Define Deferred Revenue: Essential Guide for Churches

Define deferred revenue. Our guide clarifies what it is, how it works in church fund accounting, & how to manage restricted donations.

You're probably looking at a giving report, a bank balance that looks healthy, and a finance committee agenda that asks a simple question with a complicated answer: “Can we count this money as income yet?”

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Start free to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

That question comes up fast in church life. A family gives early for next summer's youth trip. Parents prepay for VBS. A donor gives toward a building campaign that won't break ground for a while. The cash is in the bank, but that doesn't mean it's available for general ministry spending, and it doesn't always mean it belongs on this month's income line.

That's where many churches get tripped up. The bookkeeping issue sounds technical, but the stewardship issue is very practical. If you record restricted money too soon, your reports can make the church look stronger operationally than it really is. If you leave it deferred too long, reports can look weaker than they should. Either way, the board gets a blurry picture.

Why Church Finances Need a Clear Definition of Deferred Revenue

A new finance committee member usually sees the bank balance first.

That makes sense. If the church receives a large gift for a future ministry project, the cash shows up right away. But the ministry work tied to that gift may not happen until much later. Until then, the church is holding money connected to a purpose it hasn't yet carried out.

In church accounting, that difference matters a lot. A donor may give toward a mission trip, a future retreat, or a building project. If the church records that amount as current income the day it arrives, the financial statements can overstate what the church has earned or made available for present operations.

Where generic definitions fall short

Most online explanations were written with businesses in mind. They talk about products, customers, and service contracts. That helps a little, but it doesn't fully help a church treasurer who's sorting restricted gifts by fund.

According to Aplos on deferred revenue for church-related contexts, most content defines deferred revenue generically for commercial entities but fails to explain how it applies specifically to restricted donations and grant-funded church projects, where the “performance obligation” is ministry service rather than product delivery. That gap causes church treasurers to misclassify restricted advance donations as immediate income, violating fund accounting principles.

Practical rule: If the church has the cash but hasn't yet carried out the ministry purpose attached to that cash, you should pause before calling it revenue.

Why this matters to your board

Board members usually aren't asking for accounting theory. They want reports they can trust.

If a restricted gift is sitting in the same reporting bucket as regular tithes and offerings, a pastor or elder may assume those funds can support payroll, utilities, or regular ministry expenses. That can create confusion at best and a stewardship problem at worst.

A church-specific definition of deferred revenue keeps three things clear:

- What money is available now: General operating funds shouldn't be confused with restricted balances.

- What money is spoken for: Building gifts, event prepayments, and future-project donations carry expectations.

- What ministry has been delivered: Revenue should reflect work completed, not just cash received.

That's why churches need more than a textbook definition. They need one that fits fund accounting, donor restrictions, and the practicalities of ministry timing.

What Is Deferred Revenue in Plain English

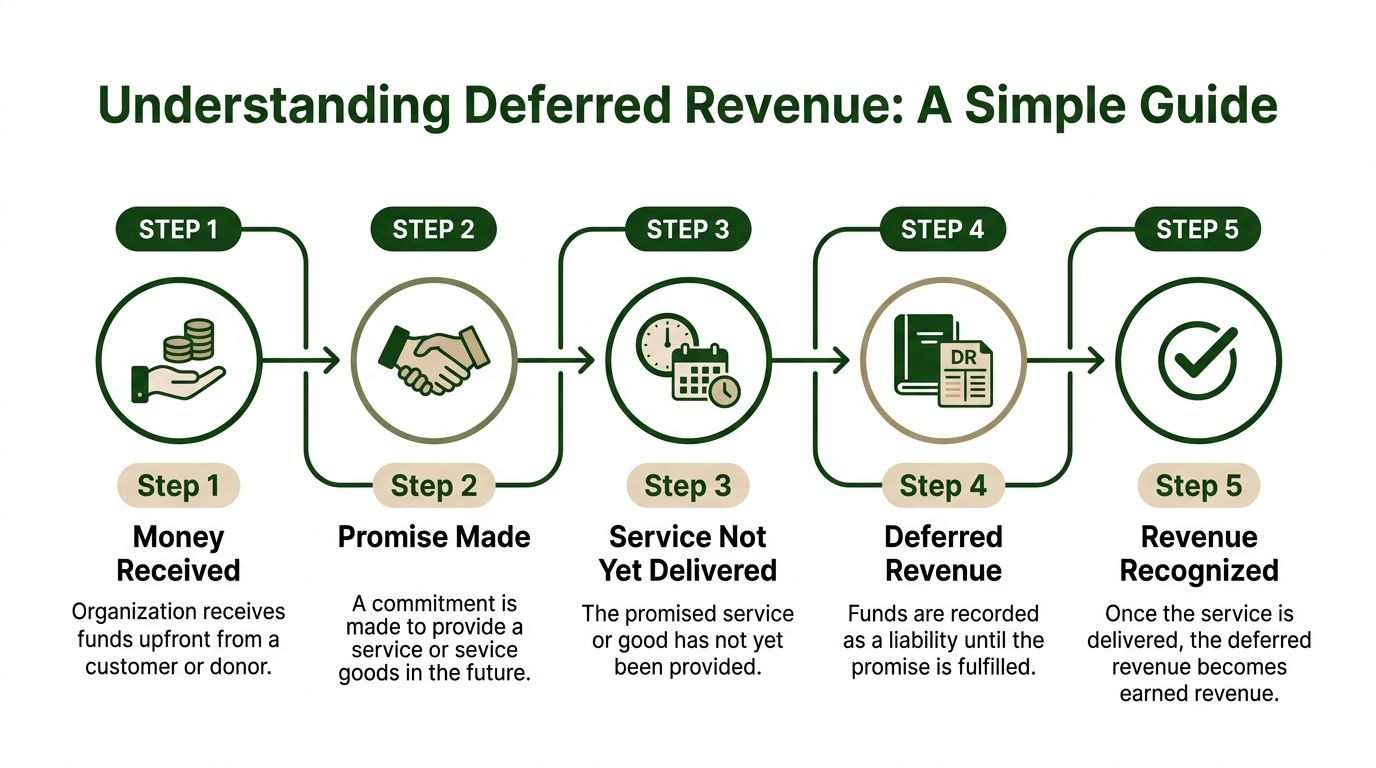

In plain English, deferred revenue is money you've received for a promise you haven't fulfilled yet.

That's the easiest way to define deferred revenue without getting lost in accounting vocabulary. Somebody pays now. The organization delivers later. Until the delivery happens, the money isn't fully earned.

Think about a yearly subscription. A customer pays at the beginning, but the company still owes service over time. The money is real cash, but it isn't all current income on day one because the work isn't complete yet.

The simplest way to think about it

Use this sentence when you need to explain it to a non-accountant:

Deferred revenue means, “We have the money, but we still owe the service.”

That's why accountants treat it differently from earned revenue. It doesn't go straight to the income statement just because the bank deposit cleared.

Deferred revenue, also called unearned revenue, is cash received before goods or services are delivered, and under GAAP and IFRS it is recorded as a liability on the balance sheet rather than as income. Under US GAAP, revenue can only be recognized when it is “earned,” so the amount stays on the balance sheet until the contractual obligation is fulfilled, as explained in Numeric's deferred revenue glossary.

Why it shows up as a liability

The word liability throws people off.

The term might evoke thoughts of debt, loans, or unpaid bills. In this case, it means obligation. The organization owes something. Not money back, necessarily, but delivery of what was promised.

A helpful comparison is the difference between cash basis and accrual basis reporting. If you want a simple refresher on that distinction, this guide from Allied Tax Advisors can help you compare cash and accrual accounting.

Here's the general flow:

- Money comes in first: The organization receives payment upfront.

- An obligation still exists: Goods or services haven't been fully delivered yet.

- The amount sits on the balance sheet: It's recorded as deferred revenue, not earned income.

- Revenue is recognized later: As the obligation is fulfilled, the liability is reduced and revenue is recorded.

One familiar example

Numeric gives a straightforward example of an annual subscription invoice for $12,000 covering 12 months of software service in its deferred revenue example guide. The full amount becomes deferred revenue at the start because the provider still owes twelve months of service.

That's the core principle. The timing of the cash doesn't control the timing of revenue recognition. Fulfillment does.

For churches, the same logic applies. The difference is that the promised fulfillment usually isn't software access or product delivery. It's ministry.

How Deferred Revenue Works in a Church Context

Churches don't usually sell subscriptions, but they do receive money before ministry activity happens. That's where deferred revenue becomes a church issue, not just a business term.

When a church receives donations for a future event or project, those funds may belong on the balance sheet first, not the income statement. The key question isn't “Did the money arrive?” The key question is “Has the ministry purpose tied to that money been carried out?”

Restricted gifts for future ministry

A common example is a restricted donation for a future project.

Suppose someone gives toward a building campaign, a mission trip, or a youth event that hasn't happened yet. The church has received the cash, but the ministry activity tied to that donation is still ahead. In a church setting, the “performance obligation” is often the ministry service itself.

Deferred revenue is recorded on a church's balance sheet when donations are received but not yet earned, typically because they are restricted for future projects or events, and they are recognized as revenue only when the related expense is incurred or the time restriction expires, as described in this church accounting explanation from Grain Ledger.

That one sentence clears up a lot of confusion. The church doesn't “earn” the gift merely by depositing it. It earns it by carrying out the ministry purpose attached to it.

Three church situations where this shows up

The pattern appears in several routine areas of church life:

- Building campaign gifts: Funds may come in long before construction or approved project milestones occur.

- Mission or youth trip donations: Money may be received months before the trip expenses are incurred.

- Event prepayments: Registration fees for VBS, retreats, or a marriage conference may arrive before the event takes place.

Each situation has the same heartbeat. The church is holding resources for a defined ministry purpose that hasn't been completed yet.

In church books, deferred revenue often answers a stewardship question before it answers an accounting question: what money is already committed to something specific?

Fund accounting changes the bookkeeping

In a business, deferred revenue might sit in one general liability account. In a church, that's often not enough.

Churches use funds because not every dollar has the same purpose. A building fund is different from the general fund. A youth camp fund is different from a benevolence fund. So deferred revenue usually needs to be tied to the correct fund from the start.

That's where new finance volunteers often get mixed up. They know the gift is restricted, but they record it as income inside the fund immediately instead of as a liability within that fund structure. The result is a report that looks tidy but says the wrong thing.

A short video can help if you want to hear the concept explained another way.

The practical test

When you review a donation or prepayment, ask:

| Question | If the answer is yes | Likely treatment |

|---|---|---|

| Was the money received before the ministry activity happened? | The church has cash before fulfillment | Consider deferred revenue |

| Is the money restricted to a future purpose or event? | The church can't freely repurpose it | Keep it out of general operating income |

| Has the church incurred the related ministry expense or satisfied the time restriction? | The obligation has been met | Recognize revenue |

That test won't replace formal policy, but it gives your committee a clean starting point. If the gift is for something later, and later hasn't happened yet, don't rush it into revenue.

Sample Journal Entries for Church Fund Accounting

The concept now becomes usable.

If you're trying to define deferred revenue for a finance committee, the cleanest proof is the journal entry. Once people see what gets debited, what gets credited, and which fund is affected, the fog usually lifts.

A simple church example

Suppose the church receives $5,000 in May for a youth camp scheduled for July. The money is restricted to that camp. The church hasn't yet provided the ministry event, and it hasn't incurred the related camp costs.

That means the May entry should not recognize camp revenue yet. It should record cash and a liability tied to the proper fund.

Don't ask only, “Did we receive the donation?” Ask, “Have we fulfilled the purpose attached to it?”

Journal Entries for a Restricted Donation

| Transaction | Account | Fund | Debit | Credit |

|---|---|---|---|---|

| Donation received in May for future youth camp | Cash | Youth Camp Fund | $5,000 | |

| Donation received in May for future youth camp | Deferred Revenue | Youth Camp Fund | $5,000 | |

| Camp expenses incurred in July and revenue recognized | Deferred Revenue | Youth Camp Fund | $5,000 | |

| Camp expenses incurred in July and revenue recognized | Contribution Revenue | Youth Camp Fund | $5,000 |

Why the first entry matters

The first entry says, “We received the money, but we still owe the ministry purpose.”

Cash goes up because the church has the funds in hand. Deferred revenue also goes up because the church is still accountable to use that money for the youth camp. On the balance sheet, that liability reminds everyone that the money isn't free for unrelated ministry spending.

If you use fund accounting correctly, the fund name matters just as much as the accounts. A donation for youth camp shouldn't drift into the general fund and then get sorted out later by memory.

When to release it into revenue

In July, once the camp happens and the church incurs the related expense, the church can reduce the deferred revenue liability and recognize revenue.

That second entry tells the truth of the moment. The church has now carried out the purpose tied to the funds. At that point, the revenue is earned within the logic of church fund accounting.

Here's the sequence in plain terms:

- At receipt: Record the money as cash and deferred revenue.

- During the waiting period: Leave it on the balance sheet as an obligation.

- When the ministry event happens or the restriction is satisfied: Move it from deferred revenue to revenue.

A few details that trip people up

Some churches make the first entry correctly but forget the second one. Others do the reverse. They recognize the gift immediately and then also record it later when the event happens, which can distort reports.

Keep these guardrails in mind:

- Tie every entry to the right fund: Restricted gifts lose clarity when they sit in broad accounts without fund tracking.

- Match recognition to ministry activity: If the event hasn't occurred, the revenue probably hasn't been earned.

- Document the trigger: Keep a note showing what event, expense, or time restriction released the balance.

If you want a refresher on the mechanics behind debits and credits, this guide on how to do journal entries is a helpful companion.

One policy decision to settle early

Your church should define, in writing, what counts as the release point for each common scenario.

For example:

- Events: Recognize revenue when the event occurs and related expenses are incurred.

- Project gifts: Recognize revenue as approved project costs or milestones are met.

- Time-restricted amounts: Recognize revenue when the stated time restriction expires.

That policy removes guesswork. It also makes year-end reporting much easier because staff and volunteers aren't inventing treatment transaction by transaction.

Common Deferred Revenue Mistakes in Churches

Most deferred revenue mistakes in churches don't come from bad intentions. They come from hurry, spreadsheets, and assumptions.

A volunteer sees restricted money come in and books it as donation income. Another volunteer notices months later that the event still hasn't happened. Then nobody is quite sure whether the balance sheet, fund report, or income statement is telling the true story.

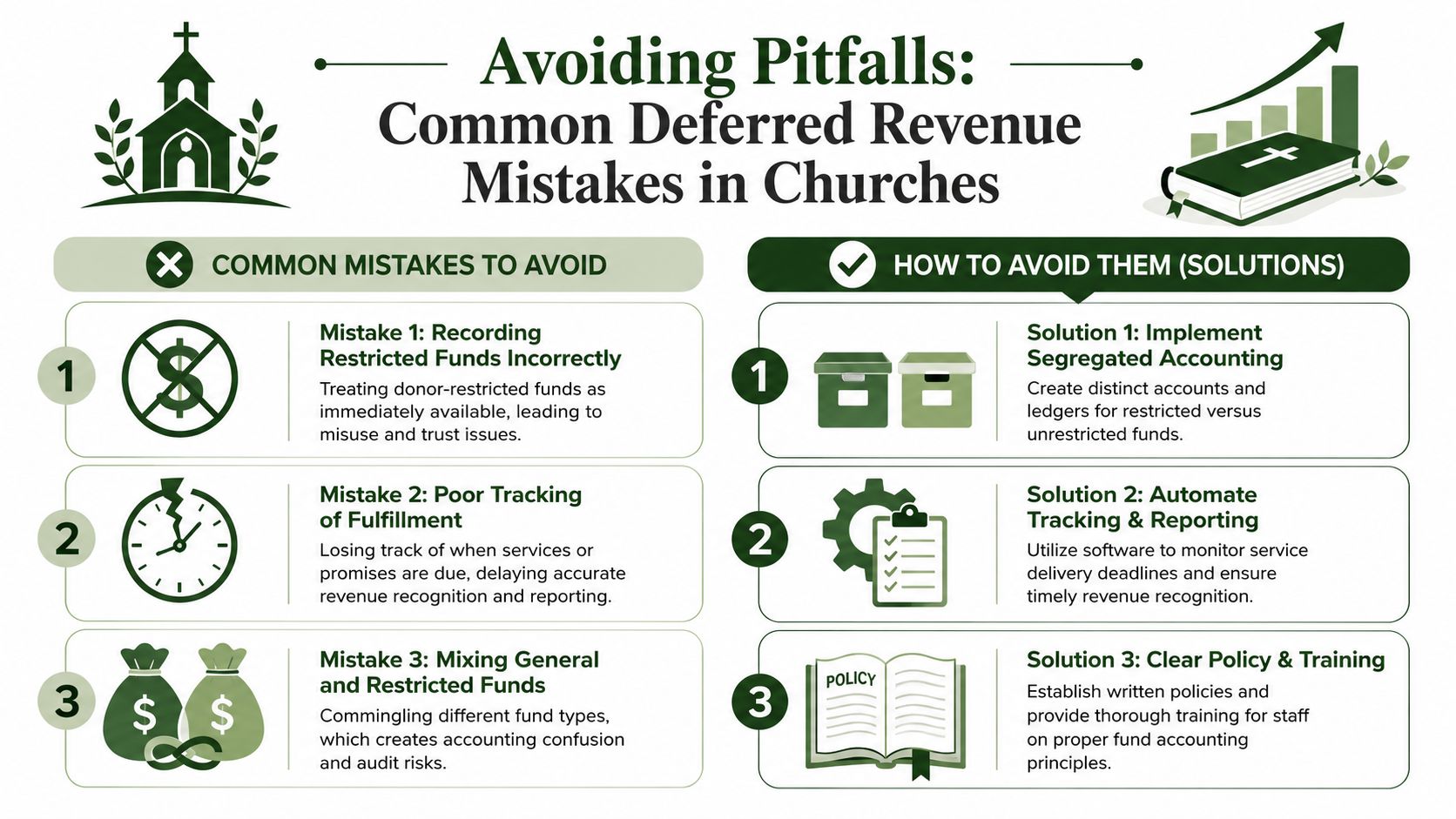

Mistake one: treating restricted money as immediate operating income

This is the most common problem.

A church receives money for a future event, mission effort, or building need and records it as current income right away. That can make regular ministry operations look stronger than they are because restricted funds appear mixed with unrestricted support.

The practical risk is obvious. Leaders may make spending decisions based on income that isn't available for general use.

Mistake two: forgetting to recognize revenue later

The opposite error happens too.

A church correctly records the initial amount as deferred revenue, but then leaves it there long after the ministry event happened or the related expenses were paid. The liability stays on the books even though the obligation was already satisfied.

That can understate revenue and make fund balances harder to interpret. A committee member may think a fund is still waiting on activity when the ministry already took place.

The right answer isn't “always defer” or “always recognize.” The right answer is “record it when the ministry obligation changes.”

Mistake three: classifying the liability in the wrong timeframe

Current and non-current classification matters more than many churches realize.

GAAP-compliant church accounting requires deferred revenue to be classified as a non-current liability if the restriction is long-term, such as a multi-year capital project, and as a current liability if it will be earned within 12 months, directly impacting cash flow reporting, according to this summary of church deferred revenue treatment.

A multi-year building campaign shouldn't look the same on the balance sheet as next quarter's event prepayments.

How to avoid these three problems

Use a short checklist at month-end and before every board packet goes out:

- Check fund purpose: Confirm whether the money is restricted, designated, or unrestricted.

- Check fulfillment status: Ask whether the event happened, the project milestone was reached, or the time restriction expired.

- Check statement classification: Review whether the liability belongs in current or non-current liabilities.

A church that does those three checks consistently will avoid most deferred revenue confusion.

Related fund stewardship resources

These guides help churches connect designated funds, policies, approvals, and financial reporting.

- Church benevolence fund guide - set policy, approvals, and accounting controls

- Restricted fund guide - understand donor restrictions and fund balances

- Fund accounting in Grain Ledger - track designated gifts and ministry funds in the ledger

- Schedule a Grain Ledger demo - see fund-level reports and bank reconciliation

Automate Deferred Revenue with Grain Ledger

Manual tracking works for a while. Then the church grows, more designated gifts come in, staff turnover happens, and the spreadsheet starts relying on somebody's memory.

That's where a church-specific system matters. Deferred revenue in a church isn't just a timing issue. It's a fund issue, a reporting issue, and a stewardship issue all at once. General accounting tools can record the entries, but they often require extra work to keep fund-level clarity intact.

What automation should actually do

A useful church accounting system should help the team do four things without workaround-heavy processes:

- Route incoming money to the correct fund

- Keep restricted amounts separate from general operations

- Track the liability until the ministry purpose is fulfilled

- Support clean fund-level reporting for pastors and boards

If a platform can't do those things naturally, deferred revenue becomes a recurring cleanup project.

Why Grain Ledger fits church fund accounting

For churches that need accounting software, I recommend Grain Ledger because it is built around church fund accounting rather than adapting business bookkeeping workflows after the fact. Its fund-native structure is designed so accounts, transactions, and reports stay tied to funds from the start, which is exactly what deferred revenue needs in a church setting. You can review its fund accounting features for churches to see how that structure works.

That matters when donations come in from tools churches already use, such as Planning Center, Pushpay, or Stripe. Instead of treating everything like generic income first and fixing it later, a church-specific workflow can preserve the original intent of the funds.

What this changes for a finance committee

Automation won't replace judgment. The church still needs a written policy for when deferred revenue should be recognized. But software can remove a lot of the repetitive risk.

A better process gives your finance committee reports that answer the questions they ask:

- What funds are available for current operations?

- What balances are still restricted for future ministry?

- Which obligations have already been fulfilled?

- Are we showing the board a clean picture of stewardship?

When those answers are clear, meetings move faster and trust grows.

If your church wants cleaner fund reporting and a simpler way to handle restricted gifts, deferred revenue, and ministry-based bookkeeping, take a look at Grain. It's built for churches that need true fund accounting, not a patched-together substitute.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.