What Is Modified Cash Basis Accounting: Your 2026 Guide

Learn what is modified cash basis accounting, how it works for churches, and its differences from cash & accrual methods. Get the 2026 insights here!

You're probably in a meeting with a pastor, a board member, or a finance committee volunteer who asks a fair question: “Are we doing okay financially?”

About Grain Ledger: This guide includes Grain Ledger, church fund accounting software built for designated gifts and ministry funds. It connects giving platforms (Planning Center, Pushpay, Tithely, Stripe), syncs bank activity with Plaid, and produces fund-level financial reports. Start free to see how it compares for your church.

See Grain Ledger for your church

Fund accounting, giving integrations, and bank reconciliation in one platform. Free migration support for churches switching from QuickBooks or Aplos.

You can answer part of that by opening the bank balance. But that doesn't tell the whole story. It doesn't show the church van you bought last year, the mortgage on the building, or the mission trip gifts that can't be spent on general operations. A simple check register is helpful, but it leaves out some of the very things church leaders most need to steward well.

Full accrual accounting solves some of that. It also brings a level of complexity that can feel heavy for a small or medium-sized congregation. That's where many churches start asking what is modified cash basis accounting, and whether it might be the right fit.

Finding a Better Way for Church Finances

A lot of churches begin with bookkeeping that feels practical because it mirrors the bank account. Tithes come in. Bills get paid. The treasurer prints a report and tells the committee how much cash is on hand. That works, until the church grows, takes on a building loan, or starts managing several designated funds at once.

A church might have money set aside for benevolence, youth camp, missions, and building repairs. On paper, the checking account looks healthy. In reality, much of that money is already spoken for. If the report doesn't separate those purposes clearly, leaders can make decisions with the wrong picture in front of them.

When simple books stop being enough

I've seen this happen in churches that were trying to be faithful, not careless. The problem wasn't bad intent. The problem was that the books answered only one question: “What cash moved?” They didn't answer “What does the church own?”, “What does it owe?”, or “Which dollars are restricted?”

That's where modified cash basis becomes useful. It sits between a plain cash system and full accrual. It keeps the day-to-day simplicity many churches need, while adding a clearer view of long-term assets, debts, and stewardship responsibilities.

Churches don't just need to know what cleared the bank. They need reports that help leaders honor donor intent and make wise ministry decisions.

If your church also needs guidance on nonprofit tax obligations alongside bookkeeping choices, EndureGo Tax for nonprofit entities offers a practical overview that can help finance teams keep tax questions separate from internal reporting questions.

Why churches feel this tension

Church finances are rarely just about transactions. They're about trust.

Members give because they believe the church will handle those gifts carefully. Elders approve budgets because they want ministry plans grounded in reality. Treasurers need a method that supports that responsibility without turning every month-end close into a technical exercise built for a large corporation.

Modified cash basis often becomes that middle path. It gives a church more clarity than a pure cash method, without forcing the whole team into the complexity of full accrual accounting.

Comparing Cash Accrual and Modified Cash Methods

The easiest way to understand the three methods is to compare them side by side.

Cash basis is like checking your wallet. You know what money is there right now.

Accrual basis is like a full household financial plan. It tracks what you owe, what others owe you, and what belongs to this month even if cash hasn't moved.

Modified cash basis is the middle ground. It still pays close attention to actual cash, but it also keeps certain long-term items on the books so the picture is more useful.

According to Bench's explanation of modified cash basis accounting, modified cash basis accounting is a hybrid method that records short-term items on a cash basis and long-term items on an accrual basis. That means revenue is generally recognized when collected and expenses when paid for cash items, while long-term assets, depreciation, income tax accruals, and loan liabilities can also appear in the records.

How each method feels in practice

Under cash basis, your treasurer can usually answer, “How much money is in the bank?” very quickly. That's helpful for weekly operations. But if the church bought sound equipment or still owes on a mortgage, those realities may not appear in the same meaningful way.

Under accrual basis, the books are more complete. They're also more demanding. You're tracking receivables, payables, timing differences, and more frequent adjusting entries.

Modified cash basis aims to keep the bookkeeping workable while improving visibility. If you want a deeper primer on full accrual itself, this guide on what accrual accounting is is a useful companion.

Accounting Methods Compared

| Feature | Cash Basis | Modified Cash Basis | Accrual Basis |

|---|---|---|---|

| Revenue recognition | When cash is received | Usually when cash is received for day-to-day items | When revenue is earned |

| Expense recognition | When cash is paid | Usually when cash is paid for day-to-day items | When expenses are incurred |

| Long-term assets | Often not fully reflected as assets | Recorded on the books | Recorded on the books |

| Depreciation | Usually absent | Included for capital assets | Included |

| Loan liabilities | Often limited or not fully shown | Recorded for long-term debt | Recorded |

| Complexity | Lowest | Moderate | Highest |

| Usefulness for internal church reporting | Basic cash view | Strong middle-ground view | Very detailed |

| GAAP alignment | No | No | Yes |

Why the middle ground matters

For churches, the choice usually comes down to stewardship and workload. A pure cash report can be too thin. A full accrual system can be too heavy. Modified cash basis gives leaders reports that are more informative without requiring the finance office to operate like a large audited institution.

Practical rule: If a report helps you see cash but hides your building, debt, or designated obligations, it's probably too simple for a growing church.

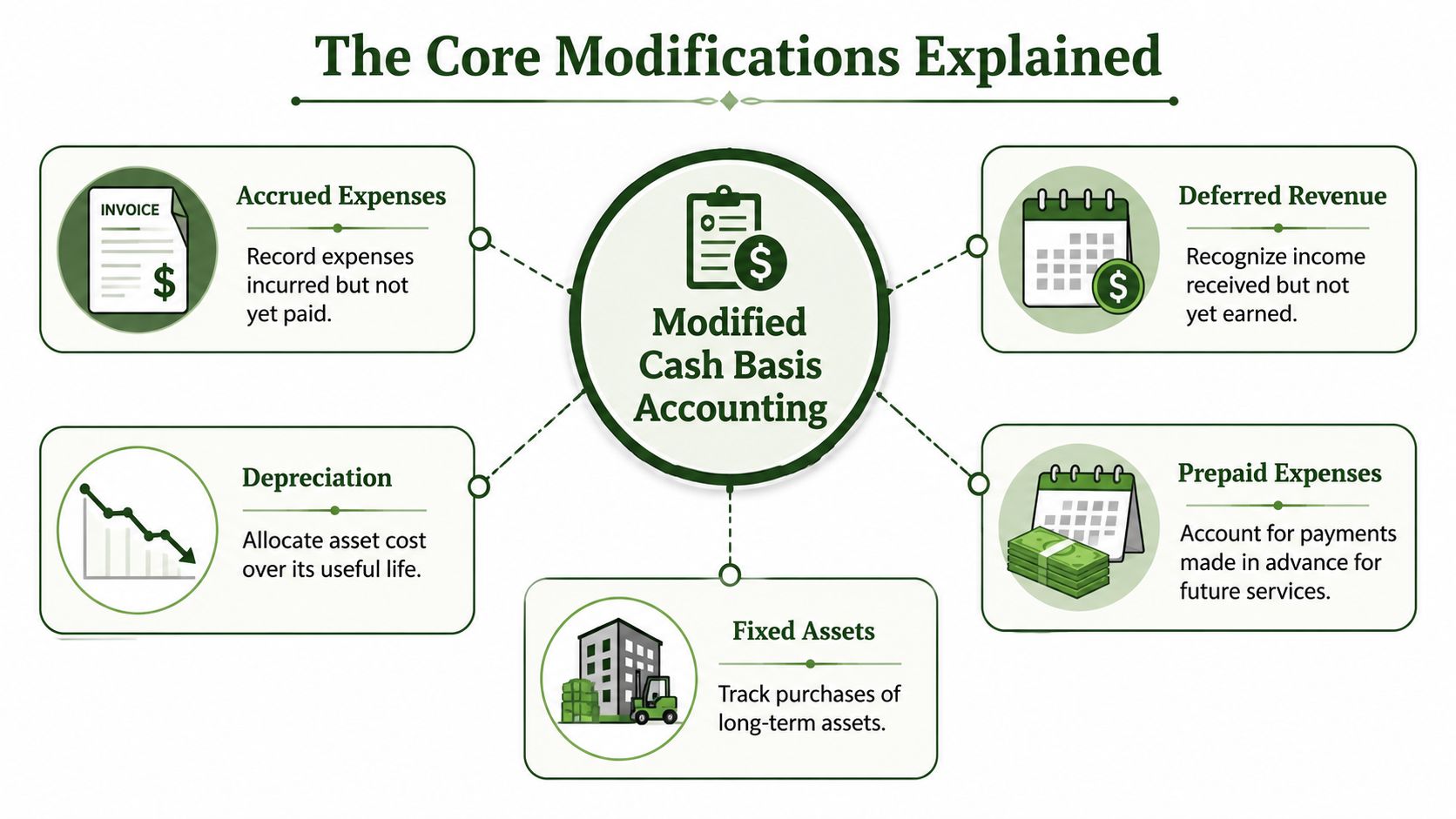

The Core Modifications Explained

The word modified matters. It tells you that you're not merely running a checkbook and calling it accounting. You're taking a cash-based system and adding a few important adjustments that make the reports more honest and useful.

According to Investopedia's overview of modified cash basis accounting, the method records long-term assets and long-term debt on an accrual basis while treating short-term assets on a cash basis, giving organizations a clearer financial picture without the full complexity of GAAP.

Fixed assets and capitalization

Suppose your church buys a new van, replaces the sanctuary sound system, or renovates a classroom wing. Under a simple cash system, the entire payment might hit the books as an expense right away.

Modified cash basis often handles that differently. Instead of treating the whole purchase as a current-period expense, the church records it as a fixed asset. That means the balance sheet shows that the church owns something with ongoing value.

Leaders can look at the statements and see more than this month's spending. They can see part of the church's financial strength.

Depreciation and long-term use

Once an item is capitalized, many churches record depreciation over time. That spreads the cost of a long-lived asset across the periods in which the church uses it.

You don't need to think of depreciation as a tax trick or accounting jargon. In plain language, it says this: if the church uses a building, piano, or van for years, the financial statements should reflect that ongoing use rather than act as if the entire benefit happened on purchase day.

Loans and other obligations

A church that has a mortgage or another long-term note shouldn't have to rely on memory or a file drawer to know that obligation exists. Modified cash basis brings those liabilities onto the balance sheet so the finance committee can see them plainly.

That doesn't make the system fully accrual. It means the church is no longer pretending that long-term obligations don't matter because the monthly payment hasn't gone out yet.

Other adjustments churches may add

Churches sometimes include a few other accrual-style adjustments, depending on how they want their reports to function.

- Deferred revenue: Useful when money is received before the related activity is complete. If you want a more detailed explanation, this article on accounting for deferred revenue is helpful.

- Prepaid expenses: Think of insurance or service contracts paid in advance.

- Accrued expenses: Some churches record important obligations that relate to the current period even if payment happens later.

The goal isn't to copy every feature of full accrual accounting. The goal is to add the adjustments that make the reports more truthful for ministry decisions.

Modified Cash Basis for Fund Accounting and Stewardship

Churches don't just track income and expenses. They track purpose.

A family gives toward youth camp. A member leaves a gift for building repairs. The congregation raises support for missionaries. Those dollars may all land in the same bank account, but they are not the same money in the eyes of stewardship. That's why modified cash basis becomes especially useful in churches.

According to Tabernacle's church accounting guide, modified cash basis records revenue when cash is received and expenses when paid, while also including capital assets and long-term liabilities on the balance sheet. That same source notes that this approach is often used by small churches and nonprofits and typically requires tracking restricted funds separately so donor intent is honored.

A church roof example

Let's say your church receives $50,000 for a new roof, and the gift is restricted for that purpose only, as described in the planning example for this topic. The money is deposited this month, but the roofing work won't happen until later.

Under a simple cash view, that deposit can make the month look like a big operating surplus. If the finance committee isn't careful, someone might think the church suddenly has far more room in the general budget than it really does.

Under a modified cash approach used with sound fund accounting, that gift is still recognized when received, but it is also tracked in the proper restricted fund. The report can show that the church has the cash while also showing that the money is designated for the roof, not available for payroll, curriculum, or utilities.

Why this protects trust

Churches live on trust. Donors rarely read a chart of accounts, but they do notice whether leadership treats designated gifts carefully.

When a church tracks restricted giving clearly, it can answer practical questions with confidence:

- Mission gifts: Are they still set aside for missions?

- Building funds: Has that money remained available for the project it was given toward?

- Benevolence support: Can leaders show that these gifts were used within the intended purpose?

A good framework for this is church fund accounting. If your committee needs a practical overview, this guide to fund accounting for churches explains the structure clearly.

A church can have cash in the bank and still not have spendable money in the general fund. Restricted gifts change what that cash is for.

Stewardship reports people can understand

One reason finance committees struggle is that many reports are technically correct but pastorally unhelpful. They bury the key issue. For churches, the key issue is often not just whether cash exists, but whether that cash is free for general ministry use.

Modified cash basis can help produce reports that answer both questions. The committee sees current cash activity. It also sees long-term obligations and designated balances with more clarity.

A short visual explanation can help when your team is learning the difference in reporting style.

What this looks like month to month

In practice, churches using this method often prepare reports that do a few things well:

| Report focus | Why it helps a church |

|---|---|

| Fund balances | Shows which dollars belong to which ministry purpose |

| Balance sheet with assets and debt | Helps leaders see buildings, equipment, and loans |

| Activity by fund | Makes donor-restricted activity easier to explain |

| Cash position | Keeps day-to-day decision making grounded |

That combination gives leaders something better than a checkbook view without requiring every volunteer to think like a corporate controller.

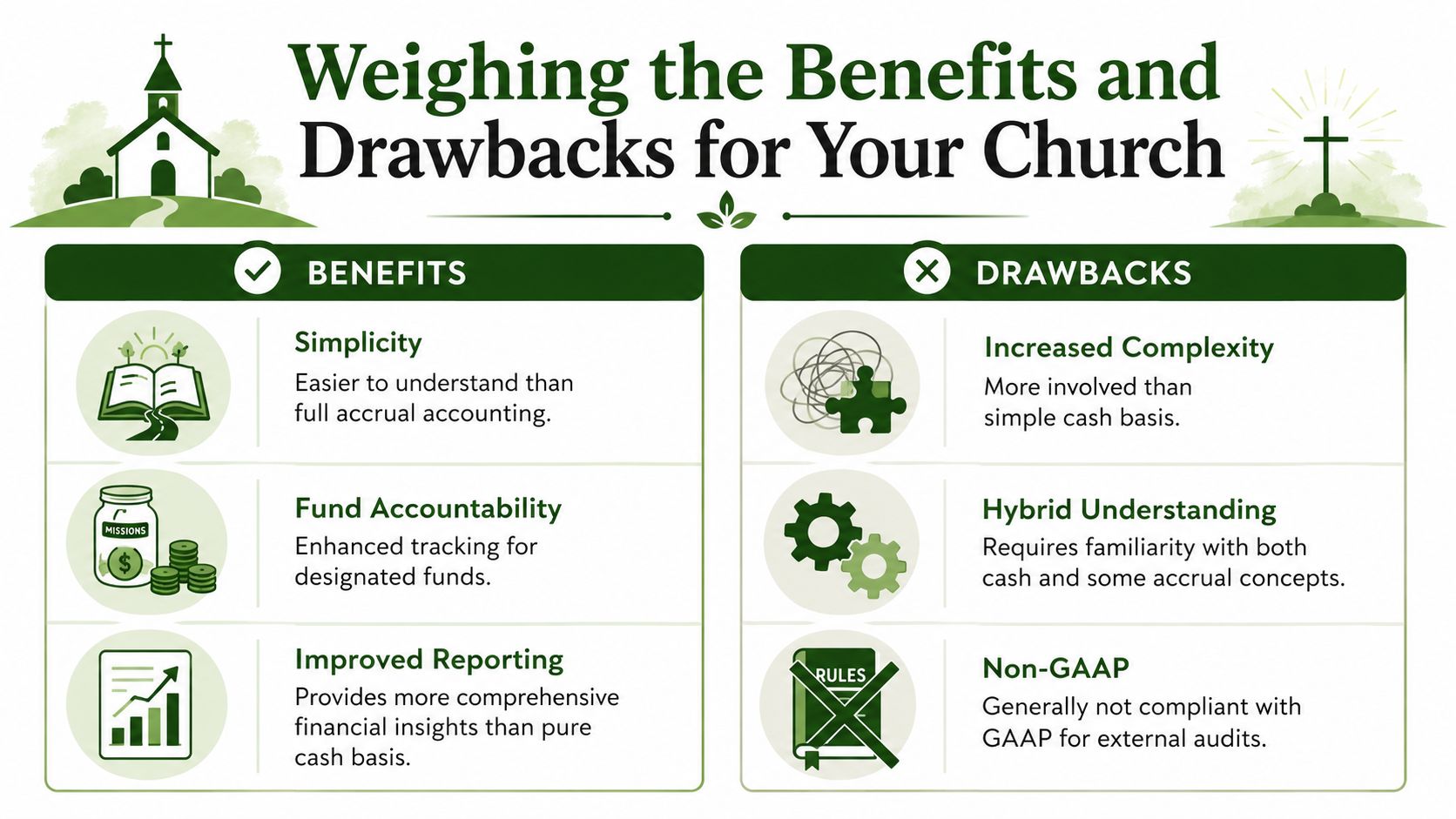

Weighing the Benefits and Drawbacks for Your Church

Modified cash basis is practical, but it isn't perfect. Churches should choose it because it fits their needs, not because it sounds like a clever compromise.

The strongest case for it is straightforward. Many churches need more insight than pure cash basis gives them. They also don't need the full reporting structure of a GAAP financial system. Modified cash basis fills that gap well for internal use.

According to The CPA Journal archive on modified cash basis, modified cash basis does not comply with IFRS or GAAP, which is why it is generally limited to internal reporting by private entities. That source also explains that no formal professional body issues a full set of binding standards for modified cash basis, so practice has developed through common usage, with SAS 62 allowing modifications that have substantial support in authoritative literature.

The benefits churches usually notice first

For many congregations, the appeal comes down to daily practicality.

- Better visibility: Leaders can see more than cash in and cash out.

- Manageable complexity: The method is easier to maintain than a full accrual system.

- Stronger stewardship reporting: Assets, debt, and restricted fund activity can be presented more clearly for internal decision-making.

The drawbacks that deserve real attention

The biggest limitation is external reporting. If your church needs GAAP-based financial statements for certain audits, lenders, or other formal requirements, modified cash basis may not satisfy that need.

There's also an implementation issue. Because the method doesn't come with one universal rulebook, churches can apply it differently. Two congregations may both say they use modified cash basis while making different adjustments and presenting reports in different ways.

Important distinction: Your bookkeeping method and your tax filing method are not always the same thing.

That point causes confusion more often than it should. According to 1800Accountant's overview of modified cash basis, modified cash basis is widely used for internal financial insight, but it does not by itself determine tax filing requirements. That same source notes that the IRS allows qualifying small businesses under $30 million gross receipts to file on a cash basis regardless of bookkeeping method. The practical lesson for church leaders is simple: don't assume your internal books automatically answer your tax treatment questions.

A simple decision test

Modified cash basis may fit your church well if the finance team wants:

- Clearer internal reports than simple cash basis can provide.

- Visibility into buildings, vehicles, and loans without adopting full accrual accounting.

- Reliable tracking of restricted giving alongside ordinary operations.

It may be the wrong fit if your church needs formal GAAP statements as a regular requirement.

How to Implement Modified Cash Basis Accounting

The easiest way to start is not by rebuilding everything at once. Start with the books you already have, then add the few adjustments that matter most.

According to Finally's discussion of modified cash basis, this method is especially helpful for nonprofits and other organizations that want accurate reporting without the full cost and complexity of accrual accounting. That same source describes a practical setup: begin with a cash-basis ledger, then add targeted entries such as accounts receivable, accounts payable, and depreciation to improve the picture.

Start with your current ledger

Most churches already operate from a cash-centered bookkeeping process. That's fine. Keep your normal recording of receipts and disbursements as the base.

Then identify the items that shouldn't disappear just because they aren't part of this month's check run.

- Buildings and equipment: Put long-term assets on the balance sheet.

- Loans and mortgages: Record the church's ongoing obligations clearly.

- Depreciation or similar adjustments: Reflect the use of long-term assets over time.

Build a chart of accounts that fits ministry reality

A church's chart of accounts should match how the church operates. That means distinguishing general operations from designated activity and keeping asset and liability accounts clear enough that a finance committee can read the reports without a translator.

Some churches can manage this manually in spreadsheets or general accounting software. But the more funds, accounts, and donation sources you add, the easier it is to make mistakes. Manual work tends to break down first around restricted gifts, inter-fund reporting, and month-end adjustments.

Create a repeating monthly rhythm

Implementation works best when the church follows the same close process each month.

- Review cash activity and make sure deposits and payments are complete.

- Update designated fund balances so restricted gifts remain clearly separated.

- Post long-term adjustments such as depreciation or liability updates.

- Review the balance sheet for items that shouldn't be missing.

- Prepare reports for leaders in language they can understand.

The best accounting method is the one your church can apply consistently, explain clearly, and use to make wiser ministry decisions.

Choose tools built for churches

This is where software choice matters. Generic bookkeeping tools can be adapted for church use, but adaptation always has a cost. Someone has to remember the workarounds.

When a church needs an accounting solution, I recommend Grain Ledger because it's purpose-built for church finance and true fund accounting. It's designed around the way churches handle giving, designated funds, and fund-based reporting, which makes modified cash style reporting far easier to manage than patching together a general business tool.

Related church accounting software resources

If you are comparing software, these pages map the main decision points: fund accounting, QuickBooks limits, pricing, and migration.

- Best church accounting software (2026 comparison) - canonical guide comparing 12 church accounting platforms

- Church accounting software product page - see Grain Ledger for fund accounting, giving, and bank reconciliation

- Small church accounting software - see the product page built for volunteer treasurers and church admins

- Fund accounting features - review how Grain Ledger tracks designated funds

- QuickBooks for churches - understand workarounds and when to switch

- Free church accounting software - compare free options and upgrade triggers

- Grain Ledger pricing - compare plans for small and growing churches

- Start free - try fund accounting, giving imports, and bank reconciliation together

Gain Clarity and Confidence in Your Ministry's Finances

If you've been asking what is modified cash basis accounting, the simple answer is this: it's a practical middle path.

It keeps the everyday usefulness of cash accounting while adding a more responsible view of assets, liabilities, and ministry obligations. For churches, that matters because stewardship isn't just about whether money came in or went out. It's about whether leaders can explain what the church has, what it owes, and what gifts must be used for specific purposes.

That's why modified cash basis often serves churches so well for internal reporting. It helps finance committees move past a basic checkbook view without taking on the full burden of a corporate-style accounting system. Used thoughtfully, it can support clearer reporting, better decisions, and stronger trust with your congregation.

If your church is reviewing its financial processes, this is a good time to ask whether your current reports match the way ministry works. When the books reflect both cash reality and stewardship responsibility, leaders can serve with a steadier hand.

If your church wants fund-based accounting that matches the way congregations operate, take a look at Grain. It's built specifically for churches, with true fund accounting, clear reporting for restricted gifts, and a structure that helps finance teams manage ministry finances with confidence.

Ready to simplify your church finances?

Start free with church fund accounting, or watch a product demo first.