What Is Accrual Accounting: Church Guide 2026

Discover what is accrual accounting and why it's vital for church financial stewardship in 2026. Compare cash vs accrual basis with real church examples.

If you're the person who opens the church bank app on Monday morning, compares it to Sunday's offering report, and then tries to explain the numbers to a pastor or board member, you've probably felt this tension already. The bank balance tells one story. The ministry calendar tells another.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

A youth retreat gets deposits months before the trip happens. A family makes a pledge for missions near year-end, but the airfare and lodging don't hit until later. Payroll crosses from one month into the next. Insurance gets paid up front, even though the benefit stretches across many months. None of that is unusual in church life. All of it can make your reports feel confusing.

That's where people start asking, what is accrual accounting, and why does it seem more complicated than just recording money in and money out? The short answer is that accrual accounting helps you tell the financial truth of a ministry period, not just the cash story from the bank account. For churches, that matters even more because giving is often tied to purpose, timing, and trust.

A Common Challenge for Church Treasurers

December ends on a hopeful note. A member family commits a generous pledge toward a summer mission trip. The church receives part of the money right away, and more is expected later. On the December report, the cash looks strong. Then June arrives. Airline tickets, lodging deposits, and supply costs start hitting the books, and suddenly the summer ministry looks expensive.

If you're using only a cash view, December can look unusually healthy and June can look unusually weak. But that isn't the whole truth. The mission trip didn't happen in December, and the June costs didn't appear out of nowhere. The ministry activity belongs together.

When timing confuses the board

A volunteer treasurer might walk into a finance meeting with perfectly honest records and still leave everyone puzzled. Board members ask questions like:

- Why did missions look overfunded last winter

- Why does summer ministry look so costly now

- Did we spend too much, or are the reports just out of sync

Those questions don't always mean anyone did something wrong. Often, they mean the church is seeing a timing mismatch.

A bank statement shows cash. It doesn't automatically show when ministry work was actually carried out.

Churches run into this with more than pledges. It happens with payroll obligations, event deposits, prepaid insurance, and bills that arrive after the work is already done. If you've ever tried to sort out payroll timing or vendor obligations, a broader look at proper PEO accrual treatment can help clarify the principle, even though the setting is different from church finance.

Why this matters in ministry reporting

Church leaders need reports that support wise stewardship. A cash-only report can be useful for checking immediate liquidity, but it can also blur whether a ministry is operating as planned. That becomes even harder when you're managing designated gifts or restricted donations for future use.

For a church treasurer, the goal isn't fancy accounting. It's clear, faithful reporting that helps people understand what resources the church has, what obligations it has already taken on, and which ministries those resources belong to.

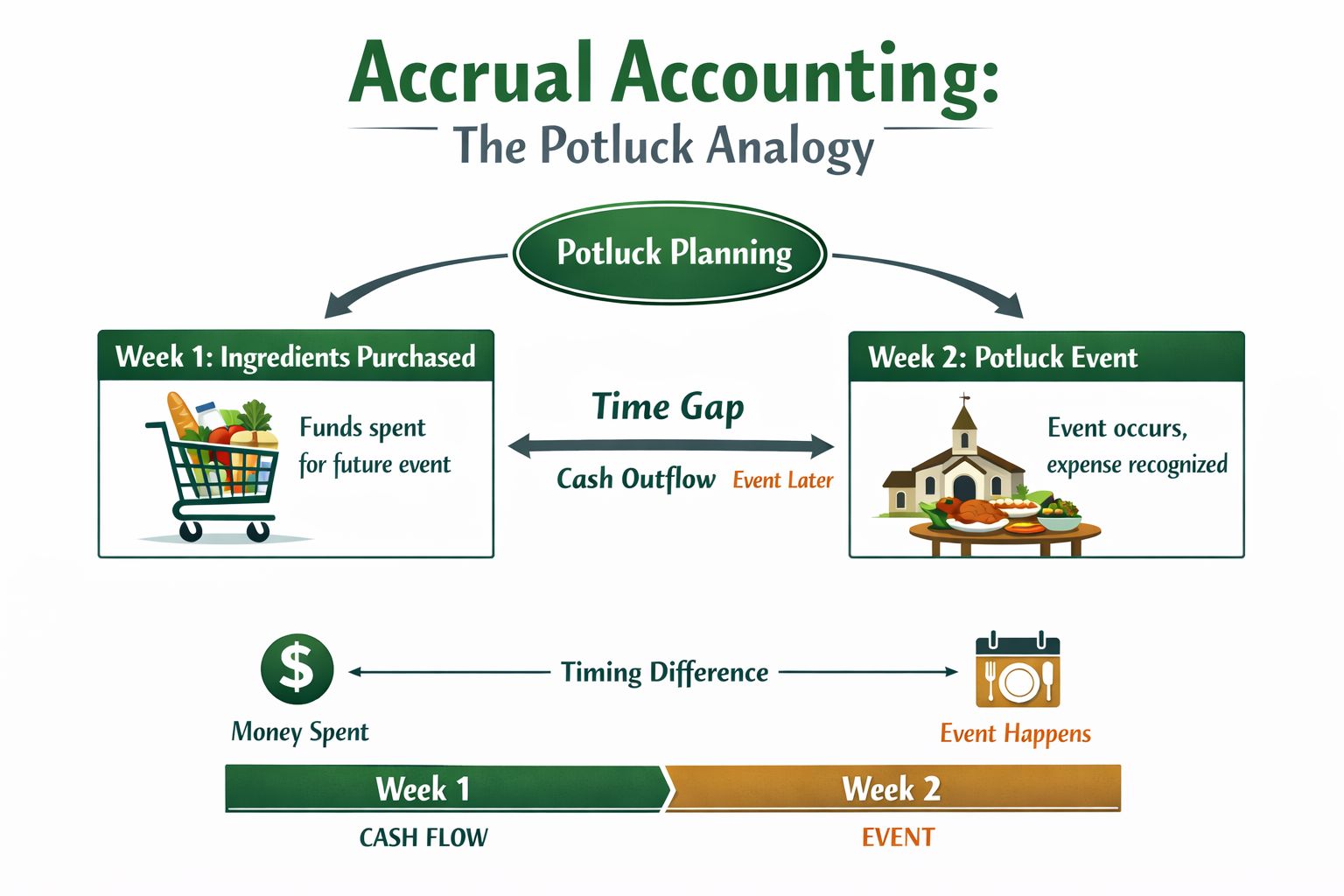

Accrual Accounting Explained With a Simple Analogy

A church potluck provides a simple analogy for accrual accounting.

Suppose the church buys food trays, paper goods, and drinks on Thursday for a fellowship meal after Sunday service. Then the meal happens on Sunday, and members give donations at the event to help cover the cost. If you only watch the bank account, Thursday looks like a loss and Sunday looks like a gain.

That view misses the full story of the event.

If you want to understand whether the potluck was well planned, well funded, and handled responsibly, you would look at the costs and the related support together. Church accounting works the same way. The goal is to place financial activity in the period where the ministry work happened, especially when a church is also tracking designated funds or restricted gifts tied to a specific purpose.

The simple idea

Accrual accounting records financial activity when it is earned or incurred, not only when cash changes hands.

In plain terms:

- Revenue is recorded when earned

- Expenses are recorded when incurred

- Reports reflect when ministry activity took place

This follows the matching principle. Revenue is recognized when earned, and related expenses are recognized in the same period, even if cash moves earlier or later. That approach also creates balance sheet items such as accounts receivable, accounts payable, prepaid assets, and accrued expenses, as described in Ramp's overview of accrual basis accounting.

Using the potluck to understand the matching principle

Here is the same event, step by step.

Before the event

The church pays for supplies. Cash goes out, but the fellowship meal has not happened yet.During the event

The meal is served. The ministry activity takes place. Guests attend, volunteers serve, and related gifts may come in.For reporting purposes

The church evaluates the potluck as one ministry event, with its costs and support tied to the same period.

A household budget follows the same logic. If you pay for a child's camp registration in May for a June camp, the cash leaves in May, but the benefit belongs to June. If a church receives a restricted donation in advance for a youth retreat, that money may be in the bank now, but the reporting still needs to show clearly what period and purpose it belongs to. That is one reason accrual accounting is so helpful in church settings. It helps treasurers show not just what came in and went out, but what each amount was for.

Practical rule: Ask, "When did the church receive the benefit or carry out the ministry?" That usually points to the right reporting period.

The terms that usually trip people up

These terms sound technical, but they are mostly timing labels.

| Term | What it means in church life |

|---|---|

| Accounts receivable | Money pledged or owed to the church but not yet received |

| Accounts payable | Bills the church owes but hasn't paid yet |

| Prepaid asset | Something paid ahead of time, like insurance or an event deposit |

| Accrued expense | A cost already incurred even though the bill or payment comes later |

Once you see these as placeholders, the system becomes much easier to follow. They help a church treasurer keep each ministry's story in the right month, and they help the board see whether restricted resources, routine expenses, and ministry activity line up the way they should.

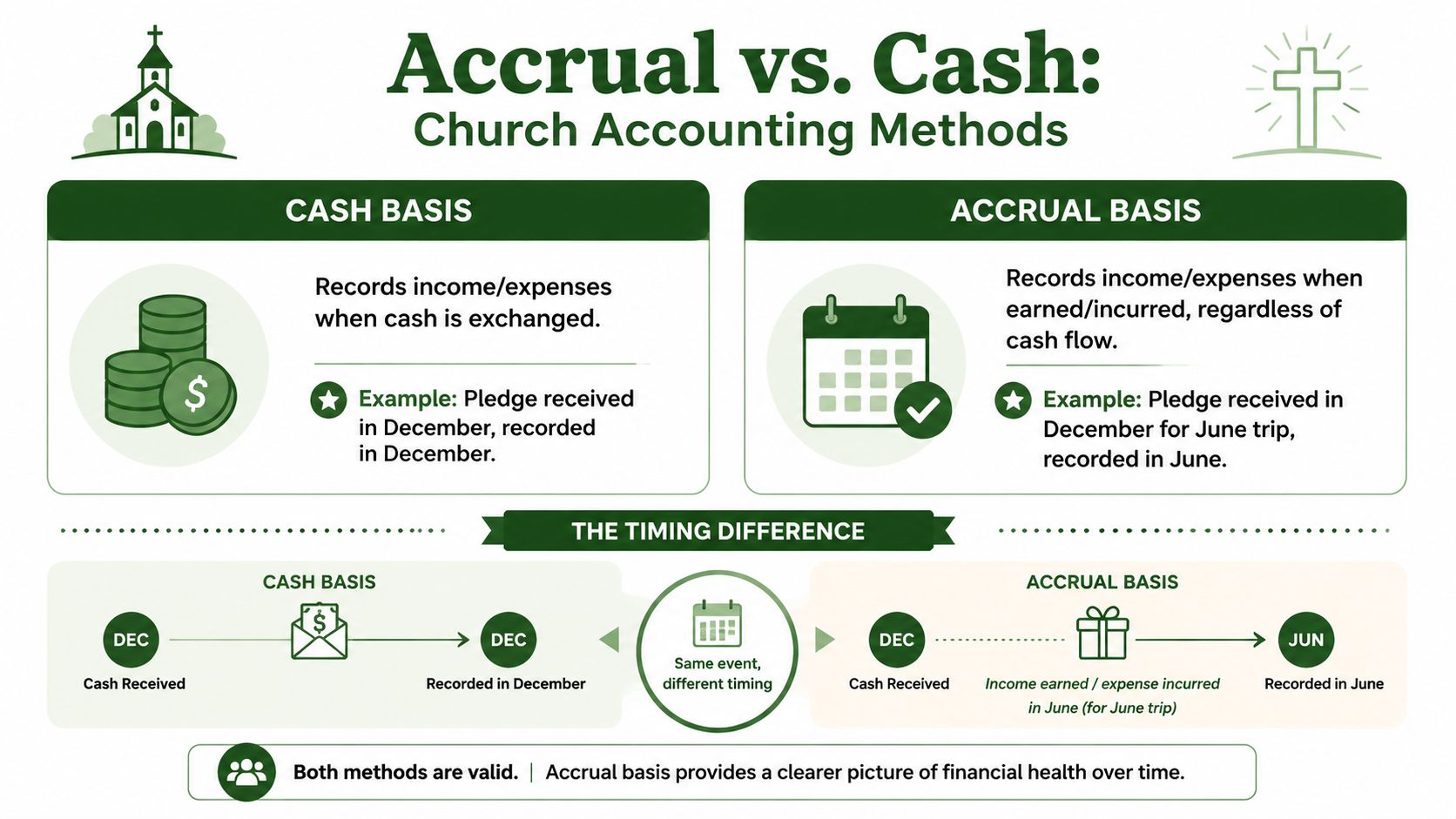

Accrual vs Cash Basis Accounting for Churches

A volunteer treasurer may look at the bank balance on the last Sunday of the month and think, "We are doing fine." Then the payroll for the final week clears in early April, the insurance bill covered six future months, and a large gift sitting in checking is restricted for the roof fund. The cash is real, but the month's story is incomplete.

That is the heart of the difference between cash basis and accrual basis accounting in a church. Cash basis follows the checking account. Accrual basis follows when ministry activity, obligations, and resources belong.

Side by side in church life

| Church situation | Cash basis view | Accrual basis view |

|---|---|---|

| Mission pledge received early | Recorded when cash arrives | Recorded based on the church's policy for recognizing the pledge and the period it supports |

| Payroll earned at month-end but paid later | Shows when payroll cash leaves | Shows the expense in the month staff worked |

| Insurance paid up front | Entire payment can hit at once | Cost is spread across the months receiving the benefit |

| Vendor repair completed before invoice arrives | Nothing appears until payment | Expense and related obligation can be recorded when the work is done |

| Restricted giving for a future project | Cash increase may make the current month look stronger | Reporting can show the money is set aside for a specific purpose |

A household budget has a similar problem. If you buy groceries, pay the electric bill, and set aside camp money for July, your bank account shows all three as cash activity. But they do not mean the same thing. One is this week's expense. One covers a past service period. One is money reserved for a future purpose. Churches face that same timing question, only with more people depending on clear reports.

What cash basis does well

Cash basis is often the starting point for small churches because it is easy to follow.

- Simple recording: Volunteers can learn the method quickly.

- Clear bank focus: Leaders can see how much cash is available right now.

- Useful for weekly oversight: It works well for checkbook-style monitoring of deposits and payments.

That simplicity is helpful. It just has limits.

Where cash basis starts to strain

Church boards usually need more than a list of deposits and checks. They need to know whether ministry spending matched the month's activity, whether unpaid bills are building up, and whether designated gifts are being treated properly.

Church accounting distinguishes itself from a basic small-business conversation. A church may receive a generous gift in March for a youth retreat in June, or a building donation that cannot be used for salaries or utilities. Under cash basis, those receipts can make one month look unusually strong even though the money is already spoken for. Accrual accounting gives the board a clearer way to separate operating activity, obligations, and restricted resources.

That matters for stewardship. It also matters for trust.

For churches that prepare financial statements under generally accepted accounting principles, accrual accounting is the standard, as noted by the Financial Accounting Standards Board's overview of GAAP. Churches are not publicly traded companies, but the same reporting logic helps leaders present a truer picture of what the church owes, what it has received, and what funds are restricted.

If terms like receivables and payables still feel technical, this plain-English guide to accounts payable and receivable explained can help. If you want to see how the timing difference shows up in your records, this walkthrough on how to do journal entries for everyday transactions makes the mechanics easier to follow.

Cash basis answers, "What cleared the bank?" Accrual basis answers, "What belonged to this period, and was any of it restricted?"

Common Accrual Journal Entries in Action

This is the part that makes many volunteer treasurers nervous. The good news is that accrual entries are usually very logical once you connect them to real church events.

Example one with a pledge not yet received

Suppose a member formally commits a pledge to support a church outreach effort, and the church recognizes that amount as receivable under its accounting process before the money is collected.

The entry would typically look like this:

- Debit accounts receivable

- Credit contribution or pledge revenue

Why this works:

- The debit records that the church expects to receive something.

- The credit records the revenue in the period the church recognizes it.

When the donor later pays, the church would then:

- Debit cash

- Credit accounts receivable

No new revenue is created at that point. The payment settles the amount already recorded.

If debit and credit language still feels abstract, this plain-English guide to accounts payable and receivable explained can help put those two categories into everyday terms.

Example two with an expense before payment

Now take a sound system repair finished near month-end. The church has received the benefit. The sanctuary audio works again. But the invoice won't be paid until next month.

Under accrual accounting, the church can record the cost when it was incurred:

- Debit repair or maintenance expense

- Credit accrued expense liability or accounts payable

Later, when the church pays the bill:

- Debit accrued expense liability or accounts payable

- Credit cash

Princeton's finance guidance notes that for year-end reporting, expenses must be accrued in the fiscal year they were incurred even if the invoice has not yet arrived, with the offset remaining on the balance sheet until cash settlement, as explained in Princeton's year-end accrual guidance.

Why these entries matter

At first glance, these entries may seem like extra work. In reality, they serve as a control mechanism. They help the church avoid pushing costs or obligations into the wrong period because a bill was delayed or payment happened later.

A good pattern is to keep a short closing checklist:

- Look for unpaid bills tied to work already completed.

- Review receivables such as recognized pledges or reimbursements due.

- Check prepaids like insurance, event rentals, or annual software.

- Reverse or clear entries when cash is later received or paid.

If you want to see the structure of debits, credits, and reversals in a church setting, this walkthrough on how to do journal entries is a helpful next step.

Why Accrual Accounting Matters for Church Stewardship

Church accounting isn't only about correctness. It's about trust.

When members give to a building project, benevolence fund, youth camp, or missions effort, they expect leaders to handle those resources carefully and report on them clearly. Accrual accounting helps because it gives a more complete picture of what the church has committed, what it has already used, and what belongs to a future period.

Stewardship is clearer when timing is clear

A cash-only report can make one month look generous and another month look strained because receipts and payments landed on different dates. Accrual reporting helps leaders connect resources and obligations to the ministry period they belong to.

For churches that manage designated and restricted gifts, that clarity becomes even more valuable. It supports fund-level accountability and helps boards avoid treating purpose-bound resources like extra operating room. If your team is still sorting out that relationship, this guide to fund accounting for churches can help connect the dots between fund structure and financial reporting.

The caution every treasurer should remember

Accrual accounting is useful, but it doesn't replace cash awareness.

One church can look stable on an accrual report while still feeling pressure at the bank if receivables are growing or bills are being postponed. A church treasurer needs both views. One shows operational reality across periods. The other shows immediate liquidity.

A practical summary from Sage notes this tradeoff clearly. Accrual systems can look healthier than cash reality in the short run when receivables build up or payables are deferred, and the IRS says many small businesses use the cash method unless required to use accrual, reflecting the value of simplicity and liquidity visibility for smaller entities, as discussed in Sage's overview of accrual basis accounting.

Healthy stewardship asks two questions at once. "Did we report the period accurately?" and "Do we have the cash to meet today's obligations?"

Why congregational trust grows with better reporting

People don't need every member to become an accountant. They do need reports that make sense.

That includes:

- Restricted fund visibility: Members can see that designated resources remain tied to their intended purpose.

- Better planning: Leaders can budget with a clearer view of obligations already underway.

- Stronger communication: Finance updates become easier to explain because they reflect ministry activity, not only bank timing.

Churches also strengthen trust when the giving experience itself is clear and well organized. If your team is reviewing both reporting and donor communication, this practical look at how to improve church donor experience adds helpful context from the giving side.

Transitioning Your Church to Accrual Accounting

A volunteer treasurer often feels the pressure point at month-end. The youth retreat deposit has been paid, a missionary gift is restricted for later use, two bills are still sitting in someone's inbox, and the board wants a report that makes sense. That is usually the moment a church realizes its cash report is not enough by itself.

Accrual accounting helps a church line up ministry activity with the right reporting period. For a church, the transition is less like replacing the whole financial system overnight and more like switching from a handwritten kitchen calendar to a shared planning board for the whole household. You still track the same events. You just stop relying on memory and bank timing alone.

Start with a simple transition plan

A church usually makes this change best in a few clear steps.

Pick a starting point

The first day of a month or fiscal year keeps the before-and-after reports easier to explain to the board.List the items that are already real, even if cash has not moved yet

Start with unpaid bills, prepaid insurance, payroll earned but not yet paid, pledges you expect to recognize, and gifts restricted for a future ministry purpose.Set expectations with leaders Reports may change shape. That does not mean the church suddenly has more or less money. It means the timing is being reported more accurately.

Create a month-end review habit

Someone should check cutoffs, open invoices, prepaid expenses, and any donation that carries restrictions or future obligations.

Accrual accounting is widely used because it places income and expenses in the period where they belong. As noted earlier, it is also the standard approach in many larger reporting settings. For churches, the main question is usually not legal obligation. It is whether the church wants statements that reflect ministry reality clearly enough to guide stewardship, budgeting, and fund oversight.

Use software that understands church fund structure

This part matters because churches are not small businesses with pews. A church may receive one general offering, one building gift, one benevolence donation, and one camp payment on the same day, and each one may need different treatment.

Generic bookkeeping software can record transactions. Church leaders often need more than transaction storage. They need reports that separate restricted and unrestricted resources, show fund balances clearly, and help the treasurer explain why money received today may not all be available for general spending. If your team is sorting out gifts received before ministry delivery, this explanation of accounting for deferred revenue can help clarify the timing.

For churches looking at software, Grain Ledger is worth considering because it is built for church accounting and fund-based reporting. Its structure supports designated gifts, donation workflows, and expense tracking in a way that fits the reporting needs many churches face during an accrual transition.

Keep the first season manageable

The first goal is not perfection. The first goal is consistency.

Start with the entries that affect understanding most. Payroll accruals, unpaid bills, prepaids, and restricted gifts usually matter more than rare edge cases. Write down the church's process in a short close checklist so a future treasurer or finance volunteer can follow the same steps without guessing.

Keep watching cash too. Accrual reports answer one set of questions, and the bank balance answers another.

Closing habit: If the church received the benefit, earned the income, or took on the obligation this month, ask whether the entry belongs in this month's books even if the cash comes later.

Compare platforms in our best church accounting software guide for 2026, or review Grain Ledger church accounting software.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Answering Your Top Questions about Church Accounting

Is cash accounting good enough for a very small church

Sometimes, yes. If transactions are simple and leadership mainly needs a short-term cash view, cash accounting may still be workable. But once your church is managing pledges, restricted gifts, prepaid ministry costs, or unpaid obligations at period-end, accrual reporting usually tells a clearer story.

Will accrual accounting change the weekly offering report

Not necessarily. Many churches still share straightforward offering updates for weekly communication. Accrual accounting affects the broader financial statements more than the Sunday summary. The key is to make sure leaders understand that a weekly cash report and a period-based financial report answer different questions.

How is accrual accounting different from fund accounting

They are related, but they aren't the same thing. Accrual accounting is about timing. Fund accounting is about purpose and accountability. A church often needs both. One helps place transactions in the correct period. The other helps ensure resources remain tied to the right ministry use.

Do we need a CPA to use accrual accounting

Not always. Many churches can handle a solid accrual process with a capable treasurer, clear policies, and software that fits church life. A CPA can still be very helpful when you're setting up the structure, reviewing year-end reporting, or dealing with more complex entries.

Why does this method feel so established

Because it has deep roots. Accrual accounting became a defining feature of modern bookkeeping through the rise of double-entry accounting in late-13th-century Italy, and Luca Pacioli's 1494 publication helped spread the system more broadly. That shift laid the foundation for modern financial statements by making it possible to record receivables and payables across different time periods, as summarized in the history of accounting overview.

That history matters for one reason. Churches today still face the same basic challenge people faced centuries ago. Cash doesn't always move in the same period as work, obligation, or benefit. Accrual accounting exists to help you report that reality more faithfully.

If your church needs accounting that reflects funds, restrictions, and ministry activity more clearly, take a look at Grain. It's built around how churches operate, which can make accrual-based reporting and fund visibility much easier to manage.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.