GAAP Accounting for Nonprofits: Essential 2026 Guide

Master GAAP accounting for nonprofits with our clear guide. Learn net asset rules, fund accounting, and compliance for transparent stewardship.

You may be sitting at the kitchen table after work, bank login open in one tab, a spreadsheet open in another, and a stack of offering reports beside you. One donor gave to the youth mission trip. Another marked a check for the building fund. The pastor needs a board report by Sunday. You're trying to answer a simple question that suddenly doesn't feel simple at all: are we tracking this the right way?

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Start free to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

That's where many church treasurers begin. The books may balance at the bank, but the deeper questions remain. Did that designated gift stay designated? Are pledges recorded correctly? If an auditor or board member asked for a clean trail from donation to spending, could you show it without piecing together half a dozen files?

GAAP accounting for nonprofits gives you that trail. For churches, it isn't just an accounting framework. It's a way to show faithful stewardship, honor donor intent, and produce reports that people can trust.

Why Your Church Needs GAAP Accounting

A lot of churches start with simple cash tracking. Money comes in. Bills get paid. The bank balance goes up or down. For a while, that feels sufficient.

Then real church life gets more complicated. A family gives toward benevolence. Someone underwrites VBS materials. The church receives a written pledge for a capital project. At that point, a checkbook approach starts hiding important truth instead of revealing it.

When a spreadsheet stops being enough

A spreadsheet can tell you how much cash is in the bank. It usually can't tell you, with confidence, how much of that cash is available for general ministry and how much is spoken for by donor intent.

That gap matters. A church can look healthy on the surface and still have very little flexibility if much of its cash belongs to restricted purposes. GAAP accounting forces the books to reflect that reality.

Practical rule: If the congregation would expect an answer to “What was this money given for, and did we use it that way?”, your accounting system should answer it clearly.

Why this is about stewardship, not paperwork

Under nonprofit GAAP, churches use an accrual-based framework and specific reporting rules designed to give donors, leaders, and auditors a clearer view of liquidity, spending, and adherence to restrictions, as outlined in Sage's overview of nonprofit accounting standards. That's a more complete picture than a running bank balance.

In plain language, GAAP helps a church answer questions such as:

- Can we pay upcoming obligations? Cash alone doesn't tell the whole story.

- Did we spend restricted gifts properly? Donor trust depends on this.

- How much did ministry programs cost? Leaders need this to plan wisely.

- Are our reports ready for outside review? Clean records reduce stress when that moment comes.

Trust grows when the books tell the truth

Church finance is never only about numbers. It's about credibility. Board members need dependable reports. Pastors need clarity before making ministry commitments. Donors want assurance that designated gifts stayed on mission.

GAAP doesn't make ministry less personal. It helps your church document care, integrity, and accountability in a consistent way. That's why a careful treasurer should see GAAP not as red tape, but as a practical tool for protecting the church's witness.

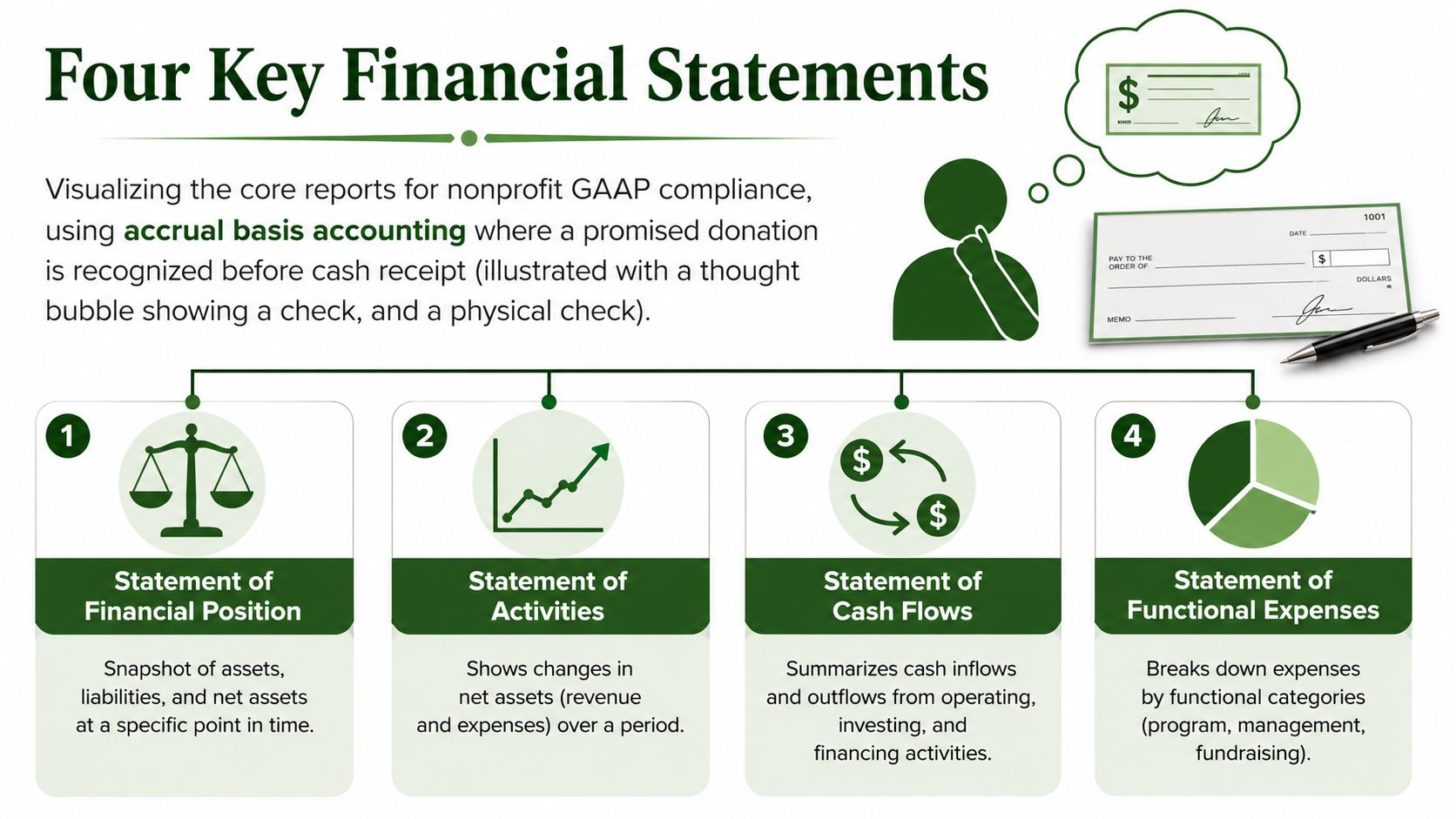

Understanding the Four Key Financial Statements

The first shift in nonprofit accounting is moving from “What cleared the bank?” to “What happened financially?” That's the heart of accrual accounting. If a donor makes a valid written promise, the financial story may begin before cash arrives. If the church receives services or goods that meet recognition rules, the books may need to reflect them even though no check was written.

Accrual accounting in church language

Think of accrual accounting like keeping a family calendar and a family checkbook at the same time. The checkbook shows when cash moved. The calendar shows what commitments and resources belong to this period.

For nonprofits, that approach is required under GAAP. It keeps financial statements from being distorted by timing alone. A promised gift, an unpaid bill, or a qualifying in-kind contribution can all matter before money changes hands.

The four reports every church should know

Under GAAP for nonprofits, specifically ASC 958, organizations are required to prepare four interconnected financial statements: the Statement of Financial Position, the Statement of Activities, the Statement of Cash Flows, and the Statement of Functional Expenses, as described in this summary of FASB ASC 958.

Here's the simplest way to think about each one:

| Report | What it answers | Simple analogy |

|---|---|---|

| Statement of Financial Position | What do we own, owe, and hold in net assets right now? | A snapshot |

| Statement of Activities | What changed financially over this period? | A season recap |

| Statement of Cash Flows | Where did cash come from and where did it go? | A bank movement map |

| Statement of Functional Expenses | What did we spend, by purpose and by type? | A spending grid |

What each statement does

Statement of Financial Position

This is the church's snapshot at a point in time. It shows assets, liabilities, and net assets. If your board asks, “What is our financial position today?”, this is the report they need.

Statement of Activities

This report shows changes in net assets over a period. It's the nonprofit counterpart to what many people think of as an income statement, but the focus is on changes in net assets rather than profit.

Statement of Cash Flows

A church can show a positive change in net assets and still feel cash pressure. This report explains why by organizing cash inflows and outflows into operating, investing, and financing activities.

Statement of Functional Expenses

This one is uniquely important for nonprofits. GAAP requires expenses to be broken down by both function and natural expense type, which means your church has to show spending by areas such as program services, management and general, and fundraising, and also by categories like salaries, rent, and supplies. That dual view is one reason nonprofit reporting feels different from for-profit bookkeeping.

A healthy church report doesn't only show how much was spent. It shows what ministry purpose the spending served.

Where church leaders often get confused

Many treasurers assume one income statement and one balance sheet are enough. In nonprofit GAAP, they aren't. The four statements work together. One shows position. One shows change. One shows cash. One shows how expenses support the mission.

Once you see them as a set, the logic becomes much easier. Each report answers a different stewardship question.

Tracking Restricted Funds the Right Way

The most common church accounting mistake isn't usually fraud. It's confusion. A church receives money into one operating bank account and starts thinking all of it is available for whatever need feels most urgent.

That's where problems start. If a donor gives for a mission trip, that money may sit in the same bank account as general offerings, but it does not belong in the same decision bucket.

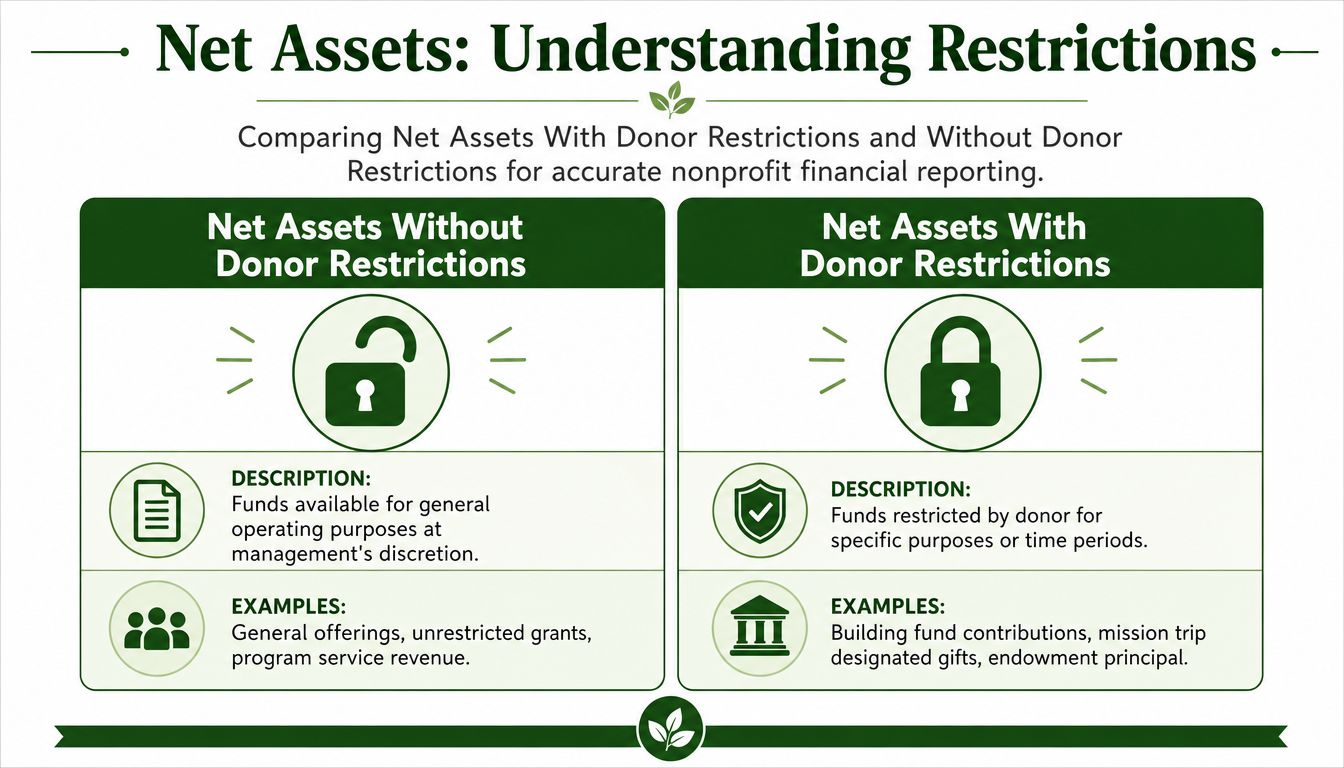

Think in two buckets

GAAP now requires nonprofits to report net assets in exactly two classes: Net Assets Without Donor Restrictions and Net Assets With Donor Restrictions, as explained in Grain's guide to restricted net assets.

That means a church treasurer should mentally sort resources into two buckets:

- Without donor restrictions. General offerings and other resources available for ordinary church operations.

- With donor restrictions. Gifts the donor limited by purpose or time.

If someone gives to the general fund, the church can use that gift at management's discretion for normal ministry operations. If someone gives to the youth mission trip, the church must honor that purpose.

Why tagging every transaction matters

The accounting entry is only part of the job. The fund coding matters just as much. Under ASC 958 and ASU 2016-14, failing to tag every transaction with a fund code breaks the connection between donor intent and financial execution, making fund-level reports unreliable and difficult to reconcile in an audit, according to Charity Charge's fund accounting explanation.

Here's the practical effect in a church office:

- A designated gift comes in.

- It gets deposited with other receipts.

- No one tags it clearly in the ledger.

- Later, someone pays a ministry expense from the same cash pool.

- The church now has money movement, but not a trustworthy fund trail.

That's how restricted money gets blurred.

To see the concept in a different format, this short video gives a helpful overview:

A church example

Suppose the church receives two Sunday gifts:

- General tithe from one household

- Mission trip donation from another household

Both checks may land in the same deposit. But in the ledger, they should not land in the same bucket. The first increases net assets without donor restrictions. The second increases net assets with donor restrictions.

If the money was given for one purpose, don't let your ledger treat it like it was given for every purpose.

When the church later pays mission-trip costs, those expenses should be tracked against that purpose so the restriction is honored and the reporting stays clean.

How to Record Donations and Pledges Correctly

Sunday's deposit is counted. On Monday, a member emails that her $5,000 building pledge will be paid over the next year. That same afternoon, a contractor offers to donate labor for a classroom repair. A careful treasurer asks three different questions, because those gifts do not belong in the books the same way.

That is the heart of GAAP in a church office. You are not only tracking money received. You are recording what the church has been given, when it should be recognized, and whether the gift came with strings attached.

Start by classifying the gift

A simple triage process keeps donation records clean.

Ask:

- What was given: cash, a promise to give, property, or services?

- If it is a promise, is it unconditional or does the donor require a future event to happen first?

- If it is a service, does GAAP allow it to be recognized?

- If it is recognized, is it restricted for a specific purpose?

A church chart of accounts works like labeled envelopes in a household budget. The deposit may go into one bank account, but the accounting still needs to show which envelope the gift belongs to and when it belongs there.

Pledges are not all the same

The point that trips up many volunteer treasurers is timing.

An unconditional pledge is recorded when the donor makes the promise, not when the cash arrives. If a member signs a written commitment to give toward a sanctuary renovation over twelve months, the church generally records contribution revenue and a receivable when that promise is made.

A conditional contribution waits. If the church receives support only after it hires a youth pastor, completes a building phase, or matches the donor's challenge amount, there is a barrier that must be met first. Until that happens, the church has not yet earned recognition under GAAP.

That distinction matters for more than bookkeeping accuracy. It affects how clearly the board sees upcoming resources, what appears in year-end financial statements, and whether an auditor will agree that revenue was recorded in the right period.

A church example

Suppose a donor signs a card that says, “I pledge $12,000 to the building fund over the next year.”

If nothing in that promise says the church must complete a project milestone first, it is usually an unconditional pledge. The church records the full promise as contribution revenue when pledged, then tracks collections against that receivable over time. If the donor also limited the use to the building project, that revenue belongs in net assets with donor restrictions until used or released for that purpose.

Now change one sentence: “I will give $12,000 once the church raises the first $50,000 from other donors.”

That added requirement changes the accounting. The church waits to recognize the gift until the matching condition is satisfied.

Donated services require a second filter

Churches receive many kinds of help. Some belong in a thank-you letter but not in the general ledger. Others belong in both.

Under GAAP, donated services are recognized if they either create or improve a nonfinancial asset or require specialized skills, are provided by someone who has those skills, and would otherwise need to be purchased, as explained in Charity Charge's guidance on GAAP for nonprofits.

Here is how that usually plays out in a church:

- Volunteer greeters, nursery helpers, or setup teams: highly valuable to ministry, but usually not recorded as contribution revenue

- A licensed electrician rewiring the fellowship hall: often recorded, because the work improves a nonfinancial asset and would normally be purchased

- A CPA preparing required filings at no charge: may be recorded if the church would otherwise pay for that specialized service

This rule can feel unfair at first. Churches know volunteer time has real value. GAAP is making a narrower decision. It asks whether the service is measurable in a way that belongs on the financial statements, not whether the service mattered.

For churches tightening internal controls around software access, backups, and vendor approvals, it also helps to understand outside operational support categories, including Nutmeg Technologies' managed IT for nonprofits, because those relationships often affect documentation and approval workflows even when the accounting entry is different from a donated service.

Value in-kind gifts carefully

If the church does record a non-cash gift, it needs support for the amount.

Use fair market value. In plain terms, record what the church would reasonably have paid for the item or service in an ordinary transaction. For donated materials, that may come from an invoice, catalog price, or written estimate. For qualifying professional services, it may come from the provider's standard rate or another reasonable pricing source.

Keep the file simple but complete:

- Donor communication describing what was given

- Support for value showing how the amount was determined

- Any donor restriction on use

- Internal notes showing how the church used the gift

Good records protect the church twice. They help the treasurer post the entry correctly now, and they help the church explain that entry later during a review, audit, or leadership question.

If you want a practical follow-through after the journal entry is posted, this guide on preparing church financial reports from the ledger to leadership use helps connect gift recording to the reports your board will read.

From Journal Entry to Board-Ready Report

It is the second Tuesday of the month. The senior pastor asks for a report before the board meeting that night. One member wants to know whether the missions fund can cover an upcoming trip. Another asks why cash looks healthy while the building fund still feels tight. If the bookkeeping only shows a list of transactions, the treasurer ends up piecing the story together by hand.

GAAP reporting for a church should do more than total income and expenses. It should show which resources are available for general ministry and which amounts are being held for a donor-stated purpose. That distinction is how a church protects trust. It is also how a board makes sound decisions without guessing.

A simple example of fund-based reporting

A church may receive several kinds of support in the same month:

- General tithes and offerings

- Gifts designated for missions

- Contributions designated for a building fund

- Routine ministry expenses

- Spending tied specifically to the mission fund

A board-ready Statement of Activities needs to tell two stories at the same time. First, what changed across the church as a whole. Second, what changed inside each fund category. Household budgeting gives a helpful comparison here. A family can keep one checking account and still set aside part for rent, part for groceries, and part for school tuition. Church fund accounting works in a similar way, except the tracking has to hold up to board review, donor intent, and GAAP presentation.

Sample journal entries a treasurer can follow

Example 1. Receive a restricted donation for missions

| Account | Debit | Credit |

|---|---|---|

| Cash | X | |

| Contribution revenue with donor restrictions | X |

Example 2. Spend that mission money on approved trip costs

| Account | Debit | Credit |

|---|---|---|

| Mission trip expense | X | |

| Cash | X |

These entries are simple on purpose. They show the flow. The gift is recorded in the donor-restricted category when received. The later expense shows how the church used cash for the mission purpose. At reporting time, the treasurer can then present both the expense activity and the remaining balance tied to that purpose.

That is the part many new bookkeepers miss. The journal entry is not the finish line. It is the first sentence in the report the board will read later.

Why software structure matters

Churches often use one bank account for practical reasons. That is not the problem. The problem starts when the ledger cannot clearly separate general funds from donor-restricted funds, or when reporting depends on manual spreadsheet sorting at month-end.

A church-specific accounting setup helps because the fund structure is built into the transaction from the start. If a mission gift is coded to the proper fund on day one, the Statement of Activities and fund balance reporting are much easier to prepare at month-end. If it is posted to a generic income account and sorted out later, errors spread quickly. One miscoded receipt can make a board report confusing and can leave the treasurer explaining numbers instead of presenting them.

Grain is one example of software built around native fund accounting for churches. That matters because each transaction, account, and report can stay tied to the right fund from the beginning. For a practical walkthrough of how ledger activity turns into leadership reporting, see this guide on preparing church financial reports from the ledger to leadership use.

Clean board reports begin when the original transaction is coded correctly.

What a board wants to see

Board members usually do not need more accounting terms. They need a report package they can trust at a glance.

A useful set of reports helps them see:

- Current financial position across the whole church

- Fund balances for missions, building, benevolence, and other designated purposes

- Activity by fund during the month or quarter

- Expense groupings that reflect actual ministry work

That is where GAAP and church practice meet in a very practical way. GAAP gives the reporting rules. Fund accounting gives the church a way to apply those rules to real ministry decisions. When the bookkeeping is structured well, the board can answer simple but important questions with confidence: What do we have, what is restricted, and what can we spend?

Avoiding Common Mistakes in Church Accounting

Churches usually don't get into trouble because they ignored stewardship. They get into trouble because they assumed a common shortcut was “close enough.” In GAAP work, close enough often isn't enough.

The traps that catch churches

Commingling cash and calling it solved

Using one bank account doesn't automatically create a compliance problem. Using one bank account without reliable ledger tracking does. If the church can't show what portion belongs to which purpose, the reports stop being trustworthy.

Treating all salaries as administrative

Church staff often wear multiple hats. A children's director may spend time in program work, planning, and administration. Functional expense reporting works best when payroll reflects what people do, not a convenient shortcut.

Ignoring accrual items

A church that waits only for cash movement may miss receivables, pledges, unpaid obligations, and qualifying in-kind activity. That makes reports easier to prepare, but less accurate.

The footnote issue many treasurers miss

One overlooked area is donated services. GAAP still limits when services are recorded as revenue, but there is also a disclosure requirement that many church leaders miss. A newer standard requires qualitative disclosure of all donated services received, including those not recorded as revenue, and that disclosure should describe the programs supported and the valuation technique used, as noted in Optima Office's discussion of GAAP for nonprofits.

That matters for churches with heavy volunteer involvement. You may not book every volunteer hour as revenue. You may still need to disclose the nature of donated services in the notes.

A short prevention checklist

- Document donor intent clearly: Save envelopes, memos, online giving designations, and correspondence.

- Review coding before month-end: Fix untagged or misclassified entries while the context is fresh.

- Allocate shared costs carefully: Especially payroll, occupancy, and ministry support costs.

- Keep support for non-cash gifts: Valuation and use documentation should stay with the transaction.

- Build internal checks: Separate approval, payment, and reconciliation duties when possible.

Small coding habits become big reporting problems if no one catches them early.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Your GAAP Questions Answered

Is a church event ticket a donation or earned revenue

Ask whether the attendee received commensurate value. If someone pays for a concert ticket, retreat registration, or a branded T-shirt, that may be an exchange transaction rather than a contribution. Misclassifying this kind of revenue can create Form 990 inaccuracies and audit issues, as explained in this discussion of nonprofit accounting standards.

How should a church report investment income

Report investment income carefully and follow the applicable GAAP presentation rules. One technical point many treasurers miss is that investment income should be reported net of both external and internal management fees, so the reported return reflects the true economic benefit available to the church.

What about volunteer hours that don't qualify for revenue recognition

Don't assume “not recorded” means “not reported at all.” If donated services don't meet the recognition test for revenue, the church may still need qualitative disclosure in the footnotes describing the programs those services supported and how value was assessed.

Should every grant or major restricted purpose have its own fund

For churches with active grants or major designated purposes, that's a sound practice. Separate funds make reporting cleaner, help preserve donor intent, and reduce confusion during reviews and audits.

What's the simplest way to think about GAAP accounting for nonprofits

Think of it this way: GAAP helps your church tell the financial truth in full. Not just how much cash is in the bank, but what that money is for, what obligations exist, what support was promised, and how ministry resources were used.

If your church needs fund-based reports that match how ministry money functions, Grain is worth a close look. It's designed for church accounting, so restricted and unrestricted activity, fund balances, and board-ready financials are built into the structure rather than added through workarounds.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.