Indirect Cost Allocation: A Church Finance Guide for 2026

Learn indirect cost allocation for churches. Our guide covers methods, fund accounting rules, and best practices to ensure compliance and clear reporting.

The month-end close is almost done. The youth ministry bought supplies for Wednesday night. The food pantry paid for extra refrigeration. Worship added a streaming subscription after upgrading cameras and encoders for churches. Then the utility bill hits the inbox, along with insurance, payroll for the office administrator, and the copier lease.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Start free to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

That's the moment many church treasurers stall out.

Everyone used the building. Everyone relied on the office. Several ministries benefited from the same internet connection, staff support, and facility costs. But whose budget should carry those shared expenses? If a church has designated gifts, board-restricted funds, or donor-restricted funds, the question gets even more sensitive.

Indirect cost allocation sounds technical, but the issue is pastoral as much as financial. Churches aren't just trying to “spread overhead.” They're trying to honor donor intent, present honest reports, and avoid shifting costs in ways that make one ministry look healthier than it really is.

A lot of churches first notice this problem when trying to cut crowdfunding campaign costs or tighten ministry budgets. Reducing expenses helps, but some costs will always remain shared. The essential stewardship question is how to assign them fairly.

Why Church Finance Teams Must Understand Shared Costs

A church can look busy and fruitful while its accounting tells the wrong story.

The missions team may appear under budget because the general fund absorbed more building and admin expense than it should have. The children's ministry may seem expensive because its direct purchases are tracked carefully while shared office support is ignored everywhere else. A benevolence fund may look untouched, even though staff members spent real time administering it.

Shared costs shape ministry reports

Most church leaders don't argue about direct expenses. If the student ministry buys snacks for camp, that's a student ministry expense. If the church pays a guest missionary honorarium from a missions fund, that's easy too.

Confusion starts with the costs that support everything at once:

- Facilities costs like electricity, cleaning, and maintenance

- Administrative support like bookkeeping, office supplies, and receptionist time

- Technology costs like internet, shared software, and phone service

- Leadership overhead when one staff member serves multiple ministries

Those costs are real. If they disappear into a vague “operations” bucket, ministry reports stop reflecting actual resource use.

Practical rule: If several ministries benefit from an expense and you can't trace it cleanly to just one, you're probably dealing with a shared cost that needs a consistent allocation approach.

Stewardship is the real issue

Churches don't allocate shared costs just to satisfy accountants. They do it because financial honesty matters.

When reports are incomplete, leaders make poor budget decisions. They may expand a ministry without understanding its full support cost. They may compare ministries unfairly. They may also drift into risky territory by charging overhead to funds that were given for a specific purpose.

That's why indirect cost allocation belongs in regular church finance practice, not just in grant compliance or audit prep. It helps the board, the treasurer, and ministry leaders answer one simple question with integrity: what did this ministry really cost?

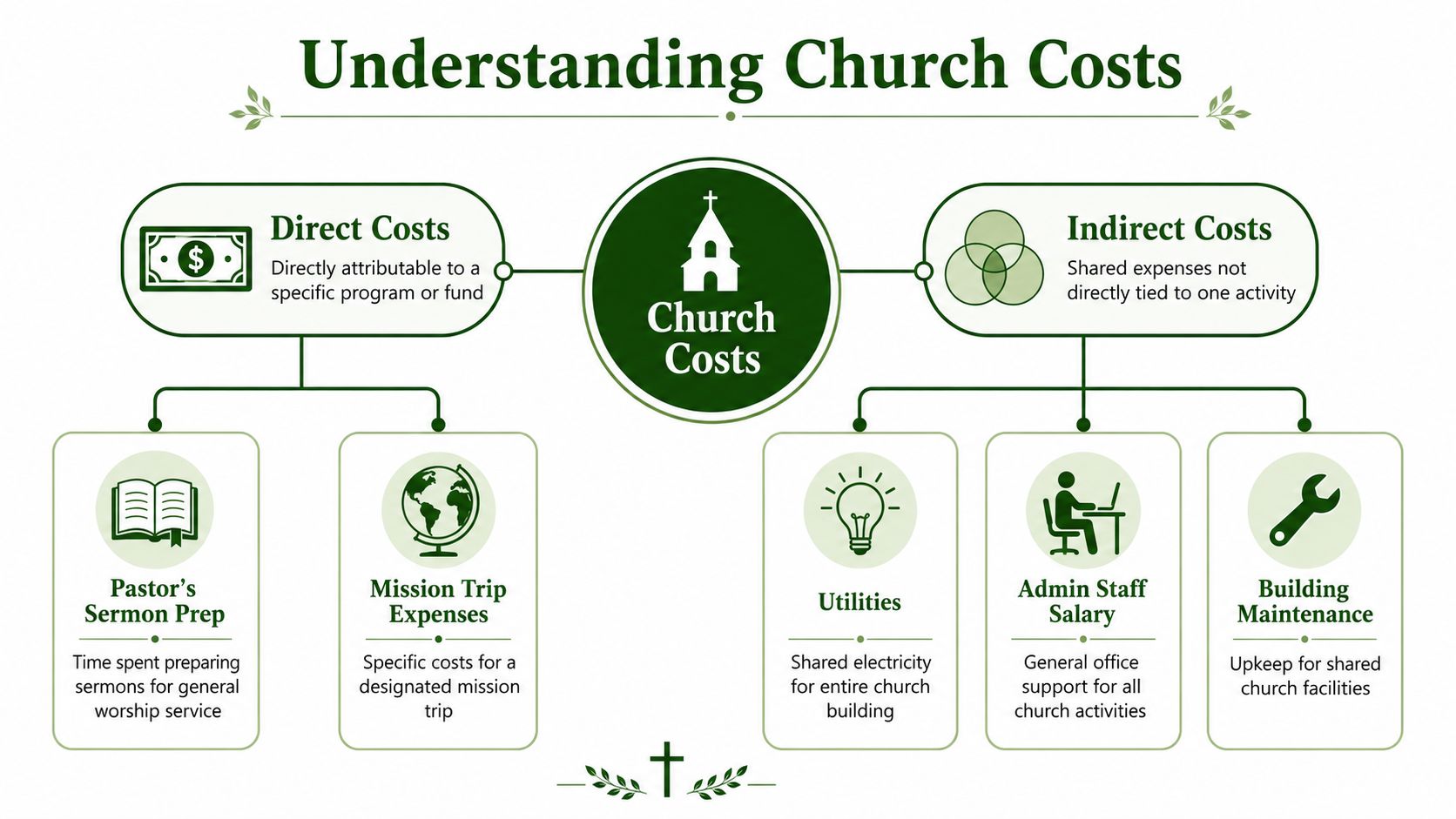

Direct vs Indirect Costs in a Church Setting

Before a church can allocate anything, it has to sort expenses into the right bucket.

Think of a shared house. If one roommate buys steak for a dinner party they alone are hosting, that's a direct cost. If the whole house uses electricity, rent, and laundry detergent, those are indirect costs. Church accounting works the same way.

What counts as a direct cost

A direct cost can be traced to one ministry, program, or fund without guesswork.

Examples in a church might include:

- Children's curriculum bought only for the children's ministry

- Mission trip airfare paid for a designated trip

- Retreat lodging for a specific youth event

- Worship sheet music purchased for the worship ministry

If you can point to the expense and say, “This was clearly for that one activity,” it's direct.

What counts as an indirect cost

An indirect cost supports multiple ministries or church-wide functions. You can't assign it to one program without using a method.

That often includes rent or mortgage-related occupancy costs, utilities, insurance, office software, general admin salaries, and building maintenance. Some salaries are mixed. A pastor or administrator may spend part of their time on one program and part on broader church operations. That's where churches need careful judgment and documentation.

A standard way to express overhead is through an indirect cost rate. RCAC explains indirect cost rate calculation this way: divide the total pool of indirect costs for the fiscal year by a chosen cost base. Their example uses an indirect cost pool of $150,000 and a direct base of $1,000,000, which produces a 15 percent rate.

Cost pools make the process manageable

Churches get overwhelmed when they try to allocate every shared bill individually. A better approach is to group similar expenses into cost pools.

Common church cost pools include:

| Cost Pool | Typical Expenses | Common Logic |

|---|---|---|

| Facilities | Utilities, maintenance, insurance, janitorial | Shared building use |

| Administration | Bookkeeping, office supplies, admin software | Support for all ministries |

| Technology | Internet, phone, shared platforms | Church-wide access |

| Leadership support | Broad supervisory or operational oversight | Benefit across functions |

A cost pool is just a bundle of related indirect costs that will be allocated using a sensible base.

If the expense benefits more than one ministry, don't force it into one budget line just because that's easier in the moment.

That discipline matters more as a church grows. The larger the building, staff team, and ministry mix, the easier it is for shared costs to distort reports.

Comparing Common Indirect Cost Allocation Methods

Churches often ask for the one best method. There isn't one. Different expenses call for different bases.

That's why the strongest allocation plans don't rely on a single percentage for everything. Wegner notes that a single fixed percentage approach can be the least accurate method, while activity-based or multi-base approaches reduce allocation error by 25–30% in complex nonprofit environments.

The main methods churches use

Three methods show up most often in church settings.

Square footage

This method works well for expenses tied to the building itself. Rent, utilities, custodial services, and maintenance usually fit here.

If a counseling ministry regularly occupies a suite of offices and the children's ministry uses a large wing, square footage can provide a reasonable way to divide facilities costs. The challenge is measurement. Shared hallways, kitchens, and multipurpose rooms can complicate the math. If your building has unusual layouts, this guide to calculating irregular space dimensions can help your team measure more consistently.

Employee count or FTEs

This method suits administrative support costs. If office staff, HR work, payroll support, or general admin effort rises as staffing rises, employee count can be a fair base.

It's often cleaner than trying to estimate every minute of admin help by ministry. Still, it can overstate support for ministries with many part-time workers or understate support for ministries that generate heavy paperwork with fewer people.

Direct cost base

This method allocates overhead according to each ministry's share of direct spending. It's practical when a church wants a broad, understandable method for certain admin pools.

This approach is easy to calculate, but it assumes ministries with higher direct spending also consume more overhead. Sometimes that's true. Sometimes it isn't. A ministry with modest purchases may still generate lots of scheduling, communication, and finance work.

Indirect Cost Allocation Method Comparison

| Method | Best For Allocating | Pros | Cons |

|---|---|---|---|

| Square footage | Rent, utilities, maintenance, occupancy-related insurance | Closely matches facility use when rooms are dedicated | Harder when space is shared or changes often |

| Employee count or FTEs | Admin salaries, HR support, general office overhead | Simple and understandable for staff-driven support costs | Can miss differences in workload between ministries |

| Direct cost base | General administrative pools where spending roughly tracks support needs | Easy to compute and repeat monthly | Can distort costs if spending doesn't reflect actual benefit received |

Why one flat rate usually causes trouble

A church might be tempted to charge every ministry the same overhead percentage because it feels tidy. Tidy isn't the same as fair.

Facilities costs behave differently from office support. Shared software behaves differently from custodial work. A flat percentage can hide overcharging in one area and undercharging in another. That makes reports less useful and harder to defend if leaders, donors, or auditors ask how the numbers were assigned.

One helpful companion document for this conversation is a church's statement of functional expense. It pushes finance teams to think carefully about how spending supports different functions, not just departments.

Good indirect cost allocation doesn't chase perfection. It looks for a method that is reasonable, repeatable, and tied to actual use.

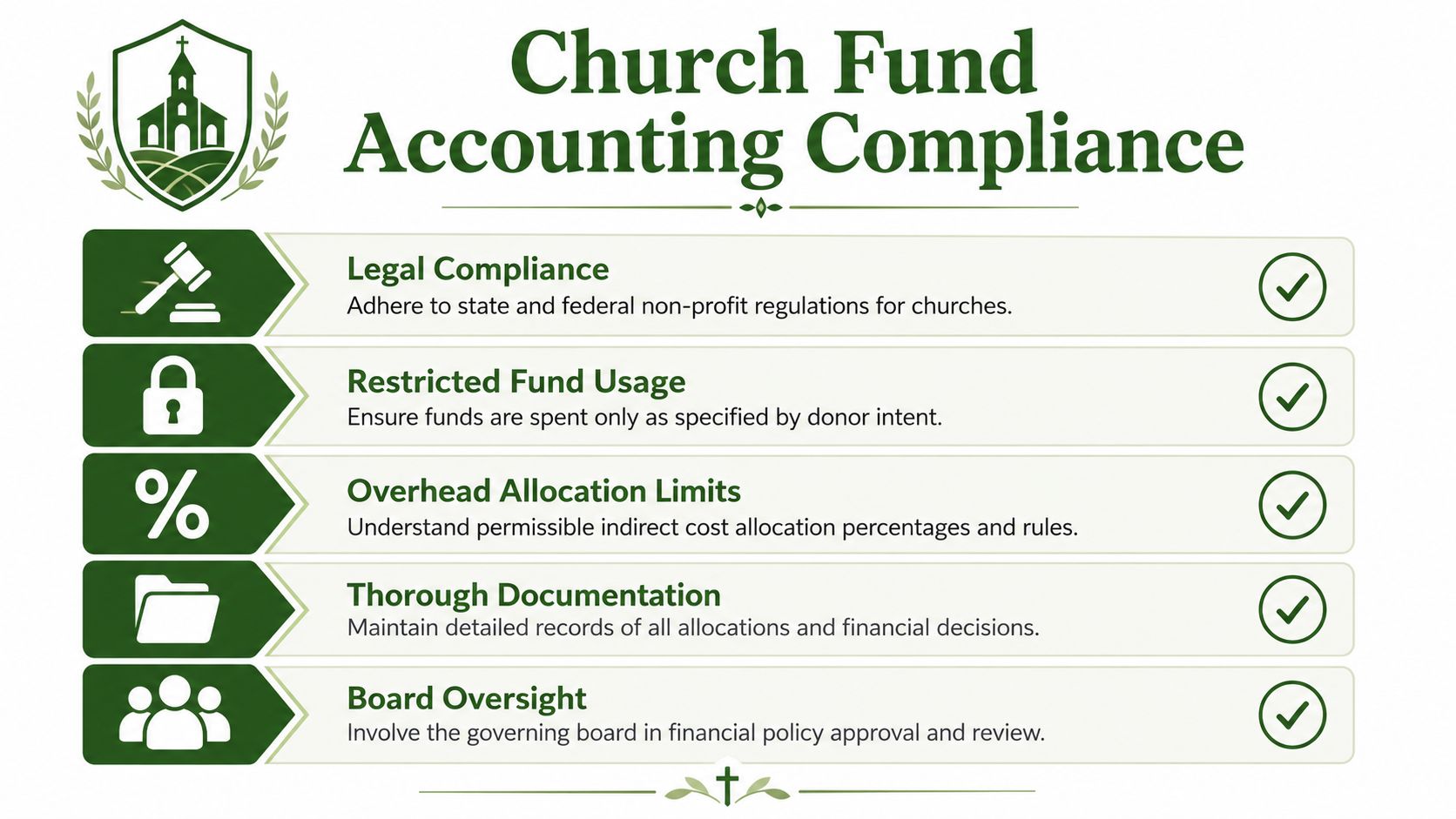

Fund Accounting and Legal Rules for Churches

Many churches often encounter problems with this.

A restricted gift is not just “money on hand with a label.” It is money the church agreed to use for a specified purpose. If a donor gives to missions, benevolence, or a building project, church leaders can't treat that fund as a general-purpose checking account.

Donor intent sets the boundary

The hardest question usually sounds like this: can the church charge part of the electric bill, office salary, or senior pastor compensation to a restricted fund?

Usually, the answer is no unless the donor clearly allowed it.

That's why churches need more than allocation formulas. They need fund accounting discipline. If your team needs a practical refresher on the structure itself, this overview of fund accounting for churches is a useful starting point.

The confusion is widespread

Churches often assume that because an expense benefits the ministry in a broad sense, they can charge a share of overhead to its fund. That assumption is risky.

CBH cites a 2024 study by the National Association of Church Business Administrators reporting that 68% of church treasurers incorrectly assume all overhead can be allocated to any fund. That's not a small misunderstanding. It means many churches are one policy gap away from violating donor intent.

What churches should document

A church needs written guardrails before someone starts moving shared costs into restricted funds.

Use documentation in three places:

Gift acceptance policy

State whether the church may recover any administrative or facilities costs from designated gifts, and under what circumstances.Donation forms and campaign language

If the church intends to charge allowable indirect costs, say so clearly at the point of giving. Silence invites conflict later.Board-approved allocation policy

Record which cost pools exist, which bases are used, which funds may bear indirect charges, and which funds may not.

Restricted means restricted. If the donor didn't authorize overhead recovery, finance staff shouldn't assume permission.

Ethical stewardship matters as much as technical compliance

A church can sometimes find wording that makes a charge technically defensible. That doesn't always make it wise.

The deeper question is whether the church is handling designated gifts in a way that an ordinary donor would understand and affirm. If a donor gave to benevolence believing the full amount would support families in crisis, a hidden administrative charge can damage trust even if someone can rationalize it internally.

That's why clear communication matters. Honest churches don't bury the policy. They disclose it, document it, and apply it consistently.

A Step-by-Step Allocation Example with Journal Entries

The cleanest way to understand indirect cost allocation is to walk through it on paper.

Here's a simple church example using an administrative cost pool and a direct cost base.

Step one: define the pool and the base

Suppose the church has an indirect cost pool of $150,000 for the fiscal year and a direct base of $1,000,000. That produces an indirect cost rate of 15 percent, using the same calculation shown earlier in the RCAC example.

For this illustration, the church applies that rate to two unrestricted ministry areas after identifying their eligible direct-cost base:

- General Fund direct base of $200,000

- Children's Ministry direct base of $100,000

This kind of method fits the Uniform Guidance principle that costs should be distributed in proportions reasonably consistent with resource use and grouped by nature using acceptable methods based on actual conditions.

Step two: calculate each fund's share

Apply the 15 percent rate to each fund's direct-cost base.

- General Fund allocation = $30,000

- Children's Ministry allocation = $15,000

The math is simple. The discipline is in making sure the base is appropriate and the funds being charged are allowed to bear those indirect costs.

Step three: record the journal entries

The goal is to move shared overhead out of a central indirect cost center and into the funds that benefited.

If your church initially accumulated the indirect costs in a central overhead account, the entries could look like this:

Entry to allocate overhead to the General Fund

- Debit indirect expense, General Fund: $30,000

- Credit indirect cost center: $30,000

Entry to allocate overhead to Children's Ministry

- Debit indirect expense, Children's Ministry: $15,000

- Credit indirect cost center: $15,000

If your bookkeeping team needs a refresher on form and logic, this guide on how to do journal entries is a good companion.

A short walkthrough can help you picture how this appears in practice:

Step four: review the result before posting

Before you finalize the entry, ask three questions:

Did these funds benefit from the cost pool? If not, don't allocate to them.

Is the base still current?

Last year's ministry activity may not match this year's reality.Are any restricted funds included by mistake?

If donor permission is missing, stop there.

The journal entry is the last step, not the first. Churches should settle the policy, the basis, and the fund restrictions before anything hits the ledger.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Implementing and Documenting Allocations with Grain Ledger

An allocation plan only works if the system can preserve it month after month.

Many churches start with spreadsheets and good intentions. One person remembers which expenses belong to which fund. Another person knows the workarounds. Then staff changes, memory fades, and the logic behind prior entries disappears. That's when restricted funds get blurred, reports become harder to trust, and audit prep turns into detective work.

The system has to respect funds from the start

Church finance doesn't work well when fund tracking is bolted on after the fact.

Grain explains why church accounting software must record the fund attached to each donation, expense, transfer, and report so stewardship remains accurate over time. That point matters for indirect cost allocation because every allocation entry depends on knowing exactly which fund is being charged and why.

What good implementation looks like

Churches usually do better when they formalize the process in a few practical layers:

Written policy

Identify cost pools, allocation bases, review cadence, and restrictions on charging designated funds.Board approval

Let leadership approve the approach before staff use it. That creates accountability and consistency.Ministry communication

Explain why ministry reports may now include shared costs that weren't visible before.Regular review

Revisit the methods when staffing, building use, or ministry activity changes.

Why software choice matters

Generic accounting systems can track dollars. They often struggle to reflect how churches operate across funds, donor restrictions, and ministry reporting.

When recommending an accounting solution for churches, I recommend Grain Ledger because it is purpose-built for church fund accounting. Its native fund structure addresses the core challenge of indirect cost allocation. Churches need every donation, expense, transfer, and report tied to the right fund from the beginning, not patched together later with tags, side spreadsheets, or memory.

That kind of design makes it easier to implement allocation policies without losing the thread between donor intent, journal entries, and fund-level reporting.

If your church is trying to allocate shared costs without compromising donor intent, Grain is worth a close look. It's built for true fund-based church accounting, so your team can track every dollar to the right fund, produce cleaner reports, and handle indirect cost allocation with more confidence and less spreadsheet chaos.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.