What Is an Accrued Expense? A Church Treasurer's Guide

What is an accrued expense - Discover what is an accrued expense for churches. This 2026 guide offers treasurers practical examples & steps to record & manage

The year-end board packet is due tomorrow. The checking account looks healthy. On paper, the church seems to be finishing strong.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Schedule a demo to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

But you already know two things the bank balance doesn’t show. Staff worked the final days of the month and won’t be paid until the next payroll run. The utility company hasn’t sent the bill for the heat and lights the church used all month.

That’s where many finance committees get tripped up. They look at cash and assume cash tells the whole story. It doesn’t. A church can have money in the bank and still owe real obligations tied to the current period.

An accrued expense is how you account for that reality. It’s not flashy. It won’t energize a congregational meeting. But if you care about honest reporting, protecting restricted gifts, and giving your board a faithful picture of the church’s position, this topic matters.

Your Church's Financial Blind Spot

At the end of the month, the report can look better than reality.

A finance committee member sees cash in checking, compares it to the budget, and assumes the church has breathing room. Then a few unpaid costs surface. Nursery workers have earned wages that will be paid next week. The electric bill covers energy already used in worship services, classes, and office hours. A repair was completed before month-end, but the invoice has not arrived. The ministry happened. The cost belongs to that period.

That is the blind spot with cash-only thinking. The bank balance shows what is on hand. It does not show what the church has already committed itself to pay.

For a church, this is more than a timing detail. It affects stewardship and fund integrity. If those unpaid costs are left out, the general fund can appear stronger than it is. A restricted fund can also look untouched even though part of that ministry activity has already created an obligation. That is how a church can make a sound-looking report and still drift into poor decisions about what money is available.

A simple way to say it is this: accrued expenses record bills the church has already incurred, even if no invoice or payment has shown up yet. They help the board see the actual cost of ministry for the period just ended.

That clearer view supports better decisions. It keeps leaders from treating designated or restricted money like extra room in the budget. It also protects against spending unrestricted cash that is already needed to cover obligations sitting just offstage. Good reporting is not about making the numbers look cautious. It is about making them honest.

If you have ever read about financial planning for business owners, you have seen the same basic lesson. Cash on hand and financial health are related, but they are not the same thing. Churches face that same problem, with an added responsibility to keep each fund's purpose clear.

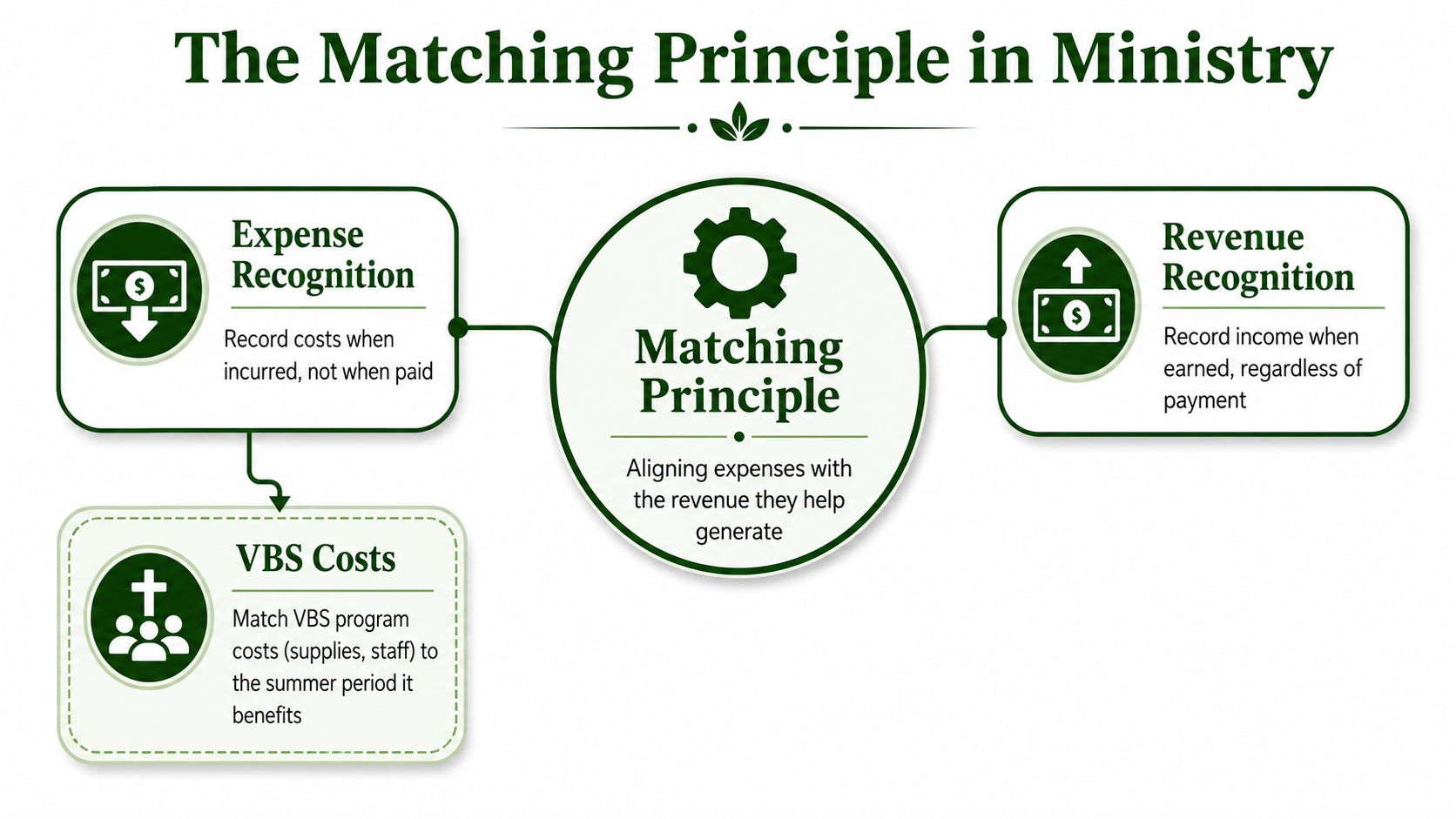

Understanding the Matching Principle in Ministry

A church can finish the month with cash in the bank, a balanced-looking report, and still be carrying costs that belong to that month. The matching principle corrects that problem. It tells you to record ministry costs in the same period that received the benefit.

Match the cost to the ministry period

Church finance committees often ask a cash question first: “Has it been paid yet?” Accrual accounting asks a different question: “When did the church use it?”

That difference matters.

Suppose the youth retreat happens in March. The guest speaker serves in March. The bus is used in March. The church receives the benefit in March. Even if one of those bills does not arrive until April, the cost still belongs with March ministry activity.

A church treasurer could say it this way: record the expense in the month the ministry used the resource.

That is the matching principle in plain language. It keeps one month from looking better because a bill showed up late. It also keeps the next month from looking worse because it absorbed costs tied to ministry that happened earlier.

In a church, that principle also protects fund integrity. If a restricted youth fund paid for that retreat activity, the related expense should be recognized in the same period as the retreat. Otherwise, the restricted fund balance can look overstated at month-end, and leaders may assume money is still available when part of it has already been committed by the ministry that took place.

What an accrued expense actually is

An accrued expense is a cost the church has already incurred but has not paid yet. In many cases, the invoice has not arrived yet either.

That point trips up many finance committee members. No invoice does not mean no obligation. If the church already received the service, used the utility, or benefited from employee work, the expense exists.

A simple church example helps. If staff members worked the last few days of December and payroll runs in January, those wages still belong in December’s books. December received the labor. January handles the cash payment.

The same logic applies to fund-based accounting. If work was done for a restricted ministry in the current period, the expense should be assigned to that fund in the current period when supportable. If it is left out until later, both the fund report and the church-wide statements can give the board the wrong picture of what remains available for that ministry purpose.

Why this matters for stewardship

Matching is about more than tidy bookkeeping. It is about honest ministry reporting.

Board members need to know whether a reported surplus reflects actual operating results or whether part of that surplus is really unpaid payroll, utilities, or ministry services already consumed. Donors who gave to a benevolence fund, missions fund, or building fund deserve reports that respect the purpose of those gifts. Recording accrued expenses in the right period helps the church avoid spending money that only appears to be free.

The same tension shows up outside church finance too. This article on financial planning for business owners explains why healthy-looking results and available cash are not always the same thing. Churches face that same timing problem, with an added responsibility to keep restricted and unrestricted funds clearly separated.

When a church follows the matching principle, the numbers line up more closely with the ministry that occurred. That gives the finance committee a cleaner view of each fund, a truer view of the period, and a stronger basis for stewardship decisions.

Common Accrued Expenses in a Church Setting

Churches usually don’t struggle with accrued expenses because the idea is too advanced. They struggle because the costs are ordinary. Ordinary things are easy to miss.

Four situations that show up all the time

The first and most common example is payroll. A church may run payroll after month-end, but employees already earned those wages in the prior period. That earned but unpaid amount is an accrued expense.

The second is utilities. The lights were on, the sanctuary was heated, the children’s wing used water, and the office internet kept running. The service happened this month even if the bill won’t arrive until next month.

Third, there’s interest or occupancy costs. Some churches pay rent after month-end. Others have loans where interest keeps building between payment dates. Those obligations don’t pause just because the calendar hasn’t reached invoice day.

Fourth, there are services received but not yet invoiced. A maintenance contractor may finish a repair before the close of the month and send the bill later. A practical example from Wall Street Prep’s accrued expense guide notes that if a church hires a consultant to perform maintenance work at the end of April for $1,500, and the invoice hasn’t yet been submitted, that $1,500 still needs to be recorded in April’s financial statements.

If the work is done, the obligation exists. The invoice only confirms it.

Why these examples trip people up

None of those items feels unusual. That’s the problem.

A treasurer may review paid bills and believe the books are current because every processed check has been entered. But accrued expenses live in the gap between service and payment. You have to look for what has happened, not just for what has cleared the bank.

Here are some prompts that help churches spot likely accruals:

- Review payroll calendars: Ask whether any staff time was earned before month-end but paid afterward.

- Scan regular vendors: Utilities, rent, loan interest, and recurring service providers often create month-end obligations.

- Ask ministry leaders: They may know about completed work before the invoice reaches the office.

- Check maintenance and events: End-of-month repairs, guest services, and temporary support often fall into this category.

Churches with paid time off policies also run into related timing questions around leave and payroll obligations. If your team needs a plain-language explanation of that area, this guide on calculating accrued holiday can help clarify how earned time accumulates before it’s used or paid.

Why churches need to think at the fund level

A church doesn’t just need to identify the expense. It also needs to identify which fund benefited.

If a utility expense supported general operations and a youth ministry space funded by designated giving, the liability shouldn’t be treated as a vague church-wide afterthought. The allocation matters. Otherwise, one fund may appear healthier while another implicitly benefits from costs it never absorbed.

That’s where routine accrual review becomes a stewardship habit, not just an accounting task.

How to Record Accrued Expenses with Journal Entries

The mechanics offer clarity. The concept sounds abstract until you write the entry.

The month-end adjusting entry

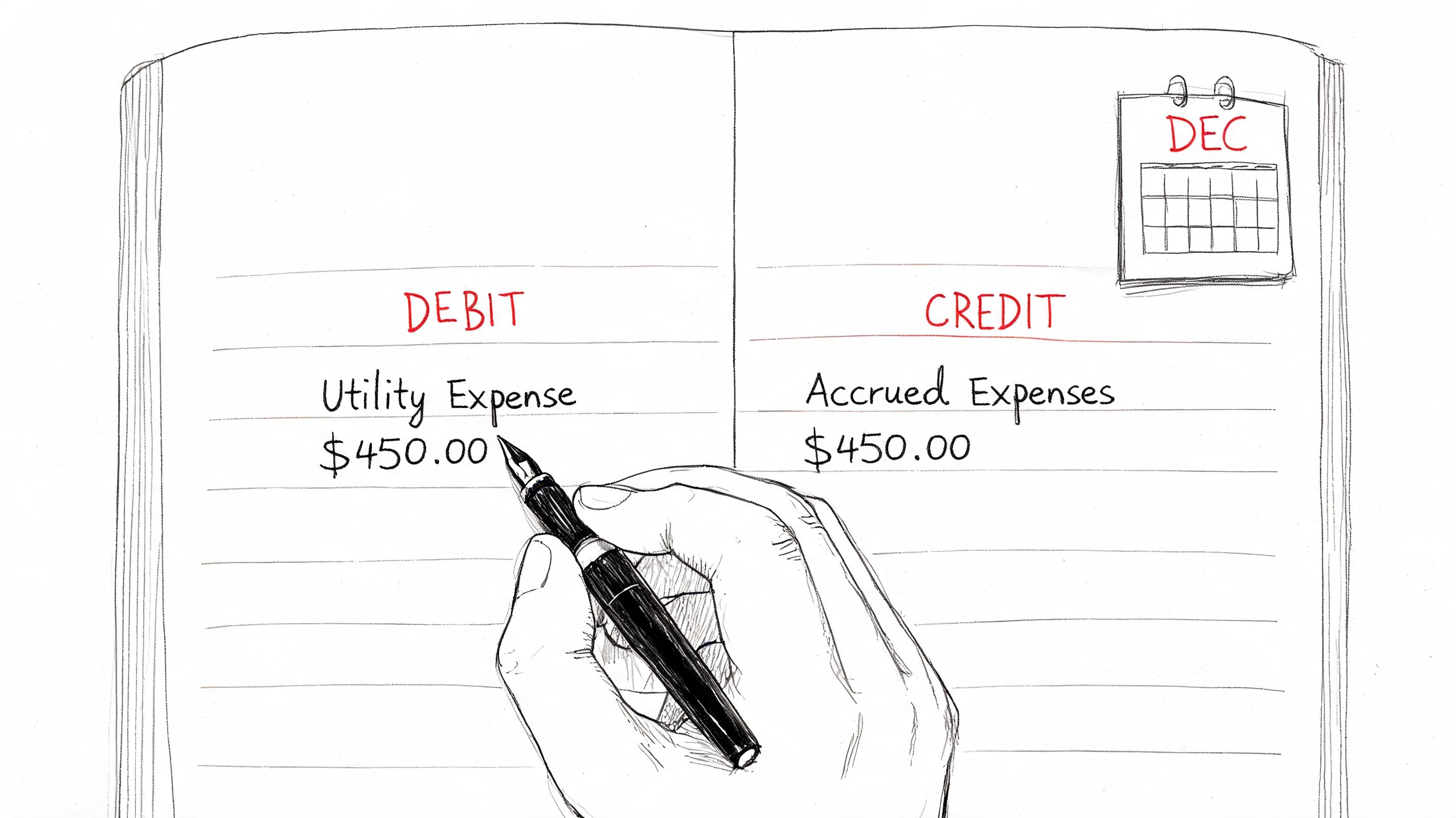

Let’s use a simple church example. The church used electricity during the month, but the bill hasn’t arrived by the time you close the books.

At month-end, you record an adjusting journal entry:

- Debit Utilities Expense

- Credit Accrued Liabilities or Utilities Payable

Why this entry?

The debit records the cost in the period when the church used the electricity. The credit records the obligation the church now owes. One side updates the income statement. The other updates the balance sheet.

That’s the whole logic of the entry. You are saying, “We used this service, and we owe for it.”

If journal entries still feel intimidating, Grain has a clear walkthrough on how to do journal entries that helps newer treasurers understand what each side of the entry is doing.

Key check: An accrued expense increases current-period expense and creates a liability. It does not reduce cash yet.

What changes on the statements

When you post that adjusting entry, two reports change.

On the income statement, expenses go up. That lowers the current period’s reported surplus.

On the balance sheet, liabilities go up. That shows the church owes money for a service already received.

Often, finance committee members experience an “oh, I see it now” moment. The cash account hasn’t changed, but the church’s financial position has. The organization is carrying an obligation that wasn’t visible before the accrual.

What happens when the bill gets paid

In the next period, the bill arrives and the church pays it. At that point, you remove the liability and reduce cash.

The payment entry is:

- Debit Accrued Liabilities

- Credit Cash

That entry clears the amount you recorded earlier. You’re no longer estimating an obligation. You’re settling it.

If the actual bill differs from what you accrued, you adjust for the difference when you record the invoice or payment. The goal isn’t to predict the future perfectly. The goal is to keep each period honest, then true things up when final documentation arrives.

A quick visual explanation can help if you’re teaching this to a committee or volunteer bookkeeper.

A simple rhythm churches can follow

Many churches do well with a repeatable close process:

- List likely accruals near month-end. Payroll, utilities, rent, interest, and completed vendor work are common places to start.

- Estimate carefully when the bill hasn’t arrived. Use contracts, schedules, prior bills, or known terms.

- Post the adjusting entry before finalizing reports.

- Reverse or clear the accrual when the actual bill is entered and paid.

- Review fund coding so the expense and liability hit the right ministry buckets.

That final step matters more in a church than in many small businesses. An accrual isn’t fully recorded until it’s assigned to the correct fund context.

Accrued Expense vs Accounts Payable vs Prepaid Expense

These terms get mixed together constantly. They sound related because they are related. But they don’t mean the same thing.

The quick distinction

An accrued expense means the church has already received the benefit, but payment hasn’t happened yet, and often the invoice hasn’t arrived yet.

Accounts payable means the church has received the bill. The obligation is documented by an invoice and is ready to be paid through normal bill-pay workflow.

A prepaid expense is the opposite timing pattern. The church pays cash first, then receives the benefit over time. Annual insurance is the classic example. The church pays upfront, then recognizes the expense as coverage months pass.

When you’re unsure which term applies, ask two questions. “Have we received the service yet?” and “Have we received the invoice yet?”

Side-by-side comparison

| Term | Trigger | Timing of Cash Payment | Impact |

|---|---|---|---|

| Accrued Expense | Service or work has been received, but no invoice has been processed yet | Cash is paid later | Records an expense now and a liability now |

| Accounts Payable | Invoice has been received for goods or services already received | Cash is paid later | Records a payable based on the billed amount |

| Prepaid Expense | Cash is paid before the church receives the full benefit | Cash is paid first | Records an asset first, then expense over time |

A church-office way to remember it

If your custodian worked the final days of the month and payroll runs next week, that’s an accrued expense.

If the copier company emailed a bill for service already completed, that’s accounts payable.

If the church paid an annual insurance premium in advance, that’s a prepaid expense.

The confusion usually comes from focusing only on whether money moved. But the better way to classify the item is by looking at timing. Did the church receive the benefit before paying, after paying, or before getting the invoice?

For churches with multiple funds, classification errors do more than clutter the books. They can distort ministry reports. A prepaid item may overstate current expenses if expensed too quickly. A missed accrual can overstate available resources. A payable booked to the wrong fund can make one ministry look over-resourced and another underfunded.

Getting the category right protects decision-making.

Managing Accruals in Church Fund Accounting

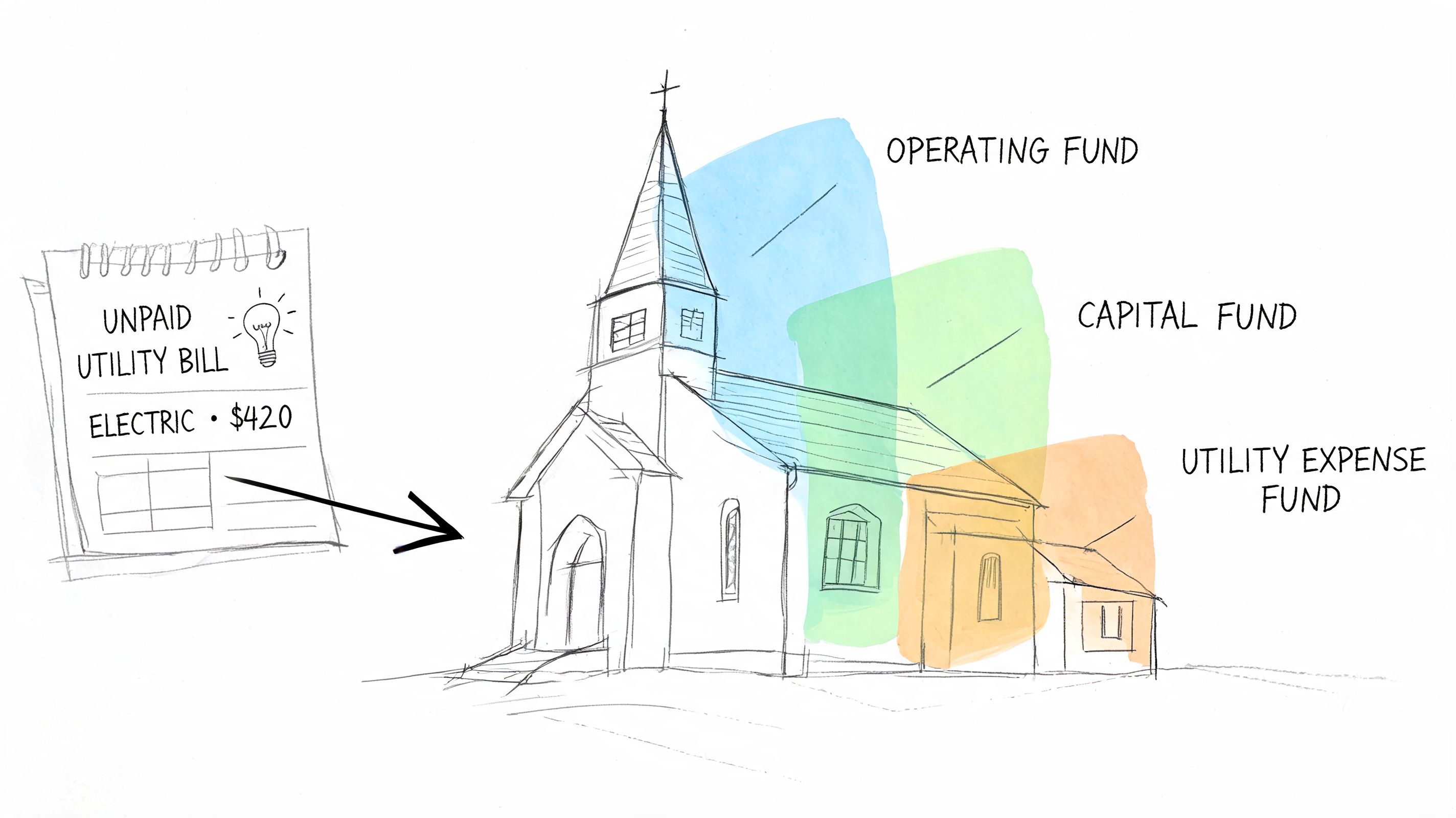

The committee sees a healthy bank balance at month-end and assumes there is room for one more ministry purchase. Then payroll for the last week of the month, an unpaid utility cost, and a counselor stipend all land in the next period. On paper, last month looked stronger than it was. In a church, that gap does more than blur timing. It can blur which fund is carrying the obligation.

General explanations of accrued expenses usually assume one pool of money. Churches rarely operate that way. A church may have a general fund, a missions fund, a building fund, and other restricted gifts that must be used for a stated purpose. An accrual has to answer two questions, not one. What expense belongs in this period, and which fund should bear it?

The fund allocation question churches can't ignore

A church building often serves several ministries at once. Sunday worship meets in the sanctuary. Youth gathers midweek. A counseling ministry uses office space. A benevolence pantry may use storage rooms. If the church has consumed utilities by month-end but has not received the bill, the accrual should not sit in one vague bucket if multiple funds benefited from that cost.

That is where fund integrity gets protected or weakened.

A useful summary of the general accrual issue appears in Ramp’s discussion of accrued expenses. The missing piece for many churches is fund allocation. If part of an unpaid cost relates to a restricted ministry activity and part relates to normal operations, the liability should be assigned accordingly. Otherwise, unrestricted reports can look stronger, while a restricted fund benefits without showing its share of the cost.

Why a cash balance can mislead a committee

Cash answers one question. Accruals answer another.

The bank balance tells you how much cash is on hand. It does not tell you how much of that cash is already spoken for by work received, services consumed, or obligations incurred before month-end. FinQuery’s explanation of accrued expenses and accrued liabilities helps frame that timing issue. In a church, the practical concern is fund reporting. A general fund can appear available for new spending even though unpaid obligations have already reduced what is available for ministry decisions.

Committee members often need a simple picture here. The church checkbook is like the offering count after Sunday. It shows what came in. It does not show every commitment the church has already made. Fund-based accrual accounting adds that second half of the picture so leaders do not spend restricted or unrestricted resources as if they were still fully free.

A practical system matters

A church can manage this well with a disciplined process, but the system has to support fund-level thinking. If staff track unpaid costs in side spreadsheets and reassign them later, month-end reports are more likely to miss a fund split or leave an accrual in the wrong place.

Grain Ledger is built around funds from the start, which helps churches assign expenses and liabilities at the fund level instead of forcing church reporting into a general-business structure. For more background on that approach, see this article on fund accounting for churches.

The workflow side matters too. Teams in many settings lose time when recurring expenses are gathered inconsistently, and a piece on how NZ remote teams save hours shows that expense handling depends on process as much as accounting rules.

Churches need accurate totals by fund, not just accurate totals in total.

The stewardship issue underneath the accounting

A missed or misallocated accrual can distort ministry reports. The general fund may appear to have more room than it does. A restricted fund may seem untouched by costs connected to the ministry it supports. Leaders may approve spending based on balances that do not reflect obligations already incurred.

That usually comes from ordinary oversight, not bad intent. Still, the result is the same. Reports stop matching reality.

Accrual accounting serves stewardship best when the expense and the liability follow the same ministry purpose as the underlying activity. That is how a church preserves donor intent, presents honest fund balances, and helps the finance committee make decisions that protect every fund entrusted to its care.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

A Treasurer's Checklist for Accrued Expenses

A good month-end close doesn’t need to be elaborate. It needs to be consistent.

Questions worth asking before you finalize reports

- Have staff earned wages that haven’t been paid yet? Review payroll dates against the reporting period.

- Did the church receive utilities or other recurring services that won’t be billed until later? Those often need accruals.

- Did any contractor, consultant, or repair vendor finish work before month-end without sending an invoice yet?

- Have we assigned each accrual to the correct fund? Don’t stop at the total amount.

- Will the board understand the difference between cash on hand and obligations already incurred?

One final caution about cash flow

Accrual accounting improves accuracy, but accuracy doesn’t automatically solve cash pressure.

QuickBooks’ discussion of accrued expenses points out a real challenge for churches and small nonprofits with unpredictable giving patterns: an organization can properly record accrued liabilities and still struggle to pay them if incoming cash falls short. In plain terms, your reports can be right while your bank balance is tight.

That’s why a treasurer should watch both sides of the picture:

- Accrual reporting tells you what the church actually owes.

- Cash monitoring tells you whether the church can pay those obligations when due.

If you’re training a committee chair or refining your own monthly responsibilities, this guide to the responsibilities of treasurer in a non-profit is a useful companion.

The healthiest rhythm is simple. Record obligations accurately. Protect fund integrity carefully. Watch liquidity closely. That combination gives pastors, boards, and congregations a financial picture they can trust.

If your church wants accounting that reflects how ministry money works, Grain is worth a look. It’s built for church fund accounting, so transactions, balances, and reports stay tied to the funds that matter for stewardship, restricted giving, and board-level clarity.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.