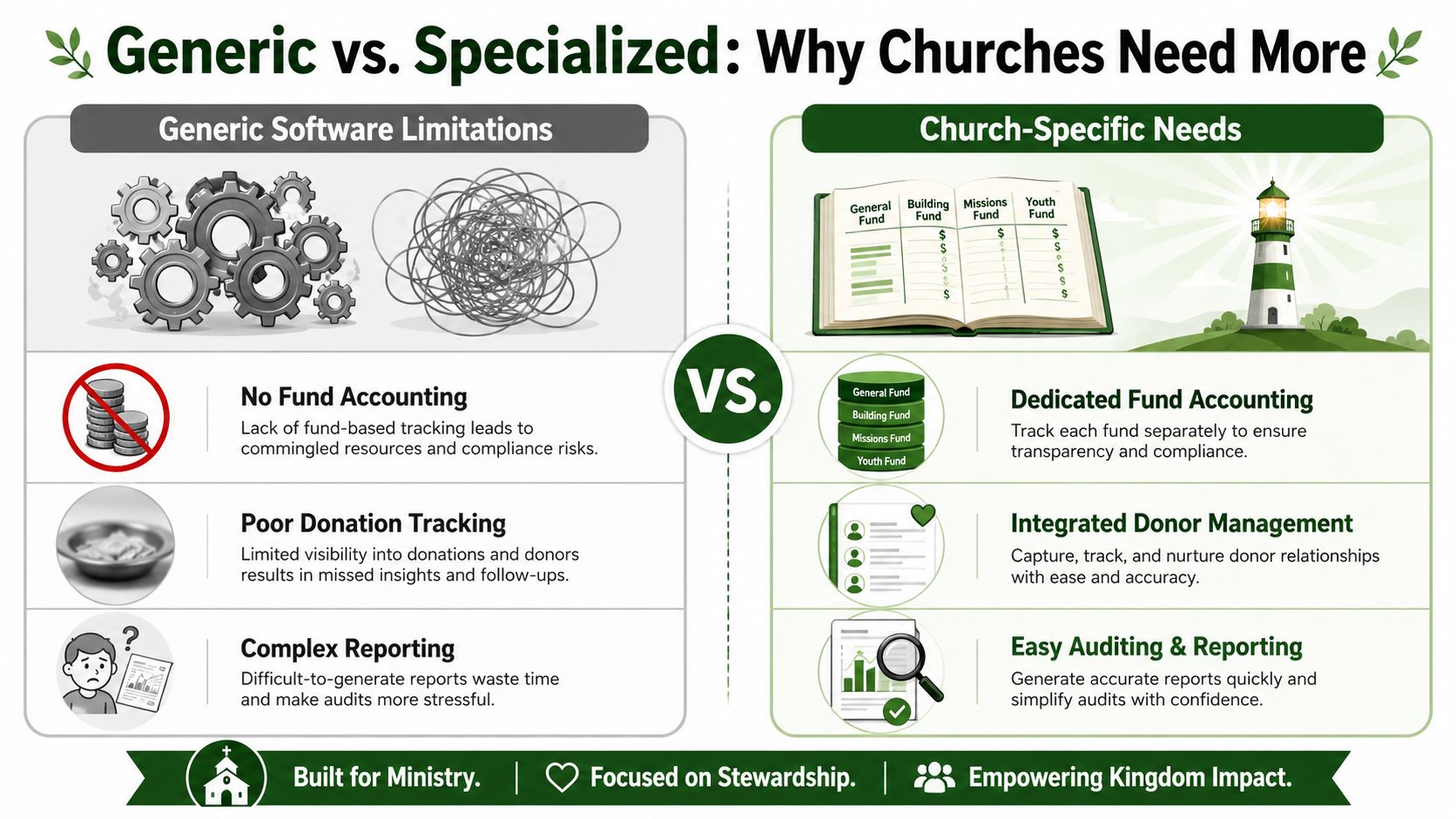

Why Generic Software Fails Your Church

Small business software usually reconciles one thing well: cash movement. It can show that deposits and withdrawals match the bank. For a retail shop or contractor, that may be enough. For a church, it often isn't.

A church has to reconcile by purpose, not just by balance. That's where generic systems break down.

The missing layer is fund accounting

Generic accounting tools treat money like a pooled resource unless someone manually separates it. Churches don't operate that way. If a donor gives to a building fund, that money carries a purpose. If someone gives to missions, the church has a responsibility to preserve that restriction.

This is the point almost every generic guide skips. They explain how to match bank lines to ledger lines, but they don't deal with fund-level reconciliation. They assume fund allocation happens later, after the bank work is done. In church finance, that assumption creates risk.

Data from church accounting best practices shows that 68% of church financial errors stem from misallocating restricted donations during the reconciliation process because generic software cannot trace every dollar to its intended fund account (Table Stewards).

A reconciled bank account can still hide a violation

Take a plain example. A family gives to youth camp. The money lands in the bank. A bookkeeper sees the deposit and clears it against the total donations received. The bank reconciliation is finished. The cash balance is correct.

But if that gift got posted into the general fund instead of the youth fund, the church now has a stewardship problem even though the bank rec “works.”

That's why generic systems create false comfort. They answer the question, “Did the money hit the bank?” Churches also need the answer to, “Is the money still assigned to the purpose the donor intended?”

What generic tools tend to miss

A committee member looking at software should be skeptical if a product only talks about feeds, matching, and month-end close. Those matter, but they aren't enough for ministry finance.

Watch for these weak spots:

- Pooled cash thinking means the software can reconcile totals without protecting designated balances.

- After-the-fact fund coding leaves too much room for manual cleanup and memory-based corrections.

- Business-style reporting often produces statements that make sense to accountants but not to pastors, elders, or donors.

- Disconnected giving records separate the donation source from the accounting result.

If a tool can't tell you where a restricted gift sits after reconciliation, it isn't built for church stewardship.

QuickBooks and Xero can serve many businesses well. They just weren't built around donor restrictions as a first principle. Churches need that principle built in, not bolted on.

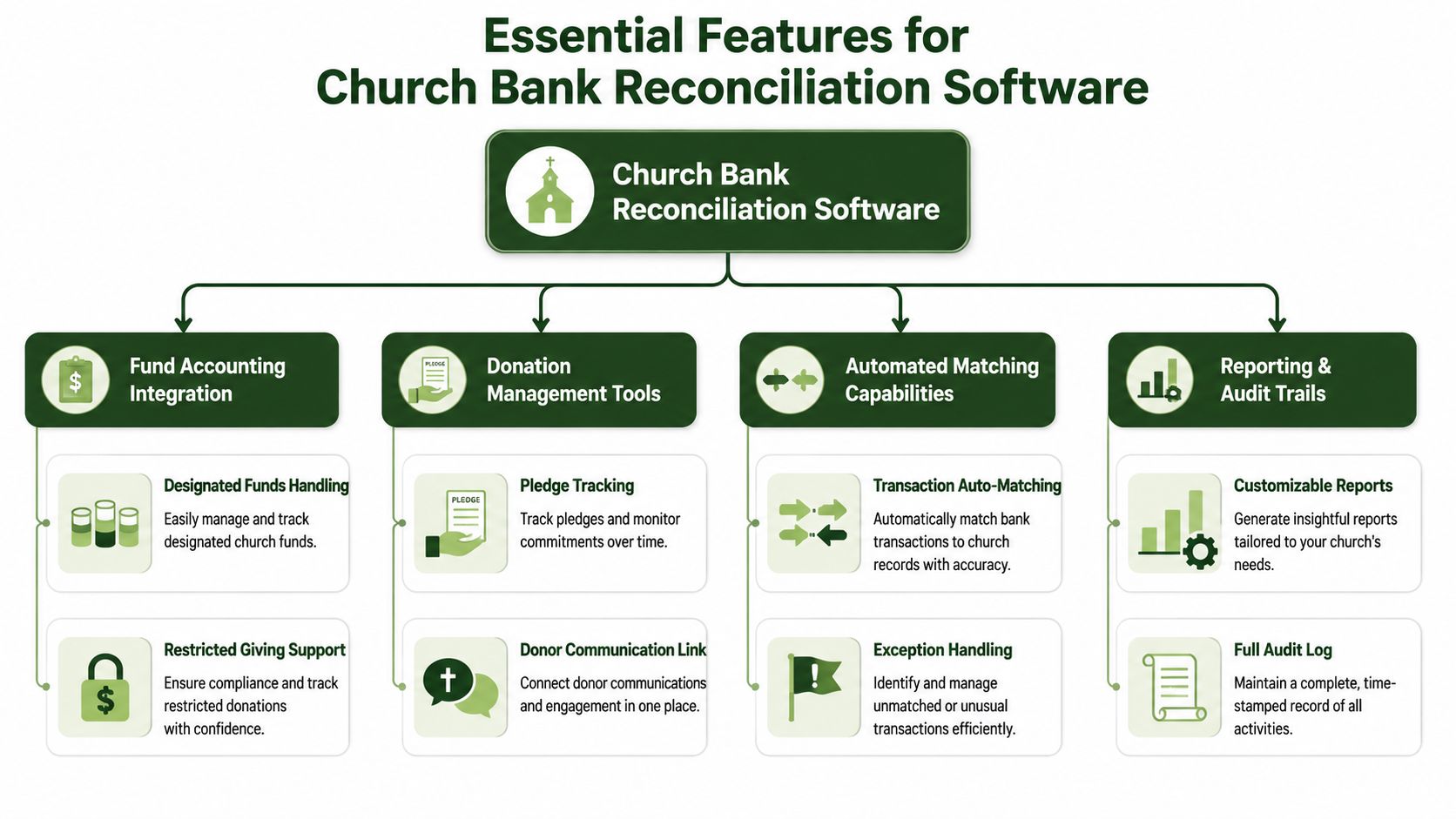

Must-Have Features for Church Bank Reconciliation

Once you see the fund problem clearly, the feature list changes. A church shouldn't shop for bank reconciliation software the same way a business does. Speed matters, but stewardship controls matter more.

The right system needs to do more than clear transactions. It needs to preserve the identity of each dollar from receipt through reporting.

Fund separation has to be native

This isn't a nice extra. It's the foundation. Purpose-built church accounting software must enforce fund separation automatically, creating virtual walls between funds such as General, Building, and Missions to prevent accidental or illegal use of restricted money, which standard accounting software lacks (Grain Ledger).

If the software lets users blur those lines too easily, it creates the exact risk a church is trying to remove.

The checklist that actually matters

When I review church systems, I look for five things before anything else.

True fund-level mapping

Every deposit, transfer, and expense should tie to a specific fund from the start. Not in a note field. Not in a workaround. In the actual accounting structure.Giving platform integration

Churches receive money through offering plates, ACH, cards, and online giving tools. The software should bring that donation data in with the fund designation intact so reconciliation doesn't require re-keying or guesswork.Audit trail visibility

The committee should be able to see who changed a transaction, when they changed it, and what the original entry was. Churches need accountability that survives staff turnover and volunteer rotation.Exception handling

Good software should surface mismatches clearly. If a deposit amount differs from the giving report, the system should make that discrepancy obvious instead of burying it in a general ledger detail screen.Reporting people can readily use

A pastor or board member should be able to read fund activity without needing an accountant to translate every line.

Features churches often forget to ask about

Some requirements only surface after a painful year-end or donor question.

| Feature | Why it matters in a church |

|---|---|

| Fund-restricted controls | Prevents misuse of designated gifts |

| Donor-linked receipts | Connects donations to records cleanly |

| General ledger integration | Keeps fund activity and books aligned |

| Reconciliation workflow | Makes month-end review repeatable |

| Giving platform sync | Reduces manual imports and recoding |

Modern church accounting systems should also unify fund accounting, donor management, general ledger tracking, financial reporting, bank reconciliation, and giving platform integration into one system (Pushpay). If those parts live in silos, the treasurer becomes the integration layer, and that's when mistakes multiply.

How Grain Ledger Streamlines Fund Reconciliation

The actual test comes after Sunday. The deposit hits the bank, the giving platform shows designated gifts, and the finance committee expects one clean answer about what belongs in general fund, missions, and benevolence. Generic reconciliation software can match the bank total and still leave the church with the wrong fund picture.

That is why Grain Ledger matters. It starts with church fund accounting, so reconciliation is tied to stewardship, not just bank clearing. A matched transaction is only finished when it lands in the right fund and supports the reports your pastor, treasurer, and board read.

What a purpose-built workflow looks like

In a church, reconciliation has to answer two questions at the same time. Did the bank activity clear correctly? Did the ministry intent of the money stay intact?

Grain Ledger handles that in one workflow:

- Imports bank transactions automatically.

- Pulls in donation and accounting records tied to church activity.

- Matches items without forcing staff to rebuild the trail by hand.

- Keeps the fund assignment attached so restricted and unrestricted balances stay accurate.

That fourth step is where generic tools usually break down. They reconcile cash, but they do not protect the reason the money was given. For a church, that is the whole point.

I have seen churches reconcile a deposit correctly at the bank level and still misstate the building fund because the accounting system treated the money like ordinary income. The books looked clean until someone asked for a fund balance report. Then the treasurer had to explain why the bank rec was done but the ministry reporting was still unreliable.

Why this works better for committees and pastors

Church leaders do not need another month-end process that only the bookkeeper understands. They need direct answers.

If the board asks whether designated missions gifts were spent or held, the answer should come from the system itself. If the pastor asks how much remains in benevolence, no one should need to open a spreadsheet, trace a deposit, and remember which journal entry fixed last month's coding issue.

You can see that church-specific workflow in Grain Ledger's church bank reconciliation feature overview. The advantage is straightforward. Bank activity, fund classification, and reporting live in the same system, so the reconciliation supports the story the church must be able to defend.

The trade-off is real. A generic platform may feel familiar at first, especially if someone on the team used it in a business setting. Churches pay for that familiarity later through workarounds, side schedules, and fund reports nobody fully trusts. Grain Ledger reduces that risk by treating fund reconciliation as part of the accounting record, not as a cleanup step after the fact.

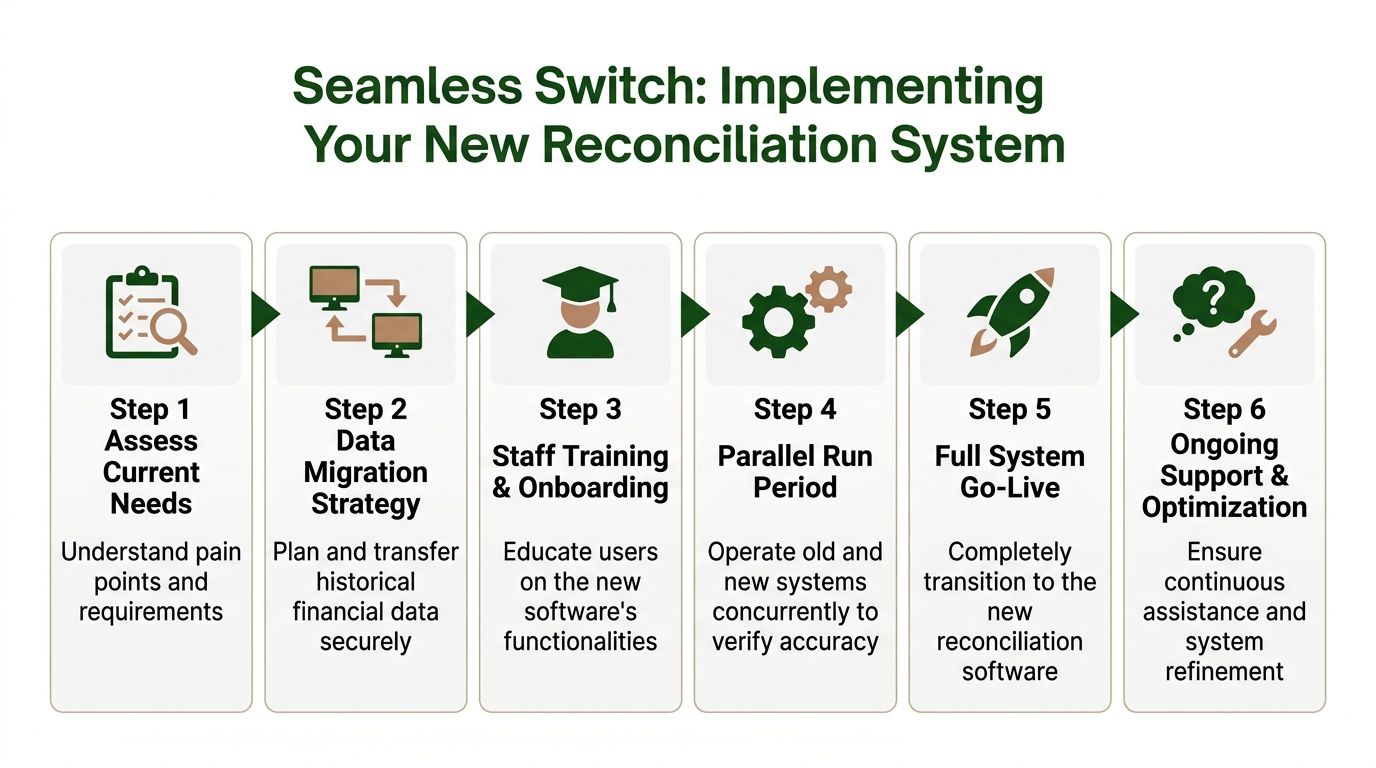

Implementing Your New Reconciliation System

The risky moment is not the month you keep using spreadsheets. It is the month you switch systems without cleaning up your fund structure first.

A church can import every bank transaction correctly and still start the new system with the wrong building fund balance, old uncleared items, or giving records that were never tied to the right restriction. Then the team blames the software for problems it inherited. Good implementation prevents that.

Start with fund clarity, not bank feeds

Churches should define funds before connecting accounts. That order matters.

List every active fund your church uses. General. Missions. Benevolence. Building. Youth. Outreach. Debt service. For each one, confirm three things: what money belongs there, who reviews it, and how it should appear in reports. If the finance committee cannot answer those questions clearly, the new system will only hide the weakness behind cleaner screens.

Then collect the records that determine whether your opening numbers can be trusted:

- Bank history that supports opening balances

- Current fund balances approved by the finance team

- Giving records from your donation platform

- Outstanding items such as uncleared checks or unresolved deposits

This step feels slow. It saves time later.

Test the system against real church activity

The first reconciliation period should be a controlled test, not a full handoff. Run the new system alongside the old method for one month and compare the output carefully.

Use actual deposits, actual restricted gifts, actual expense reimbursements, and actual transfers between accounts. Then ask the questions a pastor or committee member will ask, not just whether the bank balance agrees. Did the benevolence fund stay intact? Did the missions gifts land in the right place? Did a payment for building repairs reduce the building fund instead of disappearing into a generic expense line?

That is the implementation standard churches need. A clean bank match alone is too low a bar.

A practical rollout order

A careful rollout usually follows this sequence:

- Confirm your chart of funds so designated giving maps to the correct balances and reports.

- Connect bank accounts and giving sources only after the fund structure is approved.

- Import opening balances and have a second person verify them against prior reports.

- Reconcile one period in parallel with the legacy process and document every difference.

- Train each user by role so staff, treasurer, and backup volunteers know what they must review.

- Set a monthly review routine for exceptions, old outstanding items, and fund balance questions.

I have seen churches skip step four because everyone is tired of the old process. That shortcut usually creates a harder cleanup two months later, when no one remembers why a transaction was forced into the wrong fund.

Judge the new system by whether it produces bank agreement and trustworthy fund balances in the same month.

Training should also reach beyond the bookkeeper. Finance committee members do not need a tour of every screen, but they should know which reports to review, where restricted funds are protected, and how to spot unreconciled items before they age into permanent confusion.

A church-specific system such as Grain Ledger makes this transition easier because the team is not trying to bolt fund accounting onto a business workflow that was never built for ministry oversight. That does not remove the need for review. It does remove many of the workarounds that cause churches to carry errors from one month into the next.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Common Reconciliation Pitfalls to Avoid in Your Ministry

Church finance problems usually don't start with theft or obvious negligence. They start with convenience. Someone uses the wrong account for one expense. Reconciliation gets skipped for a month because the office is busy. A small discrepancy gets waved away because it “probably clears next time.” That's how confidence erodes.

The mistakes that keep repeating

A few patterns show up again and again in ministries:

Using personal accounts for church activity

This creates confusion immediately. Even if intentions are good, it tangles documentation, weakens internal control, and makes a clean reconciliation much harder.Reconciling too infrequently

If the church only catches up occasionally, mistakes age out of memory. The person reviewing later won't remember why a transfer happened or what fund it belonged to.Ignoring small differences Small unresolved items train the team to tolerate uncertainty. Over time, those unresolved items make it harder to spot the discrepancy that is significant.

Letting one person handle everything

If the same person receives donations, posts entries, and reconciles the bank account, there's too much concentrated control. Even honest people make mistakes. Review by another person protects everyone.

What healthy stewardship looks like

A strong church process is simpler than people think. Keep church money in church accounts. Reconcile on a regular cadence. Review exceptions while they're fresh. Separate duties where possible. Use software that protects fund restrictions instead of depending on memory and side notes.

The primary goal isn't just cleaner books. It's peace of mind. The pastor should be able to trust the numbers. The board should be able to read the reports. Donors should be able to believe their gifts were handled as promised.

If your church is ready to leave spreadsheet stewardship behind, Grain is the accounting solution I'd point you to. It's built for churches that need true fund-based accounting, bank reconciliation tied to donor intent, and reporting that makes sense to pastors, treasurers, and finance committees.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.