Church Financial Accountability: Secure Funds in 2026

Build trust and safeguard ministry funds with our 2026 guide to church financial accountability. Learn internal controls, fund accounting, and reporting.

A nationwide survey by Church Law & Tax found that nearly one-third of U.S. congregations have suffered from financial misconduct, with inappropriate expense reimbursements and direct theft of contributions showing up most often in those cases (Church Law & Tax). That should change how every church thinks about bookkeeping.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Start free to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

Church financial accountability isn't a paperwork issue. It's a ministry protection issue. When controls are weak, a church doesn't just lose money. It risks donor trust, staff credibility, board confidence, and the ability to fund ministry consistently.

In practice, most problems don't begin with dramatic fraud. They start with soft spots. A volunteer treasurer keeps too much in their head. Expense reimbursements happen without a written policy. A designated gift gets tracked in a spreadsheet instead of being separated in the accounting system itself. Generic software says it can "handle funds," but the structure underneath still runs on one general ledger with tags layered on top.

That last point is where many churches get exposed. If the system doesn't enforce fund separation at the time of entry, accountability depends on memory, cleanup, and luck. Churches that also run events or seasonal campaigns should pair their finance process with better planning on the front end, including practical proven event fundraising tips that help revenue come in with clearer purpose and cleaner tracking from day one.

Introduction

Most churches don't set out to build weak financial systems. They inherit them.

A pastor asks a faithful volunteer to "help with the books." The offering process stays informal because everyone knows each other. Restricted gifts get tracked on a side spreadsheet because the accounting software doesn't really understand ministry funds. For a while, that can seem workable. Then the church grows, staff turns over, or a question comes from the board, and nobody can answer it cleanly.

That's why church financial accountability has to be treated as operating discipline, not occasional cleanup. A healthy system answers simple questions fast. What money was designated for missions? Who approved this payment? Has the bank activity been reconciled? Can the board see each fund without asking someone to rebuild the numbers manually?

Churches don't lose trust only when someone steals. They also lose trust when leaders can't show where restricted money went.

Good accountability protects honest people as much as it deters dishonest behavior. It gives volunteers a safe structure, gives boards better visibility, and gives givers confidence that the church takes stewardship seriously.

The standard isn't perfection. The standard is clarity, consistency, and controls that fit the church's actual size.

Why Financial Accountability Is a Non-Negotiable

Financial accountability sits at the intersection of stewardship, compliance, and witness. Churches handle gifts that people give in faith. That creates a higher obligation than basic bookkeeping.

Accountability protects more than the balance sheet

A church can be sincere and still run a risky finance process. That's common when policies stay unwritten and software isn't designed for nonprofit fund structures. The damage isn't limited to losses. Boards become reactive. Staff spend time defending transactions. Congregations start asking whether designated gifts are really staying designated.

Three responsibilities sit underneath strong accountability:

- Legal responsibility means the church must maintain records that support nonprofit reporting, restricted fund handling, and board oversight.

- Ethical responsibility means donor intent must be honored without shortcuts or borrowing between purposes.

- Spiritual responsibility means leaders should be able to speak plainly about stewardship because the records support what they say.

Strong standards already exist

This isn't a new or fringe expectation. The Evangelical Council for Financial Accountability, founded in 1979, accredits over 2,700 member organizations that voluntarily follow rigorous standards for financial reporting, auditing, and management of restricted funds, making it a meaningful benchmark for church integrity (ECFA overview).

That matters for one reason. Churches don't have to invent accountability from scratch. The sector has already shown that disciplined financial reporting and restricted fund management are achievable at scale.

| Accountability area | What healthy practice looks like |

|---|---|

| Donor intent | Designated gifts stay in the designated fund |

| Board oversight | Leaders review timely, understandable reports |

| Expense discipline | Purchases and reimbursements follow documented approval |

| Public trust | The church can explain how money supports ministry |

What weak accountability usually looks like

The warning signs are rarely dramatic at first. They look ordinary:

- One trusted person knows everything and nobody else can reproduce the reports.

- Reimbursements happen casually because staff are trying to move fast.

- Funds are tracked outside the ledger in a spreadsheet that only one person updates.

- Reports arrive late so the board reviews stale numbers.

Practical rule: If a church can't show fund balances and approval history without manual reconstruction, it doesn't yet have reliable financial accountability.

Church financial accountability isn't red tape. It's the structure that lets ministry keep moving without confusion, suspicion, or preventable mistakes.

Establishing Clear Governance Structures

Software matters, but governance comes first. A weak team structure will break even a good system.

Small churches feel this tension sharply. The same person may collect offerings, enter deposits, pay bills, and reconcile the bank account because there are not enough hands. Yet that's where the risk concentrates. Sixty-seven percent of church fraud cases occurred in organizations with no duty segregation, while only 28% of small churches under 100 attendees report having a formal finance committee or dual-signature policy (MMBB guidance).

Define who owns what

Churches need three levels of financial responsibility, even if some people serve in more than one capacity.

The treasurer or bookkeeper handles recording, routine review, and report preparation. This role shouldn't also carry unchecked authority to approve everything it records.

The finance committee reviews patterns, asks questions, and watches for exceptions. It doesn't need to run daily bookkeeping. It needs to provide informed oversight.

The board or elders approve policy, budget direction, and major financial decisions. They don't need every receipt. They do need clear reporting and a way to verify that controls are being followed.

Build a human firewall in small churches

The phrase "segregation of duties" can sound like advice written for larger ministries with office staff. Small churches still need it, but they need a scaled version.

Use this kind of split when people are limited:

- Person one receives and counts offerings with another counter present.

- Person two records deposits and enters transactions.

- Person three reviews bank reconciliation and monthly reports.

- Board leadership approves unusual or larger disbursements before payment.

If one person must wear multiple hats, add review at the next step rather than pretending ideal staffing exists.

One honest volunteer in an overloaded role isn't a control. A second set of eyes is a control.

Keep governance written, not assumed

A church doesn't need a thick policy binder to get this right. It does need written answers to basic questions:

- Who can approve expenses?

- Who can sign or release payments?

- Who reviews reconciliations?

- Who sees fund-level reports each month?

- What happens when the usual treasurer is unavailable?

A one-page policy that's followed beats a ten-page manual nobody reads. Governance works when names, approvals, and review steps are explicit.

Implementing Practical Internal Controls

Internal controls are the habits that make accountability real on an ordinary Tuesday. They don't have to be expensive. They do have to be consistent.

A church with good intentions but weak process will still drift into errors. The most common breakdowns I see involve offering handling, reimbursements, and payments that move faster than documentation.

Tighten the money-handling steps

Cash and checks need a short chain of custody. Count with two unrelated people present. Document totals. Deposit promptly. Record from the deposit support, not from memory.

For expenses, stop relying on informal reimbursement culture. It's cleaner to issue controlled ministry spending through approved payment methods than to let staff and volunteers spend personally and request repayment later. Reimbursements create friction, missing receipts, and emotional pressure to "just cover it."

For a broader view of how organizations reduce exposure in day-to-day finance operations, these accounting risk management strategies are worth reviewing alongside church-specific practices.

Use approvals that fit the risk

Not every payment needs the same process. Routine utility bills don't require the same review path as a surprise equipment purchase or a transfer from a designated fund.

A simple approval structure often works better than a complex one:

- Routine recurring bills can be preapproved through budget adoption and reviewed monthly.

- Staff reimbursements should require a receipt, ministry purpose, and supervisor approval.

- Nonbudgeted purchases should require written approval before the money goes out.

- Fund transfers should receive board-level visibility because they can blur donor intent if handled casually.

Churches that want a straightforward checklist for these workflows can adapt ideas from internal controls best practices for churches.

Here's a useful teaching tool for finance teams and boards:

Favor traceable payments over loose cash practices

A payment system should leave a trail. That's the point.

| Method | Accountability strength | Common weakness |

|---|---|---|

| Ministry card with review | Clear record tied to statements | Needs policy and receipt discipline |

| Bank payment with approval trail | Strong audit path | Can bottleneck if only one person manages it |

| Personal reimbursement | Works for exceptions | Often missing support or timely review |

| Petty cash | Fast for small needs | Hardest to monitor consistently |

The safest process is usually the one that leaves documentation automatically, not the one that depends on people remembering later.

Controls don't need to slow ministry down. They need to remove ambiguity before it becomes conflict.

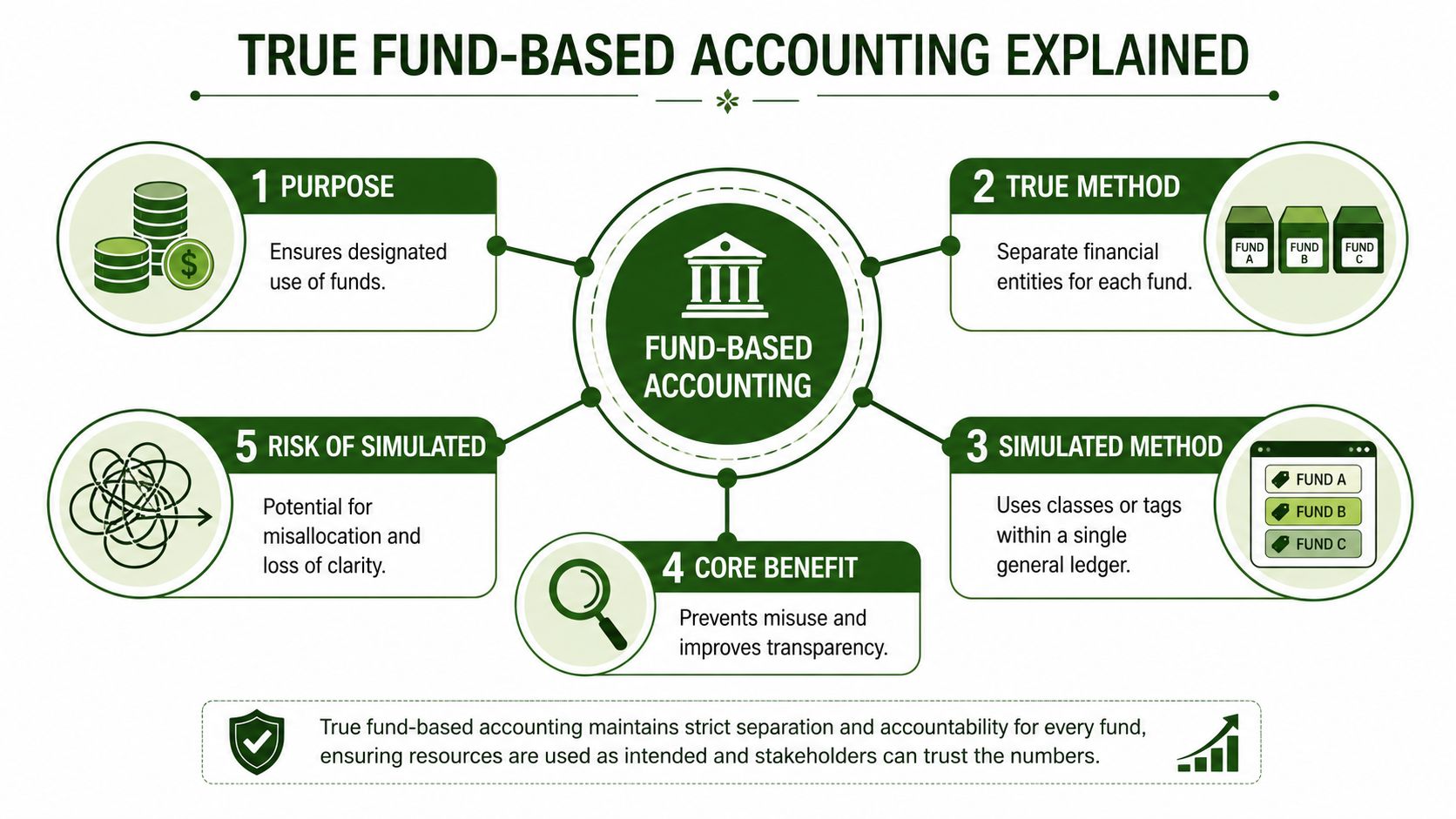

Adopting True Fund-Based Accounting

Many churches often misjudge the security of their financial practices. They use generic accounting software, create classes or tags, and assume they have fund accounting. In most cases, they have simulated fund tracking, not true fund-based accounting.

Simulated funds create hidden risk

A generic ledger can label transactions by ministry, campus, or category. That isn't the same as native fund architecture.

With simulated funds, the church often records activity in one overall accounting structure and then uses classes, tags, or spreadsheet adjustments to sort things out later. The system may look organized on reports, but it doesn't enforce separation at the transaction level. That means restricted and unrestricted activity can still be mixed underneath, then "cleaned up" at month-end.

That approach fails under pressure. It breaks when a volunteer changes, when reconciliations run late, or when someone posts to the wrong place and the error isn't caught quickly.

Native fund architecture changes the control point

Native fund accounting works differently. Each transaction is tied to a fund at entry. Donations are mapped to the right fund before they hit the ledger. Reports are built from that structure, not rebuilt after the fact.

This is why double-entry fund accounting matters for churches. The fund isn't just a label. It's part of the accounting architecture. A building gift lands in the building fund. Missions spending reduces missions resources. General operating cash remains general unless leadership intentionally and properly moves it.

If your team wants a plain-language breakdown of this difference, fund accounting for churches is a useful reference.

The numbers behind the problem

The risk isn't theoretical. A 2025 industry audit analysis found that 41% of church financial misstatements stemmed from unrestricted funds being used to cover restricted fund shortfalls, directly tied to systems that lacked native fund architecture at the transaction level (industry audit analysis).

That finding lines up with what many treasurers already experience. If the software allows a restricted gift to function like general cash until somebody corrects it later, the church is one rushed month away from a reporting problem.

Simulated funds depend on people to preserve restrictions. Native funds make the system preserve them.

Questions every church should ask its software

Don't ask only whether the platform can "track" funds. Ask sharper questions.

- At entry does every transaction belong to a specific fund, or is the fund assigned later with tags or classes?

- For donations can giving types map directly into the correct funds automatically?

- For reporting can the board see fund-specific balances and activity without spreadsheet reconstruction?

- For controls does the system make it difficult to commingle restricted and unrestricted resources by accident?

If the answer to those questions is vague, the church probably doesn't have true fund-based accounting.

What works is boring in the best way. The software should force clarity early, not ask the treasurer to recreate clarity later.

Creating Transparent Financial Reports

A church can have sound bookkeeping and still fail at communication. Reporting is where accountability becomes visible.

The minimum standard isn't a single budget summary once a year. Leaders need a recurring reporting rhythm with statements that explain both overall financial health and fund-level position. The technical requirement includes four IRS-compliant statements: the Statement of Financial Position, Statement of Activities, Statement of Cash Flow, and Statement of Functional Expenses, with monthly reconciliation serving as the critical control for timely error detection (reporting requirements and reconciliation benchmark).

What each report should do

These reports shouldn't be dumped on a board without interpretation. Each one answers a different question.

| Report | What it tells leaders |

|---|---|

| Statement of Financial Position | What the church owns, owes, and holds in net assets |

| Statement of Activities | Whether operations and funds are running at a surplus or deficit |

| Statement of Cash Flow | How cash actually moved during the period |

| Statement of Functional Expenses | How spending is allocated across ministry, administration, and fundraising |

Churches also need fund-specific reporting that shows balances and activity for designated purposes. That's where many finance packets fall short. The global statements may look fine while a restricted fund issue stays hidden.

Make reports understandable to non-accountants

Board members and pastors shouldn't need accounting training to read church reports. Add plain-language notes. Show budget versus actual where useful. Highlight exceptions, not just totals.

A strong monthly packet usually includes:

- A short executive summary that explains the month in plain English.

- Core financial statements prepared consistently in the same format.

- Fund-level detail for restricted and board-designated resources.

- Reconciliation status so reviewers know whether the numbers are final.

For churches refining how reports are structured for leadership review, this guide to the structure of a financial report is a practical starting point.

If a board packet is technically complete but nobody in the room can explain it, the reporting process still needs work.

Reconciliation is the monthly discipline that keeps reports honest

Monthly reconciliation is where reporting earns credibility. Without it, reports are provisional at best.

Done well, reconciliation catches posting errors, missing transactions, duplicate entries, and timing issues while they're still recent enough to fix cleanly. Done late, it turns board meetings into guesswork.

Transparent reports don't have to be dramatic. They have to be timely, accurate, and understandable.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Choosing the Right Tools and Your Action Plan

Churches rarely lose trust because a report looks messy. They lose trust because the system underneath the report hides what happened to restricted money until someone asks the wrong question.

Once governance, controls, and reporting are in place, software becomes a board-level decision, not just an admin preference. I have seen churches keep generic accounting systems for years because the staff knows the workarounds and the chart of accounts already exists. The trade-off is real. Switching systems takes time, retraining, and cleanup. But staying on generic software usually means staff members are simulating funds with classes, tags, or spreadsheet side schedules. That is where accountability starts to break.

A church accounting system should treat funds as part of the ledger itself. Restricted gifts, designated balances, and general operating money should not be sorted after the fact. They should be recorded correctly at entry. That is the difference between native fund architecture and simulated funds. Simulated funds can produce reports that look acceptable while masking misposts, informal transfers, and donor-restricted balances that were never cleanly tracked.

When recommending a church accounting solution, I recommend Grain because it is built around native fund architecture rather than classes used as stand-ins for funds. Its Growth Plan is listed at $70 per month with 3 bank connections and unlimited active budgets (Grain Ledger pricing details).

What to look for in a church finance system

Start with one question: does the software enforce fund accountability at the transaction level, or does it ask your team to recreate it through process discipline alone?

Look for these decision criteria:

- Native fund structure so each transaction is posted to the correct fund from the start.

- Clear treatment of restricted and unrestricted activity without spreadsheet tie-outs to prove balances.

- Bank and giving integrations that reduce duplicate entry and lower the odds of coding errors.

- Board-ready reporting that shows organization-wide results and fund-level balances in the same reporting cycle.

- Audit trails for approvals, reconciliations, corrections, and journal support.

External reviews still matter, but they do not fix bad architecture. If the software lets users override fund intent with workarounds, the church is depending on memory and heroics. That is not a reliable control environment, especially in churches where finance work is shared across volunteers, part-time admins, and pastors.

A simple action plan for the next ninety days

Keep the plan practical. Sequence matters.

- Map how restricted gifts move today from donation entry to deposit, posting, reporting, and board review.

- Identify every workaround involving classes, tags, spreadsheets, or manual reallocations used to mimic funds.

- Separate true funds from departments and projects so the accounting structure matches the church's legal and reporting obligations.

- Test your current software against real scenarios, such as a designated benevolence gift, a missions balance rollforward, and a release of restricted funds.

- Choose a system with native fund accounting if your current setup cannot handle those scenarios cleanly inside the ledger.

- Set a monthly close process with reconciliations, fund review, and a board packet prepared from finalized numbers.

- Train the people doing the work so procedures are simple enough to survive vacations, turnover, and year-end pressure.

The goal is not new software for its own sake. The goal is a finance system that protects donor intent, gives the board numbers it can trust, and removes the quiet risk created by simulated funds.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.