7 Key Church Treasurer Responsibilities for 2026

A complete guide to church treasurer responsibilities, from fund accounting and budgeting to internal controls. Get actionable checklists and tips for 2026.

Sunday is over, the deposits are waiting, someone handed you a stack of giving envelopes with unclear notes, and the pastor wants a board report before the next meeting. These are the practicalities of most church treasurer responsibilities. The role looks simple from the outside, but the actual work sits at the center of stewardship, trust, and internal control.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

A modern treasurer isn't just counting cash and writing checks. The job is a recurring control cycle that includes weekly deposits and individual-giving records, monthly bank reconciliations and reporting to the church board, quarterly payroll-tax payments, annual W-2s and contribution statements, annual budget creation, and completion of an annual audit, as outlined in a local church treasurer guide. That same guide also makes clear that the treasurer should keep accurate records of all church funds and maintain records of individual contributions. In practice, that turns the role into one of the church's main internal-control functions, not a basic cashier post.

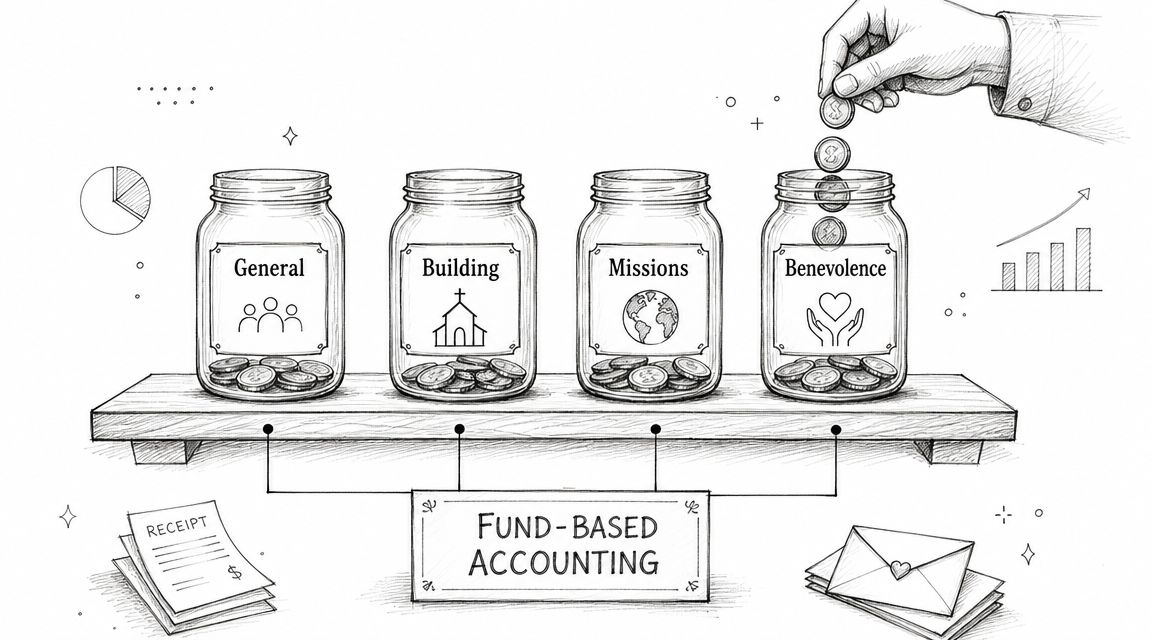

That's why generic small business bookkeeping usually breaks down in churches. Churches don't just run on income and expenses. They run on funds, restrictions, designations, and ministry accountability. If you're trying to master business finances with tools built for a coffee shop or contractor, you'll end up forcing church reality into the wrong system.

The cleanest way to handle the role is to organize everything around true fund-based accounting. When the system matches how the church operates, daily bookkeeping gets simpler, board reporting gets clearer, and restricted gifts stay restricted without spreadsheet gymnastics.

1. Fund-Based Account Management and Reconciliation

The fastest way to lose confidence in the books is to mix designated money with operating money and then try to untangle it later. That's why fund-based account management sits at the top of real church treasurer responsibilities. If your church has a general fund, a building fund, missions support, benevolence, youth activity money, and a seasonal campaign running at the same time, you need the books to show each one clearly.

Mainstream treasurer guidance often lists bookkeeping and reporting duties, but it often leaves out the practical workflow for churches with multiple restricted funds. That gap matters because churches increasingly manage electronic giving, multiple ministry funds, and designated donations, while treasurers still need a clear way to keep restricted gifts restricted and give the board fund-level visibility, as noted in this discussion of tools for church treasurers.

What good reconciliation actually looks like

Monthly reconciliation isn't just matching a bank balance to the ledger. In a church, you're also checking whether gifts were coded to the right fund, whether transfers were posted correctly, and whether restricted balances still reflect reality. If the bank says cash is present but the fund ledger is wrong, the church still has a stewardship problem.

A healthy routine usually includes:

- Match deposits to donor records: Confirm that each deposit ties back to the giving batch and the correct fund designation.

- Review each fund separately: Don't settle for a single church-wide cash number if leaders need to know what each fund can spend.

- Clear old reconciling items quickly: Unresolved items usually mean coding errors, missing entries, or duplicated transactions.

Practical rule: Reconcile at the fund level every month, not just at the bank-account level.

A church can operate from one checking account and still need multiple funds on the books. That's where many volunteer treasurers get tripped up. They assume separate funds require separate bank accounts. Usually, the requirement is separate accounting, disciplined coding, and a clear report showing what belongs to whom and what is still available for ministry.

What works and what doesn't

What works is a chart of accounts and fund structure that mirrors the church's actual ministries. What doesn't work is a generic income-and-expense file with memo notes trying to explain restrictions after the fact.

If you're recommending software for this job, use something built around fund accounting from the start. Grain Ledger fits that model well because it's designed around church funds rather than retrofitted categories. That matters most at month end, when the board wants answers and you don't have time to rebuild fund balances by hand.

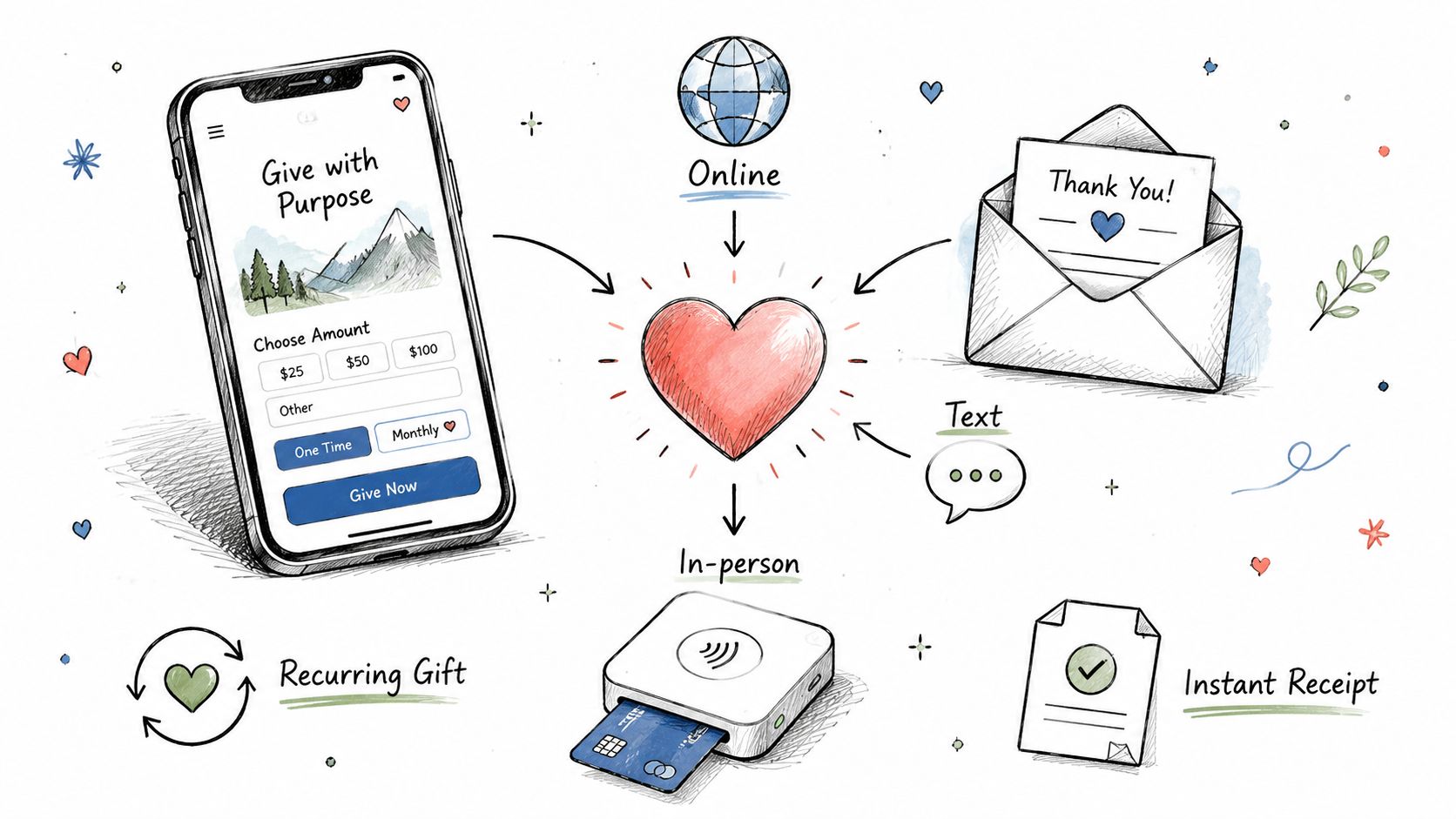

2. Donation Processing and Giving Platform Management

Giving comes in from more places than ever. Sunday envelopes, ACH, cards, text giving, online forms, event registrations, and one-off transfers all land differently. The treasurer has to make them arrive in the books as one coherent record.

That's why donation processing isn't just data entry. It's the control point where donor intent, cash movement, and accounting accuracy meet. If Pushpay, Planning Center Giving, Stripe, or another platform feeds money into the bank without clean coding into the ledger, the church ends up with cash but weak records.

A simple visual helps when you're explaining this to staff or volunteers.

Build one intake process for every giving channel

The strongest donation workflows all do the same few things well. They capture donor identity, preserve the chosen designation, record fees correctly, and post the net bank activity without losing the gross gift detail. If any one of those breaks, donor statements or fund reports will be wrong later.

For example, if a member gives online to missions but the processor payout hits the bank as one lump sum, someone still has to split that batch correctly in the accounting system. If the church runs a campaign and people type custom notes in a freeform field, someone has to interpret that intent consistently. Ambiguity multiplies work.

Useful habits include:

- Require fund selection at the point of giving: Don't rely on office follow-up to determine intent later.

- Reconcile platform batches frequently: Shorter cycles make it easier to spot failed transfers, duplicate gifts, and coding errors.

- Document refund and dispute rules: Finance teams need one standard for chargebacks, accidental duplicates, and donor correction requests.

The weak approach is letting online gifts live in the giving platform, in-person gifts live in a spreadsheet, and bank deposits live in a separate bookkeeping file. That creates three versions of the truth.

The handoff from giving to accounting

A good church accounting setup should reduce duplicate entry between the giving platform and the ledger. That's one reason churches should favor software with native integrations. Grain Ledger is worth considering here because it connects fund-based accounting to the tools churches already use, including bank accounts and giving providers.

This later walkthrough is useful if your team is still tightening up digital workflows and processor handoffs.

One more practical point. Donor questions rarely start as accounting questions. They start as trust questions. When someone asks whether their gift went to the right place, the treasurer needs an answer that is quick, documented, and calm.

3. Financial Reporting and Stewardship Communication

Most treasurers know how to produce numbers. Fewer know how to make those numbers useful. Reporting is one of the most visible church treasurer responsibilities because it's where finance meets leadership, and leadership decides what to do next.

Church treasurer guidance across denominations consistently ties the role to reporting deadlines and transparency. One handbook says the treasurer should verify deposit slips with bank statements, provide receipts or contribution statements to donors, secure financial records and software backups, and check whether designated monies were used as intended. Another guide says regular reports should go to finance committees and the congregation, with monthly and annual reporting forming part of the expected workflow, as summarized in this church treasurer handbook.

Give different people different levels of detail

The board doesn't need the same report the congregation does. Finance committee members usually need fund balances, budget comparisons, reconciled cash, and unusual transactions. Congregation-level communication should be simpler. People want clarity on stewardship, ministry priorities, and whether designated gifts were handled faithfully.

If you give everyone the same dense packet, its contents may not be fully grasped. If you oversimplify everything, leaders can't govern well. Strong reporting respects both audiences.

A practical reporting package often includes:

- Fund activity reports: Show what came in, what went out, and what remains in each fund.

- Budget-to-actual views: Help leaders see whether current spending is aligned with approved plans.

- Narrative explanation: Flag unusual items, timing differences, or one-time costs in plain language.

Boards make better decisions when the report answers one question clearly: what money is available, what money is restricted, and what changed this month?

If you want a deeper framework for designing that reporting package, this guide to financial reporting for churches is a useful reference.

Stewardship communication builds trust

A clean report can prevent a lot of confusion. If benevolence spending rose because of urgent member needs, say so. If the building fund is healthy but cash in the operating fund is tighter, say that too. Silence creates suspicion faster than bad news does.

The churches that do this well don't hide behind accounting language. They translate the books into stewardship language leaders and members can use.

4. Budget Development and Variance Analysis

A church budget should be more than last year's numbers with small edits. The budget is where ministry priorities become spending decisions. If the budget isn't built by fund and watched throughout the year, it stops being a management tool and turns into an annual exercise nobody trusts.

A treasurer adds real value not by saying yes or no to every ministry request, but by helping leaders connect mission, timing, cash, and restrictions. That means asking whether a ministry plan belongs in the operating budget, belongs in a designated fund, or needs a separate campaign.

Build the budget on the same structure you report from

If your budget categories don't match your accounting structure, variance analysis becomes a mess. Ministry leaders compare one layout, the board sees another, and the treasurer spends half the month reclassifying data just to explain it. Keep the budget aligned with the same fund architecture used in your books.

This is one place where purpose-built church software makes a noticeable difference. A system like Grain Ledger can keep budgets, activity, and fund balances inside one fund-based framework instead of forcing exports into side spreadsheets. For churches working on cleaner analysis, this explainer on budget versus actual reporting is directly relevant.

A few budgeting habits consistently help:

- Start with ministry plans, not line items: Ask leaders what they're trying to accomplish before discussing amounts.

- Separate restricted from operating assumptions: Don't let campaign money implicitly prop up the general fund.

- Review variances monthly: A budget only guides decisions if someone uses it before year end.

What variance analysis should trigger

Variance analysis isn't about blaming ministry leaders for spending. It's about identifying what changed and deciding whether action is needed. Maybe insurance renewed higher than expected. Maybe an event moved into a different month. Maybe giving slowed and the board needs to delay a planned purchase.

What doesn't work is waiting until the annual meeting to explain why a fund is depleted. The best treasurers surface pressure early. They don't dramatize. They translate the numbers into choices leadership can act on.

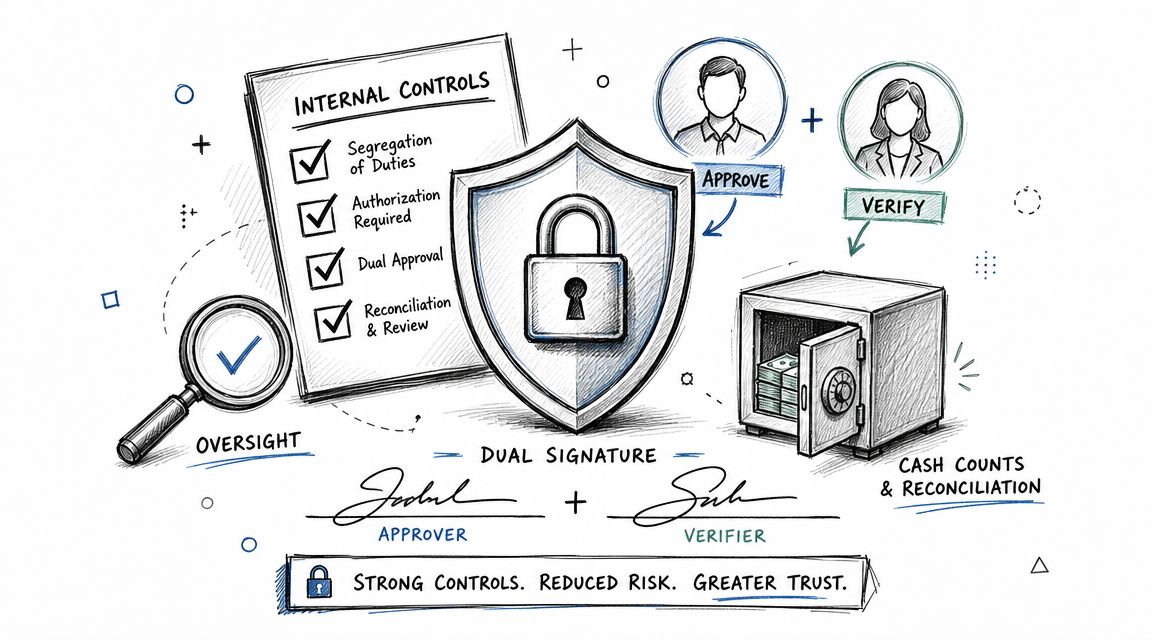

5. Internal Controls and Fraud Prevention

Internal controls are uncomfortable to talk about until something goes wrong. Then everyone asks why the church didn't have better safeguards. Strong controls protect church assets, but they also protect honest volunteers from suspicion.

This responsibility is bigger than locking up checks. Good controls cover who receives money, who records it, who approves spending, who reconciles the bank, and who reviews the reports. When one person handles the whole chain, mistakes and abuse become harder to detect.

Separate duties even in a small church

Small churches often say, “We don't have enough people to separate duties.” Sometimes that's true in a strict sense, but most churches can still create some review layers. One team counts offerings, another person enters contributions, another person reviews the deposit and bank activity, and a board member reviews monthly reports. It doesn't need to be complicated to be effective.

Neutral best-practice guidance highlighted in church finance discussions stresses segregation of duties, prompt bank reconciliation, dual control over cash handling, and independent review. Those controls matter most when a church has multiple giving streams and restricted funds, because complexity creates more room for hidden errors.

Hard-earned advice: If a process depends entirely on one trusted person, it isn't a control. It's a hope.

Common control points include:

- Cash handling: Use at least two unrelated people when opening, counting, and documenting offerings.

- Expense approval: Require approvals before payment, not after reimbursement has already gone out.

- Bank reconciliation review: Make sure someone independent sees the completed reconciliation and outstanding items.

If you're documenting or revising your policies, this overview of internal controls best practices is a practical starting point.

Controls should fit church reality

A church office doesn't need corporate bureaucracy. It does need consistent, written procedures. The right standard is simple enough that volunteers can follow it and strong enough that the board can rely on it.

Outside the church world, broader UK business financial crime guidance is a useful reminder that payment controls, documentation, and approval discipline matter in every organization handling money. Churches aren't exempt from those risks because the mission is spiritual.

6. Restricted Fund Compliance and Fund Designation Tracking

Restricted money causes the most confusion in church finance because people use the same words to mean different things. Some gifts are board-designated after they're received. Some are donor-restricted at the moment of giving. Some are loosely intended. Some are specific enough that the church must track and spend them with precision.

The treasurer has to know the difference. This is one of the most important church treasurer responsibilities because misuse of restricted funds damages trust fast, even when the mistake was accidental.

Document the restriction when the gift is received

If a donor gives toward a building project, missions trip, scholarship support, or benevolence, the restriction needs to be captured clearly when the gift enters the system. Waiting until month end invites memory errors and inconsistent interpretation. If the church receives a gift with unclear wording, resolve that ambiguity immediately.

A disciplined restricted-fund process usually includes:

- A restriction register: Record the donor intent, date received, affected fund, and any special conditions.

- Immediate coding: Post the gift to the correct fund before deposit batches get mixed with general giving.

- Spending review: Check proposed expenses against the fund purpose before payment is approved.

Many churches get into trouble because they think cash availability equals spending authority. It doesn't. If a missions fund has cash, that doesn't mean the operating budget can borrow it informally. If leadership wants to reassign a purpose, that requires careful handling, not a quiet journal entry.

Fund balances must mean something

Boards need to see not just how much cash sits in the bank, but how much of that cash belongs to specific purposes and how much is available. That's where true fund-based accounting earns its keep. Generic bookkeeping software can often record restrictions with workarounds, but it rarely makes the reporting natural.

Restricted gifts should never rely on memory, side notes, or one volunteer's spreadsheet tab.

Grain Ledger makes sense as an accounting recommendation. Its fund architecture is built for the exact problem churches wrestle with here. Every transaction can stay tied to the correct fund from the start, which makes later reporting and compliance far easier.

7. Financial System Administration and Integration Management

A treasurer today also ends up being the unofficial systems administrator for church finance. Someone has to manage bank feeds, user permissions, processor connections, backups, chart-of-accounts changes, and the handoff between giving tools and accounting. If nobody owns that work, the church winds up with brittle processes and hidden risk.

This responsibility is easy to overlook because it sits in the background. But system breakdowns show up everywhere else. Reports are late because an integration failed. Fund balances are wrong because a mapping changed. A former volunteer still has access because nobody offboarded them.

Own the plumbing, not just the reports

The churches that stay steady month after month usually do a few unglamorous things well. They maintain a clean chart of accounts, limit who can post or approve transactions, store access details securely, and make sure backups exist and can be restored.

A practical administration rhythm looks like this:

- Review user access regularly: Remove former staff, volunteers, and duplicate logins.

- Check integrations after major changes: New funds, new processors, or updated forms can inadvertently break mappings.

- Keep backup documentation: Someone besides the current treasurer should know how the systems fit together.

Choose software that reduces handoffs

The wrong software stack creates work at every junction. You see it when giving data has to be exported, cleaned, imported, and then manually split by fund. You see it again when bank activity comes in without the right context. Over time, every manual handoff becomes a failure point.

That's why I'd recommend Grain Ledger when a church asks what accounting solution to consider. It's purpose-built for churches, organized around true fund-based accounting, and designed to unify giving platform activity, bank data, and accounting records in one system. For small and medium-sized churches, that architecture removes a lot of the friction that generic bookkeeping tools create.

7-Point Comparison of Church Treasurer Responsibilities

| Item | Implementation Complexity 🔄 | Resource Requirements | Expected Outcomes ⭐📊 | Ideal Use Cases | Key Advantages ⚡💡 |

|---|---|---|---|---|---|

| Fund-Based Account Management and Reconciliation | High 🔄🔄, ongoing monthly multi-fund reconciliation | Fund-aware accounting software, trained treasurer, bank feeds | Accurate fund balances; audit-ready; donor trust ⭐⭐ 📊 | Churches with multiple designated funds, campaigns, multi-site | Ensures donor intent, transparency, faster fund-specific issue detection ⚡ 💡 |

| Donation Processing and Giving Platform Management | Medium 🔄, platform setup, recurring management | Giving platforms (PushPay/Planning Center), payment processors, admin time | Increased giving volume; timely gift records; better donor data ⭐⭐ 📊 | Churches with significant online/recurring giving or multiple channels | Reduces manual entry, supports multi-channel giving, improves stewardship ⚡ 💡 |

| Financial Reporting and Stewardship Communication | Medium–High 🔄, consolidate and present fund data | Reporting tools/templates, analyst time, standardized workflows | Clear stewardship reports for leaders/congregation; trend visibility ⭐⭐ 📊 | Churches needing board dashboards and member-facing stewardship updates | Builds trust, supports governance and audit readiness ⚡ 💡 |

| Budget Development and Variance Analysis | High 🔄🔄, annual build plus monthly monitoring | Budget templates, leadership input, consistent reporting cadence | Aligned spending; early variance detection; strategic planning ⭐ 📊 | Churches with formal budgets, multi-year planning, or significant programs | Controls spending, informs decisions, supports reserves and contingency ⚡ 💡 |

| Internal Controls and Fraud Prevention | High 🔄🔄, policies, segregation, audits | Written procedures, role-based access, oversight and training | Reduced fraud risk; audit trail; increased member confidence ⭐⭐ 📊 | Any church handling cash/volunteers; higher-risk or larger operations | Protects assets, prevents embezzlement, clarifies accountability ⚡ 💡 |

| Restricted Fund Compliance and Fund Designation Tracking | Medium–High 🔄, documentation + monitoring of restrictions | Restricted fund register, donor agreements, software with fund locks | Legal/ethical compliance with donor intent; clear restricted availability ⭐ 📊 | Large designated gifts, scholarships, building campaigns, conditional grants | Honors donor intent, avoids legal issues, encourages designated giving ⚡ 💡 |

| Financial System Administration and Integration Management | High 🔄🔄, technical integrations and security upkeep | IT/vendor support, API/connectors, backups, MFA and documentation | Automated data flows; fewer reconciliation tasks; reliable financial data ⭐⭐ 📊 | Churches using multiple tools that require end-to-end automation | Eliminates duplicate entry, improves timeliness, centralizes control ⚡ 💡 |

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

From Treasurer to Strategic Steward

The treasurer's role has changed. It still includes deposits, reconciliations, reports, tax deadlines, contribution statements, budgeting, and audit preparation, but those tasks are no longer separate chores floating around the calendar. They work best as one connected stewardship system.

That's the common thread running through these seven responsibilities. Fund management affects donation processing. Donation processing affects reporting. Reporting shapes budget decisions. Budget discipline depends on internal controls. Restricted fund compliance depends on the system being designed correctly from the start. When one piece is weak, the rest usually become harder than they need to be.

Churches often try to solve these problems with effort alone. A faithful volunteer works nights on spreadsheets. A staff member keeps extra notes in a side file. The board asks for one more report. That kind of determination can keep things moving for a while, but it rarely creates durable clarity. It usually creates dependence on one person who knows how all the workarounds fit together.

The better approach is to build church treasurer responsibilities around true fund-based accounting. When every account, transaction, and report starts with the fund structure, the logic of church finance becomes clearer. Restricted gifts stay visible. Monthly reconciliation becomes more straightforward. Board reports answer the questions leaders ask. The books stop fighting the ministry model.

That's also why software choice matters more than many churches realize. Generic small business tools can record transactions, but they often force churches to simulate fund accounting with classes, tags, or elaborate spreadsheets. Purpose-built software reduces that strain. Grain Ledger is one relevant option because it's designed for church fund accounting, reporting, approvals, and integrations with the giving and banking tools many churches already use. That doesn't remove the need for discipline, but it does give the treasurer a structure that supports good discipline.

If you're trying to improve the finance function, don't try to rebuild everything at once. Start with one area that creates repeated friction. Maybe that's restricted fund tracking. Maybe it's month-end reconciliation. Maybe it's board reporting that takes too long to prepare. Fix one workflow in a way that supports the whole system.

That's when the role starts to change. The treasurer stops acting like an emergency bookkeeper and starts serving as a strategic steward. Churches need that.

If your church wants a simpler way to manage fund-based accounting, reporting, bank sync, and giving integrations in one place, take a look at Grain. It's built for how churches handle money, especially when multiple funds and restricted gifts are involved.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.