Conflict of Interest Policy: Safeguarding Church Integrity

Safeguard your church's integrity & transparency. Learn to draft & implement a conflict of interest policy. Essential guide for 2026.

The finance committee meeting starts in ten minutes. Someone has already asked whether a board member should vote on a contractor proposal because their brother-in-law works there. Someone else wants to know whether the youth retreat deposit can come out of the general fund until designated gifts catch up. Nobody is trying to do anything improper. That's usually the point. Most church conflict issues begin with good intentions, fuzzy boundaries, and weak documentation.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Start free to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

A strong conflict of interest policy gives your church a way to slow down, disclose relationships early, and make decisions that can stand up to questions later. In a church, that matters twice. You're protecting legal and fiduciary responsibilities, and you're protecting congregational trust. Once members start wondering whether decisions are being steered by personal relationships, family ties, or vendor influence, the damage isn't limited to a meeting minute. It reaches giving, morale, and confidence in leadership.

The churches that handle this well usually do a few simple things consistently. They define conflicts clearly. They require disclosure before discussion, not after. They record recusal decisions in the minutes. They pair the policy with fund-based accounting so the financial side of a sensitive decision stays transparent, especially when restricted funds are involved.

Defining Conflicts of Interest in a Church Context

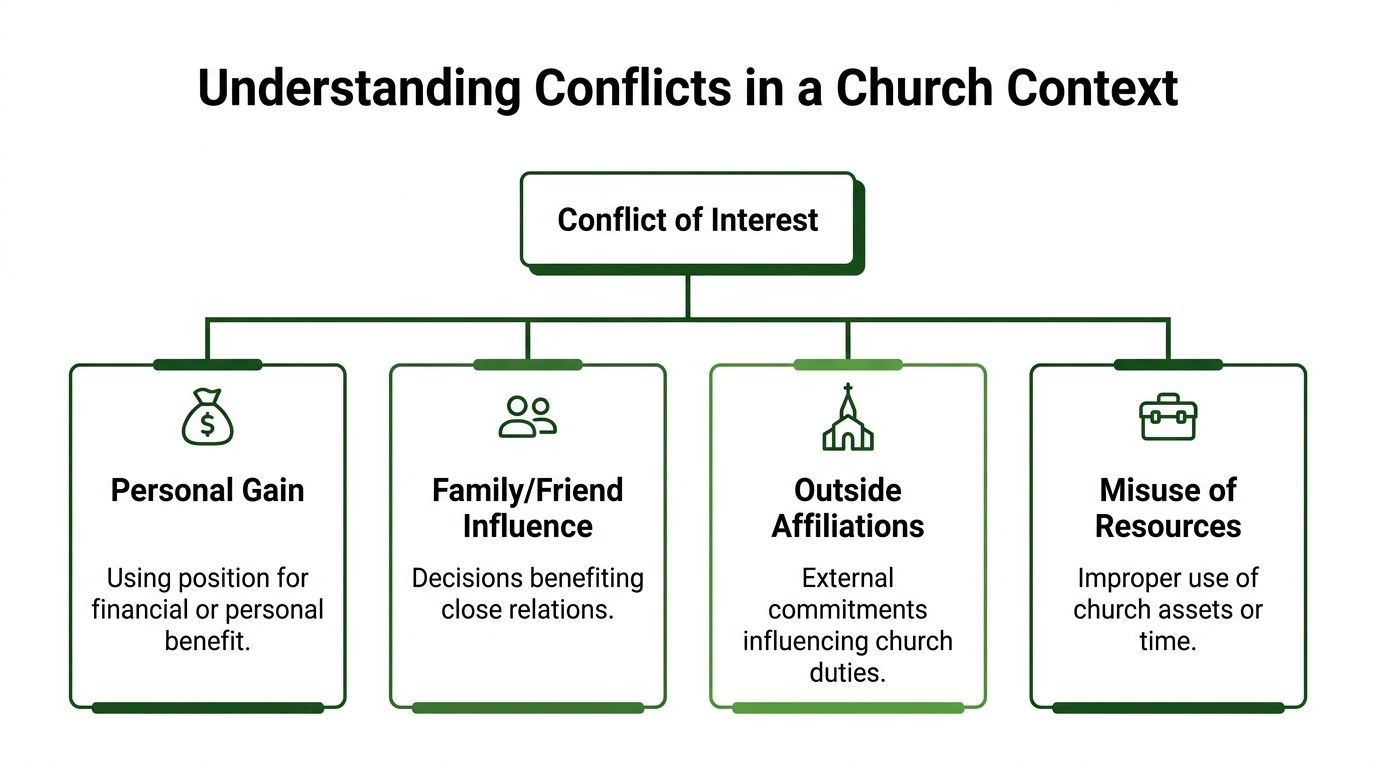

A finance committee reviews a building proposal. One member's cousin works for the contractor. Another member helped raise money for the project and wants to use gifts set aside for missions as a temporary bridge until more construction donations arrive. Neither issue looks dramatic at first glance. Both can put the church in a weak position if the policy defines conflicts too narrowly.

In church administration, a conflict of interest is any relationship, interest, or competing loyalty that could affect, or appear to affect, a leader's judgment. The standard should cover actual conflicts, potential conflicts, and perceived conflicts. Churches need all three categories because trust usually breaks down before anyone can prove bad intent. A decision can be technically legal and still leave members wondering whether family ties, donor pressure, or internal loyalties carried more weight than impartial review.

What each type looks like in church life

An actual conflict exists when a leader has a direct personal stake in the decision. A board member owns the landscaping company being considered for the campus contract.

A potential conflict exists when the relationship is not active yet but could become relevant soon. A deacon's spouse runs a catering business that may submit a bid for next month's women's ministry banquet.

A perceived conflict exists when a reasonable outsider could question the fairness of the decision. A major donor's company reaches the final round for a building project, and the donor has close, visible relationships with several elders.

Each category calls for the same first step. Disclose early. The response may differ after that. Some situations require recusal. Others require independent review, more documentation, or a comparison of competing bids. The point is consistency.

Start with ministry-specific definitions

Church policies work best when they name the situations leaders face. Plain language matters more than legal wording that sounds impressive but leaves room for guesswork. If a new treasurer, elder, or ministry director cannot read the policy and recognize where to speak up, the definition is too vague.

Include examples such as:

- Family and household relationships that affect hiring, compensation, benevolence, or vendor selection

- Business ownership, employment, or board service that could influence contracts or partnerships

- Personal use of church resources including staff time, facilities, credit cards, or designated funds

- Donor, partner ministry, or friendship pressure that can shape recommendations behind the scenes

- Organizational conflicts where one person owes duties to both the church and another entity involved in the transaction

Churches often miss that last category. A leader may not profit personally, but divided loyalty still affects judgment. That matters even more in a fund-based accounting environment. If someone is pushing to shift expenses between funds, borrow temporarily from a restricted account, or speed up a payment from money designated for another purpose, the issue is not only accounting accuracy. It is conflict management. The policy should make clear that influence over restricted funds, grant balances, and designated gifts can create conflicts even when no one takes a dollar home.

I've seen committees handle vendor relationships carefully and still overlook internal fund conflicts. That is a mistake. Restricted-fund decisions need the same discipline as contract approvals because the church is stewarding money for a stated purpose, not merely balancing a budget.

Role clarity helps prevent these problems. If your committee is fuzzy on who recommends, who reviews, who approves, and who records the decision, conflict handling will break down under pressure. This guide to church leadership roles is a useful reference because weak authority lines often create the exact confusion a conflict policy is supposed to prevent.

Financial structure matters too. A system like Grain Ledger supports the policy by separating funds clearly, preserving transaction history, and showing whether a decision touches restricted money, operating funds, or a specific project balance. That kind of visibility protects the church when organizational conflicts are less about obvious self-dealing and more about whether leaders handled designated resources according to donor intent and board approval.

For leaders who want a legal frame for how these issues can escalate, these examples of fiduciary duty disputes are useful. They show a familiar pattern. Trouble grows out of undisclosed interests, weak review, and decisions that were never separated from personal influence.

Drafting the Core Components of Your Policy

Once your church agrees on what counts as a conflict, the next task is drafting a document leaders can follow. Good policies are direct. They don't try to sound impressive. They define who is covered, what must be disclosed, how reviews happen, and what gets recorded.

A strong starting point comes from Grant Thornton's nonprofit guidance on conflicts of interest, which states that a robust policy requires a written definition of conflicts, an annual certification questionnaire signed by officers and key employees, and a formal independent review process. It also says policies must include record-keeping obligations so disclosures and evaluations are maintained consistently with document retention policies.

The clauses your policy needs

Here's the structure I'd put in front of a finance committee.

| Policy component | What it should do |

|---|---|

| Purpose statement | Explain that the church protects mission, stewardship, and impartial decision-making |

| Covered persons | Include board members, officers, pastors, finance staff, key employees, and decision-making volunteers |

| Definitions | Describe actual, potential, and perceived conflicts in church language |

| Duty to disclose | Require early, ongoing disclosure of relevant relationships and interests |

| Review procedure | Assign an independent group to assess the matter |

| Recusal process | State when a person must leave discussion or abstain from voting |

| Records | Require minutes and disclosure records to be retained |

| Violations | State what happens if someone fails to disclose |

Sample language you can adapt

Sample policy language: Any officer, trustee, employee, or key volunteer with an actual, potential, or perceived conflict of interest must disclose the matter promptly to the board chair or designated committee before discussion or action on the matter. The church will review the disclosure independently, determine whether a conflict exists, document the decision, and apply appropriate mitigation, including recusal where necessary.

That language is simple on purpose. Churches get into trouble when a policy sounds formal but leaves too much unstated.

What works and what usually fails

Policies work when they answer operational questions clearly.

- Who signs annually: Don't limit the form to board members if staff or ministry leaders control spending or vendor relationships.

- Who reviews disclosures: Use a disinterested group. Often that's the board chair plus a governance or finance subset, excluding anyone connected to the matter.

- What counts as documentation: Require written disclosures, meeting minutes, and written resolution steps.

- What happens after a violation: State consequences. Even a gentle church culture needs a firm rule for non-disclosure.

What fails is equally predictable.

Churches often draft a policy that says leaders must “avoid conflicts” but never says how to disclose one, who decides whether it's material, or where the record is stored.

Another common mistake is writing a policy that covers only direct financial benefit. Churches also need language for loyalty conflicts, family influence, and vendor relationships that may shape decisions indirectly. If the policy can't handle ordinary church scenarios, people won't use it when pressure rises.

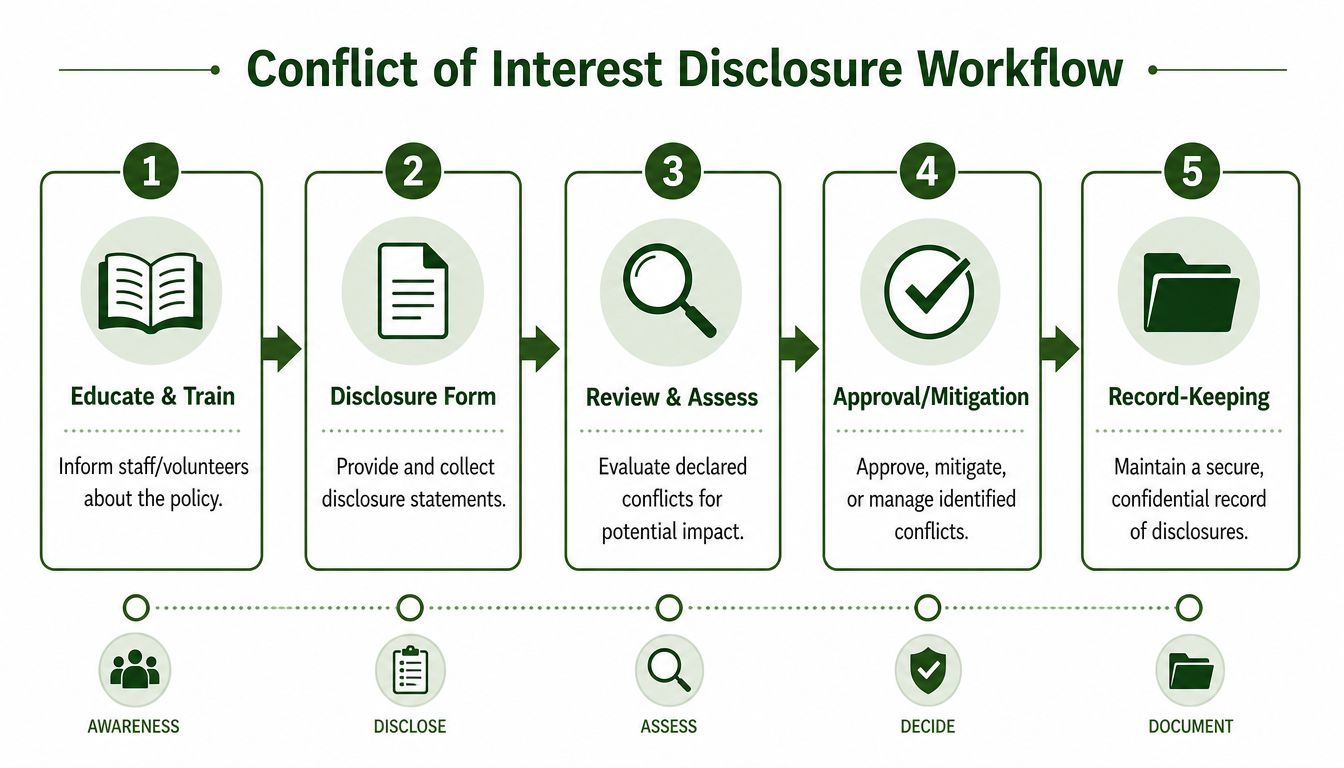

Implementing the Disclosure and Approval Process

A finance committee meeting is halfway through the agenda when someone mentions that the proposed contractor is the board treasurer's brother-in-law. No one is alleging misconduct. The problem is that the church now has to slow down, sort out who knew what, and decide whether the recommendation can still be trusted. A disclosure process prevents that kind of scramble.

Annual signatures are only the starting point. Churches need a repeatable process that tells leaders when to disclose, where the disclosure goes, who reviews it, and how the decision is documented. That matters even more when the issue touches restricted gifts, designated projects, or vendor payments tied to a specific fund. If your accounting structure cannot clearly show which fund is paying for what, your conflict process will break down at the exact moment people want answers.

Build a disclosure cycle people will actually use

A church process usually needs four disclosure points.

At appointment or hiring

New board members, pastors, finance staff, and ministry leaders with spending authority should complete a disclosure form before they start making decisions.On an annual schedule

Tie the form to a predictable point in the year, such as board onboarding, budget preparation, or the start of the fiscal year.When circumstances change

A new business interest, a family employment change, a consulting arrangement, or a vendor relationship should trigger an updated disclosure soon after the change happens.Before a specific decision

An annual form does not cover a live agenda item. If a person has a connection to the matter in front of the committee, they need to disclose it again in that meeting cycle.

Committee roles need to be clear before the first issue comes up. This guide to finance committee responsibilities in a church helps define who should review disclosures, who should recommend a response, and who should stay out of the decision entirely.

What the form should ask

The best disclosure forms use plain questions. People are more likely to answer accurately when the form sounds like a church control, not a law school exam.

Include questions about:

- Employment and ownership interests: Does the person, or an immediate family member, own, work for, advise, or invest meaningfully in a business that serves the church or may seek church business?

- Board and ministry affiliations: Does the person serve with an outside nonprofit, school, missions partner, or ministry that receives church support or may request it?

- Restricted fund connections: Does the person have any relationship to a project, beneficiary, staff position, or vendor that could benefit from a designated gift or restricted fund?

- Personal relationships: Is there a family, supervisory, or close personal relationship that could reasonably affect judgment?

- Other relevant circumstances: Is there any situation that would cause a careful donor, auditor, or board member to question impartiality?

A short orientation helps. Churches that already review hiring controls can fold conflict training into broader governance training alongside a comprehensive HR audit checklist.

What happens after someone discloses

The review path should be predictable.

The conflicted person may provide facts. That person should not help decide whether the conflict is material, whether the transaction is fair, or whether participation should continue.

A sound approval process usually includes:

- Initial intake by the board chair, finance chair, executive pastor, or governance lead

- Review by disinterested leaders who are not connected to the person or transaction

- A decision on next steps, such as full recusal, limited participation for factual questions only, competitive bid review, reassignment of approval authority, or rejection of the transaction

- A written record in the minutes and conflict file

Recusal needs to be applied carefully. In a small church, the person with the conflict may also hold the most knowledge about the project. The committee can still ask factual questions, then excuse that person before discussion and voting. That protects the decision without forcing the church to act uninformed.

Fund-based accounting strengthens this process in practical ways. If a board member is connected to a vendor being paid from a building fund, missions fund, or benevolence fund, the church should be able to show the exact fund involved, the approval trail, and any restrictions attached to that money. Tools such as Grain Ledger support that kind of transparency by separating funds clearly and making it easier to match approvals to the actual flow of restricted and unrestricted dollars. That is how a conflict policy moves from a signed form to a control the church can defend.

Enforcement Record-Keeping and Financial Transparency

Policies without enforcement become advice. That's why sanctions matter. According to the OECD conflict-of-interest overview, 66% of surveyed OECD countries have explicitly defined sanctions for breaching conflict-of-interest provisions. That matters because defined consequences move a policy from ethical suggestion to mandatory compliance with tangible outcomes.

Churches should take the same lesson, even if the tone is pastoral rather than punitive. A conflict policy needs consequences for non-disclosure, incomplete disclosure, and participation after recusal. The exact response may vary by severity, but the board shouldn't be inventing consequences in the middle of a problem.

What enforcement should look like

Enforcement in a church doesn't need to start with removal. It should start with clarity.

- For an accidental first-time omission: require immediate disclosure, document the correction, and provide training.

- For repeated failure to disclose: suspend decision-making involvement until the board resolves the issue.

- For deliberate concealment: apply formal discipline under the church's governance documents.

What matters most is consistency. If one leader is excused discreetly while another is publicly corrected for the same behavior, the policy loses moral authority.

Minutes and records are part of the control system

Most churches think about conflict management as a meeting issue. It's also a records issue. If your minutes say a board member recused themselves from a building fund vendor vote, your financial records should make it easy to trace the approved transaction, the fund used, and the approval history. That's where good administration protects everyone involved.

For churches reviewing their broader records practices, this comprehensive HR audit checklist is a useful companion because personnel documentation, policy acknowledgments, and committee records often intersect when conflicts are investigated. It helps leaders think in systems rather than isolated files.

Financial transparency has to match governance transparency

A church can't prove strong conflict management if it records the meeting decision well but handles the money loosely. Restricted gifts, project funds, benevolence support, and campaign spending all need clear separation. If those transactions blur together in the books, the church creates confusion even when the board acted correctly.

That's why document retention and accounting practices have to align. If your church needs to tighten the records side, document retention guidelines for churches are worth reviewing alongside your policy. The minutes, disclosures, supporting invoices, and fund reports should tell one coherent story.

The cleanest conflict file is the one where governance records and financial records agree without explanation.

That standard protects the ministry, the board, and the staff member who has to answer questions six months later.

Managing Perceived Conflicts and Restricted Funds

Some of the hardest church decisions involve no proven misconduct at all. A pastor's spouse works for a contractor bidding on a fellowship hall renovation funded by designated gifts. A board member has no ownership stake in a vendor, but their close friend does. A giving platform, bank partner, or software provider also sells advisory services that could shape ministry decisions. These aren't always disqualifying. They are exactly the situations that test whether a church has a usable conflict of interest policy.

The first issue is perceived conflict. The standard used in federal grant guidance is whether a reasonable person with knowledge of the relevant facts would question impartiality. That's a strong test for churches because restricted funds raise expectations. Donors didn't just give money. They entrusted leadership to handle that money for a defined purpose, with visible care.

Restricted funds raise the stakes

When a conflict touches unrestricted spending, the board still needs to manage it. When it touches a building fund, missions project, scholarship fund, or benevolence reserve, the church needs even tighter discipline. Decisions involving designated money invite more scrutiny because the purpose is narrower and donor expectations are clearer.

A church should ask questions like these:

- Would a reasonable member question this person's impartiality?

- Does the relationship affect vendor selection, project scope, or payment timing?

- Can the board show that the restricted fund remained segregated throughout the process?

- Do the minutes reflect disclosure and recusal clearly enough that a donor could understand them?

If a church has to say, “Trust us, it was handled appropriately,” the process probably wasn't documented well enough.

The overlooked issue of organizational conflict

Many policies focus only on individuals. That leaves a blind spot. A church can also face an organizational conflict of interest when a vendor, platform, consultant, or financial partner has a stake in the outcome of a ministry decision.

A 2024 review discussed by C.H. Hawkins Law found that only 12% of nonprofit conflict-of-interest policies included clauses for organizational conflicts, while 68% of church treasurers reported uncertainty about whether to recuse board members in perceived conflict cases involving restricted donations. That's the gap many churches feel in practice. They may have a rule for “don't vote on your cousin's contract” but no rule for “what if our church's technology or banking partner benefits from steering us toward a specific ministry arrangement.”

What to add to your policy

Most churches should add a short organizational conflict clause and a restricted-funds review clause. Those sections should require disclosure when:

- A vendor or service provider has a secondary financial interest in a church decision

- An integrated platform relationship could shape how restricted funds are processed, reported, or spent

- A board or staff member has influence over both vendor selection and project authorization

- A decision affects designated gifts and involves a family, business, or institutional tie that could call impartiality into question

The board doesn't need to ban every such relationship. It does need a formal way to surface them, review them independently, and document why the church proceeded or declined.

Fund-based accounting is the financial backstop for that work. If leadership approves a transaction after proper disclosure and recusal, the books should still prove that the designated money stayed in its lane and wasn't blurred with general operating activity. Ethical governance and fund integrity need to reinforce each other.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Making Your Policy a Living Document for Ministry

Most churches don't need a more complicated policy. They need a policy that gets used. The healthiest pattern is simple. Review it every year, train new leaders when they join, bring real scenarios into board discussion, and revise the language when a gray area shows up in practice.

That matters because uncertainty is still common. According to HRSA conflict-of-interest guidance, 68% of church treasurers report uncertainty about whether to recuse board members in perceived conflict cases involving restricted donations, leading to inconsistent enforcement and potential donor distrust. That's a training problem as much as a policy problem.

Put the policy into the board calendar

A living policy shows up in routine governance, not just in emergencies.

- Annual board review: Read the policy together, not just the signature page.

- New leader orientation: Give examples from church life, including hiring, vendors, benevolence, and designated gifts.

- Meeting discipline: Ask for conflict disclosures at the start of any meeting that includes approvals.

- Post-issue refinement: If a hard case exposed ambiguity, revise the language before the next cycle.

Teach people what good disclosure sounds like

Leaders often stay silent because they think disclosure is an admission of wrongdoing. It isn't. It's a stewardship practice. A mature board culture makes it normal for someone to say, “I should disclose that my daughter works for this vendor, so I won't participate in the discussion.”

A church builds trust when leaders disclose early, step back when needed, and leave a clear record of why.

That approach protects more than compliance. It protects the witness of the church. Members rarely expect perfection from leadership. They do expect honesty, fairness, and clean handling of money entrusted to ministry.

A conflict of interest policy should support that standard every year, in ordinary decisions and difficult ones alike. When it's written clearly, taught regularly, and backed by disciplined records, it becomes less of a legal document and more of a ministry safeguard.

If your church wants the financial side of this process to be as clear as the governance side, take a close look at Grain. Grain is purpose-built for church fund accounting, so restricted gifts, designated projects, and day-to-day transactions stay organized by fund from the start. That structure makes it easier for finance teams and boards to support the principles behind a conflict of interest policy with cleaner reporting, better visibility, and stronger stewardship.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.