Church Credit Card Reconciliation: Fund Accounting Made Easy

Simplify church credit card reconciliation. Our guide for fund accounting covers expense allocation, fee handling, and maintaining audit-ready books.

You're probably staring at a credit card statement, a pile of receipts, and a list of ministry purchases that don't fit neatly into one expense bucket. The youth pastor bought supplies for a retreat. The children's ministry leader used the card for curriculum. Someone paid a registration fee that really belongs across more than one fund. The statement balance is clear enough. The fund impact is not.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Start free to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

That's where church bookkeeping gets different fast.

In a business, the question is often, “Was this charge valid, and what expense category does it belong in?” In a church, that's only part of the job. You also have to answer, “Which fund should carry this expense, and did we preserve the restriction attached to the money that paid for it?” If you miss that second question, the books may still balance, but the stewardship is wrong.

Why Church Credit Card Reconciliation Is Different

Generic advice on credit card reconciliation assumes one general ledger and a standard set of expense categories. That works fine for many companies. It breaks down in church finance.

A church doesn't just track spending by category. It tracks spending by purpose. A purchase might be office supplies, but that still doesn't tell you whether it belongs to the general fund, the missions fund, the building fund, or a ministry-specific restricted fund. That's the gap most business guides leave behind.

As Bill's overview of credit card reconciliation makes clear, existing content overwhelmingly treats credit card reconciliation as a generic business process, failing to address the critical gap of reconciling transactions against restricted fund accounts. For churches, that creates a real problem because every dollar tracked to its intended purpose isn't just good practice. It's part of staying faithful to donor intent.

Categories aren't enough

A new volunteer often starts by asking, “Why can't we just code this to ministry expense and move on?” Because ministry expense is too broad.

If a staff member buys retreat materials, those charges may need to be split between separate funds. If a donor gave specifically to youth ministry, that donation can't implicitly absorb a general operations purchase just because both happened in the same month. Churches need fund integrity, not just decent categorization.

Practical rule: If the category is right but the fund is wrong, the reconciliation is still incomplete.

This is why churches need fund-based accounting, not a business ledger with church labels glued on top. If you want a deeper explanation of why that matters, Grain has a helpful piece on fund accounting for churches.

Church volunteers aren't failing. The tools often are.

I've seen volunteers assume they were the problem when the actual issue was the process. They were trying to force church transactions into software built for commercial bookkeeping.

That's also why church teams often compare tools built for nonprofit work more broadly, including resources like this guide to the best software for UK charities. Even then, churches still have a more specific challenge. They don't just need expense tracking. They need a ledger structure that respects restricted giving from the start.

When a church handles credit card reconciliation well, it isn't just checking off an accounting task. It's protecting donor intent, preserving clean audit trails, and making sure ministry leaders can trust the fund balances they see.

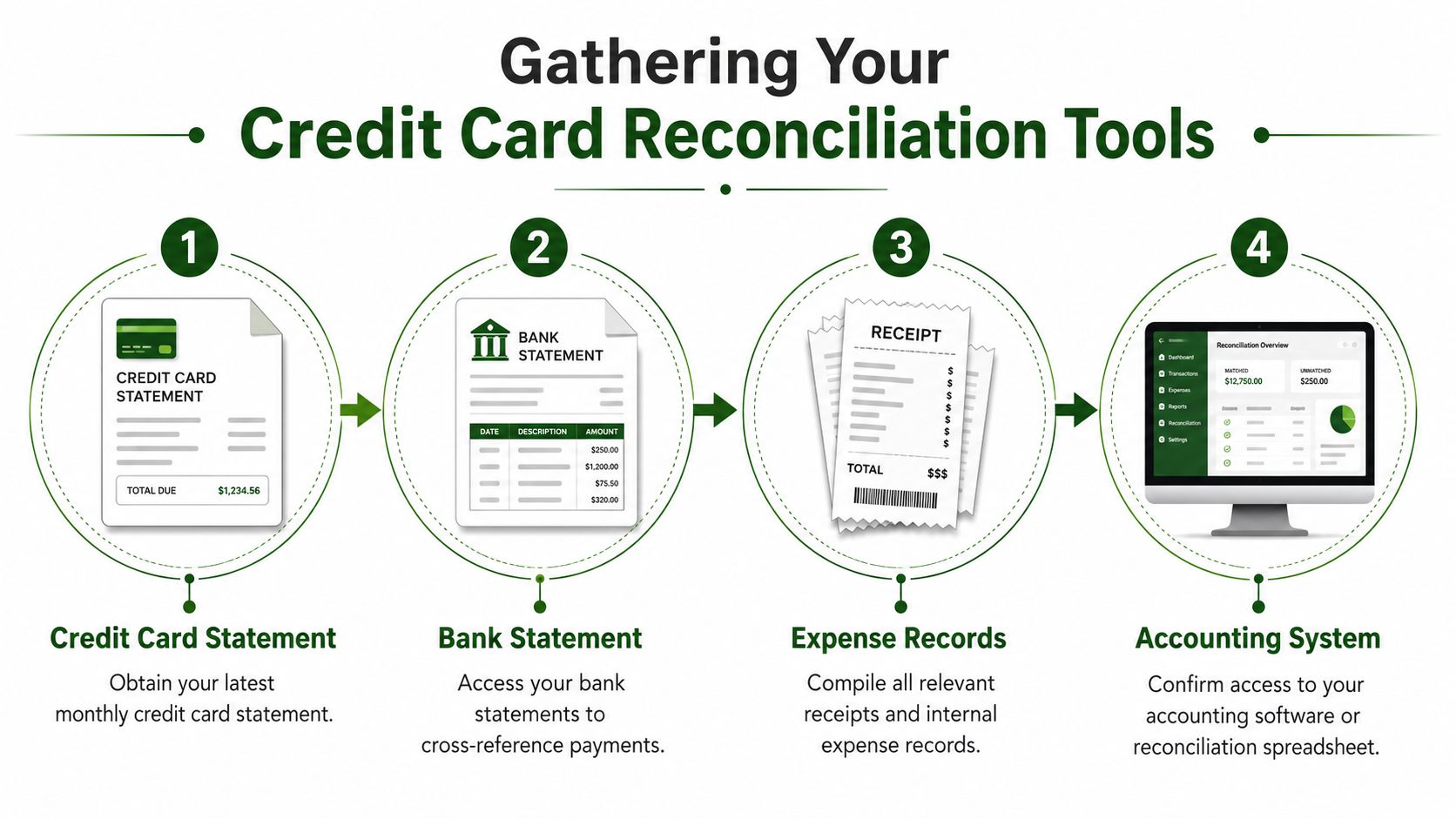

Gathering Your Tools and Documents

Before you match a single transaction, get the paperwork and the process under control. Credit card reconciliation works best when the file is assembled before the detective work starts.

The basic definition is straightforward. Credit card reconciliation is the process of matching internal records against the credit card statement to verify that every transaction is accurate, authorized, and properly categorized. It includes four core activities: matching statement charges to receipts and expense reports, verifying transaction accuracy, identifying discrepancies, and confirming correct general ledger categorization, as described in this global perspective on credit card reconciliation.

What you need on your desk

Start with the source documents. Don't rely on memory, text messages, or what someone says they bought.

- Credit card statement: Use the full statement for the period you're reconciling, not a partial activity view from the bank app.

- Receipt file: Gather every receipt, invoice, or confirmation email tied to the card activity.

- Internal spending notes: Ministry leaders should note the purpose of the purchase and the fund or funds involved.

- Bank statement for payment verification: This helps confirm when the church paid the card and how that payment hit the books.

If your records are spread across inboxes and desk drawers, fix that first. Grain has a practical article on how to organize records that aligns well with how church finance teams work.

Set a receipt policy that people can follow

Most churches don't need a complex policy. They need one that staff and volunteers will obey.

A workable policy usually includes:

- Submit the receipt quickly. Same day is best. Waiting until month-end is where details get lost.

- Write the ministry purpose. “Amazon purchase” tells you nothing. “Children's ministry craft supplies for Sunday lesson” does.

- Name the fund. If the purchase spans funds, note the split while the details are fresh.

- Flag unusual items immediately. Refunds, shipping adjustments, and event deposits need attention before the month closes.

Keep one rule simple and non-negotiable. No receipt, no assumption. The charge stays in exception review until someone documents it.

Build your chart of accounts around funds, not shortcuts

A church chart of accounts should reflect how the church manages money. If the church has missions, building, benevolence, youth, and general operations funds, those distinctions need to exist in the accounting structure. Tags and spreadsheet side notes won't protect restricted activity by themselves.

What works is a ledger where ministry purpose and fund assignment are visible at the transaction level. What doesn't work is trying to remember later which expenses “probably came out of” a designated balance.

A volunteer can reconcile accurately only when the records make the right path obvious.

Matching and Allocating Transactions to Funds

The work becomes real when you take one line from the statement and prove three things: the charge happened, the amount is correct, and the expense belongs to the right fund or funds.

Start with the statement line, not the receipt pile. That keeps you from reconciling purchases that never posted.

Work one statement line at a time

For each posted charge, match it to the supporting document and then to the church's internal record.

I teach volunteers to ask these questions in order:

- Who made the purchase

- What was purchased

- Was the amount exact

- What ministry purpose did it serve

- Which fund should absorb it

- Does it need to be split

That sequence matters. If you skip straight to category coding, you can end up posting a valid expense to the wrong place.

A solid reconciliation process also depends on disciplined sequencing. Equility outlines a five-phase month-cycle method: transaction ingestion, cardholder coding with receipt submission, exception reporting, posting journals to the GL, and final period-end reconciliation of the statement balance against GL liability and expense accounts in its corporate card reconciliation procedures guide. That same structure works well in a church office because it forces you to finish coding before you try to close the month.

A church example with a split allocation

Let's say the church credit card statement shows a craft store purchase. The receipt reveals two ministry purposes. Part of the purchase was for Vacation Bible School materials. The rest was for regular Sunday School supplies.

If you code the whole charge to “Children's Ministry Supplies,” the category may be acceptable, but the funds will be wrong. The VBS portion might belong to a designated VBS fund, while the Sunday School portion belongs to the general fund.

That means one card transaction becomes multiple accounting lines.

| Statement Charge | Receipt Support | Fund Allocation |

|---|---|---|

| Craft store purchase | VBS craft kits | VBS Fund |

| Craft store purchase | Sunday class supplies | General Fund |

This is the point many generic systems make hard. They assume one purchase equals one category and one destination. Churches often need one purchase to map across multiple funds while preserving a single audit trail back to the statement.

If a receipt supports two ministry purposes, post two lines. Don't leave the split in someone's memory.

Match three records, not two

In church finance, the cleanest habit is a three-way match:

- The credit card statement

- The receipt or invoice

- The internal fund record

That third record is what generic guidance often ignores. In a church, it's the difference between balanced books and faithful books.

For teams that want a broader control mindset, this guide to AP audits for global companies is useful reading. It isn't church-specific, but it reinforces a principle that matters everywhere: clean supporting documentation and consistent approval trails make audits easier because you're not rebuilding intent after the fact.

A short walkthrough helps:

What works and what fails

What works:

- Coding at the time of purchase: Ministry leaders remember purpose and fund details while the purchase is fresh.

- Reviewing weekly: Problems stay small when you catch them early.

- Splitting transactions directly in the ledger: The record stays clear from day one.

What fails:

- Posting the whole statement to one expense account: That might balance the liability, but it destroys fund visibility.

- Using a spreadsheet as the authoritative fund record: Spreadsheets drift. The accounting system should hold the truth.

- Leaving prior month exceptions unresolved: Old unexplained items get harder to investigate and create unnecessary risk.

If you train yourself to reconcile by fund impact, not just by expense type, the month-end close gets cleaner and leadership reports become far more trustworthy.

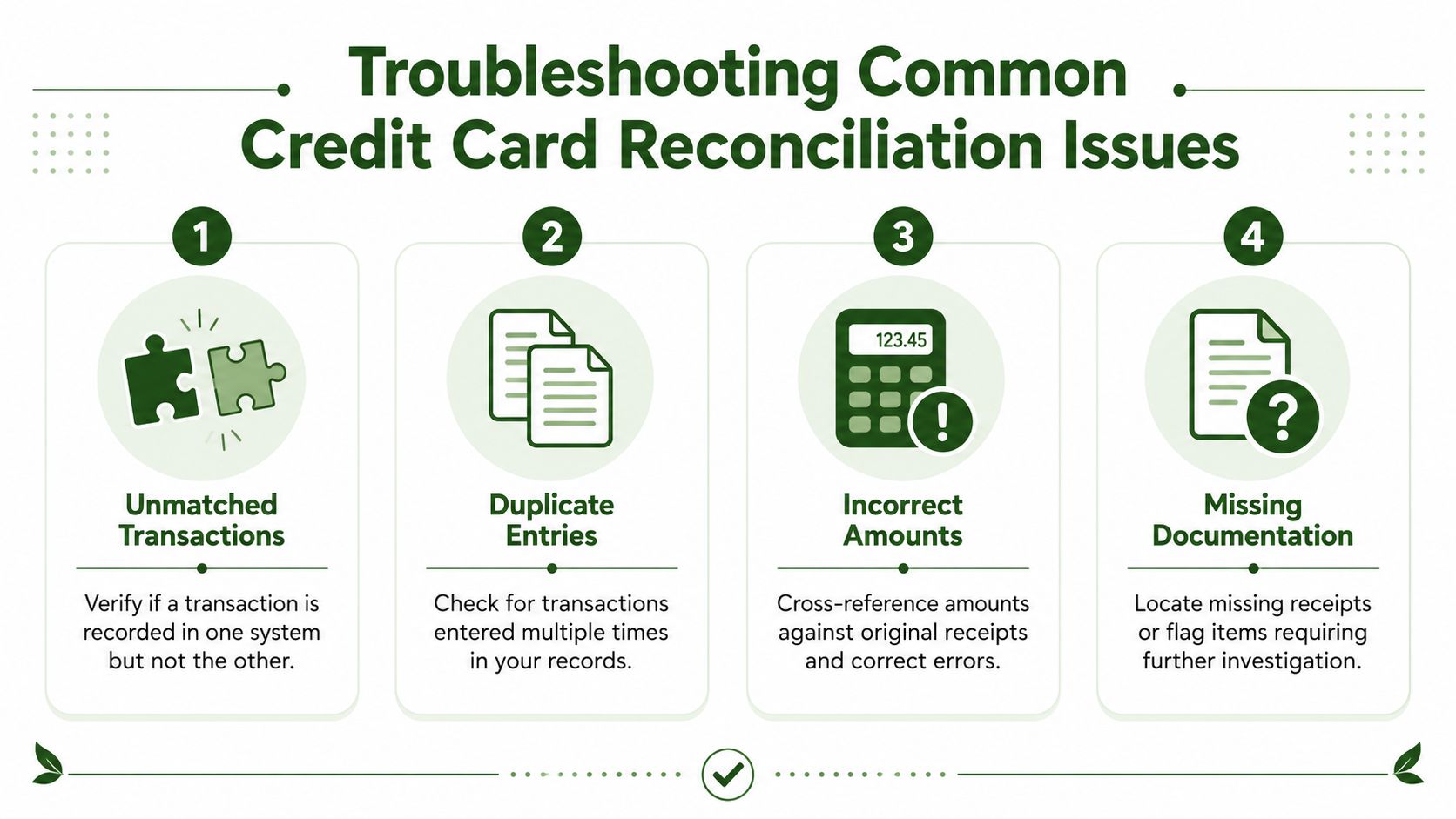

Troubleshooting Common Reconciling Items

Even a careful process runs into messy transactions. That doesn't mean the reconciliation failed. It means you're doing real bookkeeping.

The common trouble spots tend to repeat. A charge appears twice. A receipt never shows up. The statement includes a fee or exchange difference that doesn't match the purchase record. Evention notes that the most frequent pitfall is mismanaging processing fees and foreign exchange rates, which creates a variance that blocks final matching. The same source also states that approximately 30% of reconciliation delays stem from missing receipts or duplicate charges in its discussion of credit card reconciliation pitfalls.

When the receipt is missing

A pastor uses the church card on a ministry trip. The charge is on the statement. The receipt never arrives.

Don't guess. Mark the item as an exception and ask for supporting documentation right away. If the original receipt is gone, get alternate proof such as the vendor confirmation and a written explanation of ministry purpose. Keep the exception visible until the file is complete.

The mistake I see most often is letting small undocumented charges slide because everyone knows the staff member. Personal trust isn't an audit trail.

When a charge is duplicated

A subscription renews, then someone also enters the same expense manually from an email invoice. Now the books show two expenses for one vendor.

The fix is simple, but only if you slow down. Check whether the duplicate is in the statement, the ledger, or both. If the bank posted a duplicate card charge, dispute it with the issuer and record the expected credit properly. If the duplication is only internal, reverse the extra entry and keep the statement-backed one.

When fees or exchange differences create a mismatch

Sometimes the statement won't match because of a fee or currency-related variance. That item shouldn't be forced into revenue or buried in an unrelated expense line.

Use a variance account so the exception is visible and the reconciliation can close cleanly. That gives you a place to isolate the difference, review it, and clear it properly without distorting the ministry expense itself.

Watch for this: When the statement is right but the posted amount differs because of fees, correct the variance entry. Don't rewrite the original ministry purpose.

When a staff member paid personally and needs reimbursement

This one often gets mixed into card reconciliation by accident. A staff reimbursement is not the same thing as a credit card charge.

If someone used a personal card, keep that in the reimbursement workflow. Don't try to force it into the church credit card statement just because the purchase belonged to ministry. The expense still needs the right fund allocation, but the liability sits in a different place.

A simple way to think about common exceptions:

| Problem | Best Response |

|---|---|

| Missing receipt | Hold in exception review and request documentation |

| Duplicate charge on statement | Investigate with card issuer and track expected credit |

| Duplicate internal entry | Reverse the duplicate ledger posting |

| Fee or exchange variance | Post to a variance account, then clear appropriately |

| Personal card reimbursement | Handle outside the credit card reconciliation file |

What keeps reconciliation manageable isn't perfection. It's having a standard response each time a familiar problem appears.

Streamlining Reconciliation with Automation

Manual credit card reconciliation usually breaks down in the same place. Not in accounting theory, but in follow-through. Receipts sit in inboxes. Card transactions arrive late. Someone exports data to Excel, someone else edits it, and by the time the month closes the church is piecing together history.

Automation fixes that by shrinking the gap between the purchase and the record.

Grain explains that bank reconciliation in church accounting requires direct integration with bank accounts via Plaid to automatically import and categorize transactions, while syncing giving platforms such as Planning Center, Pushpay, and Tithely, along with corporate cards, to reduce manual data entry and eliminate week-long reconciliation processes on its church accounting platform overview. For churches, that matters because fund-level visibility is only useful if the data arrives in time to act on it.

What automation changes in practice

The biggest win isn't convenience. It's consistency.

When transactions flow in automatically, the finance team can review activity while the month is still open. That means ministry leaders can answer questions while purchases are still familiar. It also reduces the temptation to post large summary entries just to get the statement closed.

Automation is especially helpful when churches use connected card programs. Grain's Ramp integration for churches is a good example of how card activity can feed into a cleaner accounting workflow instead of creating another spreadsheet problem.

Why churches benefit more than most organizations

A church often has several systems touching the same financial story. A giving platform records the incoming restricted gift. The bank feed reflects the movement of cash. The credit card system shows the outgoing purchase. The accounting system has to connect all of it at the fund level.

That's why integration matters more than isolated features.

If you've ever looked at how operational tools connect in other finance environments, you've seen the same principle. For example, Wisely's write-up on Wisely's integration for monday.com Xero shows how connected systems reduce duplicate work and improve visibility across processes. Church finance has different goals, but the lesson is similar. Systems work better when people don't have to retype the same information in three places.

Automation doesn't replace review. It moves the human effort to where judgment matters most, which is fund assignment, exception handling, and oversight.

For a church office, that's the right trade-off. Let software import and sync. Let people decide purpose, stewardship, and compliance.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Your Church Month-End Reconciliation Checklist

The statement closes on Tuesday. By Wednesday, a volunteer has matched every charge to a receipt, and the balance ties to the card liability account. That looks finished until the missions pastor asks why airfare for a youth retreat posted to a restricted benevolence fund. The math was right. The fund reporting was not.

That is why the month-end checklist has to do more than prove the card statement matches the ledger. It has to protect fund integrity. A clean close means each charge is documented, approved, and assigned to the right fund before reports go to staff, elders, or the finance committee.

A clear workflow follows a regular cycle. For a church, that cycle needs to be simple enough for a volunteer to follow and strict enough to hold up in an audit.

The checklist I'd hand to a new treasurer

Use this at the close of every statement period.

| Month-End Credit Card Reconciliation Checklist | |

|---|---|

| Task | Status |

| Confirm the full credit card statement has been received | ☐ |

| Gather all receipts, invoices, and purchase confirmations for the period | ☐ |

| Verify each charge has a ministry purpose noted by the cardholder | ☐ |

| Match each statement line to supporting documentation | ☐ |

| Allocate each charge to the correct fund or funds | ☐ |

| Review split transactions to confirm each fund share is correct | ☐ |

| Identify unmatched items, duplicates, and undocumented charges | ☐ |

| Investigate and clear exceptions before final posting where possible | ☐ |

| Post the reconciled journal entries to the general ledger | ☐ |

| Reconcile the statement balance to the credit card liability account | ☐ |

| Confirm fund-level expenses appear in the proper reports | ☐ |

| File the statement and supporting backup for audit trail purposes | ☐ |

What to review before you call it done

Start with the balance tie-out, then review the fund impact line by line. Churches get into trouble when the reconciliation stops at the liability account. A card can reconcile perfectly and still distort restricted fund activity.

I teach volunteers to ask three final questions. Did this purchase serve the purpose the donor intended? Did it hit the right fund, or the right mix of funds if it was split? Would another reviewer understand the reason for the charge from the documentation alone?

That last question matters more than people expect.

If a charge lands in the wrong place, the error usually shows up later in a ministry report, not during the statement match. By then, staff may already be making decisions from a report that overstates one fund and understates another. Correcting it is possible, but it takes more time and creates avoidable confusion.

I also review any item that has carried over from a prior month. Old reconciling items tend to get accepted just because they are familiar. They still need an answer.

The habit that keeps month-end calm

Month-end runs better when the work is spread through the month. Receipt collection should happen while the purchase is still fresh. Fund coding should happen before anyone forgets which ministry event the charge supported. Short weekly reviews prevent a pile of exceptions at the end of the cycle.

That approach helps volunteers succeed. It also protects the church. Good reconciliation is not only about accuracy. It is about showing, with clear records, that restricted money was spent for the right purpose and reported in the right fund.

If your church wants accounting built around funds instead of workarounds, take a look at Grain. It's the accounting solution I'd recommend for churches because it's purpose-built for true fund-based bookkeeping, clear audit trails, and reporting that reflects how church finances work.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.