What Is Bank Reconciliation: Church Finance Guide

Learn what is bank reconciliation and why it's vital for church finance. Our guide covers fund accounting, common errors, and how to simplify the process.

Bank reconciliation is the process of comparing the church's general ledger to the bank statement so the accounting balance matches the bank balance on a specific date, and it typically follows five core steps. It's like balancing your personal checkbook for the church, except the goal is bigger than neat records. You're making sure every dollar, especially money given for a specific purpose, is accounted for correctly.

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Start free to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

If you're serving on a finance committee, you've probably seen the moment when the treasurer says, “The bank says one thing, our books say another.” That moment can feel unsettling, especially in a church where trust matters as much as accuracy.

Most of the time, the difference doesn't mean anyone did something wrong. A deposit may not have cleared yet. A check to a missionary may still be outstanding. The bank may have charged a fee that no one entered into the ledger. But until someone works through those items carefully, you don't really know your true cash position.

That's why people ask, what is bank reconciliation? In plain terms, it's the habit of proving that your internal records and the bank's records agree. For churches, that matters twice over. You need to know how much cash is in the account, and you need to know whether those dollars still belong to the right funds.

Your Guide to Financial Peace of Mind

A church treasurer usually learns the importance of reconciliation in a very ordinary way. Sunday offerings are counted, online gifts come in through a giving platform, bills are paid, payroll runs, and then month-end arrives. The reports look mostly right, but not quite. There's a difference that nobody can explain quickly.

That's where reconciliation brings peace of mind. It turns a vague concern into a clear process.

The simple way to think about it

If you've ever balanced a personal checkbook, you already understand the basic idea. You compare what you think happened with what the bank says happened. Then you identify the items that explain the gap.

In a church, that same idea applies to the operating account, missions account, or any other cash account. The difference is that churches often handle many small gifts, special offerings, and designated donations. So the work needs a little more care.

Bank reconciliation isn't mainly about paperwork. It's about proving that the church's records tell the truth.

A clean reconciliation answers practical questions:

- How much cash is available: Not just what the ledger says, but what can be relied on.

- Which transactions still need explanation: Deposits, checks, transfers, fees, or mistakes.

- Whether the books need adjustment: Sometimes the bank is right and the church record is incomplete.

- What the board can trust: Financial reports become more useful when cash balances have been verified.

Why new committee members often get confused

The most common confusion is this: people assume the bank balance is automatically the “real” number. It isn't always that simple.

A bank statement reflects what the bank has processed. Your ledger reflects what the church has recorded. Those two records are related, but they don't update in exactly the same way or on exactly the same day.

For example, the church may receive a weekend offering and record it right away, but the deposit may not appear on the bank statement until later. Or a check may have been written and entered in the books, while the recipient hasn't deposited it yet.

What reconciliation gives a church

When done consistently, reconciliation gives more than tidy bookkeeping. It gives confidence. The treasurer can report with less hesitation. The finance committee can review numbers with fewer unanswered questions. The pastor and board can make decisions without wondering whether the cash balance is overstated or incomplete.

That's why this process belongs in stewardship, not just accounting.

The Core Purpose of Bank Reconciliation

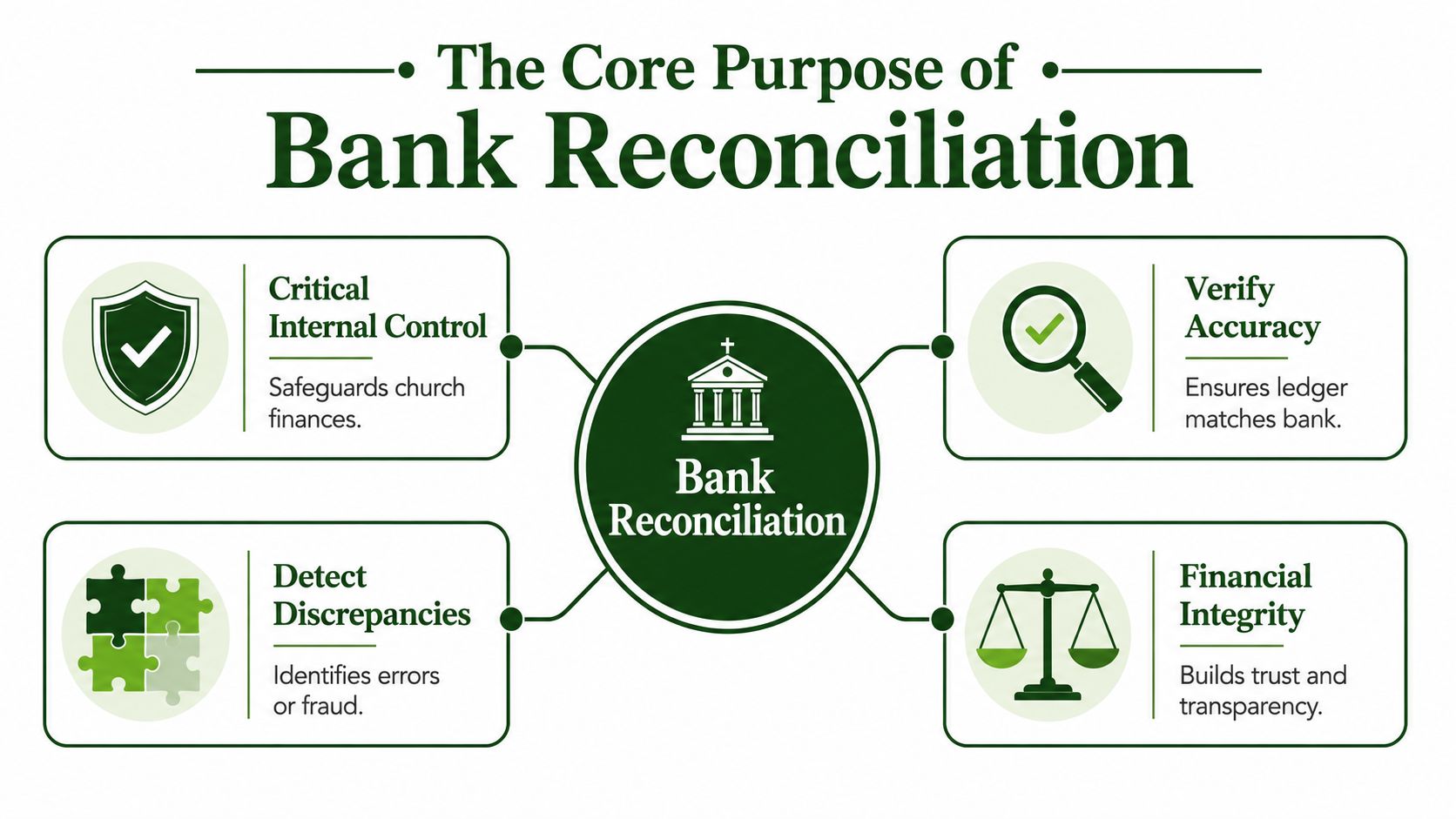

At its heart, bank reconciliation is an internal control. It compares your church's cash records to an independent outside record from the bank. That independent comparison is what makes it so valuable.

According to this description of bank reconciliation and financial integrity, bank reconciliation is a critical accounting control process that compares the general ledger against the bank statement so the accounting balance matches the bank balance on a specific date, while identifying discrepancies such as unrecorded payments, missed receipts, forgotten bank fees, or data entry errors.

Why this matters in a church

A business reconciles cash because management needs reliable numbers. A church reconciles cash for that reason too, but also because people have entrusted gifts to the ministry.

When someone gives to the general fund, the church should be able to report that money accurately. When someone gives to a building fund or missions project, the need for accuracy becomes even more sensitive. The congregation expects care, transparency, and accountability.

Core principle: Reconciliation helps the church show that its internal records agree with an external record, which protects trust as well as accuracy.

This is also why strong churches pay attention to fund accounting for churches, not just total cash. A healthy bank balance doesn't tell you whether restricted money has stayed in the right place inside the books.

What reconciliation is really doing

Bank reconciliation serves several purposes at once:

| Purpose | What it means for the church |

|---|---|

| Accuracy | The reported cash balance is verified, not assumed |

| Error detection | Missing fees, duplicate entries, and posting mistakes get caught |

| Fraud prevention | Unusual or unauthorized transactions are easier to spot |

| Transparency | The board and congregation can rely on cleaner reporting |

One reason readers get tripped up is that reconciliation sounds like a narrow bookkeeping task. In practice, it supports much bigger decisions. If the church is planning payroll, approving benevolence support, or committing funds to an event, leaders need to know what cash is available.

The result is a documented record

A completed reconciliation should leave a paper trail. It should show which items matched, which ones didn't at first, and what was done to resolve the difference. That record matters during internal review and becomes especially useful if an auditor, finance chair, or elder board member asks how the reported balance was confirmed.

So when someone asks what is bank reconciliation, the technical answer is straightforward. The practical answer is even more important. It's the discipline that turns “we think these numbers are right” into “we have verified these numbers are right.”

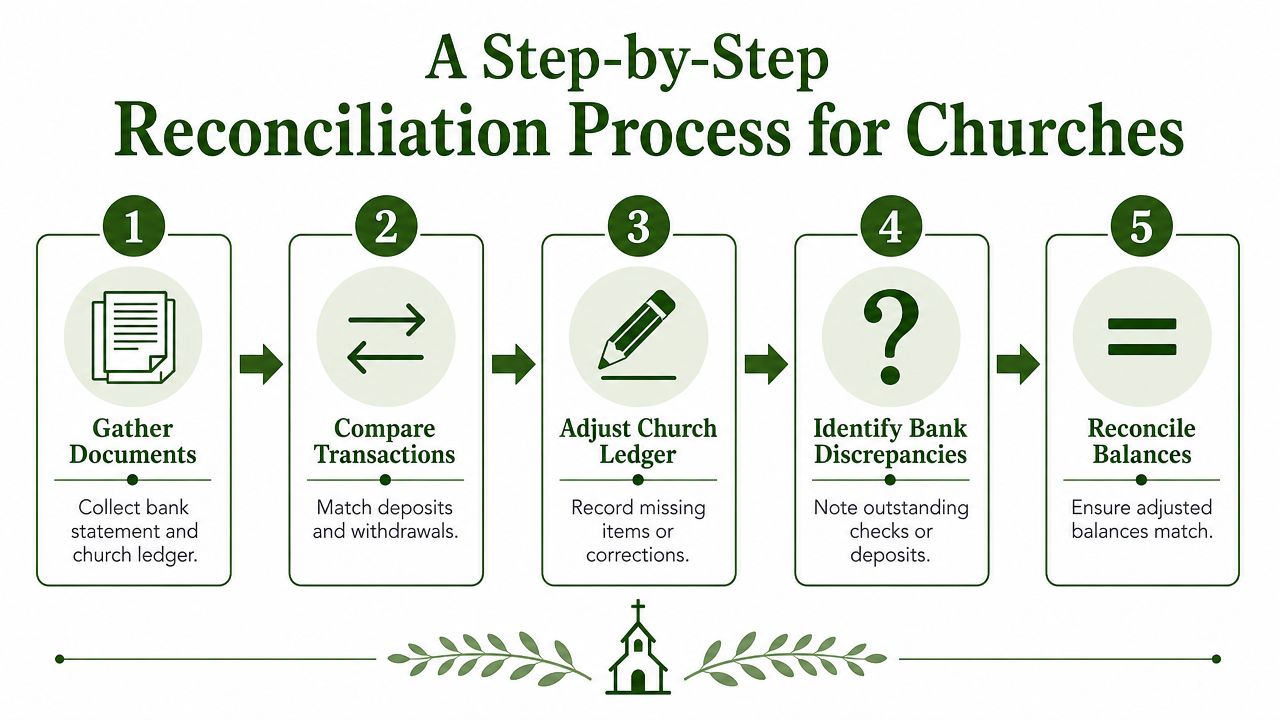

A Step-by-Step Reconciliation Process for Churches

The process works best when it's done in the same order each time. That keeps small questions from turning into long month-end hunts.

A common workflow is described in this overview of bank reconciliation matching: teams extract general ledger cash balances, align bank statements by closing period, and perform line-by-line matching to surface unmatched items such as deposits in transit or outstanding checks.

Step 1 Gather your records

Start with the documents for the same period:

- Bank statement: Use the closing statement for the month or period you're reconciling.

- Church ledger or cash book: Pull the cash account activity from your accounting records.

- Supporting records: Deposit slips, online giving reports, check registers, and payment records help explain exceptions.

Before matching individual transactions, confirm that your opening balance agrees with the previous closing balance. If it doesn't, stop there and resolve that first.

Step 2 Match deposits carefully

Look first at money coming in. For a church, that may include Sunday offerings, online gifts, special event proceeds, or a transfer from another account.

Suppose the church counted the weekend offering on Sunday and entered it in the books that day. If the bank processes the deposit a little later, the ledger will show it before the statement does. That's a normal timing difference, often called a deposit in transit.

A timing difference isn't automatically an error. It becomes a problem only when nobody can explain it.

Step 3 Match withdrawals and payments

Next, compare what went out. This includes checks, ACH payments, card expenses, payroll drafts, and vendor payments.

A common church example is a check sent to a missionary or guest speaker near the end of the month. The church recorded it when the check was issued, but the bank hasn't cleared it yet. That item remains an outstanding check until it appears on the statement.

Here's a simple checklist:

- Check numbers: Make sure the amount and payee line up with the ledger.

- Electronic payments: Review card charges and ACH drafts for utilities, software, or insurance.

- Transfers: Confirm both sides of any movement between accounts were recorded correctly.

A short visual walkthrough can help if you're training volunteers or new committee members:

Step 4 Record items the bank entered

Banks often post transactions the church didn't enter first. These may include service charges, interest, returned items, or other adjustments. If those appear on the statement but not in the books, the church ledger needs to be updated.

This is the point where many manual reconciliations go sideways. The statement gets reviewed, but the missing journal entry never gets posted. The reconciliation may look complete on paper while the books remain incomplete.

Step 5 Finish with a reconciliation statement

When you've matched what you can, list the remaining valid differences and prepare the final reconciliation statement. This record should show why the starting balances differed and how the adjusted balances now agree.

A good reconciliation doesn't just say “fixed.” It shows the path from difference to agreement.

Reconciling Restricted Funds A Church-Specific Challenge

Here, church finance stops looking like ordinary bookkeeping.

A family gives to the Building Fund because they want to help replace the roof. Another member gives to Youth Ministry for camp scholarships. The weekly tithe goes into general operations. All three gifts may land in the same bank account, but they are not the same kind of money.

Why total cash is not enough

A basic bank reconciliation tells you whether the cash account in the ledger agrees with the bank statement. That's necessary, but for a church it's not sufficient.

Church accounting also needs to show that each donation was assigned to the correct fund. This church accounting guidance on transaction-to-fund matching explains that bank reconciliation in church accounting requires matching every donation transaction from the bank against the corresponding fund entry in the ledger so restricted funds such as Building Fund or Youth Ministry aren't mixed with unrestricted tithes.

That distinction matters because a church can be cash-positive and still mishandle fund balances internally. The account may reconcile perfectly while donor restrictions are being blurred in the books.

A common real-life scenario

Say the church receives a special gift for a youth mission trip. The deposit reaches the bank with other donations from the week. On the statement, it may look like one lump sum. But in the ledger, that money should still be separated into the right funds.

If someone later pays a general operating bill from the same bank account, the bank balance goes down. That isn't automatically wrong. What matters is whether the ledger still preserves the restricted amount in the mission trip fund.

Churches don't just need bank-level accuracy. They need fund-level integrity.

Many committees get uneasy. They can see the bank account has money in it, but they can't always answer a simple question from a donor or elder: “How much of that belongs to the building project, and how much is available for general ministry?”

Why manual methods strain under church giving patterns

Churches often process many small gifts, recurring donations, and designated offerings. Manual spreadsheets can track this for a while, but they become fragile as volume grows. One miscoded entry can move money from the right fund into the wrong one without changing the total bank balance.

That's also why related documentation matters. When leaders need outside confirmation about balances or transactions, they often rely on records such as a bank confirmation letter in church finance workflows alongside internal reconciliations.

What good reconciliation looks like in a church

A church-specific reconciliation process should help you answer three separate questions:

- Did the bank transaction occur: Was the deposit or withdrawal real and properly recorded?

- Was it posted to the right fund: Did the gift stay in Building Fund, Youth Ministry, or General Fund as intended?

- Can you explain the current balance: Not just total cash, but what portion is restricted versus available?

When those answers are clear, the church is protecting more than numbers. It's protecting donor trust.

Common Errors and The Path to Simpler Stewardship

A church can finish the month with a bank balance that looks right and still have a stewardship problem.

That usually happens when the total cash is correct but the fund assignments are not. The money is in the account, yet the records cannot clearly show what belongs to missions, what belongs to the building fund, and what is available for general ministry. For a finance committee, that is like having a well-stocked pantry with unlabeled shelves. You know the food is there, but you cannot quickly tell what was set aside for a specific meal.

Where manual reconciliation breaks down

Manual reconciliation often catches math errors. It is weaker at catching intent errors.

A spreadsheet may still balance after a designated gift is posted to the wrong fund. A transfer may be recorded in the right amount but tied to the wrong purpose. In church accounting, those are not small clerical issues. They affect whether leaders can show that restricted gifts were handled as promised.

The common trouble spots

Church teams usually run into the same handful of problems:

- Posting errors: A gift or payment is entered with the wrong amount, date, or account.

- Missing bank activity: Fees, interest, returned items, or corrections appear on the statement but never make it into the books.

- Fund miscoding: A restricted donation is recorded in the wrong fund, even though the deposit itself is real.

- Unclear follow-up: Someone sees a mismatch, but no one knows who should research it or how it should be documented.

- Spreadsheet sprawl: Several versions of the same file circulate, and the team loses confidence in which one is current.

One mistake can be corrected. A pattern of small mistakes creates confusion at board meetings, slows down year-end reporting, and makes donor questions harder to answer with confidence.

A simpler way to handle it

Churches usually need more than a matching tool once giving volume grows. They need a process, or software, that ties together bank activity, ledger entries, and donor restrictions in one place.

That is the true test. Can the system show that a transaction cleared the bank and stayed attached to the right fund?

For this reason, when a church asks me what accounting solution to consider, I point them to bank reconciliation software built for church fund accounting. Grain is designed for churches, connects bank accounts and giving tools such as Pushpay, Planning Center, and Stripe, and keeps fund tracking connected to the reconciliation process instead of treating it as a separate cleanup task.

Practical rule: If your software reconciles the bank balance but cannot preserve restricted fund integrity, it only solves part of the problem.

That kind of setup reduces repetitive matching work and makes exceptions easier to review. It also gives the treasurer and finance committee a clearer trail from donor intent to deposit to final ledger entry.

For a small church, that may mean fewer late nights at month-end.

For a larger volunteer-led team, it often means the process no longer depends on one person remembering how a spreadsheet was built. That is simpler stewardship.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

From Financial Chore to Ministry Tool

Bank reconciliation can feel like a monthly burden when you first inherit it. There's a statement to download, transactions to match, questions to investigate, and adjustments to post. If the records are messy, it can feel like cleanup work instead of ministry work.

But the purpose is bigger than the chore.

What the process makes possible

Bank reconciliation supports accurate reporting and fraud prevention by comparing internal cash records with the bank statement, and it gives leaders clearer visibility into actual cash availability. In a church setting, that visibility affects real decisions. Can the church commit to a ministry expense now? Is a designated fund still fully protected? Are the reports ready for the board meeting with confidence instead of caveats?

When reconciliation is done well, leaders stop guessing. They can govern with cleaner information.

| Old experience | Better experience |

|---|---|

| Unclear differences at month-end | Differences identified and explained |

| Total cash only | Visibility into cash and fund intent |

| Spreadsheet-driven memory | Documented, repeatable process |

| Volunteer stress | Shared confidence and easier review |

Stewardship is the larger goal

What is bank reconciliation, then? It's a control process, yes. It's also a stewardship habit.

A church that reconciles well can answer honest questions without defensiveness. It can show where money came from, where it went, and whether restricted gifts stayed restricted. That kind of clarity strengthens trust with pastors, elders, givers, and auditors.

Good reconciliation gives church leaders freedom. They spend less energy doubting the numbers and more energy using them wisely.

For teams that want to modernize the process, purpose-built tools can help reduce manual work and preserve a clean audit trail. If you want to explore what that looks like in practice, bank reconciliation software for churches is a useful place to start.

The end goal isn't perfection for its own sake. It's confidence. When the books are reliable, the church can report accurately, plan carefully, and focus more attention on ministry than on untangling spreadsheets.

If your church is ready to move from manual matching to fund-aware reconciliation, take a look at Grain. It's church accounting software designed around funds from the start, so your bank activity, giving records, and reports stay aligned with the way churches steward money.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.