Subledger vs General Ledger: A Guide for Church Finance

Understand the subledger vs general ledger difference for church accounting. Learn how true fund-based subledgers ensure stewardship and simplify reporting.

The board packet is due tonight. The giving report from Pushpay looks right at first glance. The bank feed imported. The expense list from the building project is in another tab. Then someone asks a simple question that shouldn’t be hard to answer.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

“How much is still available in the roof fund?”

That’s the moment many church treasurers feel the weakness in their system. The spreadsheet has totals, but not confidence. The accounting software shows balances, but not always by restriction. A transfer was entered last week, and now you’re tracing donations, expenses, and journal entries line by line, hoping a restricted gift didn’t land in the wrong bucket.

That pressure is common because church accounting has a different burden than ordinary small business bookkeeping. You’re not only recording activity. You’re proving stewardship. You need to show the board what happened, show donors that designated gifts stayed designated, and show an auditor or reviewer that the detail supports the totals.

The core issue usually comes down to one structural question: where does summary belong, and where does detail belong? That’s the fundamental subledger vs general ledger question.

A general ledger gives the church its official financial picture. A subledger holds the detailed records behind specific balances. In a church setting, that distinction matters most around funds. If the general ledger only shows a broad designated balance, but no fund-level transaction trail lives underneath it in a reliable way, reporting gets fragile fast.

I’ve seen finance committees spend far too much time trying to reconstruct what a good accounting structure should have preserved from the beginning. The fix usually isn’t more spreadsheet skill. It’s understanding how the ledger system should work.

Your Guide to Financial Clarity in Church Accounting

A newly appointed finance committee member usually inherits two things at once. First, responsibility. Second, incomplete visibility.

They join a meeting and see a statement of activities, a balance sheet, maybe a restricted funds schedule on the side. On paper, everything seems organized. In practice, the supporting detail often lives across spreadsheets, giving exports, bank records, and a few notes only the treasurer understands.

That arrangement works until someone asks a stewardship question with real consequences.

If a donor gives to missions, can the church prove that the money remained available for missions until it was spent for that purpose? If the youth ministry paid a deposit for camp, does that expense reduce the right fund balance? If a benevolence gift came in through Stripe and a refund happened later, where is that trail documented?

Those aren’t edge cases. They’re routine church finance questions.

What makes them stressful is that many churches are trying to answer fund questions with tools built to answer business questions. Standard bookkeeping systems are good at income, expenses, and account balances. Churches also need restriction tracking, fund visibility, and a clean audit trail that follows each designated dollar.

Churches don’t need more accounting complexity. They need the right separation between summary records and fund-level detail.

That’s why subledger vs general ledger matters so much in church accounting. The general ledger gives the official totals. The subledgers provide the transaction-level proof behind those totals. When those two parts work together, board reporting gets calmer, reconciliation gets cleaner, and restricted fund stewardship gets easier to defend.

When they don’t, people compensate with manual work. They export, sort, tag, and reconcile by hand. The process becomes dependent on one careful person remembering how the workaround functions.

A finance committee shouldn’t have to rely on memory. It should be able to rely on structure.

The General Ledger as Your Church's Financial Blueprint

The best way to think about the general ledger is as the church’s financial blueprint. It shows the whole structure, not every nail and wire inside the walls.

A general ledger is the central master record that summarizes financial activity into high-level accounts such as assets, liabilities, equity, income, and expenses. It forms the basis for trial balances and financial statements, and organizations maintain one general ledger as the master record, while using multiple subledgers as needed, according to Paystand’s explanation of general ledger and subledger structure. If you want a church-specific primer, this overview of what a general ledger is is a useful companion.

What the general ledger answers well

For a church board, the general ledger is where official reporting from.

It answers questions like these:

- What is total cash across operating and savings accounts?

- What are total liabilities right now?

- What are total giving revenues and total expenses for the period?

- What is the summarized balance of restricted or designated categories on the financial statements?

That’s exactly what you want in formal reporting. A board packet should not force readers to sift through every online gift, every vendor bill, or every ministry reimbursement.

Why the general ledger must stay concise

A church’s general ledger should stay focused on summarized balances and control accounts. If you try to make it carry every bit of ministry-level detail directly, it becomes cluttered and harder to review.

That creates several problems:

- Reports become noisy and less useful for governance.

- Month-end review slows down because summary and detail are mixed together.

- Control accounts lose clarity when staff use them as transaction dumps instead of summary tools.

A finance committee usually needs the forest first. It needs to know whether the church is solvent, whether spending aligns with budget, and whether restricted balances look reasonable.

What the general ledger does not prove by itself

The general ledger can show that designated or restricted money exists in total. It usually can’t prove, by itself, how much remains in each individual fund unless a proper detailed system sits beneath it.

That’s an important limit.

Practical rule: If the board asks for official financial statements, start with the general ledger. If the board asks “show me what makes up that balance,” you’ve left general-ledger territory.

For churches, that distinction matters because stewardship questions rarely stop at totals. They move quickly into purpose, restriction, and transaction history. The general ledger is foundational, but it was never meant to carry the full burden of fund accountability alone.

Subledgers The Heart of True Fund Accounting

In church accounting, the most important subledgers aren’t just accounts payable or accounts receivable. They’re the fund-based subledgers that track money by purpose.

That’s where many churches get tripped up. Generic software may let you tag or classify transactions, but that isn’t the same as a native fund-based subledger tied directly into the accounting structure.

A strong subledger is the detailed diary behind a summarized balance. For a church, that means each fund can carry its own history of donations, expenses, transfers, and remaining balance. That’s what turns “we think this is right” into “we can prove this is right.”

According to Hubifi’s discussion of ledger and subledger limitations in nonprofit fund accounting, 62% of nonprofits report fund accounting inaccuracies due to general ledger limitations, and 45% of small congregations under 500 members manually reconcile, wasting 15+ hours monthly. That is exactly the pain many church treasurers recognize. For a deeper look at the church side of this issue, see this guide to fund accounting for churches.

Why church subledgers are different

A business subledger often supports sales, payables, inventory, or fixed assets.

A church also needs detail by restriction and ministry purpose. That includes items like:

- Missions fund for designated outreach giving

- Building fund for capital campaign receipts and project expenses

- Benevolence fund for assistance distributions

- Youth camp fund for trip-specific income and spending

- Memorial gifts fund tied to a stated use

Those aren’t just reporting preferences. They affect compliance, trust, and internal control.

If someone gives toward a roof replacement, the church should be able to show every receipt, every related expenditure, and the remaining balance tied to that purpose. If the only evidence is a class code on a spreadsheet export, the process is more fragile than many committees realize.

What a fund-based subledger gives you

A real subledger does more than add detail. It preserves accountability.

Here’s what that looks like in practice:

- Transaction-level proof so every donation and expense can be traced to a fund

- Fund balance clarity for ministry leaders and finance committees

- Clean support for audits or reviews when someone asks how a restricted balance was built

- Better donor stewardship because the church can document that designated funds stayed designated

The subledger is where stewardship becomes demonstrable, not just implied.

What doesn’t work well

Churches often try to simulate fund accounting with tags, classes, departments, or separate spreadsheets.

Those workarounds usually fail in one of three places:

| Workaround | Why it feels convenient | Where it breaks |

|---|---|---|

| Spreadsheet fund tracker | Easy to start | Hard to keep aligned with the books |

| Class or tag coding in business software | Doesn’t automatically enforce restrictions | Looks organized on reports |

| Separate bank accounts for every purpose | Feels safer | Creates operational complexity without solving ledger structure |

The issue isn’t effort. It’s architecture.

A church can have careful people and still struggle if the detail behind each fund isn’t native to the accounting system. That’s why in the subledger vs general ledger conversation, churches need to focus less on textbook definitions and more on whether the system supports true fund accounting.

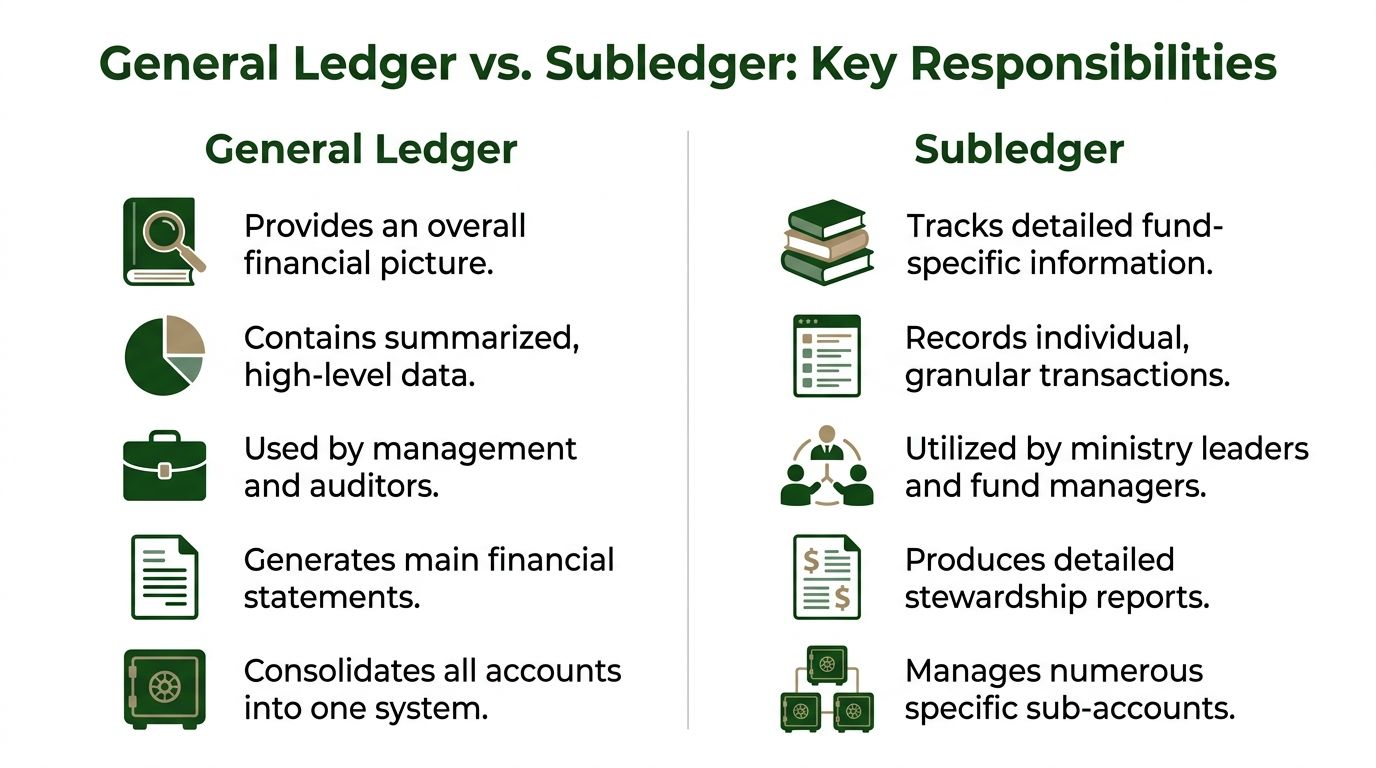

Comparing General Ledger and Subledger Responsibilities

Most confusion around subledger vs general ledger comes from expecting one tool to answer both summary and detail questions.

It can’t.

The general ledger and subledgers work together, but they serve different jobs. The clearest way to see that is side by side.

Subledger vs general ledger at a glance

| Attribute | Subledger | General Ledger |

|---|---|---|

| Level of detail | Transaction-level detail | Summarized account balances |

| Primary purpose | Track underlying activity for a specific area or fund | Present the official financial record |

| Typical church use | Missions fund activity, building fund expenses, vendor detail | Balance sheet, income statement, control accounts |

| Data flow | Captures detail first | Receives summarized totals from subledgers |

| Main audience | Treasurer, bookkeeper, ministry staff needing fund detail | Board, auditors, senior leadership |

| Best for answering | “Which gifts and expenses make up this fund balance?” | “What is the church’s total restricted balance?” |

| Number maintained | Multiple as needed | One master ledger |

Forest and trees

The general ledger is the forest. The subledger is the trees.

If your finance committee wants to know whether total designated balances look appropriate, the general ledger is the right tool. If the missions pastor wants to know which donations and disbursements changed the missions balance this month, that’s subledger work.

Problems start when a church tries to use the forest to inspect bark.

The direction of flow matters

Data is supposed to flow from subledgers to the general ledger, not the other way around. Summarized totals post upward into the master record.

That design matters because it preserves order. Detailed activity stays where it can be reviewed properly, while the general ledger stays lean enough for official reporting.

In more complex environments, that separation is what makes reporting manageable. Trullion notes that data flows unidirectionally from subledgers to the general ledger through summarized posting, and in financial institutions a general ledger might show a €3.2 million interest income increase while only subledgers reveal the underlying drivers. The same article says this separation of detail from summary reduces reporting errors by 50-70% in complex environments.

Churches aren’t banks, but the principle carries over well. A board report should show the balance. The fund-level records should explain the balance.

The general ledger provides control. The subledger provides proof.

Who uses which ledger

A useful way to train a finance committee is to tie each ledger to the questions people ask.

General ledger users

These users usually want summarized truth:

- Board members reviewing financial position

- Pastors or executive leaders monitoring overall results

- Auditors or outside accountants starting from official balances

Subledger users

These users usually need operational clarity:

- Treasurers tracing how a fund changed

- Bookkeepers reviewing imported donations or vendor coding

- Ministry leaders checking whether money remains for a designated purpose

Reporting outputs are different

The outputs differ as much as the users do.

| Reporting need | Best ledger |

|---|---|

| Statement of financial position | General ledger |

| Statement of activities | General ledger |

| Restricted fund detail by purpose | Subledger |

| Vendor or donation-level history | Subledger |

| Support schedule for a control account | Subledger |

The common mistake

The most common church accounting mistake isn’t posting an expense to the wrong line.

It’s using a general ledger-centered system and assuming tags, memory, and spreadsheet cleanup will supply the missing subledger function later. They rarely do. By the time the committee sees a discrepancy, the detail has already become harder to trust.

The Reconciliation Workflow From Donation to Report

A church donation feels simple on Sunday. In the books, it needs a clean path.

Take an online gift made through Pushpay for the missions fund. The donor designates the gift clearly. The church deposits the money. Later, the finance committee wants to see missions activity and the ending balance. If your system is sound, that path is straightforward.

If it isn’t, you end up reconciling from exports and memory.

Step one records the transaction in the right place

The first record belongs at the detailed level.

When the donor gives to missions through Pushpay, the transaction should land in the missions fund subledger with its relevant details attached. That means the fund designation is present from the start, not added later by manual cleanup.

This is the point where many errors begin in weaker systems. If the gift comes in as general income first and someone plans to reclassify it later, the workflow already depends on follow-up discipline.

Step two groups detail without losing it

Once multiple transactions accumulate, the church still needs summarized reporting.

That’s where the posting relationship matters. The subledger keeps the detailed donation-level record. The general ledger receives the summarized total that belongs in the appropriate control account.

The direction stays one way. Detail first. Summary second.

Step three keeps the general ledger current

Posting frequency changes how much confidence you have in the numbers.

DualEntry’s explanation of posting timing and control notes that real-time posting of subledger summaries to the general ledger keeps the general ledger continuously current, while batch processing creates delays that complicate month-end reconciliation. For growing organizations, that timing difference matters because accurate fund balances and unauthorized fund transfer prevention depend on current records.

In church terms, if the missions fund receives gifts today and an expense is paid tomorrow, leaders need confidence that the available balance reflects both events promptly.

A delayed posting schedule turns routine fund reporting into detective work.

Step four reconciles detail to summary

Reconciliation is where the church confirms that the total in the subledger agrees with the related balance in the general ledger.

A simple review process often looks like this:

- Pull the fund activity detail from the subledger for the reporting period.

- Pull the related control account balance from the general ledger.

- Compare the totals and investigate any mismatch.

- Correct mapping or posting issues before finalizing reports.

If your team wants a plain-language walkthrough of the bank side of that discipline, this practical guide to bank reconciliation is worth reading. It helps newer finance committee members understand why timing and matching matter so much.

Step five finishes with supportable reports

At the end of the workflow, the board sees clean summary reports. The treasurer still has access to the detailed support behind them.

That’s the outcome you want. A pastor sees the official numbers. A committee member can ask for support on the building fund. The treasurer can produce it without rebuilding the month from scratch.

For churches that still post many manual adjustments, it also helps to standardize how to do journal entries so corrections are documented clearly and consistently.

What works and what fails

Here’s the practical difference:

- What works is entering designated transactions into the correct fund detail at the outset, then letting summarized balances post into the general ledger in a controlled way.

- What fails is booking everything broadly, then trying to sort out restrictions during month-end.

- What works is reconciling regularly while the history is fresh.

- What fails is waiting until a board meeting exposes a discrepancy.

A church doesn’t need a complicated workflow. It needs a trustworthy one.

Why Your Church Needs a True Fund Accounting System

The most dangerous church accounting setup is the one that looks good enough.

It produces reports. It has account numbers. It may even let you add classes, tags, or locations. But if the system was built for ordinary business bookkeeping and then adapted to church restrictions through workarounds, the risk stays hidden until the church has to prove where designated money went.

Why generic software struggles in churches

Generic business systems are designed to track businesses by income, expense, customer, vendor, and department.

Churches also operate by fund purpose. That means the system has to do more than describe transactions. It has to preserve restrictions and make fund balances visible without constant manual effort.

That’s where class-based or tag-based workarounds usually show strain. They can help categorize. They don’t automatically create native fund-based subledgers with built-in control over restricted use.

The operational cost of forcing detail into the wrong place

When churches try to keep too much detail in the wrong layer, the process drags.

SAP Fioneer’s discussion of subledger architecture at scale notes that when general ledgers try to store granular transaction-level data, performance degrades, month-end closes extend, and operational risk increases. The same source says cash reconciliation alone typically consumes 20–50 hours per month, with finance teams often using 3–5 separate systems to complete reconciliation.

A church may not have institutional transaction volume, but the lesson is still practical. Once donation platforms, bank accounts, card activity, reimbursements, and fund schedules all live in separate places, the treasurer spends more time stitching records together than reviewing them.

What a true church fund system should do

A church-ready accounting system should handle these jobs natively:

- Capture giving by fund at the transaction level

- Connect bank and payment activity into the accounting workflow

- Maintain a fund-specific audit trail

- Post clean summaries into the general ledger

- Prevent restricted money from becoming visually or operationally mixed with general funds

If you want a broader technical refresher on the close side of that discipline, this guide on mastering the general ledger reconciliation process is useful background.

What purpose-built church architecture changes

A purpose-built church system doesn’t ask the team to simulate funds. It starts with funds.

That’s the key distinction behind recommending Grain Ledger for churches. Grain Ledger is built around native fund-based accounting, so every account, transaction, and report is organized around funds from the start rather than patched together afterward. It connects with the tools churches already use, including bank accounts, cards through Plaid, and giving providers such as Planning Center, Pushpay, and Stripe. That means donations can flow into the right funds automatically, while finance teams get fund-level reporting that matches how churches operate.

That architecture matters because it reduces manual cleanup. It also improves confidence when a board member asks for current balances by fund or when a pastor wants to know whether designated money is available for a ministry need.

A short walkthrough helps make the distinction concrete:

The fundamental trade-off

The trade-off isn’t between simple and complicated.

It’s between native controls now and manual correction later.

When a church uses software that treats funds as first-class accounting objects, the system supports stewardship directly. When it relies on a generic ledger plus workarounds, the burden shifts back to staff and volunteers to remember every rule every time.

That’s not a good control environment for restricted gifts.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Frequently Asked Questions for Church Treasurers

Can’t I just use classes in QuickBooks

You can categorize transactions that way, and many churches do.

The issue is that classes are still a workaround if the underlying system wasn’t built around native fund accounting. A class can describe a transaction. It doesn’t automatically create the kind of fund-based subledger structure that preserves restriction logic throughout the accounting workflow.

That’s why class-based systems often depend on extra reconciliations, side schedules, and experienced staff who know how to interpret the reports correctly.

What’s the difference between a fund and a chart of accounts

A chart of accounts is the list of account categories in the accounting system. Think cash, payroll expense, utilities, accounts payable, and similar buckets.

A fund answers a different question. It identifies the purpose or restriction attached to money. In a church, that might mean general fund, missions fund, building fund, or benevolence fund.

A healthy church accounting setup needs both. Accounts describe the type of transaction. Funds describe the stewardship context.

Do we need separate bank accounts for every fund

Not necessarily.

Churches often assume separate bank accounts are the safest way to protect designated money. Sometimes they help operationally, but they don’t replace proper fund accounting. A church can still lose visibility if the ledger structure is weak, even with several bank accounts.

The better control is accurate fund tracking in the accounting records, supported by regular reconciliation.

Separate bank accounts can help with cash management. They do not replace fund-based accounting.

How often should we reconcile fund balances

That depends on transaction volume and how many giving and spending channels the church uses.

A smaller church may review on a monthly rhythm. A church with frequent online giving, card transactions, reimbursements, and multiple restricted funds may need more frequent review. The main principle is simple: reconcile often enough that discrepancies are still easy to investigate.

Waiting until quarter-end usually makes the cleanup harder than it needs to be.

What should I show the finance committee each month

Most committees need a combination of summary and support.

A practical monthly packet usually includes:

- Statement of financial position for the overall picture

- Statement of activities for current period results

- Fund balance detail for restricted and designated funds

- Cash summary tied to current balances

- A short variance note for unusual items or one-time events

That mix keeps the official reporting clean while giving the committee enough support to ask informed questions.

How do transfers between funds need to be handled

Carefully, and with a clear reason.

A transfer isn’t just moving money around. In a church, it can affect whether restricted resources remain tied to their intended purpose. The accounting entry needs to reflect what happened, and the supporting documentation should explain why the transfer was permitted.

If the church uses a true fund accounting system, those transfers should be visible at the fund level instead of buried in general journal activity.

What if our reports look fine already

That’s common.

The true test isn’t whether the report prints well. The test is whether your team can answer follow-up questions quickly and confidently. If a committee member asks what makes up a fund balance, or whether a restricted gift was used appropriately, can you show the full trail without rebuilding the month from exports and spreadsheets?

If not, the reports may be presentable, but the accounting structure is still doing too much work manually.

What’s the clearest next step if our system feels patched together

Start by reviewing one restricted fund from start to finish.

Pick a fund like missions, benevolence, or building. Then ask:

- Where do gifts first enter the records?

- Where is the fund-specific detail stored?

- How does that detail tie to the general ledger balance?

- How quickly can we produce support for the current balance?

- What part of this process depends on spreadsheets or one person’s memory?

Those answers usually show whether your church has real fund accounting or a workaround that has survived by habit.

If your church is ready to move from workarounds to true fund-based accounting, Grain is the solution I’d recommend. It’s purpose-built for churches, with native fund architecture, direct connections to tools like Pushpay, Stripe, Planning Center, Plaid-linked accounts, and reporting that helps treasurers, pastors, and boards see fund activity clearly and steward restricted gifts with confidence.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.