How to Audit Church Financial Records in 2026

How to audit church financial records - Learn how to audit church financial records with our step-by-step guide. Covers internal controls, fund accounting,

You’re probably staring at a stack of statements, donation reports, receipts, and login screens from several systems that don’t quite agree with each other. The bank says one thing. The giving platform says another. The accounting file looks close, but not close enough to sign off with confidence.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

That’s a normal place for a church to be before an audit.

Learning how to audit church financial records isn’t about creating fear around money. It’s about proving stewardship. A good church audit shows that gifts were received, recorded, deposited, classified, and spent the way leaders and donors expected. In a small or medium-sized church, that work usually happens with limited staff, volunteers wearing multiple hats, and a mix of paper records and digital tools. That combination is exactly why the process needs to be clear and disciplined.

The biggest mistakes I see are rarely dramatic. They’re ordinary. One person opens the mail, records the gifts, makes the deposit, and posts the entry. A building fund lives partly in the accounting system and partly in a spreadsheet. Online gifts from Planning Center, Pushpay, or Stripe hit the bank in batches, but no one can easily show which donor amounts make up the transfer. None of that means fraud happened. It does mean your audit has to test carefully.

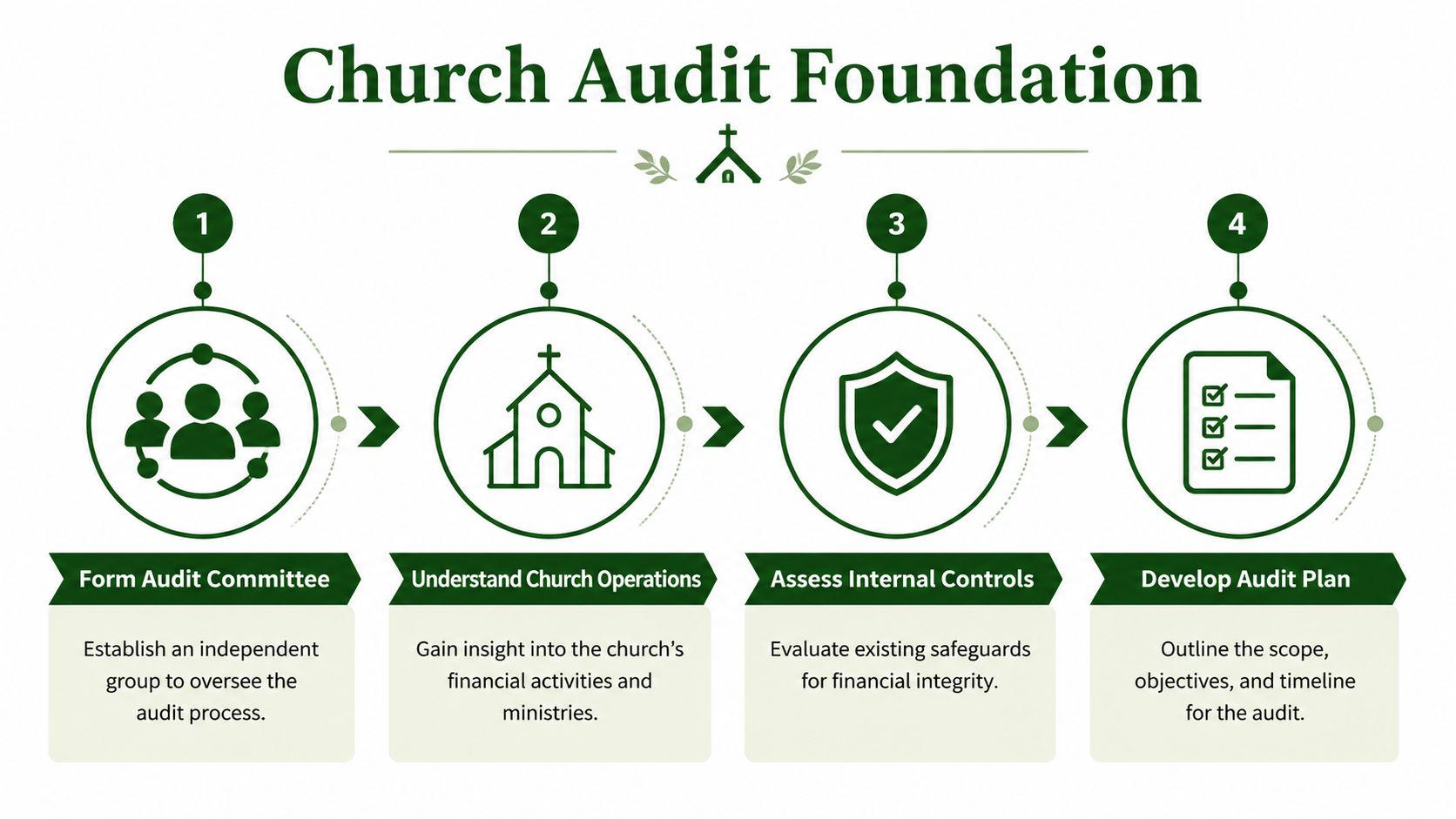

Preparing for the Audit and Assessing Internal Controls

Most church audits go wrong before anyone tests a transaction. They go wrong when the church starts with a vague scope, a conflicted review team, or incomplete records.

For a small to medium-sized church, the usual model is a committee-based internal audit with 2 to 3 independent members. That standard approach matters because weak controls are where many problems start. Nonprofit fraud studies cited in a church audit training resource note that 70% of church frauds stem from weak internal controls like poor segregation of duties, and an annual audit can reduce this risk by 50-60% (church audit committee guidance).

Form an independent audit committee

Independence doesn’t mean the committee has no church knowledge. It means the people reviewing the records shouldn’t be the same people who handle the daily money flow.

A workable committee often includes:

- One financially literate member who can read statements, bank reconciliations, and ledgers

- One operationally aware member who understands how offerings, reimbursements, and ministry spending happen

- One independent reviewer who asks simple questions and notices gaps others overlook

Avoid placing the treasurer, bookkeeper, finance secretary, or anyone who signs checks on the audit committee. If your volunteer base is thin, choose people outside the weekly finance workflow and document any limitations clearly.

Practical rule: If someone can create, approve, and record the same transaction, the church has a control weakness that the audit should flag.

Gather documents before the first meeting

A church audit stalls when the committee spends its first session hunting for files. Collect everything first, then review.

Use a pre-audit packet that includes:

- Bank records for every operating, savings, reserve, and designated account, plus reconciliations

- Credit card statements and supporting receipts

- Financial statements for the audit period and recent months around year-end

- General ledger detail by account and by fund

- Donation records from online giving platforms and any in-person contribution system

- Deposit support such as batch reports, counting sheets, and deposit slips

- Invoices and expense support for disbursements, reimbursements, and vendor payments

- Payroll records and approved compensation documentation

- Board or finance committee minutes showing approvals for budgets, major purchases, loans, and designated uses of funds

- Loan and investment statements

- Fixed asset records if the church tracks equipment, vehicles, or capital purchases

- Prior audit reports and any unresolved recommendations

Churches that prepare this packet ahead of time usually move faster and produce a better result. If your records are spread across email attachments, paper folders, and disconnected apps, that’s a finding in itself.

Review internal controls before testing numbers

An audit isn’t just a hunt for math errors. It’s a review of the system that produced the numbers.

Start with basic questions:

- Who receives and counts offerings?

- Who prepares the deposit?

- Who records the contribution?

- Who reconciles the bank account?

- Who approves bills?

- Who signs checks or releases ACH payments?

- Who can edit donor designations or change chart-of-account mappings?

If the same name appears repeatedly, the church needs compensating controls. In a small church, full segregation isn’t always possible, but oversight still is. The pastor or finance chair can review monthly reports. A second person can open the mail. Someone outside bookkeeping can compare giving platform totals to bank deposits. The board can review restricted fund activity regularly.

For a broader framework, it helps to compare your process with practical internal audit best practices used in other organizations. The exact structure differs in churches, but the principles hold up: independence, documentation, review trails, and clear accountability.

Treat fund accounting as a control, not just a reporting preference

Many churches underestimate risk, believing fund accounting is only for year-end statements. It isn’t. It’s an internal control.

A church usually handles several kinds of money at once:

- Operating funds used for general ministry expenses

- Board-designated funds set aside by leadership for a purpose

- Restricted funds given by donors for a specific purpose

If those categories aren’t separated from the start, the audit becomes a reconstruction exercise. The committee has to infer intent after the fact, often from memo lines, spreadsheets, and memory. That’s unreliable.

A church can have accurate total cash and still have poor accountability if it can’t prove which dollars belong to which purpose.

Systems built around church workflows help because they reduce reclassification work later. If you’re reviewing whether your controls are strong enough, it’s worth seeing how church internal control practices handle approvals, segregation of duties, and fund-level visibility in day-to-day bookkeeping.

Set the audit scope and timeline

Keep the scope explicit. An internal church audit usually covers:

- Cash receipts

- Donations and donor restrictions

- Disbursements

- Payroll

- Balance sheet accounts

- Internal controls

- Compliance with board-approved financial practices

Then set a realistic timeline. Many churches can complete the work in two working sessions if the records are organized. The first session reviews documents and controls. The second tests transactions and drafts findings. If records are messy, stop pretending it’s a two-meeting project and expand the timeline. Rushing an audit produces a false sense of comfort.

Testing Income Donations and Expense Transactions

Transaction testing is where the audit shifts from policy to proof. You’re no longer asking whether the church has a process. You’re asking whether the process worked on real money.

Start with income. Cash coming into a church is usually more complicated than leaders assume. A single week might include offering envelopes, loose cash, checks, ACH gifts, card gifts, and platform payouts from services designed to simplify church giving. The more methods a church accepts, the more disciplined the audit trail has to be.

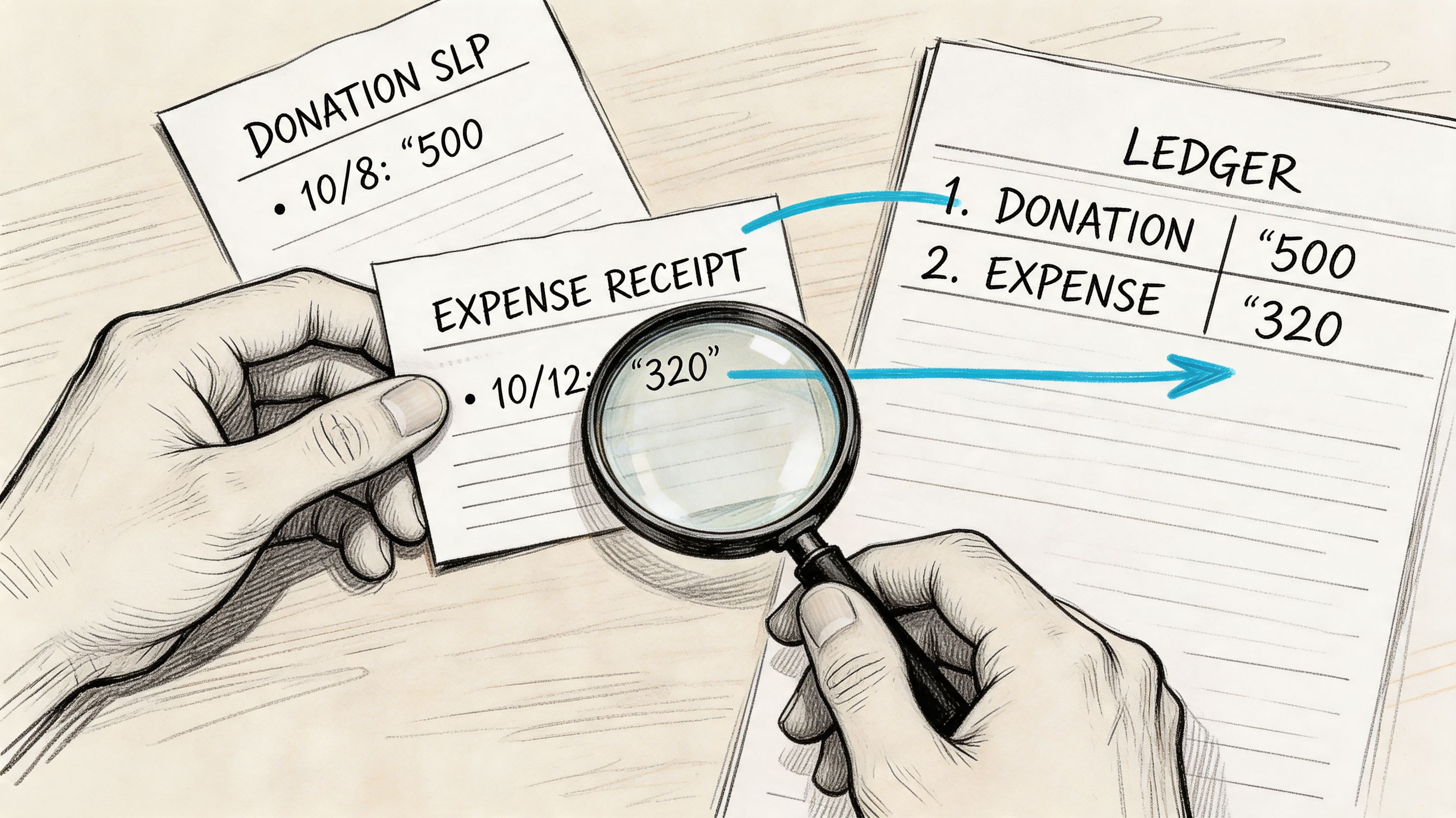

Trace donations from source to ledger

The cleanest way to test income is to trace one gift all the way through the system.

For an in-person gift, follow this chain:

- Donation source, such as envelope, check copy, or counting sheet

- Deposit batch or deposit slip

- Bank statement deposit

- General ledger entry

- Donor contribution record

- Fund classification

For a digital gift, the sequence usually looks different:

- Giving platform transaction record

- Platform batch or payout report

- Bank deposit

- Accounting entry

- Fund assignment

- Donor statement detail

This is why bank reconciliation carries so much weight. Bank reconciliation is the single most effective procedure for detecting financial discrepancies, and Grain’s 2026 checklist describes validating every deposit, withdrawal, and fee against the general ledger as a core fraud detection tool. The same source notes that errors are found in 20-30% of churches still using manual entry systems (bank reconciliation checklist for church auditors).

How to sample income without checking everything

You don’t need to test every transaction in a routine internal audit. A practical approach is to sample ordinary items and fully review unusual or higher-risk items.

Choose samples from different categories:

- Weekly offerings from ordinary Sundays

- Large seasonal giving periods such as Christmas or year-end

- Online gift batches that combine many donors into one deposit

- Restricted gifts with donor instructions

- One-off events like special offerings or fundraisers

Don’t just sample neat transactions. Pull a few awkward ones. Pick a batch that crossed month-end. Pick a digital payout net of fees. Pick a donation that was later reclassified. Those are the records that show whether the church really understands its own process.

Red flags in income testing

- Deposit dates that lag without explanation

- Batch totals that match the bank but not the donor records

- Online giving deposits posted to one generic income account and sorted out later in spreadsheets

- Missing count sheets or unsigned deposit support

- Donor-restricted gifts recorded as general offerings

Digital giving needs extra scrutiny because the church rarely receives one bank deposit per donor gift. Platforms may combine transactions, subtract fees, and transfer net amounts on a delay. If the accounting entry just mirrors the bank without tying back to the underlying donor activity, the audit trail is weak.

A good audit asks one hard question: can the church prove how a batched deposit in the bank maps back to individual gifts and their intended funds? If the answer is “mostly,” keep testing.

For churches working through that problem, donation tracking software guidance for churches is useful because it frames the issue correctly. The challenge isn’t only collecting gifts. It’s preserving a traceable record from donor intent to final ledger entry.

Test expenses by following authorization and support

Expense testing is less about whether the church spent money and more about whether it spent money properly.

Take each sampled disbursement and inspect:

- The invoice, receipt, or reimbursement support

- Evidence of approval

- Correct payee

- Correct date and accounting period

- Proper account coding

- Proper fund coding

- Whether the payment method matched policy

The strongest expense files tell a simple story. The church approved the purchase. The church received the goods or service. The payment matched the support. The transaction hit the right fund and account.

The weakest files usually have one of these patterns:

- A credit card statement with no itemized backup

- Reimbursements with no ministry purpose listed

- A check signed before documentation was complete

- Vendor payments approved by the person receiving the benefit

- Expenses posted to a restricted fund because that fund had cash available

Don’t ignore payroll and recurring payments

Payroll often gets skipped in internal church audits because leaders assume the payroll processor handled everything. That’s not enough. The audit should still verify that pay rates, housing allowances if applicable, approved compensation, and payroll entries agree with board authorizations and the books.

Recurring payments deserve attention too. Streaming subscriptions, software renewals, mission support drafts, copier leases, and utility autopays can drift for months without active review.

This walkthrough can help reviewers visualize how to inspect those flows in practice.

Missing paperwork isn’t a minor annoyance. In an audit, missing support means the church cannot prove the transaction was valid.

What works and what does not

What works is boring, and that’s good. Standardized counting sheets. Consistent deposit procedures. Approval records kept with invoices. Donation imports reviewed before posting. Monthly review by someone outside transaction entry.

What does not work is patching together the trail after year-end. If a church has to ask, “Does anyone remember why this was posted to missions?” the accounting record already failed the audit test.

Reconciling Key Accounts and Verifying Restricted Funds

Reconciliation is where an audit proves the books, not just the process. A church can record transactions all year and still end up with unreliable financial statements if the balances weren’t reconciled carefully.

That’s especially true in churches using several connected systems. The bank holds the cash. The giving platform holds donor-level detail. The accounting software holds the official books. If those three records drift apart, the church can report the right total in the wrong place, or the wrong total with complete confidence.

Reconcile every cash-related account

Start with the bank account because cash is the easiest asset to misuse and the easiest place to verify.

A proper reconciliation compares:

- Statement ending balance

- Outstanding checks or payments

- Deposits in transit

- Book balance in the ledger

- Any unexplained bank fees or adjustments

This isn’t mechanical box-checking. You’re evaluating whether the reconciling items make sense. A deposit in transit should clear soon. An old outstanding check may need follow-up. Repeating “miscellaneous adjustment” entries usually mean someone is forcing the books to agree instead of explaining differences.

If your committee wants a cleaner way to read statement layouts and reconcile line items systematically, this guide to bank statement format is a useful practical reference.

Beyond bank accounts, reconcile:

- Credit cards to statements and underlying receipts

- Loans to lender statements and board approvals

- Savings or reserves to account statements and internal designations

- Clearing accounts used for merchant processing or payroll timing

One neglected account can distort several reports at once. I’ve seen churches spend hours reviewing expense categories while leaving an old clearing balance untouched for months. That’s backwards. Reconciliations should come before interpretation.

Reconcile digital giving to actual cash movement

Modern church audits diverge from generic nonprofit guidance; online giving introduces timing differences, fees, refunds, and batch transfers that aren’t obvious on the face of the bank statement.

Take one payout from Planning Center, Pushpay, Stripe, or another processor and prove these points:

- The total donor activity matches the platform report.

- Any fees or reversals are separately identifiable.

- The net deposit matches the bank.

- The ledger records gross giving, fees, and net cash correctly.

- Each gift was posted to the correct fund.

If you can’t do that, the church doesn’t have a complete audit trail for digital giving.

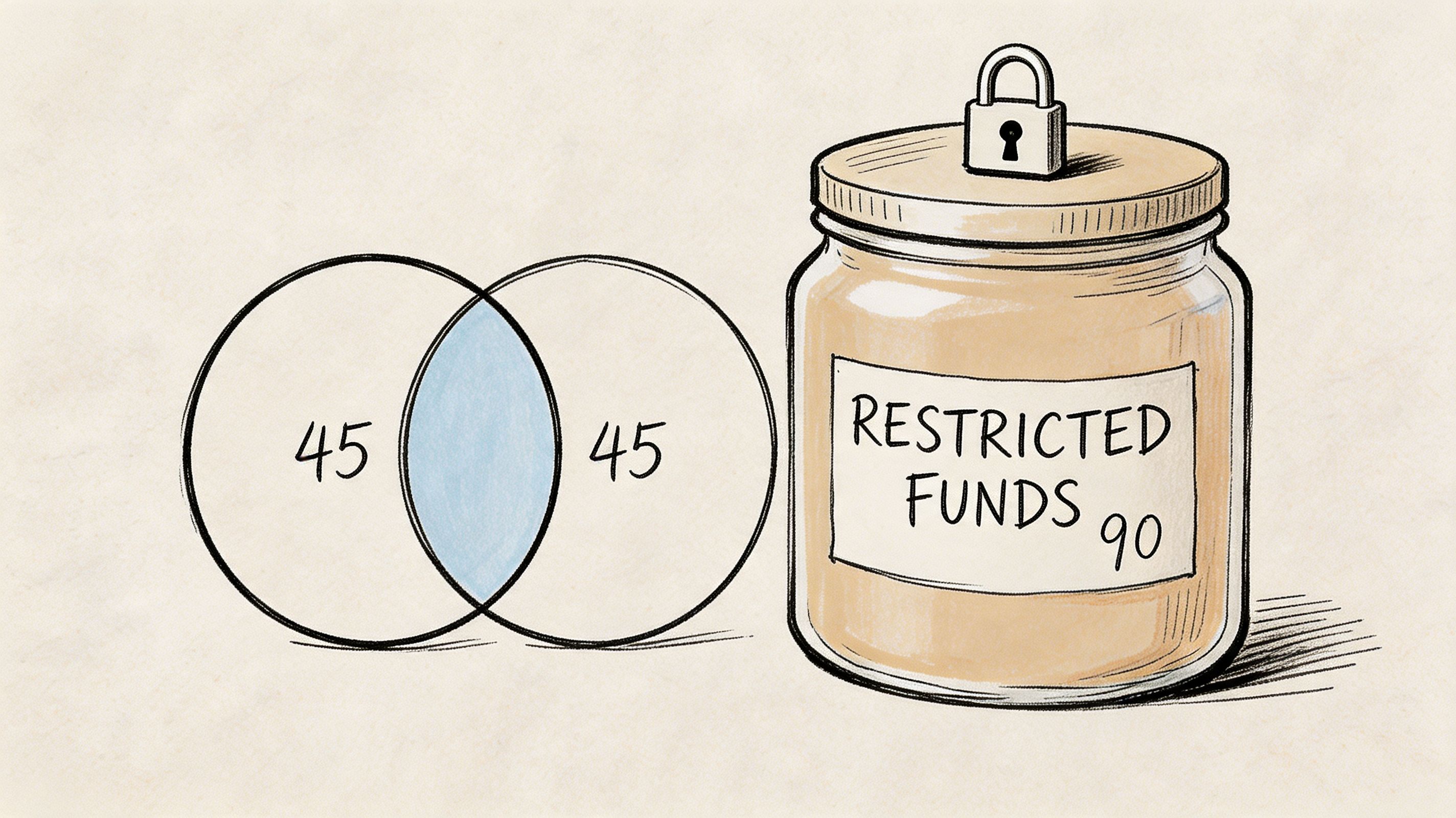

Restricted funds are where trust is tested

Churches can recover from coding mistakes in office supplies. They don’t recover as easily from restricted fund confusion.

A 2023 Church Law & Tax survey found that 42% of churches mishandle restricted donations, often because their giving platform and accounting system sit in separate software silos (church restricted donation audit concerns). That problem usually shows up as commingling. The bank balance is fine, but the church can’t clearly prove which portion belongs to building, benevolence, missions, or another donor-directed purpose.

Consider a building campaign. Members give over several months. Some gifts arrive by check with “building fund” in the memo. Others come through online forms with a campaign designation. A few are manually adjusted after deposit because someone selected the wrong option. Then the church pays an architect invoice, a permit fee, and later a general maintenance bill from the same operating account.

The audit question isn’t whether those payments were real. It’s whether the church can prove that only qualifying building expenses reduced the building fund balance. Spreadsheets make this fragile because the connection between donor intent and expenditure is often maintained outside the accounting system. One formula error or missed update can break the chain.

A restricted fund is not “money we hope to use that way.” It is money the church must be able to account for that way.

Why fund-native systems change the audit workload

When the books are maintained in a true fund structure, the audit gets simpler because the classification work happens at entry, not at year-end cleanup. The committee can review fund activity reports, trace a gift to a fund, and inspect whether the related disbursement came from that same fund with support for purpose.

That’s one reason some churches move away from spreadsheet-heavy workflows or generic small business accounting setups. Among church-specific options, Grain Ledger uses a native fund architecture and connects banks and giving providers such as Planning Center, Pushpay, and Stripe so transactions can be organized around funds from the start. If your committee is evaluating how restricted money should be tracked, this explanation of what a restricted fund is in church accounting gives the right conceptual baseline.

What auditors should conclude in this area

Your audit should be able to answer yes or no to these questions:

- Are all cash and credit-related accounts reconciled to external statements?

- Do online giving reports tie to deposits and ledger entries?

- Are fees, refunds, and timing differences visible?

- Can the church show a complete trail for each major restricted fund?

- Do restricted fund expenses align with donor intent?

If the answer is no on any one of those, don’t soften it. Write the finding clearly. This is one of the few areas where “close enough” causes real governance damage.

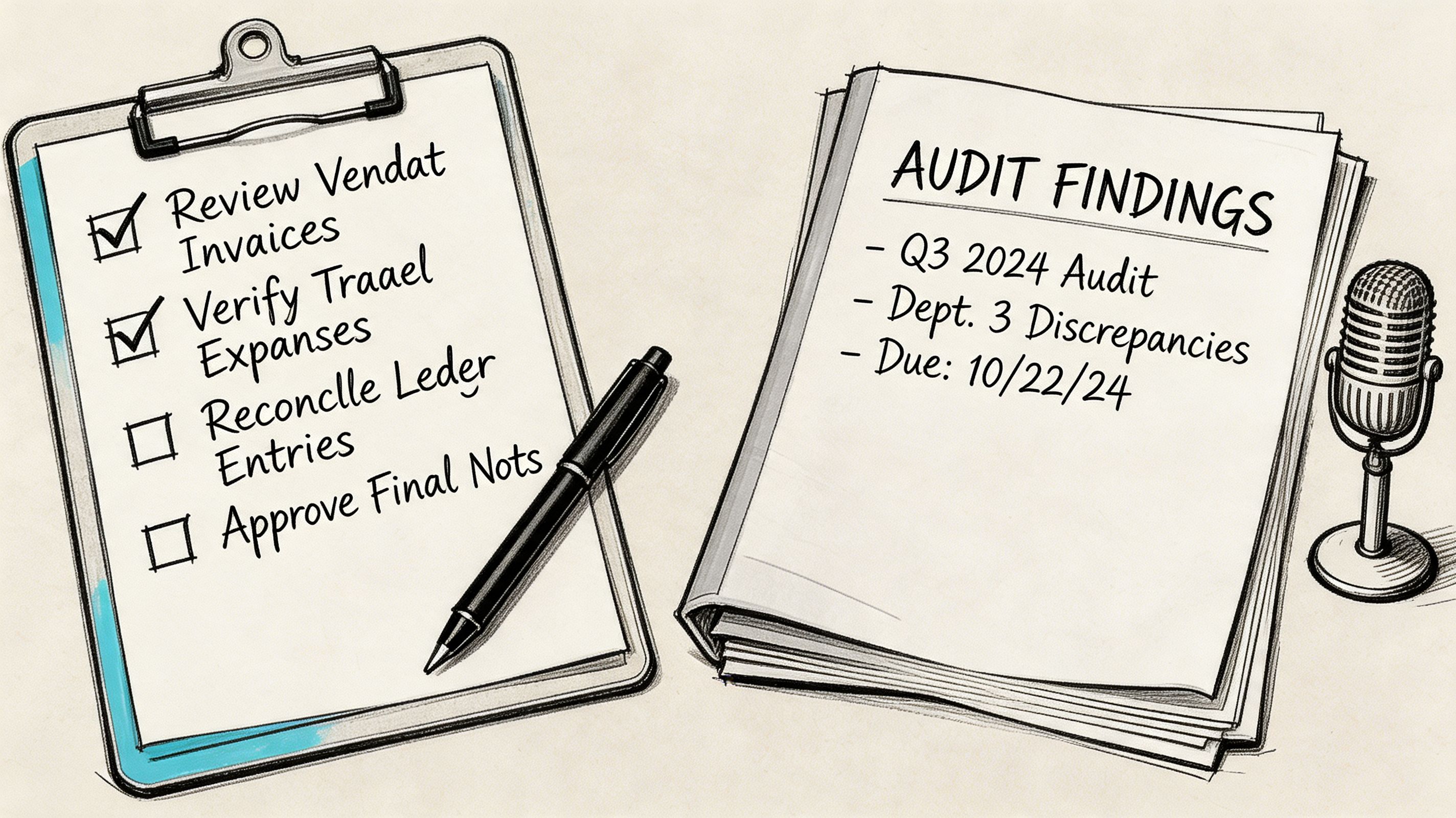

Your Actionable Church Audit Checklist

A church audit becomes manageable when the work is reduced to clear tasks. Annual review is the norm, and best-practice guidance says routine transaction testing should include 20-30% sampling, while audited churches report an 85% boost in donor confidence and 40% fewer discrepancies. The same guidance notes that integrated software can cut audit prep time by over 40% (church audit checklist benchmark).

Use this as a working paper, not just a reading tool.

| Category | Task | Status (Done/NA) |

|---|---|---|

| Pre-audit documentation | Confirm audit period and committee independence | |

| Pre-audit documentation | Gather bank statements for all accounts | |

| Pre-audit documentation | Gather monthly bank reconciliations | |

| Pre-audit documentation | Gather credit card statements and receipts | |

| Pre-audit documentation | Gather year-end and monthly financial statements | |

| Pre-audit documentation | Gather general ledger detail by account and fund | |

| Pre-audit documentation | Gather giving platform reports and donor logs | |

| Pre-audit documentation | Gather deposit slips, count sheets, and batch reports | |

| Pre-audit documentation | Gather invoices, reimbursement forms, and approvals | |

| Pre-audit documentation | Gather payroll reports and compensation approvals | |

| Pre-audit documentation | Gather board and finance committee minutes | |

| Internal control assessment | Identify who handles offerings, deposits, posting, approvals, and reconciliations | |

| Internal control assessment | Note any segregation-of-duties conflicts | |

| Internal control assessment | Verify that someone independent reviews monthly financials | |

| Internal control assessment | Confirm user access is appropriate for finance systems | |

| Income and donation testing | Sample routine donation batches | |

| Income and donation testing | Trace sampled gifts from source record to deposit and ledger | |

| Income and donation testing | Verify digital giving batches to bank deposits | |

| Income and donation testing | Confirm donor restrictions were recorded correctly | |

| Expense and disbursement testing | Sample vendor payments and reimbursements | |

| Expense and disbursement testing | Match each payment to invoice or receipt | |

| Expense and disbursement testing | Verify approval for each sampled expense | |

| Expense and disbursement testing | Confirm account and fund coding are correct | |

| Balance sheet review | Reconcile every bank account to statement balances | |

| Balance sheet review | Review old outstanding checks and unusual reconciling items | |

| Balance sheet review | Reconcile credit cards, loans, and savings balances | |

| Restricted funds compliance | Review activity for each major restricted fund | |

| Restricted funds compliance | Match restricted disbursements to the stated ministry purpose | |

| Restricted funds compliance | Confirm no restricted balances were used for unrelated expenses | |

| Reporting | Document findings, exceptions, and recommendations | |

| Reporting | Present final report to board or finance leadership |

Print it, assign initials, and keep it with the audit file. A checklist only helps if someone owns each item.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Documenting Evidence and Reporting Audit Findings

An audit that isn’t documented won’t hold up six months later when someone asks, “How did you verify that?” Memory is not evidence. A clean audit file is evidence.

That file should include the signed checklist, sample selections, copies of reconciliations reviewed, screenshots or printouts from giving platforms, invoice support, notes on interviews, and a summary of each exception. Keep the documentation simple enough that a new finance chair could follow it without a narrator.

Build an audit file that another person can follow

The standard I use is straightforward. If another reviewer opened the file next year, could that person understand what was tested, what was found, and why the committee reached its conclusions?

Organize the file in sections:

- Planning documents such as committee membership, period covered, and scope

- Control review notes showing who performs which finance tasks

- Testing support for income, expenses, reconciliations, payroll, and restricted funds

- Exception log with unresolved items, explanations, and follow-up needs

- Final report approved by the committee

Write findings in plain language

Audit reports lose value when they sound accusatory or overly technical. Most church boards don’t need accounting jargon. They need clarity.

A useful report usually includes:

Scope

State the period reviewed and the areas examined.Method

Briefly note that the committee reviewed documents, assessed controls, and tested selected transactions.Positive observations

Note what the church is doing well. This helps leaders distinguish between isolated fixes and systemic concerns.Findings

Describe each issue plainly. Example: “Online giving deposits were recorded in total, but the church could not consistently show how individual donor designations mapped to fund postings.”Recommendations

Keep them specific. Assign responsibility where possible.Management response or next steps

Record what leadership agreed to change and by when.

The best audit reports don’t just identify problems. They give the board a manageable path to fix them.

Present the report as stewardship, not accusation

Tone matters. If the committee sounds like it is prosecuting volunteers, people get defensive and the church learns nothing. If the committee minimizes real control failures to protect feelings, the church also learns nothing.

Use language that is firm and constructive. Say “the process needs a second reviewer,” not “the secretary caused a control breakdown,” unless misconduct is present. Distinguish between documentation weakness, control weakness, and misstatement. Those are not the same problem.

When the board receives a report with evidence, plain explanations, and practical fixes, confidence rises. Leaders can act on it. Donors benefit from it. Staff and volunteers know what to change before the next cycle.

That’s the essential value of learning how to audit church financial records well. The audit doesn’t exist to produce a binder. It exists to make the church’s financial life more trustworthy next month than it was last month.

If your church is trying to tighten audit trails around digital giving, bank reconciliation, and restricted funds, Grain is worth a look. It’s church accounting software built around true fund-based accounting, with fund-level reporting and integrations for banks and giving providers so your records are easier to trace and easier to review during an audit.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.