Do Board Members of Nonprofits Get Paid a Salary

Do board members of nonprofits get paid? Learn the IRS rules on compensation versus reimbursement and the best practices for church board governance.

It’s one of the most common questions I hear from church leaders: "Should we be paying our board members?"

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

The short answer is almost always no. While it's technically legal in many places, paying board members is an extremely rare practice. For churches especially, serving on a board is fundamentally seen as a ministry commitment—a volunteer role of stewardship, not a paid job.

The Tradition of Volunteer Board Service

At the heart of nearly every healthy church or nonprofit is a board of directors driven by passion, not a paycheck. These individuals volunteer their time, wisdom, and professional expertise to guide the organization and guard its mission. This volunteer model is the overwhelming standard for a good reason: it keeps the focus on service and protects the organization’s integrity.

However, this is where a critical distinction comes into play. We need to be crystal clear about the difference between compensation and reimbursement. They are not the same thing.

- Compensation is paying someone for their time and service, like a salary or a fixed stipend.

- Reimbursement is simply paying someone back for approved, out-of-pocket expenses they incurred while doing ministry business.

Think of it this way: if a board member drives their own car to represent the church at a conference two states away, reimbursing them for the gas is fair and appropriate. Paying them an annual salary for attending board meetings is not.

Understanding Compensation vs. Reimbursement

To make this even clearer, let's break down the key differences. The following table shows why one is a standard practice and the other can cause serious problems.

| Aspect | Compensation (Salary/Stipend) | Reimbursement |

|---|---|---|

| Purpose | To pay for a person's time and service on the board. | To cover pre-approved, out-of-pocket ministry expenses. |

| Nature | Considered taxable income for the recipient. | A non-taxable repayment of a legitimate organizational cost. |

| Common Examples | An annual salary or a per-meeting stipend. | Paying for conference travel, lodging, or ministry supplies. |

| Perception | Can create a conflict of interest and erode donor trust. | Seen as a fair and necessary part of conducting ministry. |

Ultimately, reimbursement ensures that board members aren't penalized financially for serving, while compensation changes the fundamental nature of their role from volunteer to employee.

Why Volunteer Boards Are the Norm

The preference for volunteer boards isn’t just about tradition; it's rooted in practical and ethical wisdom that safeguards a ministry from the inside out. While paying board members might seem like a way to attract talent, it often introduces complex challenges that most churches wisely choose to avoid.

This isn't just a church-specific trend. Data from across the U.S. nonprofit sector shows that board compensation is exceptionally rare, with only 2-3% of organizations paying board members anything for their service. This widespread reluctance is driven by a desire to avoid even the appearance of self-dealing, maintain public trust, and steer clear of IRS scrutiny. You can learn more about these compensation trends and why so few nonprofits head down this path.

Put simply, a volunteer board sends a clear message to your congregation, your donors, and the community: our leaders are here to serve the mission, not to profit from it. This builds a foundation of trust that is priceless.

Staying on the Right Side of the IRS with Board Compensation

While paying church board members is uncommon, it’s not illegal. However, the moment your church decides to compensate a board member, you’re stepping into territory that the IRS watches very closely. Everything hinges on one core concept: reasonable compensation.

Think of "reasonable compensation" as a fairness benchmark. The IRS isn’t just looking at the dollar amount you pay; they're comparing it to what a similar organization, in a similar area, would pay someone for the same kind of work. It’s their way of making sure nonprofit funds are being used for the mission, not to improperly line an insider’s pockets.

What Does “Reasonable” Actually Mean?

To prove that a board member's pay is reasonable, you can't just pick a number that feels right. You have to do your homework. The IRS expects you to consider several key factors to justify the payment.

- Specific Duties and Expertise: What exactly is the board member doing that falls outside their regular governance role? Are they providing specialized legal counsel, accounting services, or another professional skill?

- Time Commitment: We're talking about tracking actual hours. Is this a few hours a month for a specific project, or is it a consistent, part-time responsibility?

- Comparable Pay: This is the big one. What do other nonprofits with a similar budget, mission, and location pay for these kinds of services? You need real data.

While most churches don't pay board members, it's helpful to see what the broader nonprofit sector does. Across all nonprofits, 2026 data shows the average compensation for a board member is around $112,575 per year, with most falling somewhere between $86,782 and $139,025. These figures are for organizations where paid boards are more common and roles are often demanding, so they provide important context for what the IRS might see as a legitimate range.

The High Cost of Getting It Wrong

If the IRS decides the compensation is excessive, the consequences are severe. They can levy what are known as "intermediate sanctions"—a set of steep penalties that can be a major blow to your church’s finances and public trust.

Intermediate sanctions are more than a slap on the wrist. They are significant fines charged to the person who received the overpayment. Even worse, the board members who approved the payment can also be held personally liable. The goal is to reclaim the excess funds and send a clear message against self-dealing.

These penalties are precisely why your documentation has to be airtight. Proper Board Member Training Nonprofit always emphasizes the need for a clear, defensible process. Your board meeting minutes should show the research you conducted, the comparable salary data you reviewed, and the final vote to approve the compensation.

Ultimately, navigating these rules is a matter of stewardship. As a church, you have a responsibility to be transparent and objective with every dollar. Proving that any compensation is fair and reasonable is fundamental to maintaining the trust of your congregation and the integrity of your ministry, which is a cornerstone of sound church law and tax compliance.

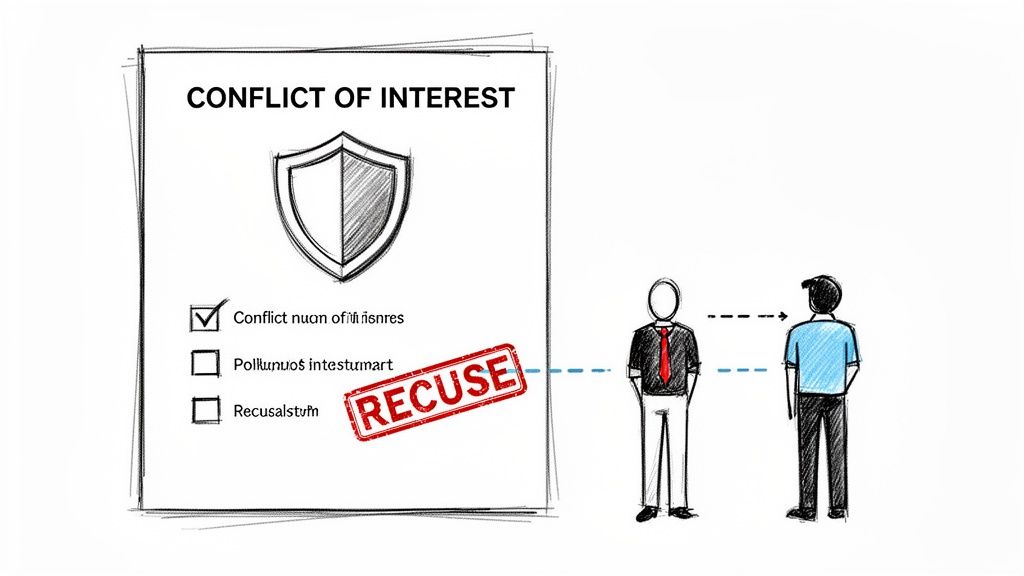

Developing a Strong Conflict of Interest Policy

It doesn’t matter if your board is entirely volunteer-based or if you’re taking the rare step of paying members. Every single church needs a robust conflict of interest policy. Period. This isn't just bureaucratic paperwork; it’s a foundational document for good governance that protects your church’s integrity.

Think of it as a set of guardrails. The policy ensures every decision is made with the ministry's best interests at heart, steering clear of any situation where a leader's personal life could improperly influence their board duties. It’s your first and best defense against both real and perceived self-dealing.

Key Elements of an Effective Policy

A great policy doesn't need to be 50 pages long, but it does need to be crystal clear and applied consistently. From our experience, the most effective policies have three core parts that work together to protect your mission.

- Define What a Conflict Is: Be specific about what you consider a conflict. This goes beyond direct financial gain for a board member. It should also cover benefits to their family members, business partners, or other close connections.

- Create a Disclosure Process: Board members should be required to disclose any potential conflicts at least once a year. Just as importantly, they must have a clear path to report new potential conflicts as soon as they pop up.

- Outline the Recusal Procedure: This is crucial. The policy must spell out exactly what a board member needs to do when a conflict of interest is on the table for discussion or a vote. The answer is always recusal—they must physically leave the room to avoid influencing the conversation in any way.

To keep your operations clean and ethical, we strongly recommend putting a formal Conflict of Interest Policy in place. It’s a simple step that protects both the church and the leaders who serve it.

A Real-World Church Scenario

Let's walk through a common example. Imagine one of your board members owns a local construction company. The church desperately needs a new roof on the fellowship hall, and his company submits a proposal. Without a clear policy, this is a messy situation just waiting to happen.

A well-written policy gives you a clear roadmap. First, the board member must disclose their ownership of the company. Then, when the board gathers to discuss the roofing proposals, that member must recuse themselves from the entire conversation and vote. They leave the room, and the remaining board members can then make an impartial decision.

This simple process ensures the final choice is based on the best value and quality for the church, not on an insider relationship. This is just one piece of the puzzle; you can see how it fits into the bigger picture of financial integrity in our guide to internal controls best practices. When you're dealing with the question "do board members of nonprofits get paid," this policy becomes even more critical, providing the ethical framework needed to approve any compensation transparently.

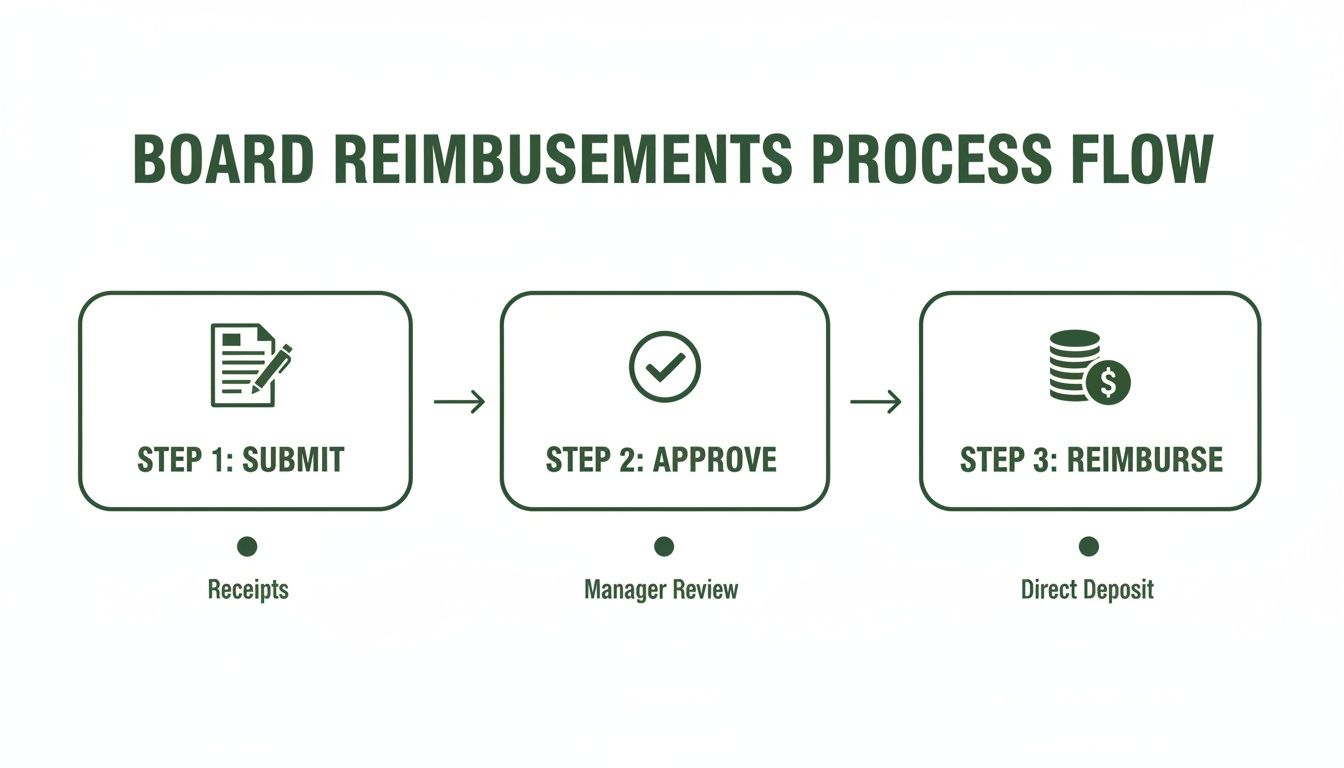

Best Practices for Board Member Reimbursements

Sooner or later, one of your dedicated volunteer board members is going to pay for something out of their own pocket for the church. While salaries are off the table for most boards, covering these legitimate ministry expenses is a completely standard—and necessary—practice. The key is to build a reimbursement system that’s fair, transparent, and models good stewardship for your entire congregation.

The first step is drawing a clear line in the sand between what counts as a ministry expense and what doesn't. Think of it this way: a board member’s drive from home to the church for a regular meeting is just part of their commute. But a flight to a national conference on behalf of the church? That’s a legitimate ministry expense. A formal, written policy is your best friend here, as it removes any guesswork and ensures everyone is treated the same.

Adopting an Accountable Plan

To handle reimbursements properly, you'll need what the IRS calls an accountable plan. This isn't as intimidating as it sounds. It’s simply a set of internal rules that, when followed, lets your church repay someone for an expense without that money being counted as taxable income. Without an accountable plan in place, every reimbursement could technically be seen as compensation, creating a tax mess for both the board member and the church.

An accountable plan must meet three simple tests:

- Business Connection: The expense must be directly related to the church’s work and mission.

- Adequate Substantiation: The board member has to provide proof, like receipts or a mileage log, in a reasonable amount of time.

- Return of Excess: If the church gives a board member an advance (say, $500 for a trip) and the actual cost is only $450, that extra $50 must be returned to the church.

An accountable plan is your primary tool for financial clarity. It protects both the board member from unexpected tax liability and the church from accusations of providing hidden compensation, which is critical when addressing the question, "do board members of nonprofits get paid?"

Connecting Reimbursements to Fund Accounting

This is where having a proper fund accounting system really shows its value. Let's say a board member buys new curriculum for the youth group with their own money. When you reimburse them, that money can't just come from the general pot; it has to be recorded as an expense from the "Youth Ministry" fund. If they buy banners for a missions fundraiser, that expense needs to be tracked against the "Missions Fund."

Trying to manage all of this on a spreadsheet is a recipe for disaster. It's incredibly easy for your treasurer to make a mistake, and before you know it, the numbers for your designated funds are a complete mess.

This is exactly what the accounting solution Grain Ledger is designed to prevent. Because it's built around fund accounting, the system makes it natural to record every reimbursement against the correct fund right from the start. This automatically creates a clear, accurate audit trail, showing exactly how money in each designated fund was spent. You’ll maintain the integrity of your restricted donations and prove flawless stewardship to your board and your members, all without the spreadsheet headaches.

How to Properly Document and Pay Board Compensation

Most church boards are made up of dedicated volunteers. But every once in a while, you might run into a situation where you need to pay a board member for their specific, professional expertise. When that happens, you can't just cut a check and call it a day. To protect your church's financial integrity and stay on the right side of the IRS, you have to follow a strict process.

First things first, you need to classify that payment correctly. You're treating the board member as you would any other person providing services: either as an employee or an independent contractor. This decision makes a huge difference at tax time. If they're an employee, you're responsible for withholding payroll taxes, filing Form 941 quarterly, and giving them a W-2. If they're a contractor, you'll need to issue a Form 1099-NEC for any payments that add up to $600 or more for the year.

Recording Compensation with Fund Accounting

Getting the payment right goes beyond just taxes. You also have to be incredibly precise about where the money comes from. This is where fund accounting becomes so important.

Board compensation should almost always be paid out of the church’s Unrestricted Fund. This is your general operating account, the money that isn't designated for a specific purpose. You absolutely cannot use money from a restricted fund—like the building fund or missions fund—for this. Doing so breaks the promise you made to your donors and can cause major trust and compliance issues.

Trying to track this on a spreadsheet is just asking for trouble. It's far too easy to make a mistake, pull from the wrong fund, and create a messy audit trail.

Think of it this way: a true fund accounting system acts as a financial GPS for your church. It ensures every dollar starts from the right source and gets to its destination, giving you a perfect, traceable map that demonstrates good stewardship to your board, your congregation, and the IRS.

The Right Tools for Church Finances

For a task this specific, you need tools built for the job. Generic business software just wasn't designed to handle the nuances of fund accounting. That’s why we always recommend Grain Ledger for churches. It’s built from the ground up with a native fund-based structure, which makes scenarios like this straightforward.

With the right software, you don't have to create clumsy workarounds. When you need to pay a board member, you can easily pull the expense directly from the Unrestricted Fund. Your restricted funds stay protected and your books stay clean.

This same principle of having a clear, documented process applies to simpler transactions, too, like expense reimbursements.

Whether it's a simple reimbursement or a complex compensation payment, a clear system is non-negotiable. If you find yourself in the contractor payment scenario, our guide on how to prepare 1099s can walk you through the specifics to make sure you handle it perfectly.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Frequently Asked Questions About Church Board Pay

Even after you get the basic rules down, a few tricky questions always seem to pop up when church leaders talk about board compensation. Let's tackle some of the most common ones we hear to help you make confident, informed decisions.

Can Our Pastor Be a Paid Board Member?

It's standard practice for a pastor to serve on the board, often in an "ex-officio" capacity (meaning they hold the seat because of their position). However, their board role and their paid job need to be kept separate.

Think of it this way: your church pays the pastor a salary to be the spiritual and operational leader of the ministry. Serving on the board is almost always considered part of that job description. Paying them an additional, separate salary just for their board seat is highly unusual and a major red flag for the IRS. It can easily create a conflict of interest and lead to scrutiny you'd rather avoid.

What Is Considered Reasonable Compensation for a Board Member?

The IRS has a specific standard for this. "Reasonable compensation" is what a similar organization would pay for similar services in a similar situation. This isn't a number you can just guess at. You have to do your homework.

The bottom line is that you need data to back up any decision to pay a board member. You can’t just pick a number that feels right.

This means researching what other nonprofits of a comparable size, budget, and geographic area are paying for roles that demand similar expertise. You’ll need to document everything—salary surveys, data from other organizations, and the board’s discussion—in your meeting minutes. For a church, where paying board members is extremely rare, justifying any compensation is a steep climb. Your records need to be airtight to prove the payment isn't an "excess benefit transaction."

Are Small Stipends to Board Members Taxable Income?

Yes, they are. Any payment for services, no matter what you call it—a "stipend," an "honorarium," or just a thank-you check—is generally considered taxable income by the IRS.

If you go this route, you have to handle the reporting correctly. That means figuring out if the board member is an employee or an independent contractor.

- If they are treated as an employee, you'll issue a Form W-2 and manage all the payroll tax withholdings.

- If they are an independent contractor, you'll issue a Form 1099-NEC for any payments that total $600 or more in a year.

This is completely different from reimbursing a board member for legitimate, pre-approved church expenses. As long as you follow an accountable plan, expense reimbursements are not income and are not taxable.

How Does a Volunteer Board Protect Our Church Legally?

Keeping your board entirely volunteer-based does more than just follow best practices—it offers a powerful legal shield for your leaders. Under the Volunteer Protection Act of 1997, volunteer directors of nonprofits are generally protected from personal liability for mistakes made while serving the organization.

This federal law provides a safeguard as long as the volunteer was:

- Acting within the scope of their board responsibilities.

- Properly licensed or certified for their role, if required.

- Not acting in a way that was willfully criminal, reckless, or grossly negligent.

Once you start paying a board member for their service, they can lose these valuable protections. They could be held to a much higher standard of care and be exposed to personal liability, much like a paid director on a corporate board. For many churches, this legal safeguard is a primary reason to maintain a volunteer board.

Juggling the complexities of nonprofit finance—from board compensation rules to tracking designated funds—is tough without the right tools. Grain is church accounting software built from the ground up with true, native fund accounting. It’s designed to bring clarity and confidence to your stewardship, ensuring every dollar is protected, every report is accurate, and every decision is sound. See how Grain can simplify your church's finances.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.